Download presentation

Presentation is loading. Please wait.

1

Endogenous growth theory III. R and D

2

Where are we? There seems to be convergence to own steady state, although rate is low We expect permanent policy differences to lead to permanent pcGDP differences BUT all countries should grow at the same rate Presumably this is because there is technological diffusion However, we still don’t know what this growth rate is

3

R and D models Technology is produced by an R and D sector The sector is profit-motivated But ideas are non-rival So how can I make profits out of an invention? They can arise from monopoly rents either naturally (trade secrets, barrier to entry), or artificially (Intellectual property)

, or artificially (Intellectual property).")

4

The schumpeterian view Traditional economics states that monopoly is bad But absent monopoly rents there would be no incentives for innovation and entrepreneurship Monopoly is bad statically but good dynamically

5

The hard-core public economics view If ideas are a public good, let us subsidize it or provide them publicly In principle, we could have zero monopoly power and a subsidy to R and D Problem: we can’t define ex-ante what a useful idea is vs. a useless idea We need a market test (although for some authors markets only matter for selection)

.")

6

R and D models of growth Horizontal innovation: we introduce new products that are valued by consumers There is growth in utility terms if not physical output terms Vertical innovation: we introduce new technologies that increase output The two can be combined, and quality innovation can also be introduced

7

What do we need for a model of horizontal innovation? A utility function such that –The number of goods can vary –Product variety is appreciated An innovation sector that introduces new goods Imperfect competition in the goods sector, which creates rents to innovators

8

The Dixit-Stiglitz paradigm

9

Taste for variety Because of concavity, consumers gain by having a greater range of goods and consuming proportionally less The effect is larger, the more the goods are complements If ε<0 the goods are “too complements” and the model does not make sense

11

Embodying DS in a growth model (Grossman-Helpman) At each date t the R and D sector produces new goods The patent owner has monopoly power over the good forever The R and D sector has free entry PDV of future monopoly profits = current R and D cost The only input in the R and D sector is the labour of researchers

At each date t the R and D sector produces new goods The patent owner has monopoly power over the good forever The R and D sector has free entry PDV of future monopoly profits = current R and D cost The only input in the R and D sector is the labour of researchers")

12

Labour Each representative agent is endowed with one unit of labour He can work either in the R and D sector or in the production sector The wage is the same throughout the economy, equal to w t

13

Monopolists Each monopolist at date t, has a CRTS production function Labour is the only input Unit productivity Takes demand function as given, as well as the aggregate price level (atomistic)

")

14

The R and D sector One unit of labour produces γ new goods per unit of time The PDV of monopoly profits from one additional good is equal to its production cost (free entry) The production cost is w t / γ

The production cost is w t / γ")

15

Can we get sustained growth? The increase in the number of goods is γL R For N to grow at a constant rate, so must dN/dt But this is impossible if L R is bounded So we assume that the productivity of R and D is proportional to the number of goods

16

The representative consumer problem

17

The intra-period allocation of consumption Same as in the static Dixit-Stiglitz model Income replaced with total expenditure at t, p t C t

18

Price normalization At any date t, p and w can be multiplied by a small factor and the nominal interest rate adjusted accordingly So we need 1 price normalization per period We pick p t = 1 All values are expressed in terms of units of utility r = real interest rate in aggregate hedonic consumption units

19

The monopoly maximization problem

20

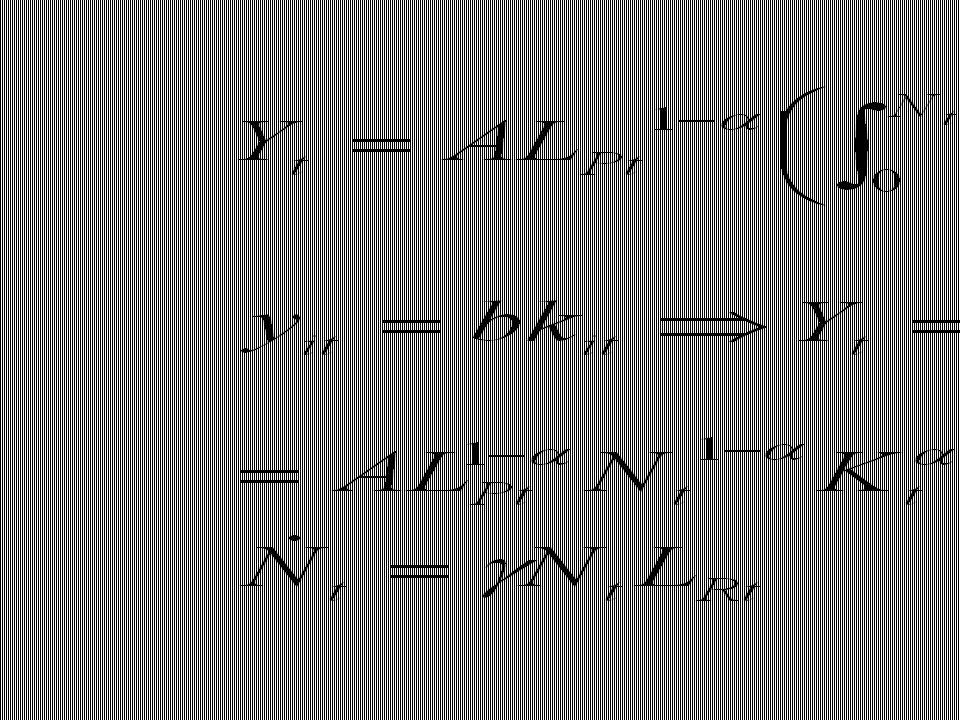

The R and D problem

21

Closing the model

22

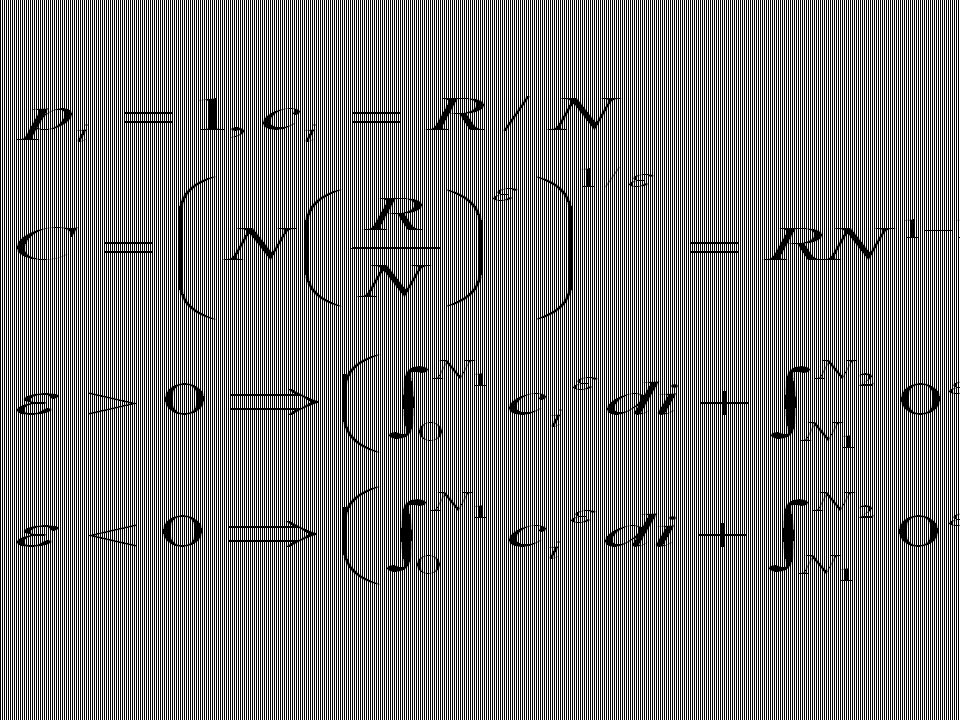

Solving the model: step 1

23

Solving the model, step 2

24

Balanced growth path

25

Growth rate determination r g Intertemporal substitution Innovation

26

An increase in L r g Intertemporal substitution Innovation

27

An increase in ro r g Intertemporal substitution Innovation

28

Welfare analysis Profits are a small fraction of the social value of innovation not enough people in R and D Monopoly markups depress the wage in the production sector too many people in R and D The latter, however, is due to the fact that R and D is the only alternative to production work Finally, more innovation reduces the cost of future innovations

29

Transforming this into a model of productivity growth: the Romer model Differentiated goods are now intermediate inputs into production “taste for variety” more varieties increase productivity Inventing new intermediate goods TFP growth in aggregate production function

31

Scale effects A key prediction of R and D models is that there are scale effects: dg/dL > 0 More people more ideas more growth The number of people engaged in R and D has increased substantially Yet no sign of accelerating growth

33

Where do scale effects come from? The externality in learning costs prevents growth in ideas from falling And this rate goes up with the number of researchers In contrast, if this externality were weaker, L would only have a level effect But trend growth in population would offset decreasing returns to research just like TFP growth offsets decreasing returns to capital!

35

Policy consequences Intellectual property, profitability and subsidies no longer have an effect on long-term growth These policies only have a level effect LT growth only depends on population growth

Similar presentations

, OUP, 2009 M. L. Ahuja, Principles of Microeconomics,>")