Download presentation

Presentation is loading. Please wait.

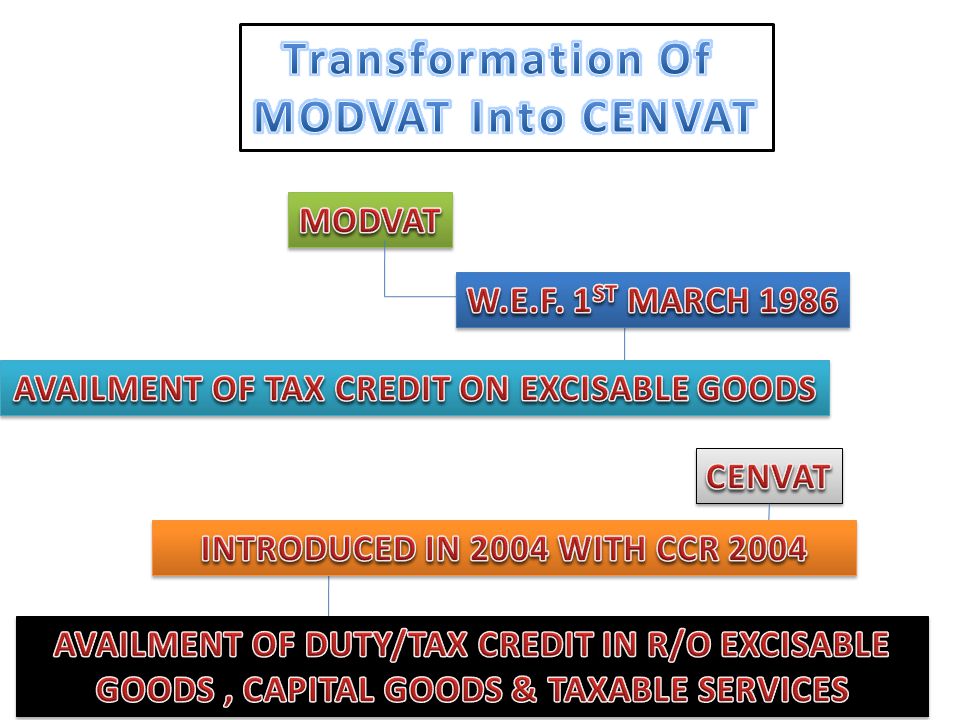

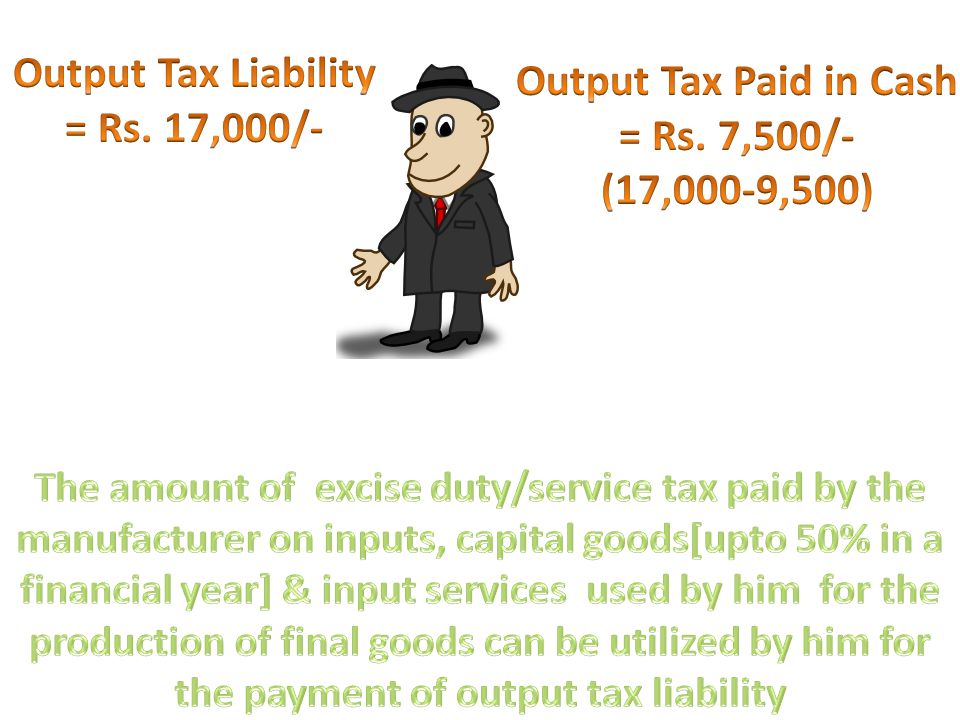

11

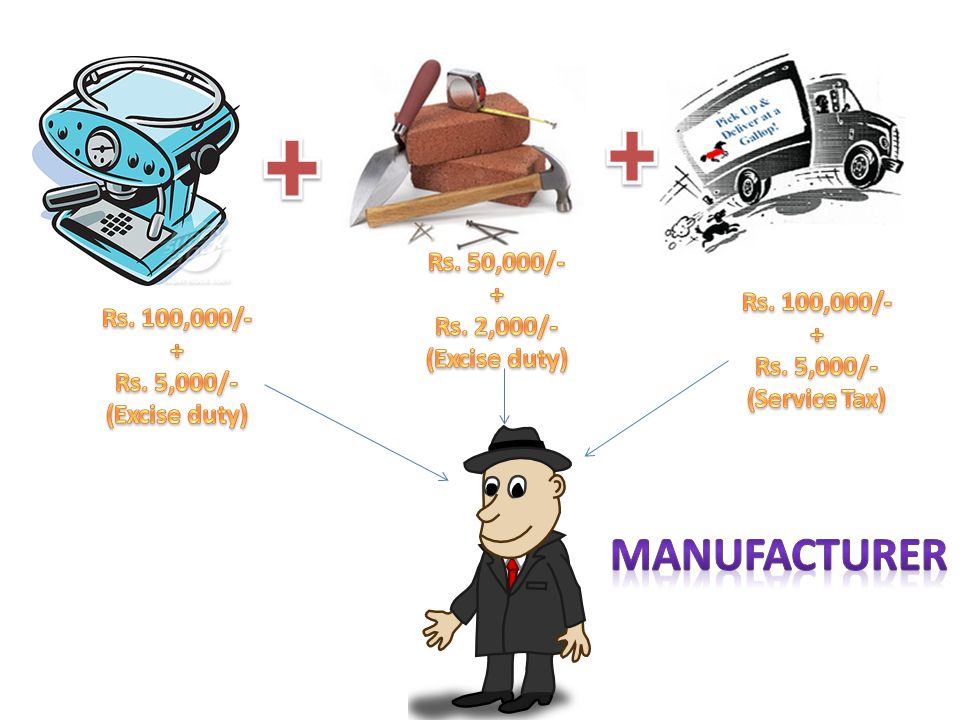

SERVICE Invoice Issued Rs. 50,000/- + Rs. 5150(S.T.) Invoice Issued Rs. 50,000/- + Rs. 5150(S.T.) Invoice Issued Rs. 100,000/- + Rs. 10,300(S.T.) Invoice Issued Rs. 100,000/- + Rs. 10,300(S.T.)

Invoice Issued Rs. 100,000/- + Rs. 10,300(S.T.) Invoice Issued Rs. 100,000/- + Rs. 10,300(S.T.).")

15

INCLUDES - A Capital goods except when used as parts or components in the manufacture of a final product Motor Vehicles Any goods, such as food items, goods used in a guesthouse, residential colony, club or a recreation facility and clinical establishment, when such goods are used primarily for personal use or consumption of any employee Any Goods Which Have No Relationship Whatsoever With The Manufacture Of A Final Product. Specific Exclusions - B

16

All goods used in the factory by the manufacturer of the final product ; Any goods including accessories, cleared along with the final product, the value of which is included in the value of the final product and goods used for providing free warranty for final products All goods used for generation of electricity or steam for captive use EXPLANATION. – FOR THE PURPOSE OF THIS CLAUSE, FREE WARRANTY MEANS A WARRANTY PROVIDED BY THE MANUFACTURER, THE VALUE OF WHICH IS INCLUDED IN THE PRICE OF THE FINAL PRODUCT AND IS NOT CHARGED SEPARATELY FROM THE CUSTOMER.

17

Light diesel oil, high speed diesel oil or motor spirit, commonly known as petrol Any goods used for Construction Of A Building Or A Civil Structure Or A Part Thereof Laying of foundation or making of structures for support of capital goods Except for the provision of any of following taxable services i.e. Port Services, Other Port Services, Airport Services, Commercial or Industrial Construction Services, Complex Construction Services, Services in Execution of Works Contract.

18

All goods used for providing any output service Specific Exclusions (Same as for Manufacturer) Motor vehicles Any goods, such as food items, goods used in a guesthouse, residential colony, club or a recreation facility and clinical establishment, when such goods are used primarily for personal use or consumption of any employee EXPLANATION. – FOR THE PURPOSE OF THIS CLAUSE, FREE WARRANTY MEANS A WARRANTY PROVIDED BY THE MANUFACTURER, THE VALUE OF WHICH IS INCLUDED IN THE PRICE OF THE FINAL PRODUCT AND IS NOT CHARGED SEPARATELY FROM THE CUSTOMER.

19

It means any services used by a manufacturer, whether directly or indirectly, in or in relation to the manufacture of final products and clearance of final products upto the place of removal. Service used in relation to modernization, renovation or repair of a factory or an office relating to such factory Advertisement or sales promotion Market Research Storage upto the place of removal Procurement of Input Accounting, auditing, financing, recruitment and quality control, coaching and training, computer networking, credit rating, share registry, security, business exhibition, legal services, inward transportation of inputs or capital goods and outward transportation upto the place of removal

20

It means any services used by a provider of taxable services, for providing an output service. Service used in relation to modernization, renovation or repair of a factory or an office relating to such factory Advertisement or sales promotion Market Research Accounting, auditing, financing, recruitment and quality control, coaching and training, computer networking, credit rating, share registry, security, business exhibition, legal services, inward transportation of inputs or capital goods and outward transportation upto the place of removal

21

Any of specified Services i.e. Architect s Services, Port Services, Other Port Services, Airport Services, Commercial or Industrial Construction Services, Complex Construction Services, Works Contract General Services if used for either of following purposes General Insurance Services Rent-a-cab Scheme Operators Services, Authorised Service Station Services, Supply of Tangible Goods in so far as they relate to a motor vehicle except when used for the provision of taxable services for which the credit on motor vehicle is available as capital goods Services such as those provided in relation to outdoor catering, beauty treatment, health services, cosmetic and plastic surgery, membership of a club, health and fitness centre, life insurance, health insurance and travel benefits extended to employees on vacation such as Leave or Home Travel Concession, when such services are used primarily for personal use or consumption of any employee. a) construction of a building or a civil structure or a part thereof b) laying of foundation or making of structures for support of capital goods, except for the provision of one or more of the specified services

construction of a building or a civil structure or a part thereof b) laying of foundation or making of structures for support of capital goods, except for the provision of one or more of the specified services.")

22

Relevant Sub-HeadingProvisions w.e.f. 01.04.2011 Expansion in the definition of Capital Goods "capital goods" means:- (A) the following goods, namely:- (i) all goods falling under Chapter 82, Chapter 84, Chapter 85, Chapter 90, [heading 6805, grinding wheels and the like, and parts thereof falling under heading 6804] of the First Schedule to the Excise Tariff Act; (ii)pollution control equipment; (iii)components, spares and accessories of the goods specified at (i) and (ii); (iv) moulds and dies, jigs and fixtures; (v)refractories and refractory materials; (vi)tubes and pipes and fittings thereof; and (vii)storage tank, Capital goods

the following goods, namely:- (i) all goods falling under Chapter 82, Chapter 84, Chapter 85, Chapter 90, [heading 6805, grinding wheels and the like, and parts thereof falling under heading 6804] of the First Schedule to the Excise Tariff Act; (ii)pollution control equipment; (iii)components, spares and accessories of the goods specified at (i) and (ii); (iv) moulds and dies, jigs and fixtures; (v)refractories and refractory materials; (vi)tubes and pipes and fittings thereof; and (vii)storage tank, Capital goods.")

23

Relevant Sub-HeadingProposed New Provisions used- (1)in the factory of the manufacturer of the final products, but does not include any equipment or appliance used in an office. (1A) outside the factory of the manufacturer of the final products for generation of electricity for captive use within the factory. Consequential amendment in Rule 4(2)(a) for the manufacturer of final products The CENVAT credit in respect of capital goods received in a factory or outside the factory of the manufacturer of the final products for generation of electricity for captive use within the factory at any point of time in a given financial year shall be taken only for an amount not exceeding 50%of the duty paid on such capital goods in the same financial year

outside the factory of the manufacturer of the final products for generation of electricity for captive use within the factory. Consequential amendment in Rule 4(2)(a) for the manufacturer of final products The CENVAT credit in respect of capital goods received in a factory or outside the factory of the manufacturer of the final products for generation of electricity for captive use within the factory at any point of time in a given financial year shall be taken only for an amount not exceeding 50%of the duty paid on such capital goods in the same financial year.")

24

These are those excisable goods which are exempt from the whole of the duty of excise leviable thereon, and includes goods which are chargeable to "Nil" rate of duty Goods in respect of which the benefit of an exemption under Notification No. 1/2011-CE, dated the 1st march, 2011 is availed. Abovementioned notification No. 1/2011-CE provides exemption to 130 excisable goods w.e.f. 01.03.2011 in excess of one per cent of ad valorem excise duty. Consequently, previously referred 130 excisable goods shall be treated as exempted goods for the purpose of CCR, 2004.Further, no CENVAT Credit will be admissible to a manufacturer in r/o excise duty paid on said 130 excisable goods by virtue of insertion of proviso to Rule 3(1)(i) of CCR, 2004.

(i) of CCR,")

25

These are those taxable services which are exempt from the whole of the service tax leviable thereon, and includes services on which no service tax is leviable under section 66 of the Finance Act Taxable services whose part of value is exempted on the condition that no credit of inputs and input services, used for providing such taxable service, shall be taken. As a result of above amendment, the abated value of relevant taxable services provided by the service provider will be considered as exempted services. Further, balance taxable value of relevant taxable services will be added to the value of taxable services for the purpose of determining CENVAT Credit available with a service provider.

27

27 Eligible Duties/Taxes Following duties paid on inputs/capital goods (A)Following duties paid on inputs/capital goods 1.Basic Excise Duty (CENVAT) i.e. excise duty specified in First Schedule & Second Schedule to Central Excise Tariff Act, 1985 2.Special Excise Duty (SED) 3.Additional Duty of Excise under AED (Textile & Textile Articles) Act 4.Additional Duty of Excise under AED (Goods of special importance) Act 5.National Calamity Contingent Duty (NCCD) 6.Education Cess on Excise Duty 7.Additional Duty of Customs (CVD) 8.Additional Duty of Excise on Tea & Tea Waste Service Tax (B)Service Tax 1.Service Tax paid on input services 2.Education Cess on Service Tax Provided CENVAT credit not be allowed in excess of 85% the additional duty of customs paid under sub section (1) of section 3 of Customs Tariff Act.

3.Additional Duty of Excise under AED (Textile & Textile Articles) Act 4.Additional Duty of Excise under AED (Goods of special importance) Act 5.National Calamity Contingent Duty (NCCD) 6.Education Cess on Excise Duty 7.Additional Duty of Customs (CVD) 8.Additional Duty of Excise on Tea & Tea Waste Service Tax (B)Service Tax 1.Service Tax paid on input services 2.Education Cess on Service Tax Provided CENVAT credit not be allowed in excess of 85% the additional duty of customs paid under sub section (1) of section 3 of Customs Tariff Act..")

29

Sr. No.Respect withCondition 1.InputImmediately on receipt of the inputs in the factory of the manufacturer or in the premises of the provider of output service. 2. (a)Capital Goods Received in a factory or in the premises of the provider of output service at any point of time in a given financial year shall be taken only for an amount exceeding 50% of the duty paid on such goods in the same F.Y.. 2. (b)Provided that the capital goods are other than components, spares and accessories, refractories and the refractory materials, moulds and dies and other goods falling under the First Schedule to the excise tariff act, are in the possession of the manufacturer of final product or provider of output services in such subsequent year, the balance of CENVAT credit may be taken in any F.Y. subsequent to the F.Y. in which the capital goods were received in the factory or in the premises.

Capital Goods Received in a factory or in the premises of the provider of output service at any point of time in a given financial year shall be taken only for an amount exceeding 50% of the duty paid on such goods in the same F.Y.. 2. (b)Provided that the capital goods are other than components, spares and accessories, refractories and the refractory materials, moulds and dies and other goods falling under the First Schedule to the excise tariff act, are in the possession of the manufacturer of final product or provider of output services in such subsequent year, the balance of CENVAT credit may be taken in any F.Y. subsequent to the F.Y. in which the capital goods were received in the factory or in the premises..")

30

Sr. No.Respect withCondition 3.Capital goodsEven if the capital goods are acquired by the manufacturer or provider of output services on lease, hire purchase or loan agreement from a financing company then also he will be allowed the CENVAT credit of the paid duty. 4.Capital GoodsThe CENVAT credit will not be allowed in respect of that part of the value of Capital Goods which represents the amount of duty paid in respect of the Capital goods, which the manufacturer or provider of output services claim as depreciation under Section 32 of the Income Tax Act, 1961.

37

If a taxable service has been exempted on the condition that no CENVAT Credit shall be taken to provide that service then the amount specified in clause (i) shall be 5 % of the exempted value

shall be 5 % of the exempted value")

38

RuleService ProviderAmount to be Paid Rule 6(3B) A Banking company & a financial Institution including a non- banking financial company[N.B.F.C.] 50% of the CENVAT credit availed on inputs and input services in that month. Rule 6(3C) A provider of Life Insurance Business Services & Management of Investment under ULIP Services 20% of CENVAT credit availed on inputs and input services in that month

![RuleService ProviderAmount to be Paid Rule 6(3B) A Banking company & a financial Institution including a non- banking financial company[N.B.F.C.] 50% of the CENVAT credit availed on inputs and input services in that month.](http://images.slideplayer.com/5/1533707/slides/slide_38.jpg "Rule 6(3C) A provider of Life Insurance Business Services & Management of Investment under ULIP Services 20% of CENVAT credit availed on inputs and input services in that month.")

40

CONTRACTORSUBCONTRACTOR AVAILING COMPOSITION SCHEME NOT AVAILING COMPOSITION SCHEME PAYING SERVICE TAX 10.3% PAYING SERVICE TAX @ 4.12% ALSO AVAILING 100% CENVAT ON INPUT SERVICES AVAILING 100% CENVAT ON INPUT SERVICES INCONSISTENCY IN OUTPUT TAX RATE (40%) AND INPUT TAX CREDIT RATE (100%)

AND INPUT TAX CREDIT RATE (100%)")

41

AVAILING COMPOSITION SCHEME PAYING SERVICE TAX @ 4.12% ALSO AVAILING 40% CENVAT NOT AVAILING COMPOSITION SCHEME PAYING SERVICE TAX 10.3% AVAILING 100% CENVAT ON INPUT CONTRACTORSUBCONTRACTOR RESTRICTION ON AVAILMENT OF CENVAT TO 40 % IN R/O ABOVE TAXABLE SERVICES TAXABLE SERVICES: 1)ERECTION COMMISSIONING & INSTALLATION SERVICES 2)COMMERCIAL OR INDUSRTIAL CONSTRUCTION SERVICES 3)COMPLEX CONSTRUCTION SERVICES TAXABLE SERVICES: 1)ERECTION COMMISSIONING & INSTALLATION SERVICES 2)COMMERCIAL OR INDUSRTIAL CONSTRUCTION SERVICES 3)COMPLEX CONSTRUCTION SERVICES

ERECTION COMMISSIONING & INSTALLATION SERVICES 2)COMMERCIAL OR INDUSRTIAL CONSTRUCTION SERVICES 3)COMPLEX CONSTRUCTION SERVICES TAXABLE SERVICES: 1)ERECTION COMMISSIONING & INSTALLATION SERVICES 2)COMMERCIAL OR INDUSRTIAL CONSTRUCTION SERVICES 3)COMPLEX CONSTRUCTION SERVICES")

43

Room Is Open For Queries

44

44 THANKS FOR GIVING A PATIENT HEARING

Similar presentations

>")

Managing Partner, TLC Legal October,>")

Member of Indirect Tax Committee of PHD/ FICCI/ Assocham Member.>")

(zzzza) of the Finance Act, 1994, the term works contract” means a contract wherein,— (i) transfer.>")