Download presentation

Presentation is loading. Please wait.

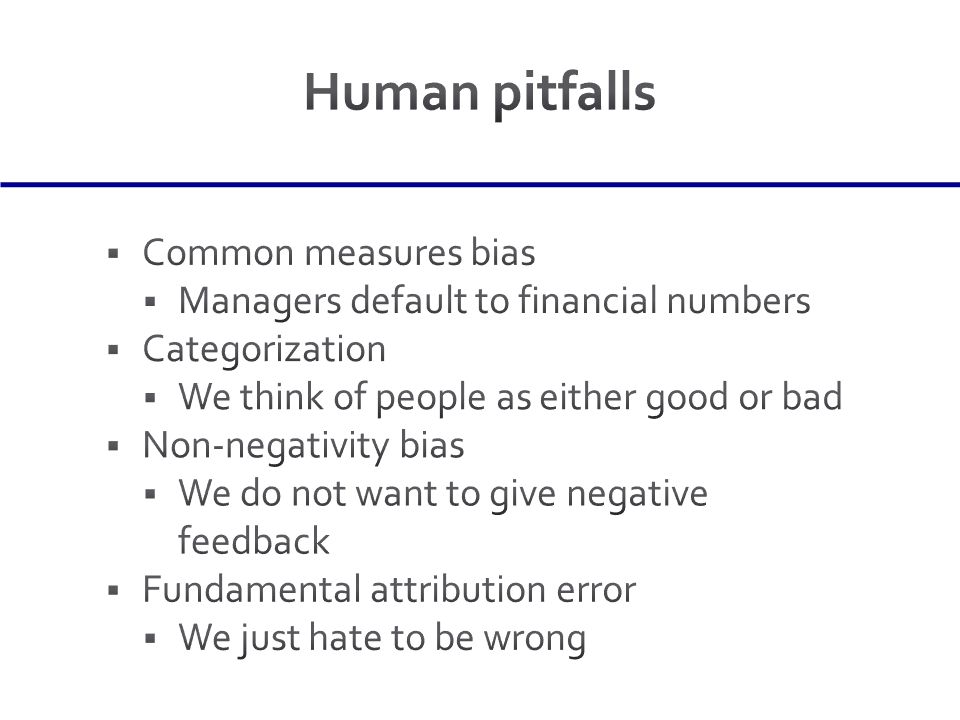

1

Incentives and BSC Managerial Accounting David Fender

14

What are you likely to see earlier? Parts not fitting of a car coming down production line Warranty claims

17

Are often leading indicators of financial performance (relevance is high) Are often leading indicators of financial performance (relevance is high) Are often more actionable Are often more actionable

Are often leading indicators of financial performance (relevance is high) Are often more actionable Are often more actionable")

23

Financial GoalsMeasures Internal GoalsMeasures Innovation GoalsMeasures Customer GoalsMeasures Customer Perspective: How should we look to our customers? Innovation & Learning Perspective: How can we continue to improve and create value? Internal Business Perspective: What must we excel at? Financial Perspective: How should we look to our shareholders? Bob Kaplan Harvard Business School

31

Performance measures Strategy

33

The balanced scorecard lays out concrete actions to attain desired outcomes. A balanced scorecard should have measures that are linked together on a cause-and-effect basis. If we improve one performance measure... Another desired performance measure will improve. Then

36

Source: C. Ittner, 2003 AIMA Conference *Gates, Aligning Strategic Performance Measures and Results

37

Employee skills in installing options Number of options available Time to install option Customer satisfaction with options Number of cars sold Contribution per car Profit Learning and Growth Internal Business Processes Customer Financial

38

Employee skills in installing options Number of options available Time to install option Customer satisfaction with options Number of cars sold Contribution per car Profit Increase Options Time Decreases Strategies Satisfaction Increases Increase Skills Results

39

Employee skills in installing options Number of options available Time to install option Customer satisfaction with options Number of cars sold Contribution per car Profit Satisfaction Increases Results Cars sold Increase

40

Employee skills in installing options Number of options available Time to install option Customer satisfaction with options Number of cars sold Contribution per car Profit Results Time Decreases Contribution Increases Satisfaction Increases

41

Employee skills in installing options Number of options available Time to install option Customer satisfaction with options Number of cars sold Contribution per car Profit Results Contribution Increases Profits Increase If number of cars sold and contribution per car increase, profits increase. Cars Sold Increases

44

Effective managerial accounting systems must reflect the value-creating activities of companies: in operations, in marketing and sales, and in product and process development… (Kaplan, 1985)

")

Similar presentations

>")