Download presentation

Presentation is loading. Please wait.

1

Prof. Alex Ampadu 340 Jacobs Management Center Phone: 645-3265

Pension Prof. Alex Ampadu 340 Jacobs Management Center Phone:

2

Pension Fund Characteristics

Noncontributory Contributory Defined Contribution Defined Benefit Vested Benefits 8

3

Types of Pension Plans

4

Features of Pension Plans

5

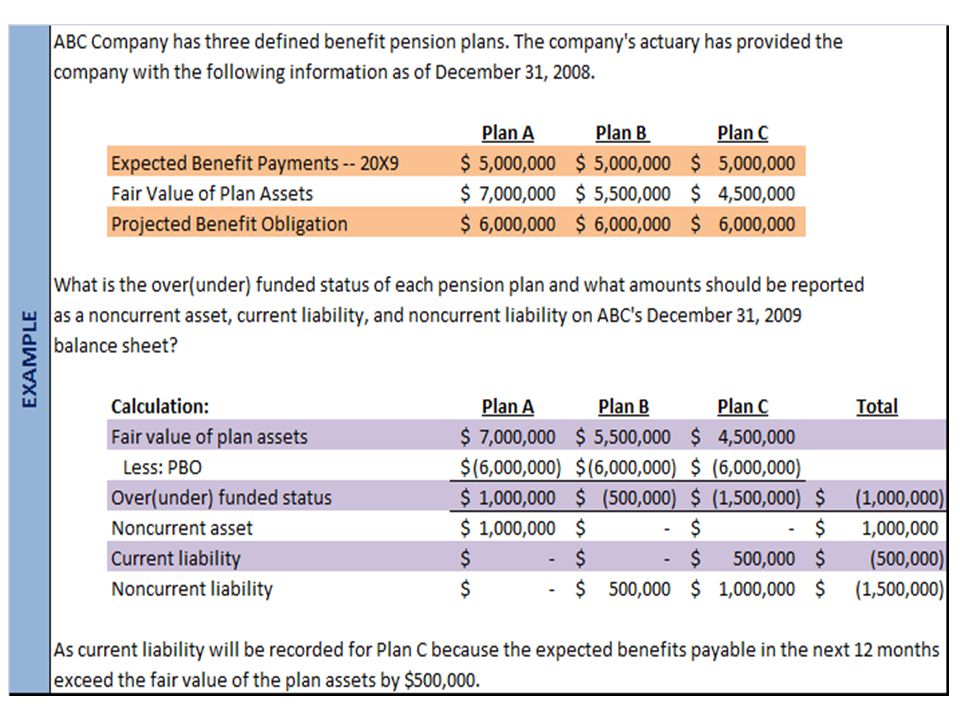

Potential Measures of Pension Liability

Benefits for vested and nonvested employees at future salaries Benefits for vested and nonvested employees at current salaries Projected Benefit Obligation Accumulated Benefit Obligation Benefits for vested employees at current salaries Vested Benefit Obligation (GAAP) PV of Expected Cash Flows 9

PV of Expected. Cash Flows. 9.")

6

Components of Pension Plans

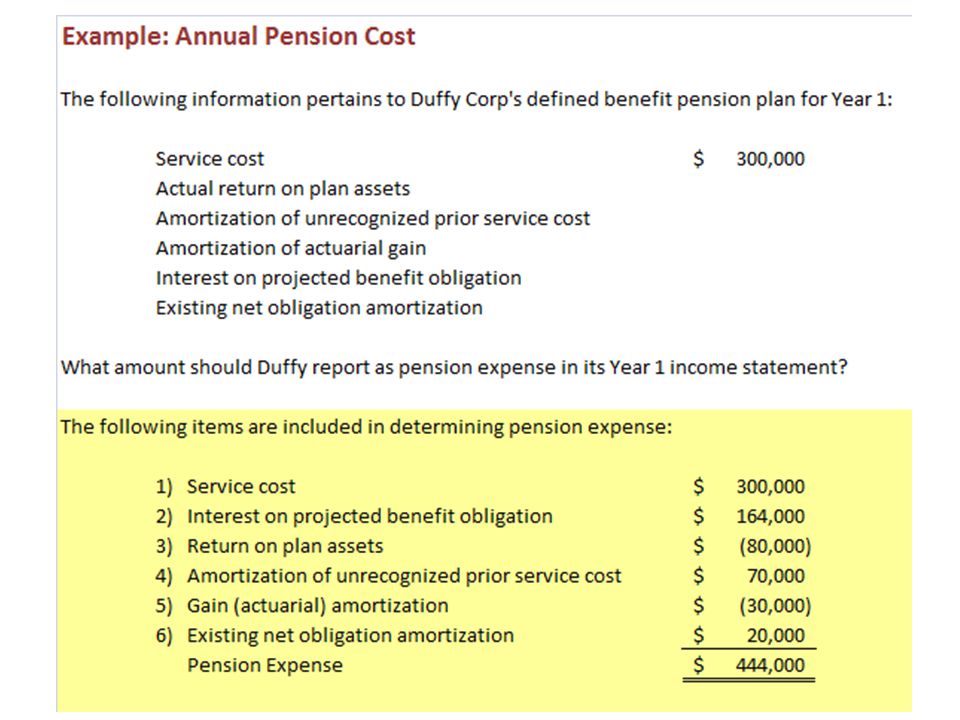

Service Cost + Interest Cost – Actual Return On Plan Assets + Amort. Of Unrecognized PSC ± Amort. Of Unrecognized Gain (Loss) Pension Expense xx Cash xx Prepaid/Accrued Pension Cost xx (Company Funding Difference)

Pension Expense xx. Cash xx. Prepaid/Accrued Pension Cost xx. (Company Funding Difference)")

7

Components of “NET PERIODIC PENSION COST”

Current Service Cost – The present value of all benefits earned in the current period. In other words, the increase in the PBO (Projected Benefit Obligation) resulting from employee services in the current period. The pension benefit formula is applied to compute a present value. The actuary provides service cost.

resulting from employee services in the current period. The pension benefit formula is applied to compute a present value. The actuary provides service cost.")

8

Interest Cost – The increase in the projected benefit obligation during the current period that is due to the passage of time. (Similar to the recognition of interest expense) FORMULA: Beg. of period PBO x Settlement rate = Interest Cost

9

Expected Return on Plan Assets – Standard setters decided that having actual return be a part of pension expense could result in large fluctuations in pension expense from year-to-year (performance of plan investments can vary widely over time – think of the recent performance of the stock market). Consequently, this component is defined as actual return adjusted for the difference between actual and expected return – in other words, expected return. FORMULA: Beg. FV of plan assets x Expected rate of return on plan assets = Expected return on plan assets We will see shortly that this difference between actual and expected return is reflected in <GAINS> and losses (UNRECOGNIZED)

")

15

Example: The average remaining service life of all active employee is 5.5 years. (beginning of the year) Projected benefit obligation 2,100,000 2,600,000 2,900,000 Market related asset value 2,600,000 2,800,000 2,700,000 Unrecognized net loss , ,000

Projected benefit obligation 2,100,000 2,600,000 2,900,000. Market related asset value 2,600,000 2,800,000 2,700,000. Unrecognized net loss , ,000.")

16

Example (cont) Corridor Test and Gain/Loss Amortization Schedule

cumulative Minimum Year PBO Plan Assets (a) Corridor (b) Unrecognized Amortization Loss (a) of Loss (current yr) x8 $2,100,000 $2,600,000 $260, $ $-0- X ,600,000 2,800, , , ,818 (c) X10 2,900,00 2,700, , , ,579 (d) All as of the beginning of the period 10% of the greater of projected benefit obligation or plan assets $400,000 - $280,000 = $120,000; $120,00 / 5.5 = $21,818 $400,000 - $290,000 + $300,000 = $678,192 $678,192 - $290,000 = $388,182 $388,182 / 5.5 = $70,579

Corridor (b) Unrecognized Amortization. Loss (a) of Loss (current yr) x8 $2,100,000 $2,600,000 $260,000 $ -0- $-0- X9 2,600,000 2,800, , ,000 21,818 (c) X10 2,900,00 2,700, , ,812 70,579 (d) All as of the beginning of the period. 10% of the greater of projected benefit obligation or plan assets. $400,000 - $280,000 = $120,000; $120,00 / 5.5 = $21,818. $400,000 - $290,000 + $300,000 = $678,192. $678,192 - $290,000 = $388,182. $388,182 / 5.5 = $70,579.")

23

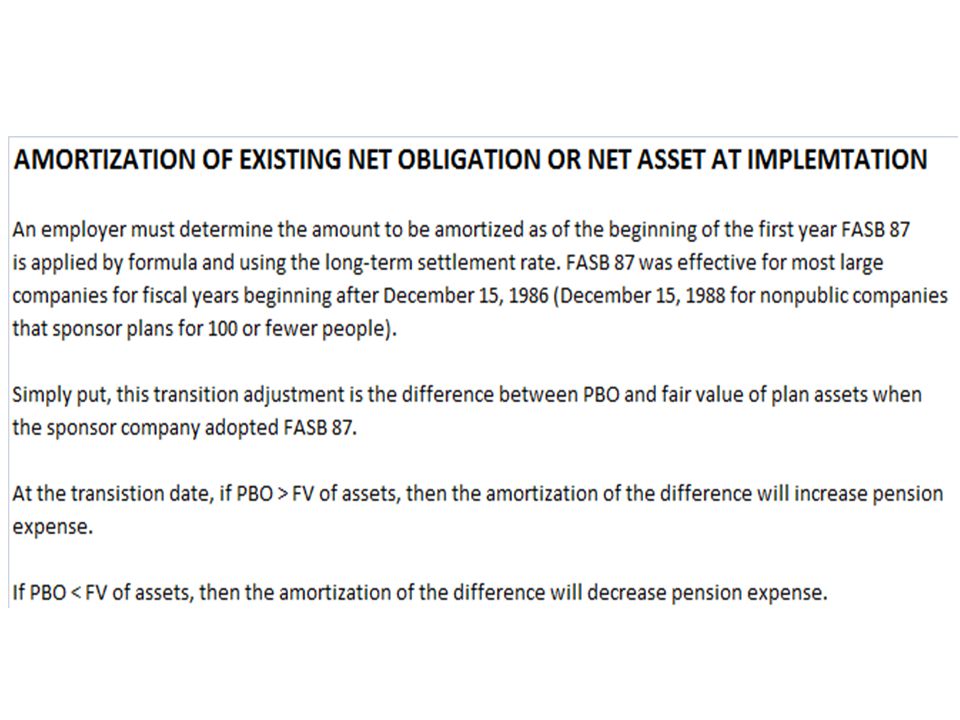

RELEVANT FACTS IFRS and GAAP separate pension plans into defined contribution plans and defined benefit plans. The accounting for defined contribution plans is similar. Both IFRS and GAAP compute unrecognized past service costs (PSC) (referred to as prior service cost in GAAP) in the same manner. However, IFRS recognizes any vested amounts immediately and spreads unvested amounts over the average remaining period to vesting. GAAP amortizes PSC over the remaining service lives of employees.

(referred to as prior service cost in GAAP) in the same manner. However, IFRS recognizes any vested amounts immediately and spreads unvested amounts over the average remaining period to vesting. GAAP amortizes PSC over the remaining service lives of employees.")

24

RELEVANT FACTS Under IFRS, companies have the choice of recognizing actuarial gains and losses in income immediately (either net income or other comprehensive income) or amortizing them over the expected remaining working lives of employees. GAAP does not permit choice; actuarial gains and losses are reported in “Accumulated other comprehensive income” and amortized to income over remaining service lives. For defined benefit plans, GAAP recognizes a pension asset or liability as the funded status of the plan (i.e., defined benefit obligation minus the fair value of plan assets). IFRS recognizes the funded status, net of unrecognized past service cost and unrecognized net gain or loss.

or amortizing them over the expected remaining working lives of employees. GAAP does not permit choice; actuarial gains and losses are reported in Accumulated other comprehensive income and amortized to income over remaining service lives. For defined benefit plans, GAAP recognizes a pension asset or liability as the funded status of the plan (i.e., defined benefit obligation minus the fair value of plan assets). IFRS recognizes the funded status, net of unrecognized past service cost and unrecognized net gain or loss.")

25

IFRS SELF-TEST QUESTION

At the end of the current period, Oxford Ltd. has a defined benefit obligation of $195,000 and pension plan assets with a fair value of $110,000. The amount of the vested benefits for the plan is $105,000. What amount related to its pension plan will be reported on the company’s statement of financial position? $5,000. $90,000. $85,000. $20,000.

26

IFRS SELF-TEST QUESTION

At the end of the current year, Kennedy Co. has a defined benefit obligation of $335,000 and pension plan assets with a fair value of $245,000. The amount of the vested benefits for the plan is $225,000. Kennedy has unrecognized past service costs of $24,000 and an unrecognized actuarial gain of $8,300. What account and amount(s) related to its pension plan will be reported on the company’s statement of financial position? Pension Liability and $74,300. Pension Liability and $90,000. Pension Asset and $233,300. Pension Asset and $110,000.

related to its pension plan will be reported on the company’s statement of financial position Pension Liability and $74,300. Pension Liability and $90,000. Pension Asset and $233,300. Pension Asset and $110,000.")

27

IFRS SELF-TEST QUESTION

At January 1, 2012, Wembley Company had plan assets of $250,000 and a defined benefit obligation of the same amount. During 2012, service cost was $27,500, the discount rate was 10%, actual and expected return on plan assets were $25,000, contributions were $20,000, and benefits paid were $17,500. Based on this information, what would be the defined benefit obligation for Wembley Company at December 31, 2012? $277,500. c. $27,500. $285,000. d. $302,500.

Similar presentations