Download presentation

Presentation is loading. Please wait.

1

GESTIÓN BANCARIA Master en Banca y Finanzas Cuantitativas (QF), 2008

Santiago Carbó Valverde Universidad de Granada

3

Santiago Carbó Valverde

Universidad de Granada Materiales docentes en:

4

Esquema de trabajo: Transparencias en inglés

Presentaciones de papers en clase Examen final Referencia básica: - SAUNDERS, A. Y M.M. CORNETT (2000): FINANCIAL INSTITUTIONS MANAGEMENT: A MODERN PERSPECTIVE, 4ª EDICIÓN, MCGRAW HILL, NEW YORK, ESTADOS UNIDOS. - SINKEY, J. (2001): COMMERCIAL BANK FINANCIAL MANAGEMENT, SEXTA EDICIÓN, PRENTICE HALL, NEW YORK, ESTADOS UNIDOS.

: FINANCIAL INSTITUTIONS MANAGEMENT: A MODERN PERSPECTIVE, 4ª EDICIÓN, MCGRAW HILL, NEW YORK, ESTADOS UNIDOS. - SINKEY, J. (2001): COMMERCIAL BANK FINANCIAL MANAGEMENT, SEXTA EDICIÓN, PRENTICE HALL, NEW YORK, ESTADOS UNIDOS.")

5

(LECTURA DE REFERENCIA: BHATTACHARYA Y THAKOR, 1993)

Tema 1 LA INDUSTRIA DE SERVICIOS FINANCIEROS: LAS ENTIDADES DE DEPÓSITO (LECTURA DE REFERENCIA: BHATTACHARYA Y THAKOR, 1993)

")

6

Why study Financial Markets and Institutions?

They are the cornerstones of the overall financial system in which financial managers operate Individuals use both for investing Corporations and governments use both for financing

7

Overview of Financial Markets

Primary Markets versus Secondary Markets Money Markets versus Capital Markets Foreign Exchange Markets

8

Primary Markets versus Secondary Markets

markets in which users of funds (e.g. corporations, governments) raise funds by issuing financial instruments (e.g. stocks and bonds) Secondary Markets markets where financial instruments are traded among investors (e.g. Bolsa Madrid, NYSE, NASDAQ)

raise funds by issuing financial instruments (e.g. stocks and bonds) Secondary Markets. markets where financial instruments are traded among investors (e.g. Bolsa Madrid, NYSE, NASDAQ)")

9

Money Markets versus Capital Markets

markets that trade debt securities with maturities of one year or less (e.g. Spanish Government bonds, U.S. Treasury bills) Capital Markets markets that trade debt (bonds) and equity (stock) instruments with maturities of more than one year

Capital Markets. markets that trade debt (bonds) and equity (stock) instruments with maturities of more than one year.")

10

Money Market Instruments Outstanding, 1990-1999 ($Bn)

")

11

Capital Market Instruments Outstanding, 1990-1999 ($Bn)

")

12

Foreign Exchange Markets

“FX” markets deal in trading one currency for another (e.g. dollar for yen) The “spot” FX transaction involves the immediate exchange of currencies at the current exchange rate The “forward” FX transaction involves the exchange of currencies at a specified date in the future and at a specified exchange rate

The spot FX transaction involves the immediate exchange of currencies at the current exchange rate. The forward FX transaction involves the exchange of currencies at a specified date in the future and at a specified exchange rate.")

13

Overview of Financial Institutions (FIs)

Institutions that perform the essential function of channeling funds from those with surplus funds to those with shortages of funds (e.g. banks, thrifts, insurance companies, securities firms and investment banks, finance companies, mutual funds, pension funds)

")

14

Flow of Funds in a World without FIs: Direct Transfer

Financial Claims (Equity and debt instruments) Suppliers of Funds (Households) Users of Funds (Corporations) Cash Example: A firm sells shares directly to investors without going through a financial institution

Suppliers of Funds. (Households) Users of Funds. (Corporations) Cash. Example: A firm sells shares directly to investors without going. through a financial institution.")

15

Flow of Funds in a world with FIs: Indirect transfer

(Brokers) (Asset transformers) Users of Funds Suppliers of Funds Financial Claims (Equity and debt securities) Financial Claims (Deposits and Insurance policies)

(Asset. transformers) Users of Funds. Suppliers of Funds. Financial Claims. (Equity and debt securities) Financial Claims. (Deposits and Insurance policies)")

16

Types of FIs Commercial banks

depository institutions whose major assets are loans and major liabilities are deposits Thrifts and savings banks depository institutions in the form of savings banks, savings and loans, credit unions, credit cooperatives Insurance companies financial institutions that protect individuals and corporations from adverse events (continued)

")

17

Securities firms and investment banks

financial institutions that underwrite securities and engage in securities brokerage and trading Finance companies financial institutions that make loans to individuals and businesses Mutual Funds financial institutions that pool financial resources and invest in diversified portfolios Pension Funds financial institutions that offer savings plans for retirement

18

Services Performed by Financial Intermediaries

Monitoring Costs aggregation of funds provides greater incentive to collect a firm’s information and monitor actions Liquidity and Price Risk provide financial claims to savers with superior liquidity and lower price risk (continued)

")

19

Transaction Cost Services

transaction costs are reduced through economies of scale Maturity Intermediation greater ability to bear risk of mismatching maturities of assets and liabilities Denomination Intermediation allow small investors to overcome constraints imposed to buying assets imposed by large minimum denomination size

20

Services Provided by FIs Benefiting the Overall Economy

Money Supply Transmission Depository institutions are the conduit through which monetary policy actions impact the economy in general Credit Allocation often viewed as the major source of financing for a particular sector of the economy (e.g. farming and real estate) (continued)

(continued)")

21

Services Provided by FIs Benefiting the Overall Economy

Intergenerational Wealth Transfers life insurance companies and pension funds provide savers with the ability to transfer wealth from one generation to the next Payment Services efficiency with which depository institutions provide payment services directly benefits the economy

22

Risks Faced by Financial Institutions

Interest Rate Risk Foreign Exchange Risk Market Risk Credit Risk Liquidity Risk Off-Balance-Sheet Risk Technology Risk Operation Risk Country or Sovereign Risk Insolvency Risk

23

Regulation of Financial Institutions

FIs provide vital financial services to all sectors of the economy; therefore, their regulation is in the public interest In an attempt to prevent their failure and the failure of financial markets overall

24

Globalization of Financial Markets and Institutions

Financial Markets became more global as the value of stocks traded in foreign markets soared Foreign bond markets have served as a major source of international capital Globalization also evident in the derivative securities market

25

Factors Leading to Significant Growth in Foreign Markets

The pool of savings from foreign investors has increased International investors have turned to U.S. and other markets to expand their investment opportunities Information on foreign investments and markets is now more accessible (e.g. internet) Some mutual funds allow ability to invest in foreign securities with low transaction costs Deregulation has enhanced globalization of capital flows

Some mutual funds allow ability to invest in foreign securities with low transaction costs. Deregulation has enhanced globalization of capital flows.")

26

(LECTURA DE REFERENCIA: ALLEN Y SANTOMERO (1997)

Tema 2 ¿POR QUÉ SON ESPECIALES LOS INTERMEDIARIOS BANCARIOS? (LECTURA DE REFERENCIA: ALLEN Y SANTOMERO (1997)

")

27

Why Are Financial Intermediaries Special?

Objectives: Develop the tools needed to measure and manage the risks of FIs. Explain the special role of FIs in the financial system and the functions they provide. Explain why the various FIs receive special regulatory attention. Discuss what makes some FIs more special than others.

28

Without FIs Households (net savers) Corporations (net borrowers)

Cash Equity & Debt Corporations (net borrowers)

")

29

FIs’ Specialness Without FIs: Low level of fund flows.

Information costs: Economies of scale reduce costs for FIs to screen and monitor borrowers Less liquidity Substantial price risk

30

Deposits/Insurance Policies

With FIs Cash Households Corporations Equity & Debt FI (Brokers) (Asset Transformers) Deposits/Insurance Policies

(Asset Transformers) Deposits/Insurance Policies.")

31

Financial Structure Puzzles: a way to explain the role of FIs

stocks are not the most important source of external financing for businesses issuing debt and equity is not the main way that businesses finance operations indirect financing is more important than direct financing banks are the most important source of external funds for businesses financial industry is one of the most heavily regulated industries only large, well-known firms have access to the securities markets collateral is an important part of debt contracts for businesses and households debt contracts are complex and often contain many restrictions for the borrower

32

Transaction Costs information and other transaction costs in financial system can be substantial How do transaction costs affect investing? How can financial intermediaries reduce transaction costs?

33

Asymmetric Information

one party to a transaction has better information to make decisions than the other party asymmetric information in financial market causes two main problems adverse selection moral hazard

34

Adverse Selection asymmetric information problem that occurs prior to a transaction examples of adverse selection result of adverse selection is that lenders may decide not to make loans if they can not distinguish between “good” and “bad” credit risks

35

Moral Hazard asymmetric information problem that occurs after a transaction risk that borrower will undertake risky activities that will increase the probability of default result of moral hazard is that lenders may decide not to make a loan

36

Lemons Problem idea presented in article by George Akerlof in terms of lemons in used car market used car buyers are unable to determine quality of car - good car or lemon? What amount is buyer willing to pay for this used car of unknown quality? How can buyer improve information on quality?

37

Lemons Problem in Stock and Bond Market

asymmetric information prevents investors from identifying good and bad firms What price will these investors pay for stock? Who has better information about the firm? Which firms will “come to the market” for financing under these conditions?

38

Principal-Agent Problem

define the principal-agent problem Who is the principal and who is the agent? What problem does a separation of ownership and control cause? How could we prevent principal-agent problem?

39

Solutions to Financing Puzzles

lemons or adverse selection problem tells why marketable securities are not the primary source of financing situation is similar in corporate bond market tells why stocks are not the most important source of external financing

40

More Solutions to Financial Structure Puzzles

importance of financial intermediaries explains importance of indirect financing explains why banks are most important source of external financing explains why markets are only available to large, well-known firms

41

Functions of FIs Brokerage function Acting as an agent for investors:

e.g. Merrill Lynch, Charles Schwab Reduce costs through economies of scale Encourages higher rate of savings Asset transformer: Purchase primary securities by selling financial claims to households These secondary securities often more marketable

42

Role of FIs in Cost Reduction

Information costs: Investors exposed to Agency Costs Role of FI as Delegated Monitor (Diamond, 1984) Shorter term debt contracts easier to monitor than bonds FI likely to have informational advantage

Shorter term debt contracts easier to monitor than bonds. FI likely to have informational advantage.")

43

Services Performed by FIs

Monitoring Costs Liquidity and Price Risk Transaction Cost Services Maturity Intermediation Denomination Intermediation

44

Services Provided by FIs

Money Supply Transmission Credit Allocation Intergenerational Wealth Transfers Payment Services (continued)

")

45

Regulation of FIs Regulation is not costless

Net regulatory burden. Safety and soundness regulation Monetary policy regulation Credit allocation regulation Consumer protection regulation Investor protection regulation Entry regulation

46

Changing Dynamics of Specialness

Trends in the United States Decline in share of depository institutions. Increases in pension funds and investment companies. May be attributable to net regulatory burden imposed on depository FIs. Technological changes affect delivery of financial services and regulatory issues Potential for regulations to be extended to hedge funds Result of Long Term Capital Management disaster

47

Future Trends Citicorp and Travelers, UBS and Paine Webber

Weakening of public trust and confidence in FIs may encourage disintermediation Increased merger activity within and across sectors Citicorp and Travelers, UBS and Paine Webber More large scale mergers such as J.P. Morgan and Chase, and Bank One and First Chicago Growth in Online Trading Increased competition from foreign FIs at home and abroad Mergers involving world’s largest banks Mergers blending together previously separate financial services sectors

48

(LECTURA DE REFERENCIA: HUMPHREY ET AL. (2006))

Tema 3 ORGANIZACIÓN INDUSTRIAL DEL SECTOR BANCARIO (LECTURA DE REFERENCIA: HUMPHREY ET AL. (2006))

)")

49

3. Bank competition 3.1. BANK COMPETITION

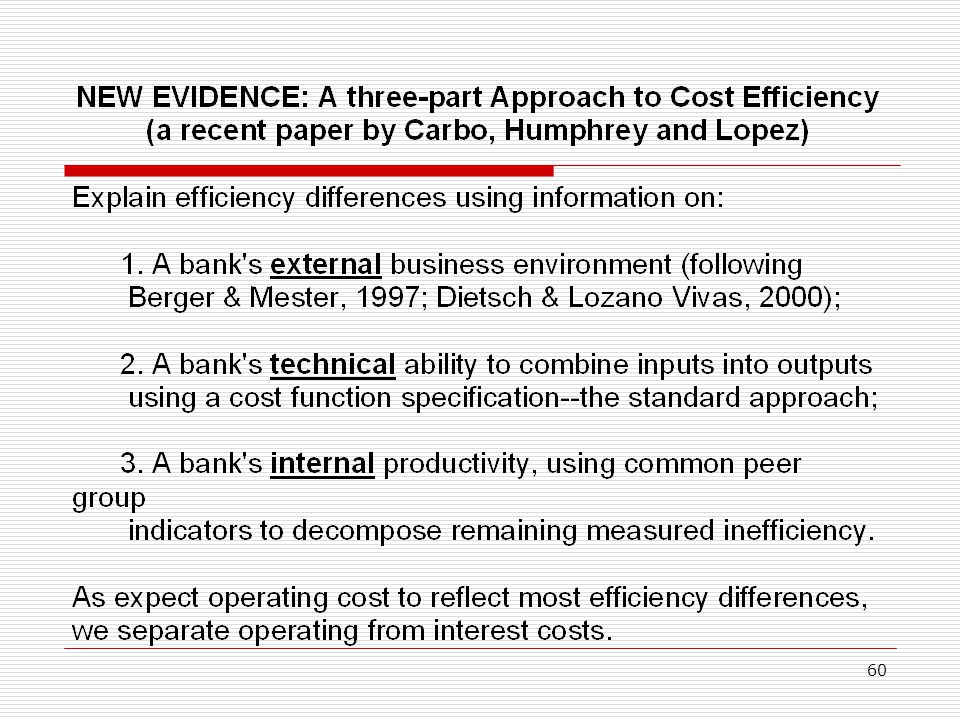

THE STRUCTURE-CONDUCT-PERFORMANACE (SCP) PARADIGM: Many empirical studies have considered concentration - mainly the Herfindahl-Hirschman Index (HHI) - as a proxy for bank market power following the Structure-Conduct-Performance (SCP) paradigm (Berger and Hannan, 1989; Hannan and Berger, 1991). However, several contributions to the banking literature during the last two decades have cast doubt on the consistency and robustness of concentration as an indicator of market power (Berger, 1995; Rhoades, 1995; Jackson 1997; Hannan, 1997).

PARADIGM: Many empirical studies have considered concentration - mainly the Herfindahl-Hirschman Index (HHI) - as a proxy for bank market power following the Structure-Conduct-Performance (SCP) paradigm (Berger and Hannan, 1989; Hannan and Berger, 1991). However, several contributions to the banking literature during the last two decades have cast doubt on the consistency and robustness of concentration as an indicator of market power (Berger, 1995; Rhoades, 1995; Jackson 1997; Hannan, 1997).")

50

IO theory predicts a correspondence between the Lerner index (L) – as the spread between prices (P) and marginal costs (C’) divided by prices - and the HHI so that , where is a conjecture parameter showing the response of the industry output to changes to a unit output change by the firm, and is the industry price elasticity of demand. If =1 there is a monopoly solution while if =0, then a Bertrand solution holds with L=0. Hence, the correspondence depends upon restrictive assumptions on the conjecture and demand elasticity parameters.

51

As contestability increases in a market, the reliability of the HHI as a measure of market power is significantly limited. Therefore, changes in the stability of the banking sector as a consequence of industry restructuring or liberalization may cast doubt on the validity of the HHI as a dynamic measure of competition. Instability will also affect conjecture and elasticity parameter so that the relationship between market power and concentration becomes blurred.

52

Although the SCP hypothesis of a positive relationship between concentration and profits can be derived from oligopoly theory under these assumptions of different solutions to a Cournot model, it is not warranted under alternative models. Some empirical studies have even tested and rejected the hypothesis of Cournot conduct in the banking industry (Roberts, 1984; Berg and Kim, 1994). Econometric developments have permitted the emergence of empirical papers from the so-called New Empirical Industrial Organization (NEIO) perspective, by directly estimating the parameters of a firm's behavioral equation – and, in particular, marginal costs - to directly obtain indicators such as the Lerner Index (Schmalensee, 1989).

. Econometric developments have permitted the emergence of empirical papers from the so-called New Empirical Industrial Organization (NEIO) perspective, by directly estimating the parameters of a firm s behavioral equation – and, in particular, marginal costs - to directly obtain indicators such as the Lerner Index (Schmalensee, 1989).")

53

Although price to marginal costs indicators are not “new” from a theoretical standpoint, marginal costs have only been econometrically estimated during the last two decades. Applications to the banking industry as in Shaffer (1993), Ribon and Yosha (1999) or Maudos and Fernández de Guevara (2004) have already shown that these price to marginal costs indicators are frequently uncorrelated with concentration ratios.

, Ribon and Yosha (1999) or Maudos and Fernández de Guevara (2004) have already shown that these price to marginal costs indicators are frequently uncorrelated with concentration ratios..")

54

The definition of the mark-up and the Lerner index can be directly derived from a simplified market structure model (Bresnahan, 1989) where banking firms are supposed to produce a single good. Assuming that banks behave as profit maximizers, the general expression for intermediate oligopolistic market structures with m banks operating in the market is expressed as:

55

where p is the price of the bank product; C(yj, wj) is a cost function defined for each bank j where yj is the quantity produced by firm j in the industry and wj represents the vector of prices of the factors of bank j. The parameter j expresses the degree of market power from perfectly competitive (j = 0) to monopolist (j = 1). This can be alternatively written as:

to monopolist (j = 1). This can be alternatively written as:.")

56

where the mark-up of price over marginal cost ([p – C’(yj, wj)]) equals the inverse of the semi-elasticity on bank product demand (1/) times the market structure parameter (j). Therefore, higher values of the mark-up measure will indicate a worsening of bank competition conditions either by a decrease in the semi-elasticity of demand on bank product () or an increase in the market structure parameter (j).

![where the mark-up of price over marginal cost ([p – C’(yj, wj)]) equals the inverse of the semi-elasticity on bank product demand (1/) times the market structure parameter (j).](http://slideplayer.com/slide/1618949/6/images/56/where+the+mark-up+of+price+over+marginal+cost+%28%5Bp+%E2%80%93+C%E2%80%99%28yj%2C+wj%29%5D%29+equals+the+inverse+of+the+semi-elasticity+on+bank+product+demand+%281%2F%EF%81%A5%29+times+the+market+structure+parameter+%28%EF%81%B1j%29..jpg "Therefore, higher values of the mark-up measure will indicate a worsening of bank competition conditions either by a decrease in the semi-elasticity of demand on bank product () or an increase in the market structure parameter (j)..")

57

The mark-up is used to compute the Lerner index, which is a relative margin computed as [p – C’(yj, wj)] / p. Higher values of the Lerner index also indicate a worsening of competition conditions.

![The mark-up is used to compute the Lerner index, which is a relative margin computed as [p – C’(yj, wj)] / p.](http://slideplayer.com/slide/1618949/6/images/57/The+mark-up+is+used+to+compute+the+Lerner+index%2C+which+is+a+relative+margin+computed+as+%5Bp+%E2%80%93+C%E2%80%99%28yj%2C+wj%29%5D+%2F+p..jpg "Higher values of the Lerner index also indicate a worsening of competition conditions..")

75

Introducción Existen, al menos, tres dimensiones en las que se precisan avances para lograr un diagnóstico más preciso de la realidad competitiva de la industria bancaria de la UE y poder arbitrar políticas acordes con los objetivos de integración y la mejora del acceso a los servicios bancarios

76

(MATERIAL DEL PROFESOR)

Tema 4 GOBIERNO Y ESTRUCTURA ORGANIZATIVA DE LA BANCA (MATERIAL DEL PROFESOR)

")

77

“It is the ability to foretell what is going to happen tomorrow, next week, next month, and next year. And to have the ability afterwards to explain why it didn’t happen.” Sir Winston Churchill

78

What are Financial Intermediaries (FIs)?

Financial Securities: contingent claims on future cash flows – debt, equity, derivatives, hybrids. All firms’ liabilities & net worth are predominately comprised of financial securities. But most firms hold real assets such as inventory, plant & equipment, buildings. FIs’ assets are predominately comprised of financial securities.

79

Transparent, Transluscent and Opaque FIs

80

What Services Do FIs Provide?

Information Liquidity Reduced Transaction Costs Transmission of Monetary Policy Credit Allocation Payment Services Intergenerational Wealth Transfer

81

FIs are the most regulated of all firms

Safety and Soundness Regulation Deposit Insurance Monetary Policy Regulation Reserve Requirements Credit Allocation Regulation (eg., mortgages) Consumer Protection Regulation Community Reinvestment Act, Home Mortgage Disclosure Act, Truth in Lending Protection Investor Protection Regulation Entry Regulation

Consumer Protection Regulation. Community Reinvestment Act, Home Mortgage Disclosure Act, Truth in Lending Protection. Investor Protection Regulation. Entry Regulation.")

82

Types of FIs Depository Institutions Insurance Companies

Securities Firms and Investment Banks Mutual Funds Finance Companies Distinctions blurred by the Gramm-Leach-Bliley Act of that created Financial Holding Companies (FHCs).

.")

83

Features Common to Most FIs

High Amount of Financial Leverage Low equity/assets ratios. Capital requirements. Off-balance sheet items Contingent claims that under certain circumstances may eventually become balance sheet items (ex. Derivatives, commitments) Revenue: Interest Income & Fees Costs: Interest Expenses and Personnel

Revenue: Interest Income & Fees. Costs: Interest Expenses and Personnel.")

84

Depository Institutions

Commercial Banks: accept deposits and make loans to consumers and businesses. Money Center Banks: Citigroup, Bank of NY, BankOne, Bankers Trust (Deutschebank), JP Morgan Chase and HSBC Bank USA. Savings Associations (S&Ls) Qualified Thrift Lender (QTL) mortgages must exceed 65% of thrift’s assets. Savings Banks Use deposits to fund mortgages & other assets. Credit Unions and Credit cooperatives Nonprofit mutually owned institutions (owned by depositors).

, JP Morgan Chase and HSBC Bank USA. Savings Associations (S&Ls) Qualified Thrift Lender (QTL) mortgages must exceed 65% of thrift’s assets. Savings Banks. Use deposits to fund mortgages & other assets. Credit Unions and Credit cooperatives. Nonprofit mutually owned institutions (owned by depositors).")

85

Overview of Depository Institutions

In this segment, we explore the depository FIs: Size, structure and composition Balance sheets and recent trends Regulation of depository institutions Depository institutions performance

86

Products of FIs Comparing the products of FIs in 1950, to products of FIs in 2003: Much greater distinction between types of FIs in terms of products in 1950 than in 2003 Blurring of product lines and services over time Wider array of services offered by all FI types

87

Specialness of Depository FIs

Products on both sides of the balance sheet Loans Business and Commercial Deposits

88

Other outputs of depository FIs

Other products and services 1950: Payment services, Savings products, Fiduciary services By 2003, products and services further expanded to include: Underwriting of debt and equity, Insurance and risk management products

89

Size of Depository FIs Consolidation has created some very large FIs

Combined effects of disintermediation, global competition, regulatory changes, technological developments, competition across different types of FIs

90

Largest Depository Institutions in the US

Total Assets ($Billions) Citigroup $1,208.9 J.P. Morgan Chase* Bank of America** Wells Fargo Wachovia Bank One* Washington Mutual Fleet Boston** U.S. Bancorp SunTrust Banks

Citigroup $1, J.P. Morgan Chase* Bank of America** Wells Fargo Wachovia Bank One* Washington Mutual Fleet Boston** U.S. Bancorp SunTrust Banks")

91

Organization of Depository Institutions

Commercial Banks Largest depository institutions are commercial banks. Differences in operating characteristics and profitability across size classes. Notable differences in ROE and ROA as well as the spread Thrifts S&Ls Savings Banks Credit Unions Mix of very large banks with very small banks

92

Functions & Structural Differences

Functions of depository institutions Regulatory sources of differences across types of depository institutions. Structural changes generally resulted from changes in regulatory policy. Example: changes permitting interstate branching Reigle-Neal Act (1994) in the US In Spain, deregulation in 1989 concerning savings banks operations

in the US. In Spain, deregulation in 1989 concerning savings banks operations.")

93

Commercial Banks Primary assets: Inference: Importance of Credit Risk

Real Estate Loans: $2,272.3 billion C&I loans: $870.6 billion Loans to individuals: $770.5 billion Investment security portfolio: $1,789.3 billion Of which, Treasury bonds: $1,005.8 billion Inference: Importance of Credit Risk

94

Commercial Banks Primary liabilities: Inference:

Deposits: $5,028.9 billion Borrowings: $1,643.3 billion Other liabilities: $238.2 billion Inference: Highly leveraged

95

Small Banks, US

96

Large Banks, US

97

Structure and Composition

Shrinking number of banks: 14,416 commercial banks in 1985 12,744 in 1989 7,769 in 2004 Mostly the result of Mergers and Acquisitions M&A prevented prior to 1980s, 1990s Consolidation has reduced asset share of small banks

98

Structure & Composition of Commercial Banks

Financial Services Modernization Act 1999 Allowed full authority to enter investment banking (and insurance) Limited powers to underwrite corporate securities have existed only since 1987

Limited powers to underwrite corporate securities have existed only since")

99

Composition of Commercial Banking Sector

Community banks Regional and Super-regional Access to federal funds market to finance their lending activities Money Center banks Bank of New York, Deutsche Bank (Bankers Trust), Citigroup, J.P. Morgan Chase, HSBC Bank USA declining in number

, Citigroup, J.P. Morgan Chase, HSBC Bank USA. declining in number.")

100

Balance Sheet and Trends

Business loans have declined in importance Offsetting increase in securities and mortgages Increased importance of funding via commercial paper market Securitization of mortgage loans

101

Some Terminology Transaction accounts

Negotiable Order of Withdrawal (NOW) accounts (“cuenta a la vista”) Money Market Mutual Fund Negotiable CDs (“certificados de depósito”): Fixed-maturity interest bearing deposits with face values over $100,000 that can be resold in the secondary market.

accounts ( cuenta a la vista ) Money Market Mutual Fund. Negotiable CDs ( certificados de depósito ): Fixed-maturity interest bearing deposits with face values over $100,000 that can be resold in the secondary market.")

102

Off-balance Sheet Activities

Heightened importance of off-balance sheet items Large increase in derivatives positions is a major issue Standby letters of credit Loan commitments When-issued securities Loans sold

103

Trading and Other Risks

Allied Irish / Allfirst Bank $750 million loss (2001) National Australian Bank $450 million loss (2004) Failure of the U.K. investment bank Barings The Bankruptcy of Orange County in California.

National Australian Bank. $450 million loss (2004) Failure of the U.K. investment bank Barings. The Bankruptcy of Orange County in California.")

104

Other Fee-generating Activities

Trust services Correspondent banking Check clearing Foreign exchange trading Hedging Participation in large loan and security issuances Payment usually in terms of noninterest bearing deposits

105

Key Regulatory Agencies

FDIC and the Office of the Comprotroller of the Currency in the US. European Central Bank National central banks National Governments Regional Governments

106

Web Resources For more detailed information on the regulators, visit:

107

Banking and Ethics Some cases for the US:

Bank of America and Fleet Boston Financial 2004 J.P. Morgan Chase and Citigroup 2003 role in Enron Riggs National Bank and money laundering concerns 2003

108

Savings Institutions Comprised of:

Savings and Loans Associations Savings Banks Effects of moral hazard and regulator forbearance. Quite a debate worldwhile.

109

Savings Institutions: Recent Trends

Industry is smaller overall Intense competition from other FIs mortgages for example Concern for future viability in certain countries.

110

Credit Unions Nonprofit depository institutions owned by member-depositors with a common bond. Exempt from taxes and Community Reinvestment Act (CRA) in the US. Expansion of services offered in order to compete with other FIs. Very important in certain European countries (Germany, Spain).

in the US. Expansion of services offered in order to compete with other FIs. Very important in certain European countries (Germany, Spain).")

111

Global Issues Near crisis in Japanese Banking

Eight biggest banks reported positive six-month profits China Deterioration, NPLs (nonperforming loans) at 50% levels Opening to foreign banks (WTO entry) German bank problems in early 2000s Implications for future competitiveness

at 50% levels. Opening to foreign banks (WTO entry) German bank problems in early 2000s. Implications for future competitiveness.")

112

Largest Banks in the World

113

(LECTURA DE REFERENCIA: ALTUNBAS ET AL.,2007)

Tema 5 La concesión de crédito, el riesgo de crédito y otros riesgos (LECTURA DE REFERENCIA: ALTUNBAS ET AL.,2007)

")

114

5.1. THE CONCEPT OF RISK Risks facing all financial institutions can be segmented into three separable types, from a management perspective. These are: (i) risks that can be eliminated or avoided by simple business practices, (ii) risks that can be transferred to other participants, and, (iii) risks that must be actively managed at the firm level.

risks that can be eliminated or avoided by simple business practices, (ii) risks that can be transferred to other participants, and, (iii) risks that must be actively managed at the firm level.")

115

The management of the banking firm relies on a sequence of steps to implement a risk management system. These can be seen as containing the following four parts: (i) standards and reports, (ii) position limits or rules, (iii) investment guidelines or strategies, (iv) incentive contracts and compensation.

standards and reports, (ii) position limits or rules, (iii) investment guidelines or strategies, (iv) incentive contracts and compensation.")

116

SOURCES OF RISK For the sector as a whole, the risks can be broken into six generic types: systematic or market risk credit risk counterparty risk liquidity risk operational risk legal risk

117

Systematic risk is the risk of asset value change associated with systematic factors. It is sometimes referred to as market risk, which is in fact a somewhat imprecise term. By its nature, this risk can be hedged, but cannot be diversified completely away. In fact, systematic risk can be thought of as undiversifiable risk.

118

Credit risk arises from non-performance by a borrower

Credit risk arises from non-performance by a borrower. It may arise from either an inability or an unwillingness to perform in the pre-committed contracted manner. This can affect the lender holding the loan contract, as well as other lenders to the creditor. Therefore, the financial condition of the borrower as well as the current value of any underlying collateral is of considerable interest to its bank

119

Counterparty risk comes from non-performance of a trading partner

Counterparty risk comes from non-performance of a trading partner. The non-performance may arise from a counterparty's refusal to perform due to an adverse price movement caused by systematic factors, or from some other political or legal constraint that was not anticipated by the principals. Diversification is the major tool for controlling nonsystematic counterparty risk.

120

Liquidity risk can best be described as the risk of a funding crisis

Liquidity risk can best be described as the risk of a funding crisis. While some would include the need to plan for growth and unexpected expansion of credit, the risk here is seen more correctly as the potential for a funding crisis. Such a situation would inevitably be associated with an unexpected event, such as a large charge off, loss of confidence, or a crisis of national proportion such as a currency crisis.

121

Operational risk is associated with the problems of accurately processing, settling, and taking or making delivery on trades in exchange for cash. It also arises in record keeping, processing system failures and compliance with various regulations. As such, individual operating problems are small probability events for well-run organizations but they expose a firm to outcomes that may be quite costly.

122

Legal risks are endemic in financial contracting and are separate from the legal ramifications of credit, counterparty, and operational risks. New statutes, tax legislation, court opinions and regulations can put formerly well-established transactions into contention even when all parties have previously performed adequately and are fully able to perform in the future.

123

5.2. REGULATION AND CREDIT RISK: AN EXAMPLE FROM BASEL II

Historically, regulation has limited who can: open or charter new banks and what products and services banks can offer. Imposing barriers to entry and restricting the types of activities banks can engage in clearly enhance safety and soundness, but also hinder competition.

124

It assumed that the markets for bank products, largely bank loans and deposits, could be protected and that other firms could not encroach upon these markets. Not surprisingly, investment banks, hybrid financial companies, insurance firms, and others found ways to provide the same products as banks across different geographic markets.

125

However, there is another type of regulation that has concentrated most of the attention in the last three decades, the bank capital regulation. Changes in reserve requirements …directly affect the amount of legal required reserves and thus change the amount of money a bank can lend out. The main recent example is BASEL II.

126

THE STRATEGIC IMPACT OF BASEL II

Basel 2 is a ‘step change’ in the regulation of capital adequacy. It will alter the industry ‘frame of reference’ for banks in many ways: Regulators are clearly recognizing market realities and seeking a much closer congruence between regulatory and economic capital. The new proposals are more complex and sophisticated than earlier schemes. They will also have to evolve as market conditions, technology and financial management techniques develop.

127

The calibration exercises that have resulted from the various Quantitative Impact Studies (QIS) are targeted (initially at least) to deliver broadly the same amount of capital as the current Accord. However, the mix of capital charges will change significantly with the wider range of risk weights and greater risk sensitivity of Basel 2. Basel 2 will clearly be much more risk-sensitive in assigning capital charges. Mortgage lending and lending to higher quality borrowers will be incentivised under Basel 2.

128

It is not clear whether the present or new Basel Accord are a binding constraint on bank’s current credit operations. Jackson et al (2001, Bank of England WP) suggest that banks may employ more conservative capital standards than those imposed under Basel 1 or likely under Basel 2. Compliance costs are likely to increase. Banks will have to evaluate (as a kind of capital investment decision) whether the costs (including compliance costs) of moving to the more advanced Basel 2 systems are worthwhile.

whether the costs (including compliance costs) of moving to the more advanced Basel 2 systems are worthwhile.")

129

Banks will increasingly target better risk management as a source of competitive advantage. Increasingly, superior risk management will become a ‘key success factor’ for those banks who are able to respond successfully to the new environment. Nevertheless, specialist banks who focus on a smaller number of core products and services should similarly be able to obtain risk management benefits of specialization.

130

Basel 2 will enhance present securitisation trends in banking

Basel 2 will enhance present securitisation trends in banking. This will help in its turn to emphasise further the strategic importance of investment banking. At the same time, lending bankers will face increasing ‘adverse selection’ trends as the better credits are able to access directly the capital markets. This trend will help to re-emphasise the importance of credit skills in lending banks. It will also put pressure on these banks to widen their margins (in order to achieve the higher risk premia needed to cover their more risky lending).

.")

131

Governance will be an increasingly important issue in the new regime

Governance will be an increasingly important issue in the new regime. More disclosure is not enough by itself to secure market discipline (the aim of Pillar 3). A wide collection of new and improved governance structures will be needed. These include: a freer market in bank corporate control; good corporate governance in banks; incentive-compatible safety nets; ‘no bail-out’ policies; and proper accounting standards. Banks will be required to disclose more information than ever before to the external market. This will involve additional compliance costs. Strategically, it will reinforce any competitive advantage gained by good risk-management banks.

. A wide collection of new and improved governance structures will be needed. These include: a freer market in bank corporate control; good corporate governance in banks; incentive-compatible safety nets; ‘no bail-out’ policies; and proper accounting standards. Banks will be required to disclose more information than ever before to the external market. This will involve additional compliance costs. Strategically, it will reinforce any competitive advantage gained by good risk-management banks.")

132

Under Pillar 3 and with likely changes in bank governance arrangements, the prospects of take-overs (and no bail-outs) for individual banks who are ‘inefficient’ are likely to increase. This ‘new world’ is a likely further threat to concepts like mutuality and subsidised (or at least protected from competition) regional banking. Insofar as the new capital regime allows non-bank financial companies a competitive advantage (via lesser capital backing), banks will attempt to alter the balance of competitive advantage through regulatory arbitrage

, banks will attempt to alter the balance of competitive advantage through regulatory arbitrage.")

133

More work is needed on stress testing under Basel 2 and banks can expect further, more detailed efforts from regulators in this area. Already, stress testing appears to be a standard management technique for many banks and most banks that stress test do so at a high frequency (daily or weekly): see Fender and Gibson (Risk, 2001).

: see Fender and Gibson (Risk, 2001)..")

134

Perhaps the most fundamental strategic impact of Basel 2 is that it will enhance the SWM (Shareholder Wealth Maximisation) model as the major strategic and managerial model for banks. The essence of this model is its focus on risk and return and the impact of this tradeoff on bank value; the model also emphasises the need for greater risk sensitivity in risk assessments and pricing. Within this model, better risk management is rewarded.

135

5.3. THE SPANISH SAVINGS BANKS AND THE NEW REGULATORY FRAMEWORK

Although most of the strategic implications mentioned earlier for retail banks apply also to Spanish savings banks, there are some specific features of the Spanish savings banks that may modify some of these conclusions. These specific features are explored in this section (and summarised in Diagram 1): There have been some recent regulatory actions regarding risk and capital in the Spanish banking system that should be taken into account when defining the threats and opportunities of the new framework for savings banks. The development of a Default Hedging Statistical Fund (the so-called FECI) by the Bank of Spain are two of the recent developments in the regulatory field that impact on the current solvency risk of Spanish savings banks

: There have been some recent regulatory actions regarding risk and capital in the Spanish banking system that should be taken into account when defining the threats and opportunities of the new framework for savings banks. The development of a Default Hedging Statistical Fund (the so-called FECI) by the Bank of Spain are two of the recent developments in the regulatory field that impact on the current solvency risk of Spanish savings banks.")

136

1. SPANISH SAVINGS BANKS AND THE NEW REGULATORY

DIAGRAM 1. SPANISH SAVINGS BANKS AND THE NEW REGULATORY CAPITAL FRAMEWORK. KEY FEATURES SPANISH SAVINGS BANKS AND THE NEW REGULATORY CAPITAL FRAMEWORK REGULATION: MARKET DEVELOPMENTS – B ASEL 2 CAPITAL REGULATION AND OWNERSHIP STRATEGIC IMPLICATIONS SECTORAL PROJECT FOR THE GLOBAL CONTROL OF RISK

137

The establishment of so-called statistical, pro-cyclical or dynamic provisions:

Requiring banks to increase these provisions when the business cycle is positive and reducing them during downturns in order to favor intertemporal risk smoothing and loan supply. Basel 2 does not appear to change the view of banking as a pro-cyclical business. Basel 2 could even exacerbate cyclical effects. It is this contingency that has led the Bank of Spain to establish the so-called pro-cyclical or dynamic provisions. The recent lending patterns of the Spanish savings banks are known to reduce these pro-cyclical effects since they have increased credit supply almost linearly over the business cycle.

138

The lending behavior of savings banks has not resulted in higher defaults. On the contrary, default risk management at savings banks has apparently been more efficient than for commercial banks, a fact that may be largely explained by the intertemporal risk smoothing advantages achieved via a close contractual relationship with their customers.

139

There are three main types of “savings-bank” specific effects:

(1) those concerning the aim of Basel 2 and the differences between economic and regulatory capital; (2) those that refer to specialization, size and lending diversification; (3) those related to the implementation of the new capital adequacy requirements, including the sectoral project of Spanish savings banks for the global control of risk.

those concerning the aim of Basel 2 and the differences between economic and regulatory capital; (2) those that refer to specialization, size and lending diversification; (3) those related to the implementation of the new capital adequacy requirements, including the sectoral project of Spanish savings banks for the global control of risk.")

140

(i) Aim of Basel 2 and Economic and Regulatory Capital Differences

While the objective of Stakeholder Wealth Maximization (STWM) may match more closely the nature of Spanish savings banks, SWM should not be a problem for savings institutions since they have to compete with commercial banks. Nevertheless, the SWM model will be reinforced by Basel 2 and Spanish savings banks may benefit from recent regulatory changes that stress their ownership status as private and non-subsidised.

may match more closely the nature of Spanish savings banks, SWM should not be a problem for savings institutions since they have to compete with commercial banks. Nevertheless, the SWM model will be reinforced by Basel 2 and Spanish savings banks may benefit from recent regulatory changes that stress their ownership status as private and non-subsidised.")

141

(ii) Size, specialisation and lending diversification

Specialist banks (like savings banks) focusing on a smaller number of core products may also be able to obtain the risk management benefits of specialisation. Continuous calibration and capital treatment may reduce the potential loss of competitiveness in retail banking. Servicing, relationship banking and dynamic lending will also be valued positively.

focusing on a smaller number of core products may also be able to obtain the risk management benefits of specialisation. Continuous calibration and capital treatment may reduce the potential loss of competitiveness in retail banking. Servicing, relationship banking and dynamic lending will also be valued positively.")

142

(iii) Final implementation of Basel 2 on Spanish savings banks: the sectoral project for the global control of risk The Spanish Confederation of Savings Banks (CECA) has led an ambitious initiative to undertake a sectoral project for the global control of risk. Since this project is oriented to the whole savings bank sector, it has to deal with various problems, like the rigidities of employing a single model for all institutions. However, the project is targetted to provide savings banks with adequate and centralised human and technological resources in order to implement their own model with a high standard of quality.

has led an ambitious initiative to undertake a sectoral project for the global control of risk. Since this project is oriented to the whole savings bank sector, it has to deal with various problems, like the rigidities of employing a single model for all institutions. However, the project is targetted to provide savings banks with adequate and centralised human and technological resources in order to implement their own model with a high standard of quality.")

143

The model for each line of business incorporates risk measurement, control and management operating with three different working groups: information management; organization and procedures; quantitative tools.

144

5.4. COMPARATIVE DESCRIPTIVE STATISTICS

The credit risk of Spanish depository institutions does not seem to be a concern in the short-run. The ratios “doubtful assets/total exposures” and “doubtful loans of other resident sectors/total exposures of resident sectors” have decreased in recent years and are lower than 1% (Table 1). “Statistical” provisions have increased over time as a percentage of total provisions (Table 1).

. Statistical provisions have increased over time as a percentage of total provisions (Table 1).")

145

TABLE 1. Source: Bank of Spain (Memory of Bank Supervision 2004)

")

146

Savings banks and credit co-operatives have enjoyed higher margins compared to commercial banks (Table 2). The margins are in line with the European standards. However, competitive presures have resulted in a decrease of margins over time during the last years.

147

TABLE 2. Source: Bank of Spain (Memory of Bank Supervision 2004)

")

148

As shown in Table 3, Spanish banks have progressively changed their financial structure to fulfill the requirements of Basel 2. Both Tier 1 and Tier 2 capital have increased significantly in recent years. Banks have increased both the average weight of credit risk exposure and off-balance sheet exposure.

149

TABLE 3. Source: Bank of Spain (Memory of Bank Supervision 2004)

")

150

Changes in capitalization structure have led to an anticipated fulfillment of Basel 2 requirements (Figure 1a). Tier 1 capital has largely contributed to a reduction in capital requirements, in a context of a significant increase in risk-weighted assets (rise in overall business and Santander’s purchase of Abbey National) (Figure 1b). However, Tier 1 capital has contributed to the growth rate of capital (Figure 1c). Reserves have contributed largely to the growth of Tier 1 capital while the contribution of intangible assets has been negative (Figure 1d).

(Figure 1b). However, Tier 1 capital has contributed to the growth rate of capital (Figure 1c). Reserves have contributed largely to the growth of Tier 1 capital while the contribution of intangible assets has been negative (Figure 1d).")

151

FIGURE 1. SOLVENCY RATIOS OF COMMERCIAL AND SAVINGS BANKS IN SPAIN (1)

Source: Bank of Spain (Financial Stability Report, n.8, 2005, May)

")

152

FIGURE 1. SOLVENCY RATIOS OF COMMERCIAL AND SAVINGS BANKS IN SPAIN (2)

Source: Bank of Spain (Financial Stability Report, n.8, 2005, May)

")

153

Measurement of credit risk

154

Types of Loans: C&I (commercial and industrial) loans: secured and unsecured Syndication Spot loans, Loan commitments Decline in C&I loans originated by commercial banks and growth in commercial paper market. Downgrades of Ford, General Motors and Tyco RE (real state) loans: primarily mortgages Fixed-rate, variable rates Mortgages can be subject to default risk when loan-to-value declines.

loans: primarily mortgages. Fixed-rate, variable rates. Mortgages can be subject to default risk when loan-to-value declines.")

155

*CreditMetrics (sistema patentado)

“If next year is a bad year, how much will I lose on my loans and loan portfolio?” VAR = P × 1.65 × s Neither P, nor s observed. Calculated using: (i)Data on borrower’s credit rating; (ii) Rating transition matrix; (iii) Recovery rates on defaulted loans; (iv) Yield spreads.

Data on borrower’s credit rating; (ii) Rating transition matrix; (iii) Recovery rates on defaulted loans; (iv) Yield spreads.")

156

* Credit Risk+ (sistema patentado)

Developed by Credit Suisse Financial Products. Based on insurance literature: Losses reflect frequency of event and severity of loss. Loan default is random. Loan default probabilities are independent. Appropriate for large portfolios of small loans. Modeled by a Poisson distribution.

157

Credit risk measurement has evolved dramatically over the last 20 years.

The five forces made credit risk measurement become more important than ever before: A worldwide structural increase in the number of bankruptcies. A trend towards disintermediation by the highest quality and largest borrowers.

158

(iii) More competitive margins on loans.

(iv) A declining value of real assets in many markets. (v) A dramatic growth of off-balance sheet instrument with inherent default risk exposure, including credit risk derivatives.

A declining value of real assets in many markets. (v) A dramatic growth of off-balance sheet instrument with inherent default risk exposure, including credit risk derivatives.")

159

Responses of academics and practitioners:

Developing new and more sophisticated credit-scoring/early-warning systems Moved away from only analyzing the credit risk of individual loans and securities towards developing measures of credit concentration risk Developing new models to price credit risk (e.g. RAROC) Developing models to measure better the credit risk of off-balance sheet instruments

Developing models to measure better the credit risk of off-balance sheet instruments.")

160

Credit Risk Management

An FI’s ability to evaluate information and control and monitor borrowers allows them to transform financial claims of household savers efficiently into claims issued to corporations, individuals, and governments An FI accepts credit risk in exchange for a fair return sufficient to cover the cost of funding (e.g., covering the cost of borrowing, or issuing deposits)

")

161

Credit Scoring Power of sale Credit scoring system

a mathematical model that uses observed loan applicant’s characteristics to calculate a score that represents the applicant’s probability of default Perfecting collateral ensuring that collateral used to secure a loan is free and clear to the lender should the borrower default Foreclosure taking possession of the mortgaged property to satisfy a defaulting borrower’s indebtedness Power of sale taking the proceedings of the forced sale of property to satisfy the indebtedness

162

Credit Scoring Consumer (individual) and Small-business lending

techniques for scoring consumer loans very similar to mortgage loan credit analysis but more emphasis placed on personal characteristics such as annual gross income and the TDS score small-business loans more complicated and has required FIs to build more sophisticated scoring models combining computer-based financial analysis of borrower financial statements with behavioral analysis of the owner

163

Ratio Analysis Historical audited financial statements and projections of future needs Calculation of financial ratios in financial statement analysis Relative ratios offer information about how a business is changing over time Particularly informative when they differ either from an industry average or from the applicant’s own past history

164

Common Size Analysis and After the Loan

Analyst can divide all income statement amounts by total sales revenue and all balance sheet amounts by total assets Year to year growth rates give useful ratios for identifying trends Loan covenants reduce risk to lender Conditions precedent those conditions specified in the credit agreement or terms sheet for a credit that must be fulfilled before drawings are permitted

165

Large Commercial and Industrial Lending

Very attractive to FIs because transactions are often large enough make them very profitable even though spreads and fees are small in percentage FIs act as broker, dealer, and adviser in credit management The standard methods of analysis used for mid-market corporates applied to large corporate clients but with additional complications Financial ratios such as the debt-equity ratio are usually key factors for corporate debt

166

The KMV Model Banks can use the theory of option pricing to assess the credit risk of a corporate borrower The probability of default is positively related to: the volatility of the firm’s stock the firm’s leverage A model developed by KMV corporation is being widely used by banks for this purpose

167

Calculating the Return on a Loan

A number of factors impact the promised return that an FI achieves on any given dollar loan the interest rate on the loan any fees relating to the loan the credit risk premium on the loan the collateral backing the loan other nonprice terms (such as compensating balances and reserve requirements)

")

168

Return on Assets (ROA) 1 + k = 1 + f + (L + m) 1 - (b(1 - R)) where

k = the contractually promised gross return on the loan f = direct fees, such as loan origination fee L = base lending rate m = risk premium b = compensating balances R = reserve requirement charge

169

Risk-Adjusted Return on Capital (RAROC)

Rather than evaluating the actual or promised annual cash flow on a loan as a percentage of the amount lent (ROA), the lending officer balances the loan’s expected income against the loan’s expected risk RAROC = One-year income on a loan/Loan (asset risk or capital at risk

, the lending officer balances the loan’s expected income against the loan’s expected risk. RAROC = One-year income on a loan/Loan (asset risk or capital at risk.")

170

APPENDIX: Bank regulation and credit risk: an example from Basel II and savings banks

Historically, regulation has limited who can: open or charter new banks and what products and services banks can offer. Imposing barriers to entry and restricting the types of activities banks can engage in clearly enhance safety and soundness, but also hinder competition.

171

It assumed that the markets for bank products, largely bank loans and deposits, could be protected and that other firms could not encroach upon these markets. Not surprisingly, investment banks, hybrid financial companies, insurance firms, and others found ways to provide the same products as banks across different geographic markets.

172

However, there is another type of regulation that has concentrated most of the attention in the last three decades, the bank capital regulation. Changes in reserve requirements …directly affect the amount of legal required reserves and thus change the amount of money a bank can lend out. The main recent example is BASEL II.

173

Basel 2 is a ‘step change’ in the regulation of capital adequacy

Basel 2 is a ‘step change’ in the regulation of capital adequacy. It will alter the industry ‘frame of reference’ for banks in many ways: Regulators are clearly recognizing market realities and seeking a much closer congruence between regulatory and economic capital. The new proposals are more complex and sophisticated than earlier schemes. They will also have to evolve as market conditions, technology and financial management techniques develop.

174

The calibration exercises that have resulted from the various Quantitative Impact Studies (QIS) are targeted (initially at least) to deliver broadly the same amount of capital as the current Accord. However, the mix of capital charges will change significantly with the wider range of risk weights and greater risk sensitivity of Basel 2. Basel 2 will clearly be much more risk-sensitive in assigning capital charges. Mortgage lending and lending to higher quality borrowers will be incentivied under Basel 2.

175

It is not clear whether the present or new Basel Accord are a binding constraint on bank’s current credit operations. Jackson et al (2001, Bank of England WP) suggest that banks may employ more conservative capital standards than those imposed under Basel 1 or likely under Basel 2. Compliance costs are likely to increase. Banks will have to evaluate (as a kind of capital investment decision) whether the costs (including compliance costs) of moving to the more advanced Basel 2 systems are worthwhile.

whether the costs (including compliance costs) of moving to the more advanced Basel 2 systems are worthwhile.")

176

Banks will increasingly target better risk management as a source of competitive advantage. Increasingly, superior risk management will become a ‘key success factor’ for those banks who are able to respond successfully to the new environment. Nevertheless, specialist banks who focus on a smaller number of core products and services should similarly be able to obtain risk management benefits of specialization.

177

Basel 2 will enhance present securitisation trends in banking

Basel 2 will enhance present securitisation trends in banking. This will help in its turn to emphasise further the strategic importance of investment banking. At the same time, lending bankers will face increasing ‘adverse selection’ trends as the better credits are able to access directly the capital markets. This trend will help to re-emphasise the importance of credit skills in lending banks. It will also put pressure on these banks to widen their margins (in order to achieve the higher risk premia needed to cover their more risky lending).

.")

178

Governance will be an increasingly important issue in the new regime

Governance will be an increasingly important issue in the new regime. More disclosure is not enough by itself to secure market discipline (the aim of Pillar 3). A wide collection of new and improved governance structures will be needed. These include: a freer market in bank corporate control; good corporate governance in banks; incentive-compatible safety nets; ‘no bail-out’ policies; and proper accounting standards. Banks will be required to disclose more information than ever before to the external market. This will involve additional compliance costs. Strategically, it will reinforce any competitive advantage gained by good risk-management banks.

. A wide collection of new and improved governance structures will be needed. These include: a freer market in bank corporate control; good corporate governance in banks; incentive-compatible safety nets; ‘no bail-out’ policies; and proper accounting standards. Banks will be required to disclose more information than ever before to the external market. This will involve additional compliance costs. Strategically, it will reinforce any competitive advantage gained by good risk-management banks.")

179

Under Pillar 3 and with likely changes in bank governance arrangements, the prospects of take-overs (and no bail-outs) for individual banks who are ‘inefficient’ are likely to increase. This ‘new world’ is a likely further threat to concepts like mutuality and subsidised (or at least protected from competition) regional banking. Insofar as the new capital regime allows non-bank financial companies a competitive advantage (via lesser capital backing), banks will attempt to alter the balance of competitive advantage through regulatory arbitrage

, banks will attempt to alter the balance of competitive advantage through regulatory arbitrage.")

180

More work is needed on stress testing under Basel 2 and banks can expect further, more detailed efforts from regulators in this area. Already, stress testing appears to be a standard management technique for many banks and most banks that stress test do so at a high frequency (daily or weekly): see Fender and Gibson (Risk, 2001).

: see Fender and Gibson (Risk, 2001)..")

181

Perhaps the most fundamental strategic impact of Basel 2 is that it will enhance the SWM (Shareholder Wealth Maximisation) model as the major strategic and managerial model for banks. The essence of this model is its focus on risk and return and the impact of this tradeoff on bank value; the model also emphasises the need for greater risk sensitivity in risk assessments and pricing. Within this model, better risk management is rewarded.

182

Although most of the strategic implications mentioned earlier for retail banks apply also to Spanish savings banks, there are some specific features of the Spanish savings banks that may modify some of these conclusions. These specific features are explored in this section (and summarised in Diagram 1): There have been some recent regulatory actions regarding risk and capital in the Spanish banking system that should be taken into account when defining the threats and opportunities of the new framework for savings banks. The development of a Default Hedging Statistical Fund (the so-called FECI) by the Bank of Spain are two of the recent developments in the regulatory field that impact on the current solvency risk of Spanish savings banks

by the Bank of Spain are two of the recent developments in the regulatory field that impact on the current solvency risk of Spanish savings banks.")

183

1. SPANISH SAVINGS BANKS AND THE NEW REGULATORY

DIAGRAM 1. SPANISH SAVINGS BANKS AND THE NEW REGULATORY CAPITAL FRAMEWORK. KEY FEATURES SPANISH SAVINGS BANKS AND THE NEW REGULATORY CAPITAL FRAMEWORK REGULATION: MARKET DEVELOPMENTS – B ASEL 2 CAPITAL REGULATION AND OWNERSHIP STRATEGIC IMPLICATIONS SECTORAL PROJECT FOR THE GLOBAL CONTROL OF RISK

184

The establishment of so-called statistical, pro-cyclical or dynamic provisions:

Requiring banks to increase these provisions when the business cycle is positive and reducing them during downturns in order to favor intertemporal risk smoothing and loan supply. Basel 2 does not appear to change the view of banking as a pro-cyclical business. Basel 2 could even exacerbate cyclical effects. It is this contingency that has led the Bank of Spain to establish the so-called pro-cyclical or dynamic provisions. The recent lending patterns of the Spanish savings banks are known to reduce these pro-cyclical effects since they have increased credit supply almost linearly over the business cycle.

185

The lending behavior of savings banks has not resulted in higher defaults. On the contrary, default risk management at savings banks has apparently been more efficient than for commercial banks, a fact that may be largely explained by the intertemporal risk smoothing advantages achieved via a close contractual relationship with their customers.

186

There are three main types of “savings-bank” specific effects:

(1) those concerning the aim of Basel 2 and the differences between economic and regulatory capital; (2) those that refer to specialisation, size and lending diversification; (3) those related to the implementation of the new capital adequacy requirements, including the sectoral project of Spanish savings banks for the global control of risk.

those concerning the aim of Basel 2 and the differences between economic and regulatory capital; (2) those that refer to specialisation, size and lending diversification; (3) those related to the implementation of the new capital adequacy requirements, including the sectoral project of Spanish savings banks for the global control of risk.")

187

(i) Aim of Basel 2 and Economic and Regulatory Capital Differences

While the objective of Stakeholder Wealth Maximisation (STWM) may match more closely the nature of Spanish savings banks, SWM should not be a problem for savings institutions since they have to compete with commercial banks. Nevertheless, the SWM model will be reinforced by Basel 2 and Spanish savings banks may benefit from recent regulatory changes that stress their ownership status as private and non-subsidised.

may match more closely the nature of Spanish savings banks, SWM should not be a problem for savings institutions since they have to compete with commercial banks. Nevertheless, the SWM model will be reinforced by Basel 2 and Spanish savings banks may benefit from recent regulatory changes that stress their ownership status as private and non-subsidised.")

188

(ii) Size, specialisation and lending diversification

Specialist banks (like savings banks) focusing on a smaller number of core products may also be able to obtain the risk management benefits of specialisation. Continuous calibration and capital treatment may reduce the potential loss of competitiveness in retail banking. Servicing, relationship banking and dynamic lending will also be valued positively.

focusing on a smaller number of core products may also be able to obtain the risk management benefits of specialisation. Continuous calibration and capital treatment may reduce the potential loss of competitiveness in retail banking. Servicing, relationship banking and dynamic lending will also be valued positively.")

189

(iii) Final implementation of Basel 2 on Spanish savings banks: the sectoral project for the global control of risk The Spanish Confederation of Savings Banks (CECA) has led an ambitious initiative to undertake a sectoral project for the global control of risk. Since this project is oriented to the whole savings bank sector, it has to deal with various problems, like the rigidities of employing a single model for all institutions. However, the project is targetted to provide savings banks with adequate and centralised human and technological resources in order to implement their own model with a high standard of quality.

has led an ambitious initiative to undertake a sectoral project for the global control of risk. Since this project is oriented to the whole savings bank sector, it has to deal with various problems, like the rigidities of employing a single model for all institutions. However, the project is targetted to provide savings banks with adequate and centralised human and technological resources in order to implement their own model with a high standard of quality.")

190

The model for each line of business incorporates risk measurement, control and management operating with three different working groups: information management; organization and procedures; quantitative tools.

191

COMPARATIVE DESCRIPTIVE STATISTICS

The credit risk of Spanish depository institutions does not seem to be a concern in the short-run. The ratios “doubtful assets/total exposures” and “doubtful loans of other resident sectors/total exposures of resident sectors” have decreased in recent years and are lower than 1% (Table 1). “Statistical” provisions have increased over time as a percentage of total provisions (Table 1).

. Statistical provisions have increased over time as a percentage of total provisions (Table 1).")

192

TABLE 1. Source: Bank of Spain (Memory of Bank Supervision 2004)

")

193

Savings banks and credit co-operatives have enjoyed higher margins compared to commercial banks (Table 2). The margins are in line with the European standards. However, competitive presures have resulted in a decrease of margins over time during the last years.

194

TABLE 2. Source: Bank of Spain (Memory of Bank Supervision 2004)

")

195

As shown in Table 3, Spanish banks have progressively changed their financial structure to fulfill the requirements of Basel 2. Both Tier 1 and Tier 2 capital have increased significantly in recent years. Banks have increased both the average weight of credit risk exposure and off-balance sheet exposure.

196

TABLE 3. Source: Bank of Spain (Memory of Bank Supervision 2004)

")

197

Changes in capitalization structure have led to an anticipated fulfillment of Basel 2 requirements (Figure 1a). Tier 1 capital has largely contributed to a reduction in capital requirements, in a context of a significant increase in risk-weighted assets (rise in overall business and Santander’s purchase of Abbey National) (Figure 1b). However, Tier 1 capital has contributed to the growth rate of capital (Figure 1c). Reserves have contributed largely to the growth of Tier 1 capital while the contribution of intangible assets has been negative (Figure 1d).

(Figure 1b). However, Tier 1 capital has contributed to the growth rate of capital (Figure 1c). Reserves have contributed largely to the growth of Tier 1 capital while the contribution of intangible assets has been negative (Figure 1d).")

198

FIGURE 1. SOLVENCY RATIOS OF COMMERCIAL AND SAVINGS BANKS IN SPAIN (1)

Source: Bank of Spain (Financial Stability Report, n.8, 2005, May)

")

199

FIGURE 1. SOLVENCY RATIOS OF COMMERCIAL AND SAVINGS BANKS IN SPAIN (2)

Source: Bank of Spain (Financial Stability Report, n.8, 2005, May)

")

200

Other Risks Faced by Financial Intermediaries

201

Risks Faced by Financial Intermediaries

Liquidity Risk Interest Rate Risk Market Risk Off-Balance-Sheet Risk Foreign Exchange Risk Country or Sovereign Risk Technology Risk Operational Risk Insolvency Risk

202

Market Risk Incurred in trading of assets and liabilities (and derivatives). Examples: Barings & decline in ruble. DJIA dropped 12.5 percent in two-week period July, 2002. Heavier focus on trading income over traditional activities increases market exposure. Trading activities introduce other perils as was discovered by Allied Irish Bank’s U.S. subsidiary, AllFirst Bank when a rogue trader successfully masked large trading losses and fraudulent activities involving foreign exchange positions

203

Off-Balance-Sheet Risk

Striking growth of off-balance-sheet activities Letters of credit Loan commitments Derivative positions Speculative activities using off-balance-sheet items create considerable risk

204

Technology and Operational Risk

Risk that technology investment fails to produce anticipated cost savings. Risk that technology may break down. CitiBank’s ATM network, debit card system and on-line banking out for two days Wells Fargo Bank of New York: Computer system failed to recognize incoming payment messages sent via Fedwire although outgoing payments succeeded

205

Technology and Operational Risk

Operational risk not exclusively technological Employee fraud and errors Losses magnified since they affect reputation and future potential Merrill Lynch $100 million penalty

206

Country or Sovereign Risk

Result of exposure to foreign government which may impose restrictions on repayments to foreigners. Often lack usual recourse via court system. Examples: Argentina Russia South Korea Indonesia Malaysia Thailand.

207

Country or Sovereign Risk

In the event of restrictions, reschedulings, or outright prohibition of repayments, FIs’ remaining bargaining chip is future supply of loans Weak position if currency collapsing or government failing Role of IMF Extends aid to troubled banks Increased moral hazard problem if IMF bailout expected

208

Liquidity Risk Risk of being forced to borrow, or sell assets in a very short period of time. Low prices result. May generate runs. Runs may turn liquidity problem into solvency problem. Risk of systematic bank panics. Example: 1985, Ohio savings institutions insured by Ohio Deposit Guarantee Fund Interaction of credit risk and liability risk Role of FDIC (see Chapter 19)

")

209

Insolvency Risk Risk of insufficient capital to offset sudden decline in value of assets to liabilities. Continental Illinois National Bank and Trust Original cause may be excessive interest rate, market, credit, off-balance-sheet, technological, FX, sovereign, and liquidity risks.

210

Insolvency Risk Management

Net worth a measure of an FI’s capital that is equal to the difference between the market value o its assets and the market value of its liabilities Book Value value of assets and liabilities based on their historical costs Market value or mark-to-market value basis balance sheet values that reflect current rather than historical prices

211

Central Bank & Interest Rate Risk

Federal Reserve Bank: U.S. central bank Open market operations influence money supply, inflation, and interest rates Oct-1979 to Oct-1982, nonborrowed reserves target regime – did not work Implications of reserves target policy: Increases importance of measuring and managing interest rate risk. Effects of interest rate targeting. Lessens interest rate risk Greenspan view: Risk Management Focus on Federal Funds Rate Simple announcement of Fed Funds increase, decrease, or no change.

212

Implications Emphasizes importance of: Measurement of exposure

Control mechanisms for direct market risk—and employee created risks Hedging mechanisms

213

Market Risk Market risk is the uncertainty resulting from changes in market prices . Affected by other risks such as interest rate risk and FX (foreign exchange) risk It can be measured over periods as short as one day. Usually measured in terms of dollar exposure amount or as a relative amount against some benchmark.

risk. It can be measured over periods as short as one day. Usually measured in terms of dollar exposure amount or as a relative amount against some benchmark.")

214

Market Risk Measurement

Important in terms of: Management information Setting limits Resource allocation (risk/return tradeoff) Performance evaluation Regulation BIS and Fed regulate market risk via capital requirements leading to potential for overpricing of risks Allowances for use of internal models to calculate capital requirements

Performance evaluation. Regulation. BIS and Fed regulate market risk via capital requirements leading to potential for overpricing of risks. Allowances for use of internal models to calculate capital requirements.")

215

(MATERIAL DEL PROFESOR)

Tema 6 ANATOMÍA DE LAS CRISIS BANCARIAS: LA CRISIS CREDITICIA DE 2007 Y 2008 (MATERIAL DEL PROFESOR)

")

216

Asymmetric information and its implications

Banking crises Definition of a banking crisis. Recent evidence and why we should care. Sources of banking crises. Regulatory responses Strengthening regulation and supervision. Reforming the financial safety net (deposit insurance and lender of last resort).

.")

217

Asymmetric Information and its Implications

218

Definition Information is asymmetric when one party to an economic relationship or transaction has less information about it than the other party or parties. Pervasive role in financial markets. Lenders often do not know the riskiness of the borrower applying for a loan; Lenders may not be able to observe whether the borrower will invest in a safe or risky project.

219

The very existence of financial institutions can be explained on asymmetric-information grounds.