Download presentation

Presentation is loading. Please wait.

1

Monetary Policy and a Stock Market Boom-Bust Cycle

Lawrence Christiano, Roberto Motto and Massimo Rostagno

2

Inflation has been relatively stable for a while

Attention has shifted to other issues: stock market volatility

3

Stock market has been volatile:

Is it ‘excessively’ volatile in the welfare sense? What role (if any) does (should) monetary policy play? Conventional wisdom – Bernanke-Gertler: ‘leave it alone’ In any case, inflation targeting will automatically stabilize

does (should) monetary policy play Conventional wisdom – Bernanke-Gertler: ‘leave it alone’ In any case, inflation targeting will automatically stabilize.")

4

Inflation appears to be falling

during the start-up of boom-bust episodes in US.

5

‘Stock Market Boom-Bust Cycle’

Episode in which: Stock prices, consumption, investment, output, employment rise sharply and then fall Inflation low during boom US examples: Interwar period Mid 1950s - mid 1970s Mid 1990s - present We’re going back to the drawing board to build a model of a boom-bust cycle.

6

Rational Theory of Boom-Bust

Follow Beaudry-Portier (see also more recently Jaimovich-Rebelo) Boom-bust cycle triggered by: Expectation that technology will be strong in future Expectation ultimately not realized Examples: Fiber-optic cable Motorola satellites In principle, there are lots of models you could build. At the broadest level there is the question of whether it is a rational one or a bubble model. We follow the lead of Beaudry-Portier and build a rational bubble.

Boom-bust cycle triggered by: Expectation that technology will be strong in future. Expectation ultimately not realized. Examples: Fiber-optic cable. Motorola satellites. In principle, there are lots of models you could build. At the broadest level there is the question of whether it is a rational one or a bubble model. We follow the lead of Beaudry-Portier and build a rational bubble.")

7

Key Findings Start by trying to build a non-monetary theory of boom-bust cycle With investment adjustment costs, habit persistence, can almost get successful theory However, miss on several key dimensions Stock market goes wrong way, highly volatile real rate, no persistence When we integrate sticky (allocative) wages and an inflation-targeting central bank, we obtain a more successful theory. perhaps boom-bust cycles reflect interaction of sticky wages and inflation targeting monetary policy an example of Levin, et al point that inflation targeting not optimal when wages are sticky

wages and an inflation-targeting central bank, we obtain a more successful theory. perhaps boom-bust cycles reflect interaction of sticky wages and inflation targeting monetary policy. an example of Levin, et al point that inflation targeting not optimal when wages are sticky.")

8

Outline Boom-bust in non-monetary economy

Bring in sticky wages/prices and monetary policy as simply as possible Redo analysis in model with additional financial frictions banking system (CCE), agency costs (BGG) permits addressing role of credit and monetary aggregates

, agency costs (BGG) permits addressing role of credit and monetary aggregates.")

10

Parameterization of RBC Model

Model is specialized version of model with many frictions estimated for US by Christiano-Motto-Rostagno (2006) Parameters: Steady state:

Parameters: Steady state:")

11

Results for RBC Model Habit persistence in preference and adjustment costs on change in investment crucial for getting ‘close’ to stock-market boom-bust… However, Stock market wrong Real interest rate highly volatile No persistence

12

All wrong!

13

Adding habit persistence and investment adjustment costs.

14

Using Static Adjustment Costs Doesn’t Help

Static (‘standard’ adjustment costs)

")

16

Static adjustment costs

don’t help.

17

Conclusions so far: Need:

habit persistence need adjustment costs in changing the flow of investment (for economic interpretation of this formulation, see Matsuyama and Lucca). Still, not good enough…..not great on persistence Increase lead time in signal (p) from 4 to 12

. Still, not good enough…..not great on persistence. Increase lead time in signal (p) from 4 to 12.")

20

What do Agents Expect After Seeing a Signal?

23

Why Does Price of Capital Fall?

Standard Present Value Formula: Real rate spikes up – not surprising PV falls

24

Why Does Price of Capital Fall?...

Price of capital from implication that price equals marginal cost: High anticipated investment implies that investment today reduces future adjustment costs

25

‘Monetizing the Model’

We add: Calvo sticky price setup (‘Phillips curve’) Calvo sticky wage equations Intertemporal Euler equation for bonds Take limit where money demand goes to zero Monetary policy rule

Calvo sticky wage equations. Intertemporal Euler equation for bonds. Take limit where money demand goes to zero. Monetary policy rule.")

26

Goods Production Final goods: Intermediate goods:

firms reoptimize and instead set price as follows:

27

Sticky Wages (Erceg, Henderson, Levin)

Homogeneous labor assembled from specialized household labor services: households reoptimize wage in given period and set their wage as follows:

28

Demand for Money Money in the utility function:

We drive coefficient on money balances to zero in equilibrium conditions.

29

Monetary Policy ‘Target interest rate’ Actual interest rate:

Parameters of monetary model

31

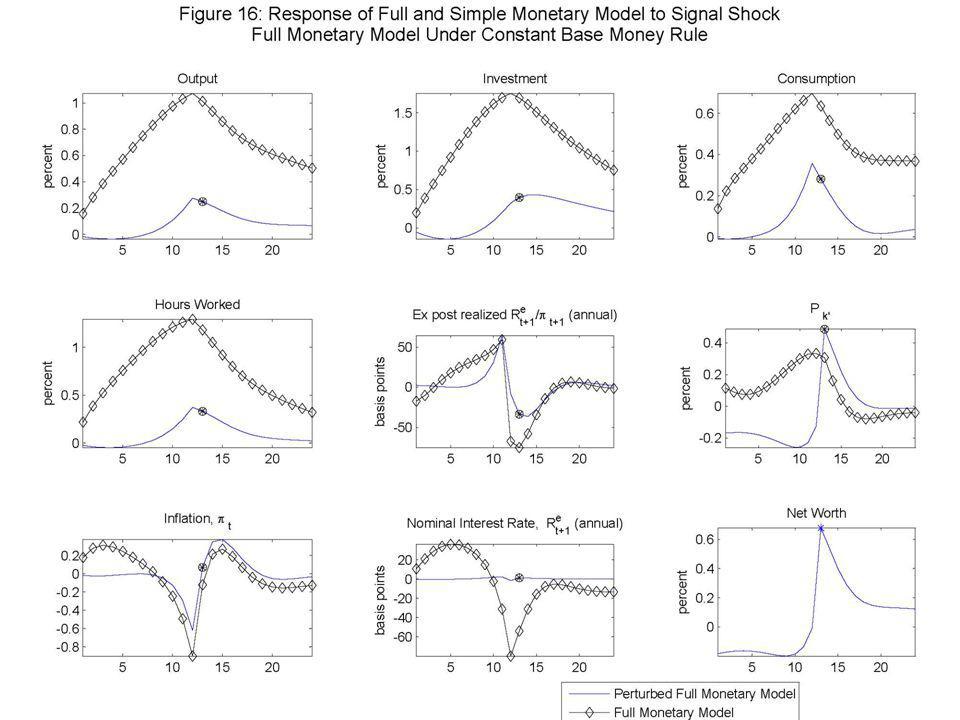

Findings Now have a (sort of) reasonable model of boom-bust

highly persistent ex post real interest rate moves only a very small amount Stock price moves in ‘right’ way (though a little anemic). Quantity movements in monetary model swamp movements in RBC model Boom-bust (though triggered by real event) is primarily a monetary policy phenomenon

. Quantity movements in monetary model swamp movements in RBC model. Boom-bust (though triggered by real event) is primarily a monetary policy phenomenon.")

32

Basic Diagnosis Application of logic in

Erceg, Christopher, Dale Henderson, and Andrew Levin, 2000, `Optimal Monetary Policy with Staggered Wage and Price Contracts,' Journal of Monetary Economics, 46, Levin, A., Onatski, A., Williams, J., Williams, N., "Monetary Policy under Uncertainty in Microfounded Macroeconometric Models." In: NBER Macroeconomics Annual 2005, Gertler, M., Rogoff, K., eds. Cambridge, MA: MIT Press. Sticky wages are the key, sticky prices unimportant Inflation targeting important Real wage ‘should’ rise in boom, but is prevented: wage is sticky price is sticky downward, because of monetary policy

34

Sticky prices don’t matter!

35

Sticky wages matter!

36

Wage indexation matters

37

Inflation targeting important!

38

‘Full’ Model has Credit, Monetary Aggregates

Model incorporates banking sector, as in Chari, Christiano and Eichenbaum. M1, M3, demand deposits, currency, bank reserves. Financial frictions as in Bernanke, Gertler and Gilchrist. Total credit (borrowing of working capital by banks, plus loans to entrepreneurs).

.")

39

M1 ~ currency + demand deposis M2/M3 ~ M1 + savings deposits

Credit ~ total borrowing (includes time deposits, but not currency) Entrepreneurs: own and rent out capital Firms: need working capital to pay factors Banks (hold reserves) Demand deposits, Savings deposits, Time deposits Households

Entrepreneurs: own and rent out. capital. Firms: need working. capital to pay factors. Banks. (hold reserves) Demand deposits, Savings deposits, Time deposits. Households.")

40

Findings BGG financial frictions attenuate somewhat the effects of boom-bust Rationalizes monetary policy of looking at credit.

45

Conclusion With habit persistence and cost-of-change adjustment costs, can make progress on generating stock market boom-bust. But, problems… Bring in sticky wages and inflation targeting, and can generate boom-bust Perhaps monetary policy should react to other variables, such as credit growth.

Similar presentations

Over the long term, money is highly positively correlated with prices, but uncorrelated with.>")

to Asset Market (MP):>")

SW (2003, 2007) “Can models with moderate degrees of nominal rigidities generate inertial inflation and persistent output movements in response.>")