Download presentation

Presentation is loading. Please wait.

1

Trading the Risk: Financialisation, Loyalty and Emerging Market Government Policy Autonomy Iain Hardie University of Edinburgh

2

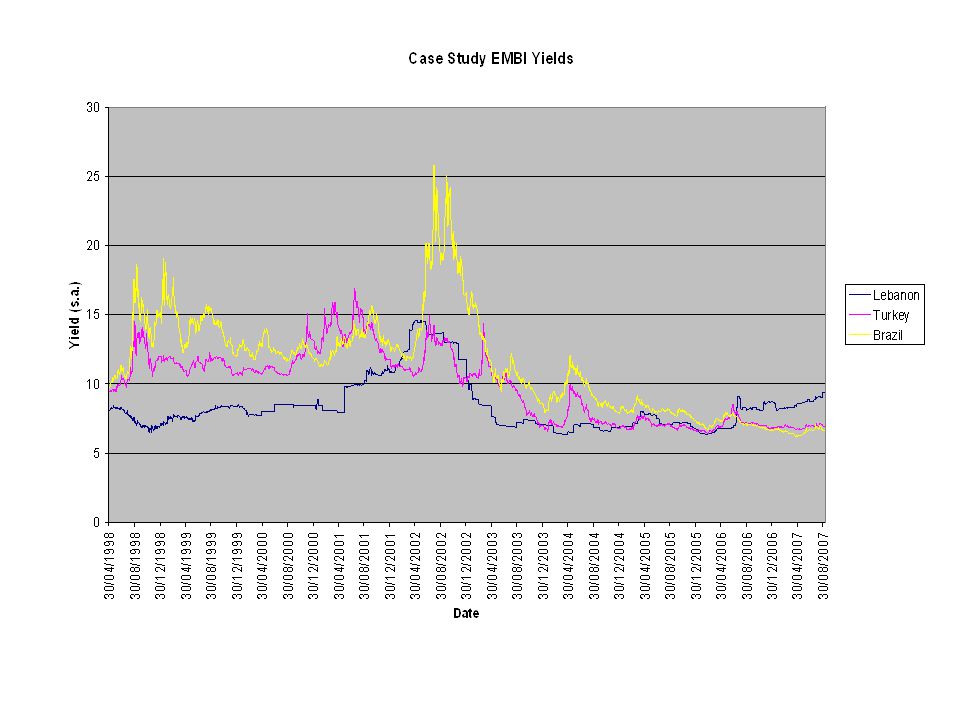

For years now, Lebanon has been able to sustain a government debt-to-GDP ratio which is well beyond levels deemed sustainable (IMF 2006)

")

3

Debt-to-GDP Ratios Selected Countries (2005) Japan 176.0 Lebanon 174.6 Greece 107.5 Italy 106.4 United States 69.9 Brazil 67.3 Turkey 58.0 China 12.5 Estonia 4.8

Japan Lebanon Greece Italy United States 69.9 Brazil 67.3 Turkey 58.0 China 12.5 Estonia 4.8")

4

The Ability to Borrow Matters to Governments Borrowing enhances Government capacity to spend without raising revenue

5

The Ability to Borrow Matters to Governments Borrowing enhances Government capacity to spend without raising revenue a crucial advantage enjoyed by the United States [during the Cold War] was the ability to finance increased arms spending by selling bonds to the public (Ferguson 2001: 406)

![The Ability to Borrow Matters to Governments Borrowing enhances Government capacity to spend without raising revenue a crucial advantage enjoyed by the United States [during the Cold War] was the ability to finance increased arms spending by selling bonds to the public (Ferguson 2001: 406)](http://images.slideplayer.com/6/1618992/slides/slide_5.jpg "The Ability to Borrow Matters to Governments Borrowing enhances Government capacity to spend without raising revenue a crucial advantage enjoyed by the United States [during the Cold War] was the ability to finance increased arms spending by selling bonds to the public (Ferguson 2001: 406)")

6

The Ability to Borrow Matters to Governments Borrowing enhances Government capacity to spend without raising revenue a crucial advantage enjoyed by the United States [during the Cold War] was the ability to finance increased arms spending by selling bonds to the public (Ferguson 2001: 406) Eventually the debt would have to be repaid. For a politician, however, eventually is a long time, certainly farther in the future than the next election (Frieden 2006: 381)

![The Ability to Borrow Matters to Governments Borrowing enhances Government capacity to spend without raising revenue a crucial advantage enjoyed by the United States [during the Cold War] was the ability to finance increased arms spending by selling bonds to the public (Ferguson 2001: 406) Eventually the debt would have to be repaid.](http://images.slideplayer.com/6/1618992/slides/slide_6.jpg "For a politician, however, eventually is a long time, certainly farther in the future than the next election (Frieden 2006: 381).")

7

Who Governments Borrow From Matters Why does anyone want to buy [the bonds of] a government which is allocating…all its revenues on interest payments?...Its a Ponzi scheme (Fund manager, London, interviewed 18 October 2005) Need to understand the sources of government financing: Who Buys Bonds?

![Who Governments Borrow From Matters Why does anyone want to buy [the bonds of] a government which is allocating…all its revenues on interest payments ...Its a Ponzi scheme (Fund manager, London, interviewed 18 October 2005) Need to understand the sources of government financing: Who Buys Bonds](http://images.slideplayer.com/6/1618992/slides/slide_7.jpg "Who Governments Borrow From Matters Why does anyone want to buy [the bonds of] a government which is allocating…all its revenues on interest payments ...Its a Ponzi scheme (Fund manager, London, interviewed 18 October 2005) Need to understand the sources of government financing: Who Buys Bonds")

8

Governments Want to Borrow Without Conditionality Bond Borrowing Does Not Impose Direct Conditionality (as IMF) But: In the sovereign debt market, national governments borrow funds in order to compensate for revenue shortfalls or to fulfil other economic management objectives…those interest rates represent the governments financing costs. When market participants punish governments, they do so by increasing the interest rates at which they will purchase government securities (Mosley 2003).

..")

9

I used to think if there was reincarnation, I wanted to come back as the President or the Pope or a.400 baseball hitter. But now I want to come back as the bond market. You can intimidate everyone (James Carville, Bill Clinton campaign strategist).

..")

10

The Issues How much can governments borrow sustainably? To what extent do governments, in order to borrow, have to follow the policy preferences of bond market investors?

12

John Zysman (1983), Governments, Markets, and Growth the structure of finance contributes to the states capacity to act in the economy But: Contrast is between financing that is: (1) capital- market based; (2) credit-based with government- administered prices; and (3) credit-based dominated by financial institutions (1) US and UK; (2) France and Japan; and (3) West Germany

, Governments, Markets, and Growth the structure of finance contributes to the states capacity to act in the economy But: Contrast is between financing that is: (1) capital- market based; (2) credit-based with government- administered prices; and (3) credit-based dominated by financial institutions (1) US and UK; (2) France and Japan; and (3) West Germany")

13

Furthermore: Zysman assumes a static financial structure. Need to analyse change. Need for study of ever more elaborate financial markets So: Financial systems need disaggregating and their analysis needs updating

14

Differentiating Financial Market Actors Consider Domestic and Foreign Investors Together

15

Differentiating Financial Market Actors Consider Domestic and Foreign Investors Together Consider Banks, Individuals, Pension Funds, Mutual Funds, Hedge Funds

16

Differentiating Financial Market Actors Consider Domestic and Foreign Investors Together Consider Banks, Individuals, Pension Funds, Mutual Funds, Hedge Funds Key Variable is Loyalty Linked to the Ability to Exit (Hirschman 1970)

")

17

Financialisation Ability to Exit is Linked to the Ability to Trade Risk: Financialisation Financialisation = The Ability to Trade Risk (Aglietta and Breton 2001)

")

18

Financialisation Ability to Exit is Linked to the Ability to Trade Risk: Financialisation Financialisation = The Ability to Trade Risk (Aglietta and Breton 2001) The Ability to Trade Risk is a function of the financialisation of a financial market actor and the financialisation of the market structure

The Ability to Trade Risk is a function of the financialisation of a financial market actor and the financialisation of the market structure")

19

Examples of Differential Investor Loyalty Time Scale of Investment: my 30 year bonds will never come back within the next 30 years (Assistant General Manager, 50 per cent foreign-owned Turkish bank, interviewed 8 December 2005)

")

20

Examples of Differential Investor Loyalty Time Scale of Investment: my 30 year bonds will never come back within the next 30 years (Assistant General Manager, 50 per cent foreign-owned Turkish bank, interviewed 8 December 2005) this position that Ive kept is three weeks old…thats a long time...Nobody buys and keeps things for six months, a year, I mean things change (Hedge fund manager, London, interviewed 23 June 2005)

this position that Ive kept is three weeks old…thats a long time...Nobody buys and keeps things for six months, a year, I mean things change (Hedge fund manager, London, interviewed 23 June 2005)")

21

Examples of Differential Investor Loyalty Time Scale of Investment: my 30 year bonds will never come back within the next 30 years (Assistant General Manager, 50 per cent foreign-owned Turkish bank, interviewed 8 December 2005) this position that Ive kept is three weeks old…thats a long time...Nobody buys and keeps things for six months, a year, I mean things change (Hedge fund manager, London, interviewed 23 June 2005) locals are…really…looking for what is going to happen tomorrow or next week. 95 per cent of the locals think like this (proprietary trader, Brazilian bank, interviewed 29 August 2006).

..")

22

Examples of Differential Investor Loyalty Disloyalty: I cant act like a hedge fund... I cant…[sell short when Turkey is hit by an earthquake], the hedge fund can do that, and he wouldnt care less if the news on the Turkish papers, saying that they have shorted the market after the earthquake...I cant do that, Im a real bank, I got…close to 5 million credit cards. I'm working with nearly every corporate in Turkey, somehow, on either a credit or a transaction basis…[R]eputation means a lot to me. I have much more good will in my corporate valuation than [a leading international hedge fund] (Deputy General Manager, Turkish bank, interviewed 5 December 2005)

.")

23

Examples of Differential Investor Loyalty Disloyalty: I cant act like a hedge fund... I cant…[sell short when Turkey is hit by an earthquake], the hedge fund can do that, and he wouldnt care less if the news on the Turkish papers, saying that they have shorted the market after the earthquake...I cant do that, Im a real bank, I got…close to 5 million credit cards. I'm working with nearly every corporate in Turkey, somehow, on either a credit or a transaction basis…[R]eputation means a lot to me. I have much more good will in my corporate valuation than [a leading international hedge fund] (Deputy General Manager, Turkish bank, interviewed 5 December 2005) If I would think that in order to make money I would have to go short, I would go short, and…in my mind still my first job is still as a prop trader rather than a bank partner and thats how it works. So my compensation has little to do with the bank result (proprietary trader, Brazilian bank, interviewed 29 August 2006).

If I would think that in order to make money I would have to go short, I would go short, and…in my mind still my first job is still as a prop trader rather than a bank partner and thats how it works. So my compensation has little to do with the bank result (proprietary trader, Brazilian bank, interviewed 29 August 2006)..")

24

Examples of Differential Investor Loyalty Financing the Government: at least I have to keep…what I already have with the government...and if the government...needs some money, I have to give it (Executive Advisor to Chairman, Lebanese bank, interviewed 8 September 2005) If you want to do something drastic you have to keep in mind that its going to…have an impact on all the rest of your portfolio and assets (Head of Treasury, Turkish bank, interviewed 7 December 2005)

If you want to do something drastic you have to keep in mind that its going to…have an impact on all the rest of your portfolio and assets (Head of Treasury, Turkish bank, interviewed 7 December 2005)")

25

Examples of Differential Investor Loyalty Performance Measurement: I believe…in free markets but you want to also act as a central banker…your business dictates that you want to make profit but not necessarily short term profit or fees, profit in the long term (Head of Treasury, Lebanese bank, interviewed 9 September 2005)

")

26

Examples of Differential Investor Loyalty Performance Measurement: I believe…in free markets but you want to also act as a central banker…your business dictates that you want to make profit but not necessarily short term profit or fees, profit in the long term (Head of Treasury, Lebanese bank, interviewed 9 September 2005) the fact that it[Brazil]s a big part of the index mean that a lot of people need to own it, in big amounts (hedge fund manager, London, interviewed 23 June 2005)

![Examples of Differential Investor Loyalty Performance Measurement: I believe…in free markets but you want to also act as a central banker…your business dictates that you want to make profit but not necessarily short term profit or fees, profit in the long term (Head of Treasury, Lebanese bank, interviewed 9 September 2005) the fact that it[Brazil]s a big part of the index mean that a lot of people need to own it, in big amounts (hedge fund manager, London, interviewed 23 June 2005)](http://images.slideplayer.com/6/1618992/slides/slide_26.jpg "Examples of Differential Investor Loyalty Performance Measurement: I believe…in free markets but you want to also act as a central banker…your business dictates that you want to make profit but not necessarily short term profit or fees, profit in the long term (Head of Treasury, Lebanese bank, interviewed 9 September 2005) the fact that it[Brazil]s a big part of the index mean that a lot of people need to own it, in big amounts (hedge fund manager, London, interviewed 23 June 2005)")

27

Examples of Differential Investor Loyalty Performance Measurement: I believe…in free markets but you want to also act as a central banker…your business dictates that you want to make profit but not necessarily short term profit or fees, profit in the long term (Head of Treasury, Lebanese bank, interviewed 9 September 2005) the fact that it[Brazil]s a big part of the index mean that a lot of people need to own it, in big amounts (hedge fund manager, London, interviewed 23 June 2005) If your investor base doesnt care about month to month P&L…, then you dont worry about your stop losses because if you have a right call its going to take 12 months to play out…, you dont really care… Now investors who we have they want a weekly update on the P&L (hedge fund manager, New York, interviewed 15 May 2006)

![Examples of Differential Investor Loyalty Performance Measurement: I believe…in free markets but you want to also act as a central banker…your business dictates that you want to make profit but not necessarily short term profit or fees, profit in the long term (Head of Treasury, Lebanese bank, interviewed 9 September 2005) the fact that it[Brazil]s a big part of the index mean that a lot of people need to own it, in big amounts (hedge fund manager, London, interviewed 23 June 2005) If your investor base doesnt care about month to month P&L…, then you dont worry about your stop losses because if you have a right call its going to take 12 months to play out…, you dont really care… Now investors who we have they want a weekly update on the P&L (hedge fund manager, New York, interviewed 15 May 2006)](http://images.slideplayer.com/6/1618992/slides/slide_27.jpg "Examples of Differential Investor Loyalty Performance Measurement: I believe…in free markets but you want to also act as a central banker…your business dictates that you want to make profit but not necessarily short term profit or fees, profit in the long term (Head of Treasury, Lebanese bank, interviewed 9 September 2005) the fact that it[Brazil]s a big part of the index mean that a lot of people need to own it, in big amounts (hedge fund manager, London, interviewed 23 June 2005) If your investor base doesnt care about month to month P&L…, then you dont worry about your stop losses because if you have a right call its going to take 12 months to play out…, you dont really care… Now investors who we have they want a weekly update on the P&L (hedge fund manager, New York, interviewed 15 May 2006)")

28

Examples of Differential Investor Loyalty Financialisation of Market Structure: Unfortunately when I want to sell Treasury papers because of a certain political issue, everybody is selling so there is no market (Deputy General Manager, Lebanese bank, interviewed 2 September 2005) you cannot imagine a big bank unloading its securities portfolio into the market. Thats not possible (Deputy General Manager, Turkish bank, interviewed 5 December 2005) A local derivatives market would…fundamentally change the way Im running my portfolio (Deputy General Manager, Turkish bank, interviewed 5 December 2005)

A local derivatives market would…fundamentally change the way Im running my portfolio (Deputy General Manager, Turkish bank, interviewed 5 December 2005).")

29

The Autonomy Curve Financialisation Government Policy Autonomy Domestic Banks Domestic Individuals Domestic Pension Funds Domestic Mutual Funds Domestic Hedge Funds International Hedge Funds/ Total Return Investors International Mutual Funds/ Index Following Investors Each different investor type is placed on the autonomy curve based on their financialisation and influence on the financialisation of the government bond market

30

Movement Along the Curve: The Changing Ability to Trade Risk 1. Financialisation of Market Structure Regulation New Financial Instruments Introduced Primary Dealer System Size of Market / Individual Bonds

31

Movement Along the Curve: The Changing Ability to Trade Risk 2. Financialisation of Market Actors Regulation Performance Measurement Transaction Costs (Size of Investor) Nature of Investment (Long-Term/Short- Term, Leverage, Disloyalty) Investment Mandates Ease of Full Exit

Nature of Investment (Long-Term/Short- Term, Leverage, Disloyalty) Investment Mandates Ease of Full Exit.")

32

The Height of the Curve Government Borrowing Requirement (but Relative to the Capacity of the Most Loyal Investors to Provide Financing) Relative Strength of Push and Pull Factors Absolute Strength of Push Factors Credit Ratings Technology Size of Economy

Relative Strength of Push and Pull Factors Absolute Strength of Push Factors Credit Ratings Technology Size of Economy")

33

Each Countrys Overall Autonomy Financialisation Government Policy Autonomy · Lebanon · Brazil · Turkey

34

Conclusions To borrow without following investor policy preferences, governments must borrow from loyal investors Investor loyalty is linked to the financialisation of government bond market structure and different market actors

Similar presentations

Households Firms Government Foreigners Financial Markets.>")

and borrowers.>")

from savers (suppliers) to investors.>")