Download presentation

Presentation is loading. Please wait.

1

Developments in Deferred Acquisition Costs (DAC) for Variable Annuities Secession 59PD - May 29, 2003 Bradley Barks, FSA, CPA, MAAA CFO and Senior Vice President Global Preferred Holdings, Inc. Bradley Barks, FSA, CPA, MAAA CFO and Senior Vice President Global Preferred Holdings, Inc.

2

Presentation Summary I. Recent Results of Public Companies II. Comparison of Methods to Address Equity Market Volatility III. Sales Inducements - Long Duration SOP IV. Loss Recognition Issues V. Internal Replacements SOP I. Recent Results of Public Companies II. Comparison of Methods to Address Equity Market Volatility III. Sales Inducements - Long Duration SOP IV. Loss Recognition Issues V. Internal Replacements SOP

3

Recent Results of Public Companies

4

Summary Methods and Assumptions DAC Adjustments Summary Methods and Assumptions DAC Adjustments

5

Recent Results of Public Companies Methods & Assumptions

6

Recent Results of Public Companies Adjustments to DAC Balances

7

Comparison of Methods to Address Equity Market Volatility

8

Summary Basis of Long-term Assumptions and Methods How Far Out on the Tail Are We? How Bad Might It Be 5 to 10 Years from Issue? Ideal Method – Achieves Best Matching Comparison of Methods to the Ideal Summary Basis of Long-term Assumptions and Methods How Far Out on the Tail Are We? How Bad Might It Be 5 to 10 Years from Issue? Ideal Method – Achieves Best Matching Comparison of Methods to the Ideal

9

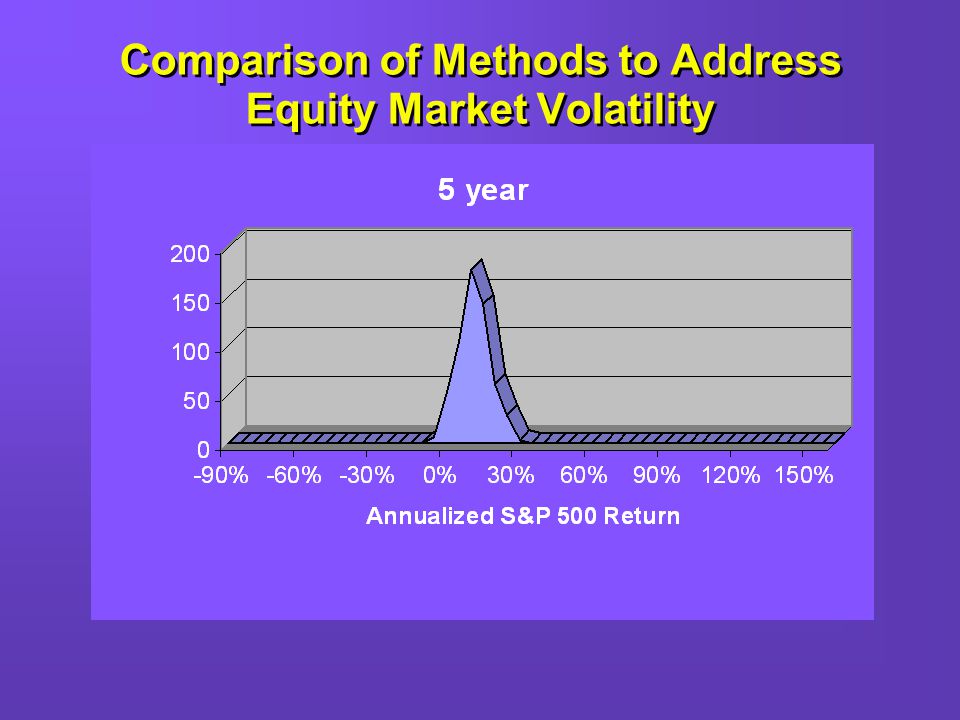

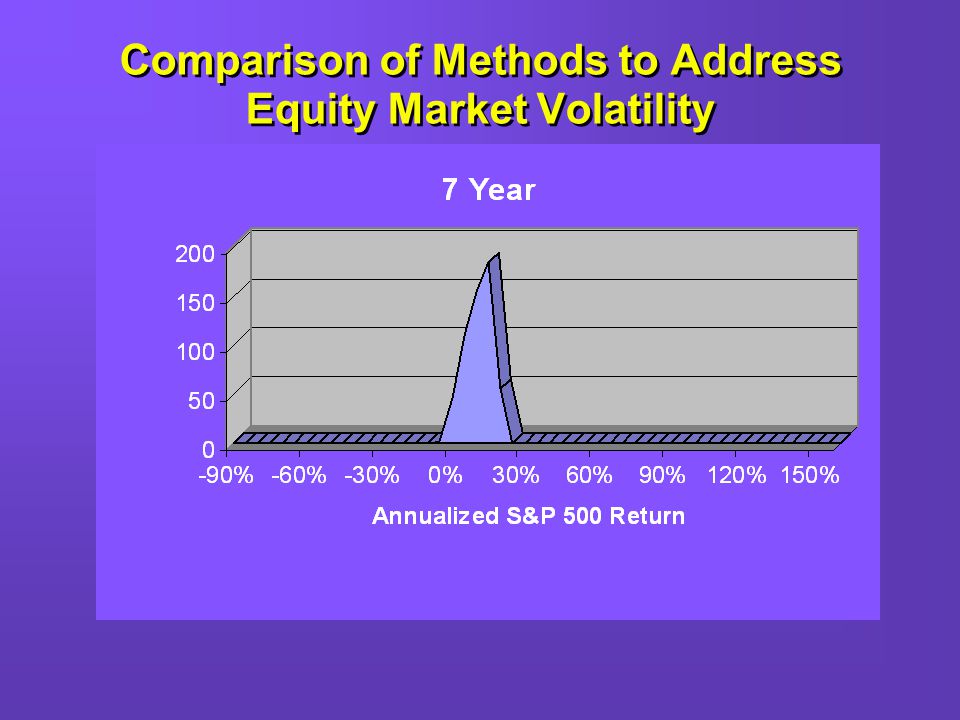

Comparison of Methods to Address Equity Market Volatility

18

Principles of Amortization Methods Match Revenue and Expense Revenue is EGP Expense is DAC (GMDB, Sales Inducements) Problem: We dont know what the future EGPs will be AND they are extremely volatile in the short-term but less volatile in the long-term. Principles of Amortization Methods Match Revenue and Expense Revenue is EGP Expense is DAC (GMDB, Sales Inducements) Problem: We dont know what the future EGPs will be AND they are extremely volatile in the short-term but less volatile in the long-term.

Problem: We dont know what the future EGPs will be AND they are extremely volatile in the short-term but less volatile in the long-term..")

19

Comparison of Methods to Address Equity Market Volatility How to Compare Different Methods? If we knew what the EGPs would be, we would have a perfect match of Revenue and Expense. The Ideal Method would be the Crystal Ball Method Comparison Can Be Made Relative to The Crystal Ball Method. How to Compare Different Methods? If we knew what the EGPs would be, we would have a perfect match of Revenue and Expense. The Ideal Method would be the Crystal Ball Method Comparison Can Be Made Relative to The Crystal Ball Method.

20

Comparison of Methods to Address Equity Market Volatility Numerical Comparisons Assumptions Single Premium $10,000 Avg. Long-term Fund Performance 9% M&E Charges 140 b.p. Expenses 50 b.p. Issue Expenses 7% of Prem. Surrender Charges 7%,6%,5%,4%,3%,2%,1%,0% thereafter Surrender Rates 4% except 15% in year 8 Numerical Comparisons Assumptions Single Premium $10,000 Avg. Long-term Fund Performance 9% M&E Charges 140 b.p. Expenses 50 b.p. Issue Expenses 7% of Prem. Surrender Charges 7%,6%,5%,4%,3%,2%,1%,0% thereafter Surrender Rates 4% except 15% in year 8

21

Comparison of Methods to Address Equity Market Volatility Numerical Comparisons Summary of Methods Crystal Ball – Assumes that actual gross profits were known at issue. Results in perfect matching. Traditional Method – Assumes that expected gross profits are based on the current fund value projected at the average long- term fund performance rate. Mean Reversion (modified for simplicity) – Traditional method except that the average long-term fund performance rate is increased or decreased to a cap (14%) or floor (0%) until the FV equals the FV projected at issue. Thereafter, the average long- term fund performance rate is used. Credibility Method – Assumes that EGPs projected at each valuation date are given 10% weight with the the rest of the weight given to the original EGPs. All EGPs given equal weight after year 10. Numerical Comparisons Summary of Methods Crystal Ball – Assumes that actual gross profits were known at issue. Results in perfect matching. Traditional Method – Assumes that expected gross profits are based on the current fund value projected at the average long- term fund performance rate. Mean Reversion (modified for simplicity) – Traditional method except that the average long-term fund performance rate is increased or decreased to a cap (14%) or floor (0%) until the FV equals the FV projected at issue. Thereafter, the average long- term fund performance rate is used. Credibility Method – Assumes that EGPs projected at each valuation date are given 10% weight with the the rest of the weight given to the original EGPs. All EGPs given equal weight after year 10.

– Traditional method except that the average long-term fund performance rate is increased or decreased to a cap (14%) or floor (0%) until the FV equals the FV projected at issue. Thereafter, the average long- term fund performance rate is used. Credibility Method – Assumes that EGPs projected at each valuation date are given 10% weight with the the rest of the weight given to the original EGPs. All EGPs given equal weight after year 10. Numerical Comparisons Summary of Methods Crystal Ball – Assumes that actual gross profits were known at issue. Results in perfect matching. Traditional Method – Assumes that expected gross profits are based on the current fund value projected at the average long- term fund performance rate. Mean Reversion (modified for simplicity) – Traditional method except that the average long-term fund performance rate is increased or decreased to a cap (14%) or floor (0%) until the FV equals the FV projected at issue. Thereafter, the average long- term fund performance rate is used. Credibility Method – Assumes that EGPs projected at each valuation date are given 10% weight with the the rest of the weight given to the original EGPs. All EGPs given equal weight after year 10..")

22

Comparison of Methods to Address Equity Market Volatility

25

Numerical Comparisons Observations: Crystal Ball – Results in perfect matching. Overall All methods perform well when market performance is constant. 75% of the 12–month periods had returns greater than 15% or less than 5%. 85% of 3-month periods were outside of this range. (Using S&P 500 for periods starting at beginning of the month from 1950 thru 2002.) Traditional Method –Results in very poor matching in volatile markets. Mean Reversion – Effectively dampens poor matching associated with the Traditional method. Tends to become volatile toward end of amortization period. Credibility Method – Good matching over entire amortization period. Numerical Comparisons Observations: Crystal Ball – Results in perfect matching. Overall All methods perform well when market performance is constant. 75% of the 12–month periods had returns greater than 15% or less than 5%. 85% of 3-month periods were outside of this range. (Using S&P 500 for periods starting at beginning of the month from 1950 thru 2002.) Traditional Method –Results in very poor matching in volatile markets. Mean Reversion – Effectively dampens poor matching associated with the Traditional method. Tends to become volatile toward end of amortization period. Credibility Method – Good matching over entire amortization period.

Traditional Method –Results in very poor matching in volatile markets. Mean Reversion – Effectively dampens poor matching associated with the Traditional method. Tends to become volatile toward end of amortization period. Credibility Method – Good matching over entire amortization period. Numerical Comparisons Observations: Crystal Ball – Results in perfect matching. Overall All methods perform well when market performance is constant. 75% of the 12–month periods had returns greater than 15% or less than 5%. 85% of 3-month periods were outside of this range. (Using S&P 500 for periods starting at beginning of the month from 1950 thru 2002.) Traditional Method –Results in very poor matching in volatile markets. Mean Reversion – Effectively dampens poor matching associated with the Traditional method. Tends to become volatile toward end of amortization period. Credibility Method – Good matching over entire amortization period..")

26

Comparison of Methods to Address Equity Market Volatility

28

Sales Inducements to Contract Holders - Non-traditional Long-duration Statement of Position (NTLD SOP)

")

29

Sales Inducements - NTLD SOP Summary Definition of Sales Inducements Accounting Treatment Disclosures Effective Date and Transition Summary Definition of Sales Inducements Accounting Treatment Disclosures Effective Date and Transition

30

Sales Inducements - NTLD SOP Definition Insurer must demonstrate that amounts are Incremental to amounts credited on similar contracts without sales inducements, AND Higher than the contracts expected ongoing crediting rates for periods beyond the inducement, as applicable, AND Must be part of the original contract Examples: Day-one bonus, persistency bonus, enhanced credited rate Applies to UL and Investment Contracts (Deferred Annuities) Definition Insurer must demonstrate that amounts are Incremental to amounts credited on similar contracts without sales inducements, AND Higher than the contracts expected ongoing crediting rates for periods beyond the inducement, as applicable, AND Must be part of the original contract Examples: Day-one bonus, persistency bonus, enhanced credited rate Applies to UL and Investment Contracts (Deferred Annuities)

Definition Insurer must demonstrate that amounts are Incremental to amounts credited on similar contracts without sales inducements, AND Higher than the contracts expected ongoing crediting rates for periods beyond the inducement, as applicable, AND Must be part of the original contract Examples: Day-one bonus, persistency bonus, enhanced credited rate Applies to UL and Investment Contracts (Deferred Annuities)")

31

Sales Inducements - NTLD SOP Accounting Treatment Recognized as part of the liability for policy benefits Cannot reflect surrenders in determining amounts to defer or amounts included in Liability for Policy Benefits Deferred and amortized New item: Deferred Sales Inducements Amortization same methodology and assumptions as DAC Amortization is included as a component of benefit expense Surrender assumption is included in amortization. Accounting Treatment Recognized as part of the liability for policy benefits Cannot reflect surrenders in determining amounts to defer or amounts included in Liability for Policy Benefits Deferred and amortized New item: Deferred Sales Inducements Amortization same methodology and assumptions as DAC Amortization is included as a component of benefit expense Surrender assumption is included in amortization.

32

Sales Inducements - NTLD SOP Disclosure Requirements Nature of costs capitalized and amortization method Amounts capitalized and amortized Unamortized balances Disclosure Requirements Nature of costs capitalized and amortization method Amounts capitalized and amortized Unamortized balances

33

Sales Inducements - NTLD SOP Transition Rules and Effective Date Effective for fiscal years beginning after December 15, 2003 Initial costs deferred prior to adoption are not adjusted Unamortized balances amortized according to SOP at initial application Cannot retroactively capitalize sales inducements not previously deferred Prospective No cumulative effects Must Adopt Retroactive to Beginning of a Fiscal Year Transition Rules and Effective Date Effective for fiscal years beginning after December 15, 2003 Initial costs deferred prior to adoption are not adjusted Unamortized balances amortized according to SOP at initial application Cannot retroactively capitalize sales inducements not previously deferred Prospective No cumulative effects Must Adopt Retroactive to Beginning of a Fiscal Year

34

Loss Recognition Issues

35

Summary Impact of GMDB Cost Sales Inducements Effect: Loss Recognition is permanent vs. DAC unlocking can be recaptured Summary Impact of GMDB Cost Sales Inducements Effect: Loss Recognition is permanent vs. DAC unlocking can be recaptured

36

Proposed SOP: Deferred Acquisition Costs On Internal Replacements

37

DAC on Internal Replacements Summary Background Supporting Literature Definition of Internal Replacement Accounting Treatment Effective Date and Transition Summary Background Supporting Literature Definition of Internal Replacement Accounting Treatment Effective Date and Transition

38

DAC on Internal Replacements Background Proposed Statement of Position released 3/14/03 Comments Due 5/14/03 Applies to DAC, Unearned Revenue Liability and Sales Inducements Note: Sales Inducements incurred because of a modification (i.e., were not contemplated in the original contract) can be deferred if the new contract is Not Substantially Different. (Contrary to NTLD - SOP) FINAL STATEMENT MAY CHANGE Background Proposed Statement of Position released 3/14/03 Comments Due 5/14/03 Applies to DAC, Unearned Revenue Liability and Sales Inducements Note: Sales Inducements incurred because of a modification (i.e., were not contemplated in the original contract) can be deferred if the new contract is Not Substantially Different. (Contrary to NTLD - SOP) FINAL STATEMENT MAY CHANGE

FINAL STATEMENT MAY CHANGE Background Proposed Statement of Position released 3/14/03 Comments Due 5/14/03 Applies to DAC, Unearned Revenue Liability and Sales Inducements Note: Sales Inducements incurred because of a modification (i.e., were not contemplated in the original contract) can be deferred if the new contract is Not Substantially Different. (Contrary to NTLD - SOP) FINAL STATEMENT MAY CHANGE.")

39

DAC on Internal Replacements Supporting Literature SFAS 60, Par. 28 SFAS 97, Par. 26,70-72 AICPA Practice Bulletin #8 (11/90) SFAS 91- Accounting for Non-refundable Fees and Costs Associated with Originating and Acquiring Loans and Indirect Costs of Leases SFAS 120 – Accounting and Reporting by Mutual Life Insurance Enterprises and for Certain Participating Contracts SFAS 140 – Accounting for Transfers and Servicing of Financial Assets and Extinguishment of Liabilities EITF # 96-19 – Guidance on Extinguishment of Debt Instruments Supporting Literature SFAS 60, Par. 28 SFAS 97, Par. 26,70-72 AICPA Practice Bulletin #8 (11/90) SFAS 91- Accounting for Non-refundable Fees and Costs Associated with Originating and Acquiring Loans and Indirect Costs of Leases SFAS 120 – Accounting and Reporting by Mutual Life Insurance Enterprises and for Certain Participating Contracts SFAS 140 – Accounting for Transfers and Servicing of Financial Assets and Extinguishment of Liabilities EITF # 96-19 – Guidance on Extinguishment of Debt Instruments

SFAS 91- Accounting for Non-refundable Fees and Costs Associated with Originating and Acquiring Loans and Indirect Costs of Leases SFAS 120 – Accounting and Reporting by Mutual Life Insurance Enterprises and for Certain Participating Contracts SFAS 140 – Accounting for Transfers and Servicing of Financial Assets and Extinguishment of Liabilities EITF # – Guidance on Extinguishment of Debt Instruments Supporting Literature SFAS 60, Par. 28 SFAS 97, Par. 26,70-72 AICPA Practice Bulletin #8 (11/90) SFAS 91- Accounting for Non-refundable Fees and Costs Associated with Originating and Acquiring Loans and Indirect Costs of Leases SFAS 120 – Accounting and Reporting by Mutual Life Insurance Enterprises and for Certain Participating Contracts SFAS 140 – Accounting for Transfers and Servicing of Financial Assets and Extinguishment of Liabilities EITF # – Guidance on Extinguishment of Debt Instruments.")

40

DAC on Internal Replacements Definition of Internal Replacement: Modification of the Contract Substantially Different Inherent Nature Changed Definition of Internal Replacement: Modification of the Contract Substantially Different Inherent Nature Changed

41

DAC on Internal Replacements Schematic of Statement Of Position Is the Modification an Internal Replacement? No Yes Is at least one of the criteria of substantially different (Par. 11) met? Also use examples in Par. 13- 18. Not Substantially Different Accounting Treatment Yes No Substantially Different Accounting Treatment Is there a Modification to the Contract? No Yes

met. Also use examples in Par Not Substantially Different Accounting Treatment Yes No Substantially Different Accounting Treatment Is there a Modification to the Contract. No Yes.")

42

DAC on Internal Replacements Modifications not considered an Internal Replacement Both Contemplated in the Original Contract AND Does Not Change the Inherent Nature of the Contract Examples in the SOP (Safe Harbors): Changes in Rates or Charges within Ranges Outlined in Original Contract without Changes in Benefits Changes in Allocations among investment alternatives (100% allocation is all right) Addition of Investment Alternative (only if Contract already has multiple alternatives) Election of an Inflation Adjustment Benefit Purchasing Paid-Up Additions Modifications not considered an Internal Replacement Both Contemplated in the Original Contract AND Does Not Change the Inherent Nature of the Contract Examples in the SOP (Safe Harbors): Changes in Rates or Charges within Ranges Outlined in Original Contract without Changes in Benefits Changes in Allocations among investment alternatives (100% allocation is all right) Addition of Investment Alternative (only if Contract already has multiple alternatives) Election of an Inflation Adjustment Benefit Purchasing Paid-Up Additions

: Changes in Rates or Charges within Ranges Outlined in Original Contract without Changes in Benefits Changes in Allocations among investment alternatives (100% allocation is all right) Addition of Investment Alternative (only if Contract already has multiple alternatives) Election of an Inflation Adjustment Benefit Purchasing Paid-Up Additions Modifications not considered an Internal Replacement Both Contemplated in the Original Contract AND Does Not Change the Inherent Nature of the Contract Examples in the SOP (Safe Harbors): Changes in Rates or Charges within Ranges Outlined in Original Contract without Changes in Benefits Changes in Allocations among investment alternatives (100% allocation is all right) Addition of Investment Alternative (only if Contract already has multiple alternatives) Election of an Inflation Adjustment Benefit Purchasing Paid-Up Additions")

43

DAC on Internal Replacements Not Substantially Different (must meet all conditions) No additional deposit, premium or charge is required above amounts contemplated in the contract No net decrease in Policy Balances No change from SFAS 60 to SFAS 97 or to SFAS91 or visa versa New Benefit does not become Primary Benefit Modification does not change Inherent Nature of Contract (more subjective) Not Substantially Different (must meet all conditions) No additional deposit, premium or charge is required above amounts contemplated in the contract No net decrease in Policy Balances No change from SFAS 60 to SFAS 97 or to SFAS91 or visa versa New Benefit does not become Primary Benefit Modification does not change Inherent Nature of Contract (more subjective)

No additional deposit, premium or charge is required above amounts contemplated in the contract No net decrease in Policy Balances No change from SFAS 60 to SFAS 97 or to SFAS91 or visa versa New Benefit does not become Primary Benefit Modification does not change Inherent Nature of Contract (more subjective) Not Substantially Different (must meet all conditions) No additional deposit, premium or charge is required above amounts contemplated in the contract No net decrease in Policy Balances No change from SFAS 60 to SFAS 97 or to SFAS91 or visa versa New Benefit does not become Primary Benefit Modification does not change Inherent Nature of Contract (more subjective)")

44

DAC on Internal Replacements Inherent Nature of Contract Consider any change including rider, amendment, exchange of contract or election of a feature within an existing contract Most significant Factors Kind and Degree of Mortality or Morbidity Risk Rights and Provisions for Determining Investment Return Legal Form of Change does not matter Election of Existing Feature may be Problematic Inherent Nature of Contract Consider any change including rider, amendment, exchange of contract or election of a feature within an existing contract Most significant Factors Kind and Degree of Mortality or Morbidity Risk Rights and Provisions for Determining Investment Return Legal Form of Change does not matter Election of Existing Feature may be Problematic

45

DAC on Internal Replacements Inherent Nature – Safe Harbors (examples) Additional Investment Alternatives (same as above) Addition of MVA provision (change only effects surrender charge) Addition of LTC Rider to Disability Contract (No Change in Primary Benefit) Addition of Enhancement of GMIB, GMAB or Annuitization Guarantee (Only Affects Benefits After Termination) Inherent Nature – Safe Harbors (examples) Additional Investment Alternatives (same as above) Addition of MVA provision (change only effects surrender charge) Addition of LTC Rider to Disability Contract (No Change in Primary Benefit) Addition of Enhancement of GMIB, GMAB or Annuitization Guarantee (Only Affects Benefits After Termination)

Additional Investment Alternatives (same as above) Addition of MVA provision (change only effects surrender charge) Addition of LTC Rider to Disability Contract (No Change in Primary Benefit) Addition of Enhancement of GMIB, GMAB or Annuitization Guarantee (Only Affects Benefits After Termination) Inherent Nature – Safe Harbors (examples) Additional Investment Alternatives (same as above) Addition of MVA provision (change only effects surrender charge) Addition of LTC Rider to Disability Contract (No Change in Primary Benefit) Addition of Enhancement of GMIB, GMAB or Annuitization Guarantee (Only Affects Benefits After Termination)")

46

DAC on Internal Replacements Inherent Nature – Failures (examples) Replace Term Life with Whole Life (adding Significant Component) Add GMDB to Contract with Insignificant Death Benefit or Visa Versa Replace Disability Contract with LTC Contract (Changes nature of Morbidity Risk) Replace UL with Life Contingent Payout Annuity Change from Discretionary to Formulaic Investment Crediting Methodology Replacement of Variable Contract with Fixed Contract or Visa Versa Inherent Nature – Failures (examples) Replace Term Life with Whole Life (adding Significant Component) Add GMDB to Contract with Insignificant Death Benefit or Visa Versa Replace Disability Contract with LTC Contract (Changes nature of Morbidity Risk) Replace UL with Life Contingent Payout Annuity Change from Discretionary to Formulaic Investment Crediting Methodology Replacement of Variable Contract with Fixed Contract or Visa Versa

Replace Term Life with Whole Life (adding Significant Component) Add GMDB to Contract with Insignificant Death Benefit or Visa Versa Replace Disability Contract with LTC Contract (Changes nature of Morbidity Risk) Replace UL with Life Contingent Payout Annuity Change from Discretionary to Formulaic Investment Crediting Methodology Replacement of Variable Contract with Fixed Contract or Visa Versa Inherent Nature – Failures (examples) Replace Term Life with Whole Life (adding Significant Component) Add GMDB to Contract with Insignificant Death Benefit or Visa Versa Replace Disability Contract with LTC Contract (Changes nature of Morbidity Risk) Replace UL with Life Contingent Payout Annuity Change from Discretionary to Formulaic Investment Crediting Methodology Replacement of Variable Contract with Fixed Contract or Visa Versa")

47

DAC on Internal Replacements Transition Effective Date: For Replacements in Fiscal Years beginning on or after December 15, 2003 Prospectively applied Prior balances should not be adjusted prior to year of adoption Must Adopt Retroactive to Beginning of a Fiscal Year Transition Effective Date: For Replacements in Fiscal Years beginning on or after December 15, 2003 Prospectively applied Prior balances should not be adjusted prior to year of adoption Must Adopt Retroactive to Beginning of a Fiscal Year

Similar presentations

* *Varies by.>")