Download presentation

Presentation is loading. Please wait.

1

Prepared by:Bryan Mette Joe OConnell Michelle Prost Erika Schoot Elizabeth Silverstein Budget and Management Division, Department of Administration, City of Milwaukee Prepared for: May 14, 2013

2

In Rem Judgment against property Used synonymously with tax foreclosure In Personam Judgment against person

3

Increasing fiscal pressure and decreasing property values Spikes in tax foreclosures and inventory of City-acquired properties Increasing costs to the City

4

Reduce residential properties that end up in tax foreclosure

5

Milwaukee taxes and assessments Comparisons to other cities Trends in tax delinquency Pre-/Post- foreclosure processes Policy constraints for the City Factors and costs associated with in rem foreclosure Early warning system model Policy options Future considerations

6

*Tax foreclosures based on measurement identified in table.Sources: Hamilton, Ohio 2012 Annual Information Statement; Minneapolis Finance and Property Services Department (2011); Christoff, Chris (2013); Baltimore County Office of Budget and Finance (2013); City of Indianapolis and Marion County (2013); Ryan, Sean (2010); U.S. Census Bureau (2011, 2012)

.")

7

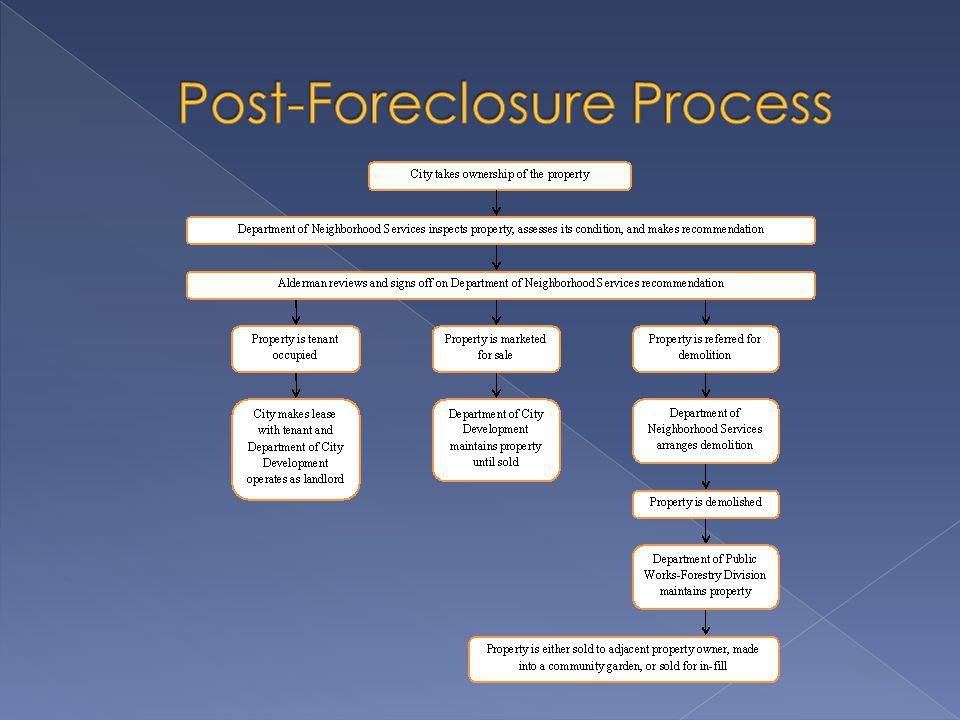

Source: Authors, using data from the Department of City Development

8

February Delinquencies November Delinquencies* Total/Avera ge Average Total 13,3703,40516,775 Average Owner-Occupied 6,9871,9908,977 Average Investor-Owned 6,3831,4157,798 Average February Delinquencies as a % of Average of All Delinquencies 79.8% Average Amount Delinquent $2,993$942$2,577 Source: Authors, using data from Office of the City Treasurer *November Delinquencies numbers include Levy Years 2008-2011.

9

Source: Authors, using data from Office of the City Treasurer

10

Step 1: In-house Collection Delinquency notices sent to owners 4 notices from City Treasurer 2 notices from City Attorney Remaining cases referred to Kohn Law Firm

11

Step 2: Collection by Kohn Law Firm Gauges ability to pay on case-by-case basis Collects back taxes, devises installment plans, pursues in personam judgment when appropriate All delinquencies found to be uncollectible are referred to City Attorney

12

Step 3: In Rem Foreclosure City Attorney initiates suit against delinquent owners in Milwaukee County Circuit Court 8-week redemption period, 30-day answer period In rem foreclosure (City takes ownership) 90 days to petition Common Council

90 days to petition Common Council")

14

Uniformity Clause (Article VIII, §1) The rule of taxation shall be uniform… Special charges added to tax bill Moral Hazard Leeway for delinquent property tax payers could decrease incentive to pay and lead to increased delinquency

The rule of taxation shall be uniform… Special charges added to tax bill Moral Hazard Leeway for delinquent property tax payers could decrease incentive to pay and lead to increased delinquency")

15

Characteristics of Properties Assessment Class Aldermanic District Assessed Property Values Assessed Value Changes During Foreclosure Process Housing Quality Disposition of Properties Owner Occupancy Previous Mortgage Foreclosure Property Complaints and Violations Characteristics of Taxes and Tax Collection Tax Delinquency Special Charges

16

Property Classes: Residential, Condominium (Improved Lots Only) Property Types: Duplex (40.0%) Single-Family (53.3%) Other (6.6%) Total Residential/Condominium Properties: 1,599 (65.1% of total)

Property Types: Duplex (40.0%) Single-Family (53.3%) Other (6.6%) Total Residential/Condominium Properties: 1,599 (65.1% of total)")

17

Source: Authors, using data from the Department of City Development and the Office of the City Assessor

19

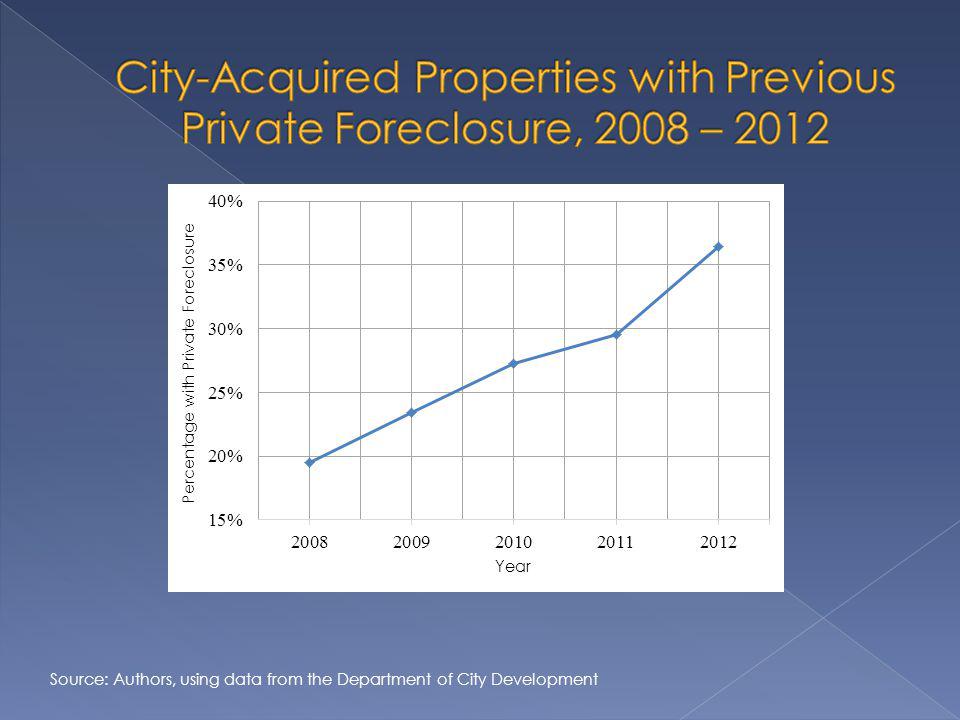

Source: Authors, using data from the Department of City Development

23

February DelinquenciesPost-February Delinquencies All Tax Delinquencies Tax Foreclosures Percentage of Delinquencies that End in Tax Foreclosure All Tax Delinquencies* Tax Foreclosures Percentage of Delinquencies that End in Tax Foreclosure Combined Percentage of Delinquencies that End in Tax Foreclosure Total 12,9816435.0%5,379500.9%3.8% Owner-Occupied 7,1762934.1%3,098311.0%3.2% Investor-Owned 5,8053506.0%2,281190.8%4.6% February Delinquencies and Foreclosures as a % of All Delinquencies and Foreclosures 71%93% Median Amount Delinquent $2,726$2,730 $1,063$1,197 Source: Authors, using data from Office of the City Treasurer

25

Source: City of Milwaukee Division of Budget and Management * Cost estimated based on inspector pay and time required to inspect home and conduct relevant paperwork/data entry. Inspections are done monthly for each property in the City's inventory. ** This estimation uses vacant lots in the calculation of property maintenance.

26

How can the City forecast properties that are at greater risk of tax foreclosure? Factors: Mortgage Foreclosure Other Recent Tax Foreclosure Owner-occupied/Wisconsin Resident Year Property was Purchased Property Type Property Value Aldermanic District

27

Increase likelihood of ending in tax foreclosure Other Tax Foreclosures Not Wisconsin Resident Property Type (Residential Vs. Condo) Aldermanic District 6, 7, 15 Decrease likelihood of ending in tax foreclosure Assessed Value Property Aldermanic District 2, 5, 9, 11, 13, 14

Aldermanic District 6, 7, 15 Decrease likelihood of ending in tax foreclosure Assessed Value Property Aldermanic District 2, 5, 9, 11, 13, 14.")

28

Early Warning System Based upon statistical analysis Used to identify the likelihood of in rem foreclosure for delinquent properties Outreach to those affected e.g., housing non-profits, other options

29

Separation of Special Charges Reduces the amount on tax bills Easier to manage delinquency City has discretion in negotiating re-payment if special charges are not added to tax bill Need effective collection of data to separate tax delinquencies from special charge delinquencies for each property

30

Credit Card Installments Currently, property tax payments by credit card must include the entire bill Gives owners more options Allow property owners to pay tax in installments by credit card Add 2.75% surcharge to cover costs

31

Hardship Loan Fund Modeled, in part, on property tax assistance programs implemented by other governments Fund managed by independent party, such as a private organization, community foundation, or housing non-profit Leverage funds from the private sector to give loans for property taxes Strict eligibility criteria

32

Data set quantifying property taxes and special charges separately Incorporate Department of Neighborhood Services data into analysis Trend analysis

33

Aaron Szopinski, who served as our contact with the City of Milwaukee Jim Klajbor, Robert Potrzebowski, and Sam Leichtling for meeting with us Professor Andrew Reschovsky and Karen Faster

34

Questions?

Similar presentations

Program Robin Ambroz Deputy Director of Programs Nebraska Investment Finance Authority.>")

› Tax Court (TX) › Civil (CV) (property tax related) › All property types: Residential, Commercial, Land, Personal Property and.>")