Download presentation

Presentation is loading. Please wait.

1

Lecture 1: What do we expect? What do we see?

17

Blanchard-Wolfers Unemployment has increase in most European countries since 1975 It was very low before And there is an increased dispersion across European countries

19

The puzzle: Shocks-based explanations do not explain the dispersion – Oil shocks and macro conditions too similar across countries Institutions-based explanations fail to account for the fact that unemployment was low while these institutions were still around

20

The solution Shocks interact with institutions Some institutions are harmless absent shocks But they can increase the magnitude of the unemployment response to the shock And they can increase the persistence of the shock

21

The Pro: it’s plausible Coordination in bargaining better response of wages to a productivity slowdown High duration of benefits More of LTU during a recession More persistence of a shock (as seen)

")

22

The Con: Hard to think of an institution which does not also increase the natural rate. More coordination less negative externalities in wage-setting lower markup of wages on prices less unemployment Longer benefits lower search intensity and greater worker outside option more unemployment

23

The shocks: the medium run A slowdown in TFP growth (why does it affect u?) An increase in the real interest rate (same question) An unexplained and poorly documented fall in labor demand…

An increase in the real interest rate (same question) An unexplained and poorly documented fall in labor demand…")

24

TFP:

26

Real interest rate:

30

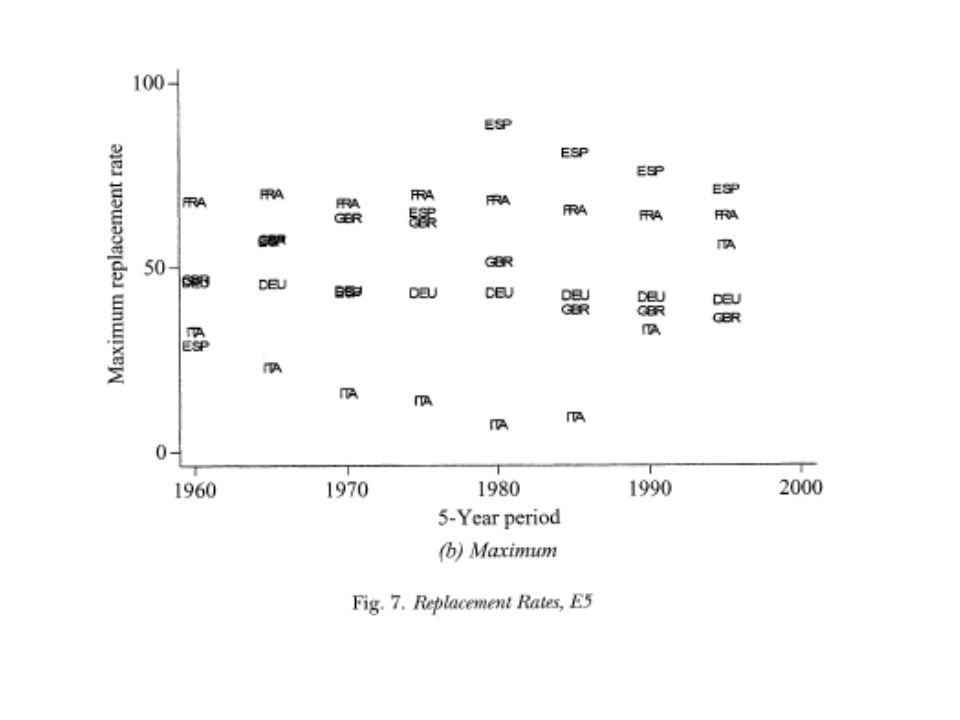

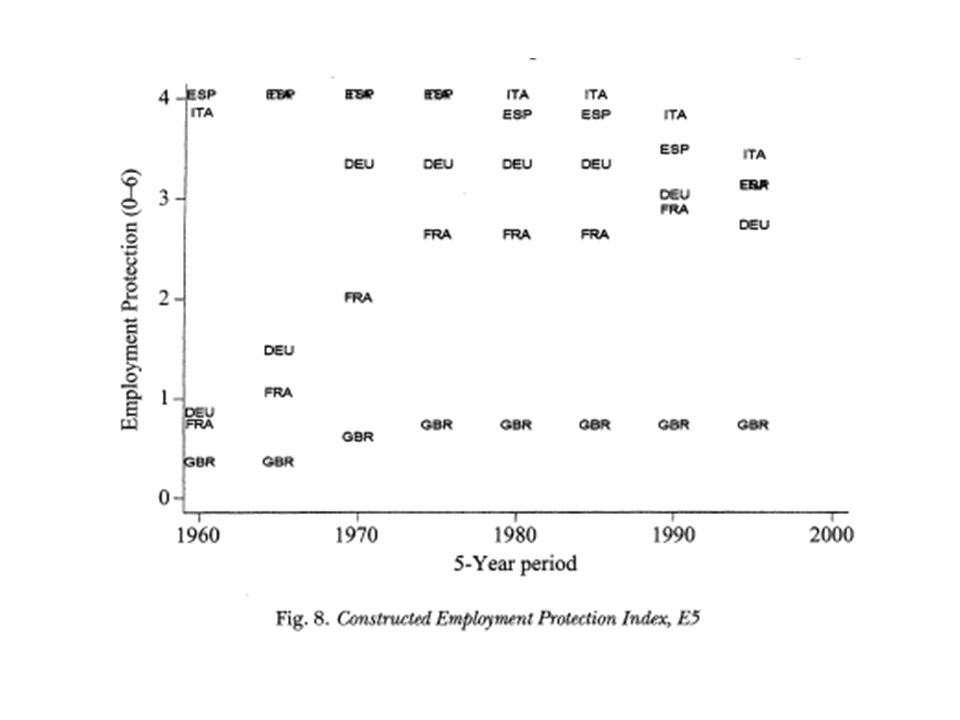

Institutions (their view) UB : Higher unemployment and higher duration EPL: Higher duration, lower inflows, ambiguous effect on employment Taxes: lower wages, lower employment, but little effect on unemployment if « aspirations » adjust proportionally to after- tax wages

UB : Higher unemployment and higher duration EPL: Higher duration, lower inflows, ambiguous effect on employment Taxes: lower wages, lower employment, but little effect on unemployment if « aspirations » adjust proportionally to after- tax wages")

34

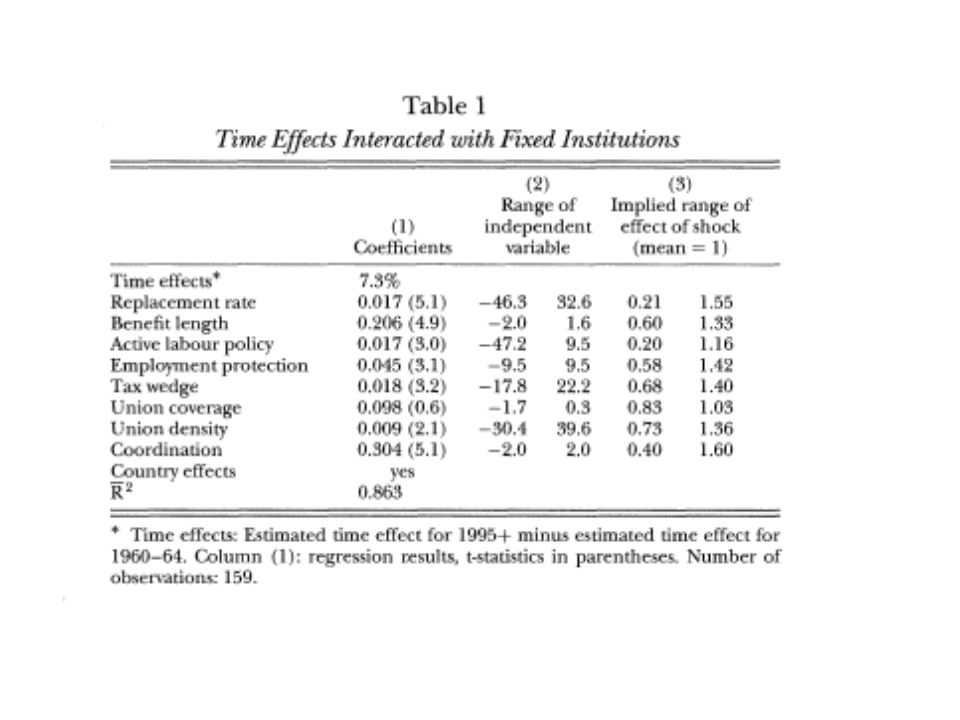

Interactions: Specification #1 We use institutions to explain the change in unemployment rather than its level We use a panel and assume the effect is the same across countries This leads to the following specification (i = country, j = institution)

")

37

Interactions: specification #2 The time dummy is replaced by a vector of country-specific shock The effect of shocks depends on institutions But a given institution has the same effect on all shocks

42

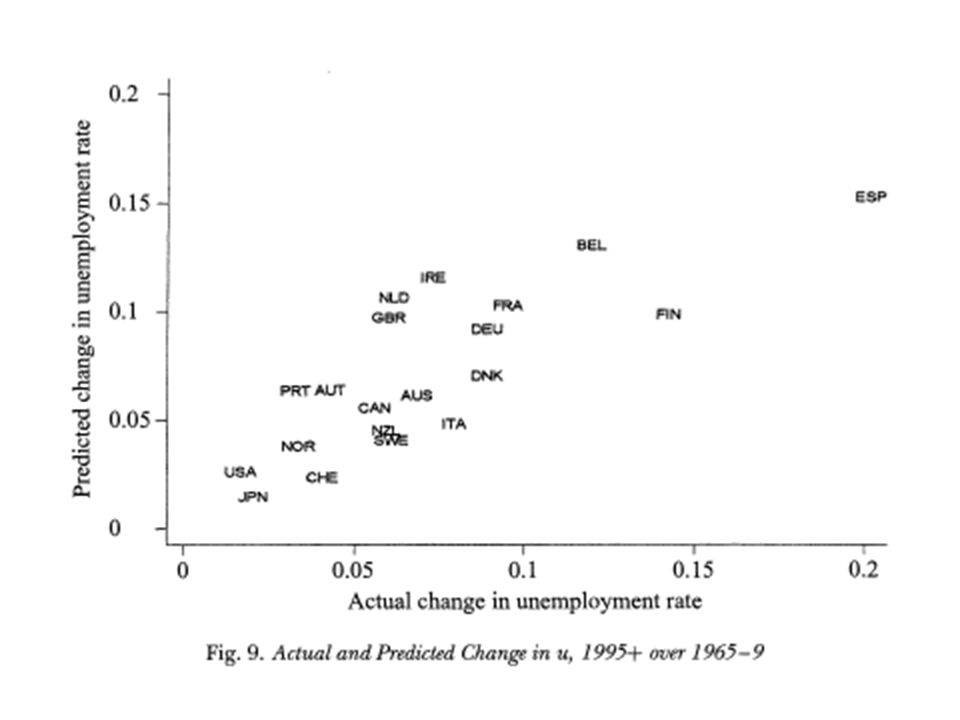

Assessment: It is hard to see why institutions could not matter on their own The authors present no institutions-only exercise If onlys S*I matters, unemployment should go away as shocks are reversed Alternative possibility: multiple equilibrium rates of unemployment

Similar presentations