Download presentation

Presentation is loading. Please wait.

1

European Steel in a Globalized Market

Prof. Dr.-Ing. Dieter Ameling Senior Counselor ThyssenKrupp Steel former President German Steel Federation former Chairman Steel Institute VDEh ABM’s 63rd Annual Congress July 28 – August 1, 2008 Santos – SP - Brazil

2

European Steel in a Globalized Market

Steel in a globalized environment Raw materials – short and expensive European steel industry – sustainable, innovative and competitive Steel and the energy and climate policy of the EU EUROFER‘s proposal to reduce the steel industries CO2-emissions worldwide

3

Explosion of World Crude Steel Production and Continuous Casting

Stahl-Zentrum

4

The European Union – 27 Member States

Stahl-Zentrum

5

The Ranking of Gross Domestic Product (GDP) by Actual Prices 2006

Stahl-Zentrum

6

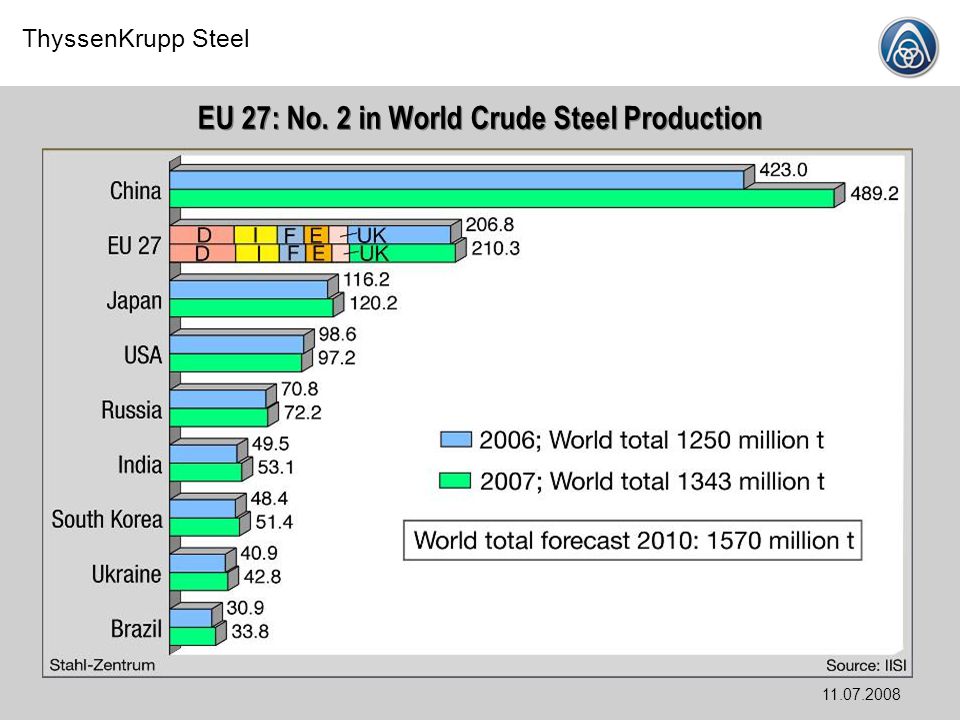

EU 27: No. 2 in World Crude Steel Production

7

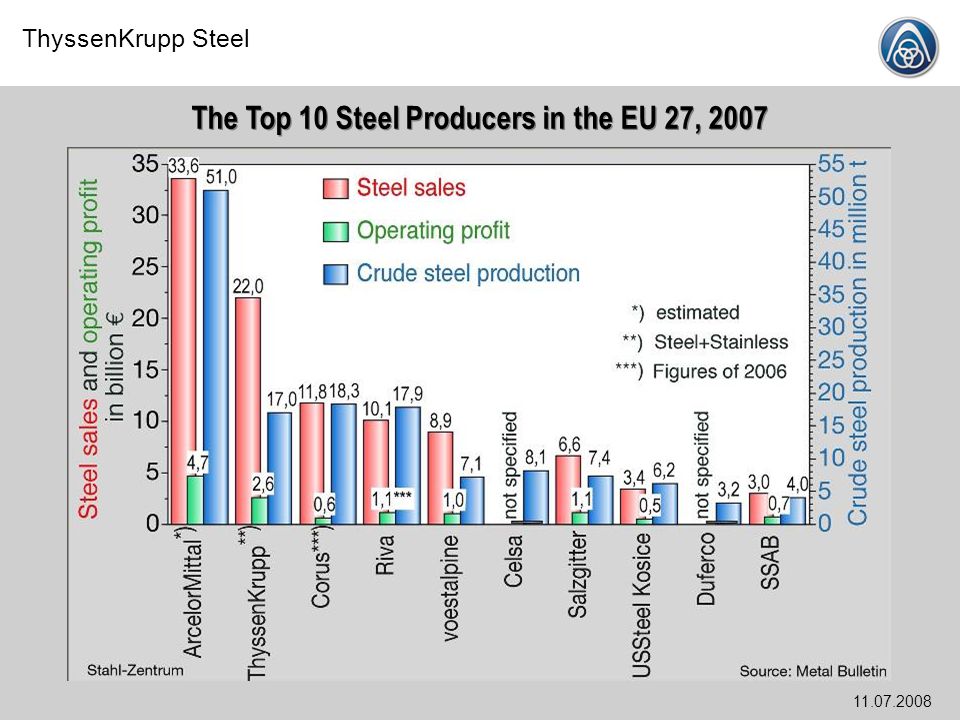

The Top 10 Steel Producers in the EU 27, 2007

8

World Trade in Steel Excludes internal trade within the EU 25

Source: ISSB Stahl-Zentrum,

9

Main Regional Steel Trade Flows (2007)

China No. 1 Steel Exporter EU 27 No. 1 Steel Importer Source: ISSB Stahl-Zentrum,

10

China: Imports and Exports

Steel Mill Products up to May 2008 and forecast 2008 Stahl-Zentrum

11

EU 27: Chinas Export Target No. 1 outside Asia in 2007

Total export volume : 68,3 Mill. t Asia total: 52,7 % Source: Trade Statistic German Steel Federation Stahl-Zentrum,

12

Actual Antidumping Complaints of EUROFER

No. 1 against EU 27 hot dipped coated sheet imports from China Str 28Mrch08 and No. 2 EU 27 stainless cold rolled sheet imports from China, Korea, Taiwan No. 3 EU 27 wire rod imports from China and Turkey Source: official EU trade statistic (Eurostat) with own calculations Stahl-Zentrum,

with own calculations. Stahl-Zentrum,")

13

The Influence of the Chinese Government on the Industry

Fiscal development aid Preferential Loans and Direct Credit Governmental regulation of production and external trade Support of individual companies Free or cheapened electric power supply Land grants Governmental support of developments of raw material sources Disregarding of environmental and occupational safety standards Subsidized freight rates Stahl-Zentrum

14

Blast Furnace in China Stahl-Zentrum Source: GEO 11/2007

15

Coking Plant in China Stahl-Zentrum Source: GEO 11/2007

16

European Steel in a Globalized Market

Steel in a globalized environment Raw materials – short and expensive European steel industry – sustainable, innovative and competitive Steel and the energy and climate policy of the EU EUROFER‘s proposal to reduce the steel industries CO2-emissions worldwide

17

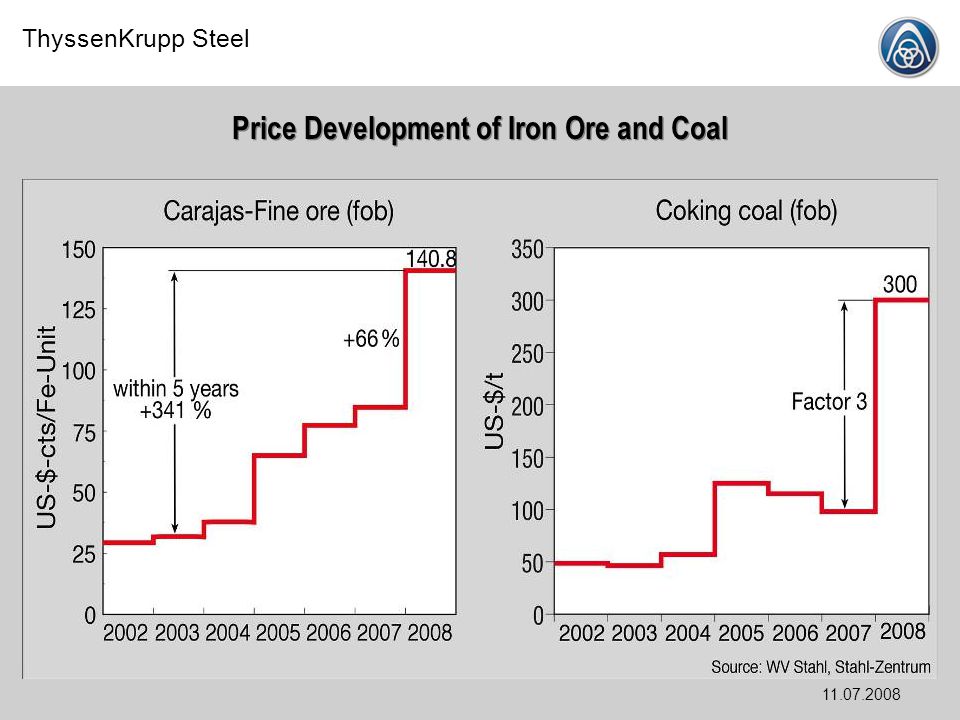

Price Development of Iron Ore and Coal

18

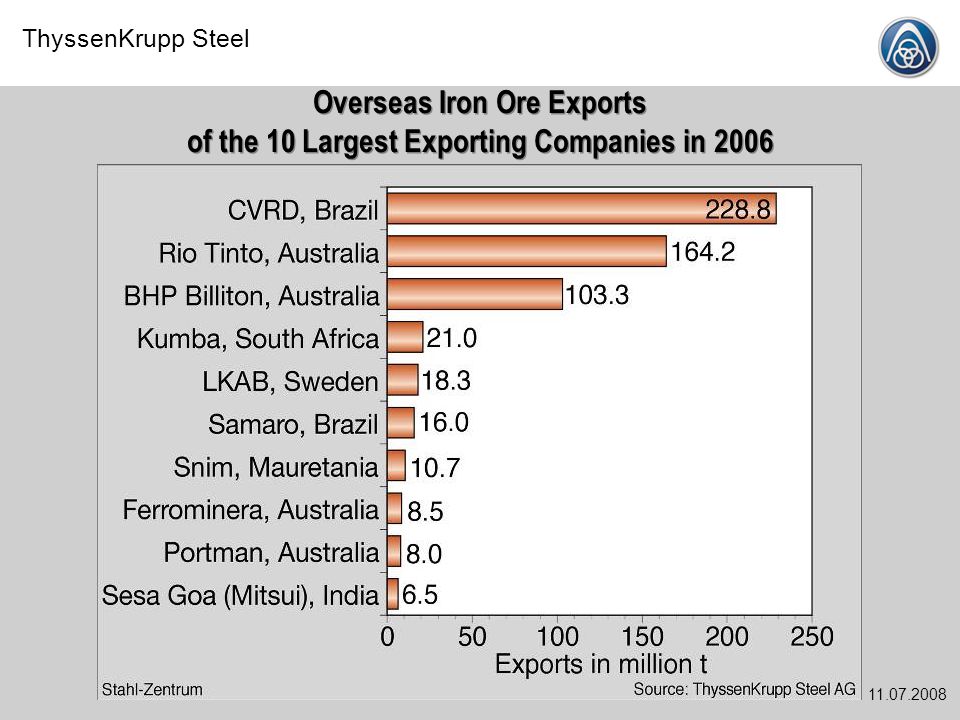

Overseas Iron Ore Exports of the 10 Largest Exporting Companies in 2006

19

Conditions for the Application of the EC Merger Regulation

Worldwide turnover of all joining companies with more than 5 Billion EUR and Rio Tinto: 22 Billion $ (2006), BHP: 39 Billion $ (2007) b. turnover in the EU of at least two joining companies with more than 250 Million EUR each and Rio Tinto: 3,9 Billion $ (2006), BHP: 11 Billion $ (2007) c. the joining companies shouldn‘t have a share of more than 2/3 of their turnover within the same member state. () We require an intervention of Brussels to stop the merger of BHP and Rio Tinto! Stahl-Zentrum

, BHP: 39 Billion $ (2007) b. turnover in the EU of at least two joining companies with more than 250 Million EUR each and. Rio Tinto: 3,9 Billion $ (2006), BHP: 11 Billion $ (2007) c. the joining companies shouldn‘t have a share of more than 2/3 of their turnover within the same member state. () We require an intervention of Brussels to stop the merger of BHP and Rio Tinto! Stahl-Zentrum")

20

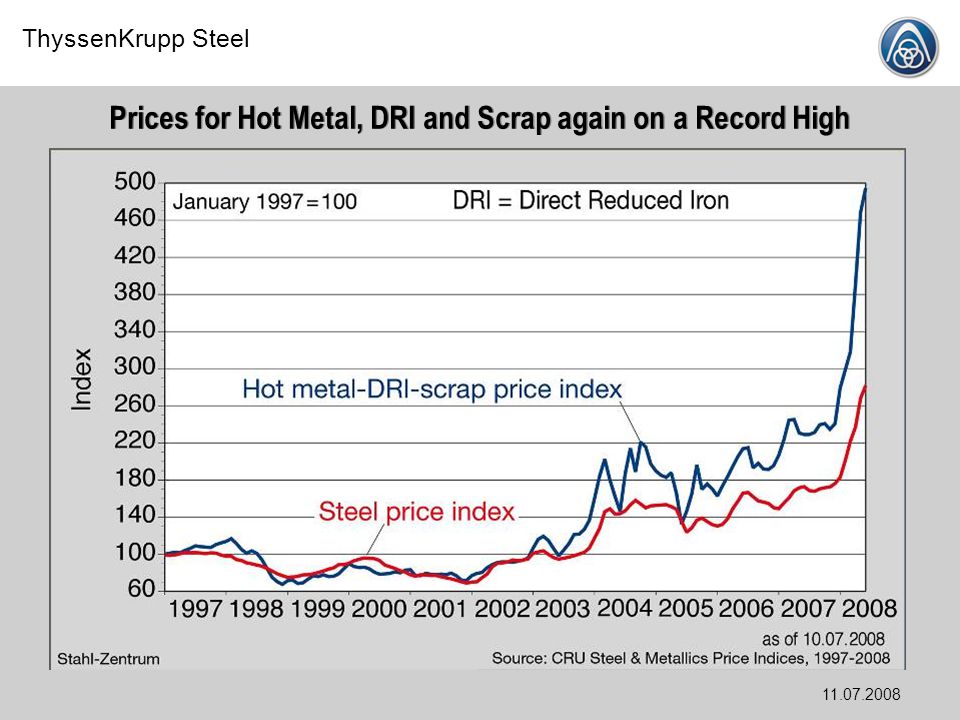

Prices for Hot Metal, DRI and Scrap again on a Record High

21

European Steel in a Globalized Market

Steel in a globalized environment Raw materials – short and expensive European steel industry – sustainable, innovative and competitive Steel and the energy and climate policy of the EU EUROFER‘s proposal to reduce the steel industries CO2-emissions worldwide

22

Stahl-Zentrum

23

Indicators of Sustainable Steel

Stahl-Zentrum

24

Reducing Agents Consumption of Blast Furnaces in the World, 2006

Stahl-Zentrum

25

Energy Efficiency and CO2-Emissions of the German Steel Industry

Stahl-Zentrum

26

Innovations for the Future

Stahl-Zentrum

27

Climate Change – Steel is the best Choice Steel – driver of innovations to increase efficiency of resources Stahl-Zentrum

28

Climate Change – Steel is the best Choice Steel – driver of innovations to increase efficiency of resources Stahl-Zentrum

29

European Steel in a Globalized Market

Steel in a globalized environment Raw materials – short and expensive European steel industry – sustainable, innovative and competitive Steel and the energy and climate policy of the EU EUROFER‘s proposal to reduce the steel industries CO2-emissions worldwide

30

Renewable Energy and Climate Change Package of the European Commission of 23.01.08:

The plan calls for a: „These targets are very ambitious: today 8.5% of energy is renewable. To achieve a 20% share by 2020 will require major efforts across all sectors of the economy and by all Member States.“ 2005 is the new basis for all calculations within the framework of this package. 20% increase in energy efficiency 20% reduction in greenhouse gas (GHG) emissions 20% share of renewables in overall EU energy consumption by 2020 10% biofuel component in vehicle fuel by 2020 Stahl-Zentrum

emissions. 20% share of renewables in overall EU energy consumption by % biofuel component in vehicle fuel by Stahl-Zentrum")

31

GHG Target: -20% compared to 1990 -14% compared to 2005 EU ETS

Non ETS sectors -10% compared to 2005 27 Member State targets, stretching from -20% to +20% Source: European Commission, DG Environment

32

The Energy and Climate Package drastically Reduces

the Crude Steel Production within the EU -21 % CO2 reduction from to 2020 Specific CO2-emissions could decrease from 1.7 to 1.56 t CO2/t steel Compared to expected steel production in 2020 of 236 Mt this would only allow a reduced steel production of Mt = Mt = % Steel Stahl-Zentrum

33

The Energy and Climate Package of the European Commission of 23. 01

The Energy and Climate Package of the European Commission of Drives the Industry Away For the energy-intensive industries sufficient allowances are indispensable to prevent relocation to outside Europe: The needed certificates have to be allocated free of charge. The foreseen auctioning would lead to a massive loss in international competitiveness. A general sectoral CO2 reduction target of 21 % cannot be fulfilled by the steel industry. The energy-intensive industries are characterised by process related emissions. Today, they are working at the minimum level. Further electricity price increases through auctioning obligation for power producers cannot be borne in the international competition. Industry needs investment certainty. Clear decisions must be made. Otherwise investments would be stopped, which would result in a lack of competitiveness as well. Stahl-Zentrum

34

The Global Energy Related CO2 Emissions are further Increasing The Measures of EU 27 without any realistic Effect Stahl-Zentrum

35

CO2 Emissions Trading in the European Union – Does it make Sense?

Stahl-Zentrum

36

European Steel in a Globalized Market

Steel in a globalized environment Raw materials – short and expensive European steel industry – sustainable, innovative and competitive Steel and the energy and climate policy of the EU EUROFER‘s proposal to reduce the steel industries CO2-emissions worldwide

37

Disadvantages of the Existing Emissions Trading System

Absolute caps are equivalent to caps on production and lead to relocations to outside the EU. The reduction targets are set „top down“ and are not consistent with technological reduction potentials. Because the emissions trading directive does only refer to direct emissions the reduction potentials of the steel industry are not addressed adequately. The pricing-in of allowances which were allocated free of charge as well as auctioning lead to inadequate increases of electricity prices. Stahl-Zentrum

38

Main Characteristics of the Baseline and Credit System

An ETS tailor-made for the steel industry. Emissions are determined in an integrated way taking into consideration all stages of production. Inputs like coke or electricity or credits resulting from using by-products do also count. The average amount of European emissions serves as a basis for the allocation of allowances. The scheme brings about continuous improvement in terms of efficiency: The average amount of European emissions serving as a reference for allocation, incentives for emission cuts are created what directly impacts on the average emissions amount ("moving target"). Ex-post-allocation taking account of the production quantity instead of absolute emissions ceilings. Stahl-Zentrum

. Ex-post-allocation taking account of the production quantity instead of absolute emissions ceilings. Stahl-Zentrum")

39

Facts about the Emissions Trading System for Steel

Stahl-Zentrum

40

Advantages of the Baseline and Credit System

Existing technological reduction potentials, but also the limits concerning process emissions are regarded. The system results in continuing efficiency improvements because the orientation to the emission average gives incentives to reduce emissions. This influences the emission baseline („moving target“). Production growth is not constrained. The baseline and credit emissions trading system targets only at efficiency. No incentives for relocations of production to outside the EU. The system is more attractive for states outside the EU and their steel industry. Stahl-Zentrum

. Production growth is not constrained. The baseline and credit emissions trading system targets only at efficiency. No incentives for relocations of production to outside the EU. The system is more attractive for states outside the EU and their steel industry. Stahl-Zentrum")

41

European Steel in a Globalized Market

Summary The world steel production continuous to grow. EU 27: No. 2 in world crude steel production China became the No. 1 steel exporter in 2007. Raw materials remain short and expensive. European steel industry – sustainable, innovative and competitive The Energy and climate package of the European Commission of drives the industry out of Europe. The only solution is a sectoral approach. Stahl-Zentrum

Similar presentations

Henriëtte Bersee Henriëtte Bersee Environment Counselor Environment Counselor Royal Netherlands Embassy Royal Netherlands.>")