Download presentation

Presentation is loading. Please wait.

1

FONASBA Buenos Aries Tanker Chartering Report October 2007

2

Tanker Market Decline 2005-20072006-2007 BDTI- 60%- 46% BCTI- 61%-45%

3

Baltic Dirty Tanker Index January 2005-October 2007

4

Baltic Clean Tanker Index January 2005-October 2007

6

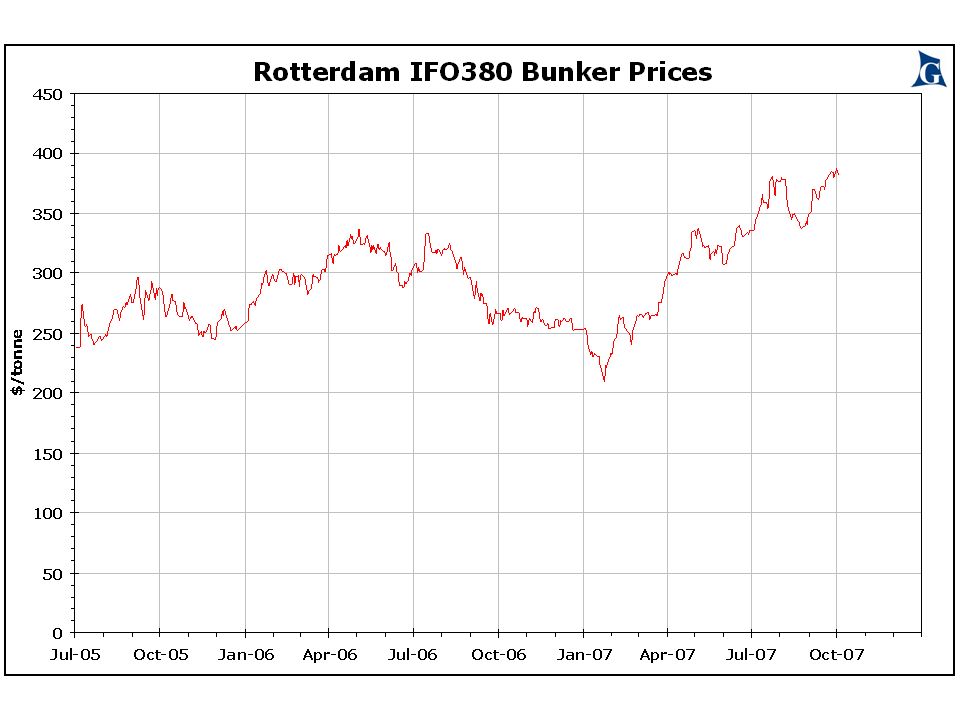

Tanker Chartering Report Bunker Prices in Rotterdam Rose from $240 to $390 per tonne Plus 62.5%

7

Tanker Chartering Report Global Oil Demand up 0.8% yoy Global Oil Demand up 0.8% yoy Forecast +1.5m b/d 2007 Forecast +1.5m b/d 2007 +2.2m b/d 2008 +2.2m b/d 2008 Oil Price $80/bbl July 07 Oil Price $80/bbl July 07

8

Tanker Chartering Report Mild winter in N hemisphere Benign hurricane season N America Decline of OPEC oil on water Refinery maintenance

9

Tanker Chartering Report China + 4.6% yoy driven by China + 4.6% yoy driven by Car ownership + 16% yoy air travel constructionagriculturepetrochemicals oil stocks

10

Tanker Chartering Report Oil Demand India+5.6% North America+1.7% Japan-10.5% Europe-3.4%

11

Tanker Chartering Report Clean Tanker Trades Clean Tanker Trades Comparatively buoyant Refinery problems in the Atlantic basin. Nigeria and USA importing from Europe Congestion in both discharge areas India increasingly a supplier to Europe and Asia

12

Tanker Chartering Report Growth of tanker fleet 3.6% dwt in first Growth of tanker fleet 3.6% dwt in first 8 months of 2007 8 months of 2007 Fleet removals started in an interesting way over 30 single hull VLCCs converting to FPSO or VLOCs Fleet removals started in an interesting way over 30 single hull VLCCs converting to FPSO or VLOCs Double Hull Fleet = 74% of existing fleet Double Hull Fleet = 74% of existing fleet

13

Tanker Chartering Report LNG continues to grow + 11% y o y LNG continues to grow + 11% y o y Korea + 12.6% Japan+ 1.3% Spain+ 2.3 m t UK+ 2.2 m t Belgium+ 1.2 m t Existing fleet 233 vsls + 11% y o y

14

Tanker Chartering Report Future influences (Short Term): Future influences (Short Term):AlternativeSuppliersFuels Response to Green Issues / emissions

: Future influences (Short Term):AlternativeSuppliersFuels Response to Green Issues / emissions")

15

Tanker Chartering Report Future influences (long term): Future influences (long term): 15 years/+ end of production from the largest fields found in last 40 yrs: 15 years/+ end of production from the largest fields found in last 40 yrs: North Sea AlaskaSakhalin

: Future influences (long term): 15 years/+ end of production from the largest fields found in last 40 yrs: 15 years/+ end of production from the largest fields found in last 40 yrs: North Sea AlaskaSakhalin")

16

Tanker Chartering Report Future influences (Long Term): Future influences (Long Term): Current finds are smaller capacity – indicating maintenance of high oil price = $ ??? or no return to low oil price = $ 20

17

Tanker Market THEEND BEGINS ?

Similar presentations