Download presentation

Presentation is loading. Please wait.

1

Long-Term Liabilities, Bonds Payable, and Classification of Liabilities on the Balance Sheet

Chapter 11 Chapter 11 covers long-term liabilities, bonds payable, and classification of liabilities on the balance sheet. 1 1 1 1 1

2

Long-Term Notes Payable

Most long-term notes are paid in installments Principal due within a year–a current asset Principal not due with in a year–long-term asset Current plus long-term equals total amount of debt Interest accrues as normal Recall that most long-term notes payable are paid in installments. The current portion of notes payable is the principal amount that will be paid within one year—a current liability. The remaining portion is long-term. Consider the $20,000 note payable in the previous chapter, signed on May 1, The note will be paid over four years with payments of $5,000 plus interest due each May 1. Remember that the amount due May 1, 2014, $5,000, is current. Notice that the reclassification entry on May 1 does not change the total amount of debt. It only reclassifies $5,000 of the total debt from long-term to current. The remaining 4 months, January through April will be recorded on May 1. In December eight months total interest ($20,000 times 6% times 8/12 = $800) for the $800 interest accrued on the note as of December 31, 2013.

for the $800 interest accrued on the note as of December 31,")

3

May 1, 2013 entries

4

Long-Term Notes Payable: Payments

Yearly payment would include: Installment amount Previously accrued interest at year-end adjusting Accrued interest since year-end adjusting Journal entry: Now it’s May 1, 2014, and the company must make its first installment payment of $5,000 principal plus interest on the note. Recall the 8 months of interest already recorded at the end of December, The accrual of four months’ interest is recorded when the first installment payment is made. The journal entry would include a debit to Interest expense for the four months’ interest to accrue for January through April. It would also include a debit to Interest payable for the interest accrued at the end of December A debit to Long-term notes payable for the $5,000 installment payment due and a credit to Cash for the installment payment and 12 months worth of interest—5,000 plus $800 accrued interest at December 21 and $400 for interest accrued for the months of January through April 2014. Notice the entry debited the Long-term notes payable account—not the Current portion of long-term notes payable. Why? Because each year, $5,000 of the note balance becomes due (is current). When we make payments on the note, we just reduce the Long-term notes payable (one entry), rather than making the payment and then doing another reclassification entry, like we did on May 1, 2013.

. When we make payments on the note, we just reduce the Long-term notes payable (one entry), rather than making the payment and then doing another reclassification entry, like we did on May 1,")

5

Long-Term Notes Payable: Payments

Entry included a debit to Long-term notes payable Current portion of long-term notes is unchanged Net long-term notes payable equals $15,000 Current portion $5,000 Long-term portion $10,000 The amount owed on the note is $15,000—the $20,000 original note minus the $5,000 payment on May 1, $10,000 is included in the Long-term notes payable account and $5,000 is in the Current portion of long-term notes payable equaling the $15,000 total due.

6

Mortgages Payable Debts backed with a security interest in specific property Title transfers if the mortgage isn’t paid Differs from notes payable Secure interest in property Specifies monthly payment Mortgages payable are long-term debts that are backed with a security interest in specific property. The mortgage will state that the borrower promises to transfer the legal title to specific assets if the mortgage isn’t paid on schedule. This is very similar to the long-term notes payable we just covered. The main difference is the mortgage payable is secured with specific assets, whereas long-term notes are not secured with specific assets. Like long-term notes payable, the total mortgage payable amount will have a portion due within one year (current) and a portion that is due more than one year from a specific date. Commonly, mortgages will specify a monthly payment of principal and interest to the lender (usually a bank). The most common type of mortgage is on property—for example, a mortgage on your home. The principal portion of the total mortgage payable that is due within one year is current. To figure the amount of each payment to apply to the mortgage payable and how much is interest expense, we create an amortization schedule.

and a portion that is due more than one year from a specific date. Commonly, mortgages will specify a monthly payment of principal and interest to the lender (usually a bank). The most common type of mortgage is on property—for example, a mortgage on your home. The principal portion of the total mortgage payable that is due within one year is current. To figure the amount of each payment to apply to the mortgage payable and how much is interest expense, we create an amortization schedule.")

7

Amortization Schedule

Details each payment’s allocation between principal and interest The principal portion of the total mortgage payable that is due within one year is current. To figure the amount of each payment to apply to the mortgage payable and how much is interest expense, we create an amortization schedule. An amortization schedule details each loan payment’s allocation between principal and interest.

8

Mortgages Payable Mortgage payment includes

Interest expense from amortization table Principal reduction form amortization table Payment amount agreed upon So after reviewing the amortization schedule, we would reclassify the portion of the $100,075 mortgage balance that is current as a debit to Mortgage payable and a credit to Current portion of mortgage payable for $1, The current portion of the mortgage is payable each year-end on December 31 rather than monthly, since the change to the account is not material from month to month.

9

S11-1: Accounting for a long-term note payable

On January 1, 2014, LeMay-Finn, Co., signed a $200,000, five-year, 6% note. The loan required LeMay-Finn to make payments on December 31 of $40,000 principal plus interest. 1. Journalize the issuance of the note on January 1, 2014. Journal Entry DATE ACCOUNTS DEBIT CREDIT Jan 1 Cash 200,000 Long-term notes payable Short Exercise 11-1 reviews accounting for a long-term note payable.

10

S11-1: Accounting for a long-term note payable

(Continued) 2. Journalize the reclassification of the current portion of the note payable. Journal Entry DATE ACCOUNTS DEBIT CREDIT Jan 1 Long-term notes payable 40,000 Current portion of long-term notes payable The exercise continues on this slide.

2. Journalize the reclassification of the current portion of the note payable. Journal Entry. DATE. ACCOUNTS. DEBIT. CREDIT. Jan 1. Long-term notes payable. 40,000. Current portion of long-term notes payable. The exercise continues on this slide.")

11

S11-1: Accounting for a long-term note payable

(Continued) 3. Journalize the first note payment on December 31, 2014. Journal Entry DATE ACCOUNTS DEBIT CREDIT Dec 31 Interest expense 12,000 Long-term notes payable 40,000 Cash 52,000 The exercise continues.

3. Journalize the first note payment on December 31, Journal Entry. DATE. ACCOUNTS. DEBIT. CREDIT. Dec 31. Interest expense. 12,000. Long-term notes payable. 40,000. Cash. 52,000. The exercise continues.")

13

Bonds Payable Long-term liability Financing in large amounts

Multiple lenders = bondholders Bond certificate evidence of loan Amount borrowed (principal) Maturity date Interest rate Bondholders receive interest Normally two times a year Principal paid at maturity Large companies need large amounts of money to finance operations. They may borrow long-term from banks or issue bonds payable to the public to raise the money. Bonds payable are groups of long-term notes payable issued to multiple lenders, called bondholders. By issuing bonds payable, a company can borrow millions of dollars from thousands of investors, rather than depending on a loan from one single bank or lender. Each investor can buy a specified amount of bonds. Each bondholder gets a bond certificate, which shows the name of the company that borrowed the money, exactly like a note payable. The certificate states the principal, which is the amount the company has borrowed. The bond’s principal amount is also called maturity value, or par value. The company must then pay each bondholder the principal amount at a specific future date, called the maturity date. People buy bonds to earn interest. The bond certificate states the interest rate that the company will pay and the dates the interest is due, generally semi-annually (twice a year).

Maturity date. Interest rate. Bondholders receive interest. Normally two times a year. Principal paid at maturity. Large companies need large amounts of money to finance operations. They may borrow long-term from banks or issue bonds payable to the public to raise the money. Bonds payable are groups of long-term notes payable issued to multiple lenders, called bondholders. By issuing bonds payable, a company can borrow millions of dollars from thousands of investors, rather than depending on a loan from one single bank or lender. Each investor can buy a specified amount of bonds. Each bondholder gets a bond certificate, which shows the name of the company that borrowed the money, exactly like a note payable. The certificate states the principal, which is the amount the company has borrowed. The bond’s principal amount is also called maturity value, or par value. The company must then pay each bondholder the principal amount at a specific future date, called the maturity date. People buy bonds to earn interest. The bond certificate states the interest rate that the company will pay and the dates the interest is due, generally semi-annually (twice a year).")

14

Bond Terminology Principal–amount to be paid back

Also called maturity value, face value or par value Maturity date–date of principal payback Stated interest rate–also termed face rate, coupon rate, or nominal rate Rate of interest paid to bondholders Cash payments during life of bond Like a note, each bond contains Principal Rate Time Bond terminology is important to understand. Principal amount (also called maturity value, or par value):The amount the borrower must pay back to the bondholders on the maturity date. Maturity date: The date on which the borrower must pay the principal amount to the bondholders. Stated interest rate: The annual rate of interest that the borrower pays the bondholders.

:The amount the borrower must pay back to the bondholders on the maturity date. Maturity date: The date on which the borrower must pay the principal amount to the bondholders. Stated interest rate: The annual rate of interest that the borrower pays the bondholders.")

15

Types of Bonds Term bonds All mature at same date Serial bonds

Mature in installments at regular intervals Secured bonds Backed by assets if company fails to pay Debenture Unsecured; not backed by company’s assets There are various types of bonds, including the following: • Term bonds all mature at the same specified time. For example, $100,000 of term bonds may all mature 5 years from today. • Serial bonds mature in installments at regular intervals. For example, a $500,000, 5-year serial bond may mature in $100,000 annual installments over a 5-year period. • Secured bonds give the bondholder the right to take specified assets of the issuer if the issuer fails to pay principal or interest. A mortgage on a house is an example of a secured bond. • Debentures are unsecured bonds that aren’t backed by assets. They are backed only by the goodwill of the bond issuer.

16

Bond Pricing (Selling Price)

Fluctuates like stock Based upon maturity date and interest rate Maturity (Par) value 100% face value Discount (Bond discount) Below 100% face Premium (Bond premium) Above 100% face Price does not affect payment at maturity A bond can be issued at any price agreed upon by the issuer and the bondholders. There are three basic categories of bond prices. A bond can be issued at: • Maturity (par) value. Example: A $1,000 bond issued for $1,000. A bond issued at par has no discount or premium. • Discount (or Bond Discount), a price below maturity (par) value. Example: A $1,000 bond issued for $980. The discount is $20 ($1,000 – $980). • Premium (or Bond Premium), a price above maturity (par) value. Example: A $1,000 bond issued for $1,015. The premium is $15 ($1,015 – $1,000). The issue price of a bond does not affect the required payment at maturity. In all of the preceding cases, the company must pay the maturity value of the bonds when they mature.

value. 100% face value. Discount (Bond discount) Below 100% face. Premium (Bond premium) Above 100% face. Price does not affect payment at maturity. A bond can be issued at any price agreed upon by the issuer and the bondholders. There are three basic categories of bond prices. A bond can be issued at: • Maturity (par) value. Example: A $1,000 bond issued for $1,000. A bond issued at par has no discount or premium. • Discount (or Bond Discount), a price below maturity (par) value. Example: A $1,000 bond issued for $980. The discount is $20 ($1,000 – $980). • Premium (or Bond Premium), a price above maturity (par) value. Example: A $1,000 bond issued for $1,015. The premium is $15 ($1,015 – $1,000). The issue price of a bond does not affect the required payment at maturity. In all of the preceding cases, the company must pay the maturity value of the bonds when they mature.")

17

Bond Prices Quoted as a percent of maturity value

A $1,000 bond quoted at would sell for $1,015 ($1,000 X 101.5) A $1,000 bond quoted at would sell for $ ($1,000 X 89.75) Issue price determines amount received Payments equal face amount of principal and interest Bond prices are quoted as a percentage of maturity value. For example: • A $1,000 bond quoted at 100 is bought or sold for 100% of maturity value, ($1,000. x 1.00). • A $1,000 bond quoted at has a price of $1,015 ($1,000 × 1.015). • A $1,000 bond quoted at has a price of $ ($1,000 × .8975).

A $1,000 bond quoted at would sell for $ ($1,000 X 89.75) Issue price determines amount received. Payments equal face amount of principal and interest. Bond prices are quoted as a percentage of maturity value. For example: • A $1,000 bond quoted at 100 is bought or sold for 100% of maturity value, ($1,000. x 1.00). • A $1,000 bond quoted at has a price of $1,015 ($1,000 × 1.015). • A $1,000 bond quoted at has a price of $ ($1,000 × .8975).")

18

Bond Prices Determining the Market Value of Bonds

Market value is a function of the three factors that determine present value: the dollar amounts to be received, the length of time until the amounts are received, and the market rate of interest.

19

Issue price of bonds payable

Bond Interest Rates Stated interest rate Rate used to calculate interest the borrower pays each year Remains constant Market interest rate Rate investors demand for loaning money Varies daily Stated interest rate Market interest rate Issue price of bonds payable 9% = Maturity value < 10% Discount (below maturity value) > 8% Premium (above maturity value) Bonds are sold at their market price, which is the present value of the interest payments the bondholder will receive while holding the bond plus the bond principal paid at the end of the bond’s life. Two interest rates work together to set the price of a bond: • The stated interest rate determines the amount of cash interest the borrower pays each year. The stated interest rate is printed on the bond and does not change from year to year. • The market interest rate (also known as the effective interest rate) is the rate that investors demand to earn for loaning their money. The market interest rate varies daily. A company may issue bonds with a stated interest rate that differs from the market interest rate, due to the time gap between the decision of what the stated rate should be and the actual issuance of the bonds. If the stated rate is equal to the market rate, the bonds will be issued at their maturity value. If the stated rate is less than the market rate, the bonds will sell below maturity value–a discount. Conversely, if the stated rate is greater than the market rate, bonds will be issued above maturity value–a premium. This is because the bonds are paying better interest than the market indicates; the market pays more because the bond is paying more interest.

> 8% Premium (above maturity value) Bonds are sold at their market price, which is the present value of the interest payments the bondholder will receive while holding the bond plus the bond principal paid at the end of the bond’s life. Two interest rates work together to set the price of a bond: • The stated interest rate determines the amount of cash interest the borrower pays each year. The stated interest rate is printed on the bond and does not change from year to year. • The market interest rate (also known as the effective interest rate) is the rate that investors demand to earn for loaning their money. The market interest rate varies daily. A company may issue bonds with a stated interest rate that differs from the market interest rate, due to the time gap between the decision of what the stated rate should be and the actual issuance of the bonds. If the stated rate is equal to the market rate, the bonds will be issued at their maturity value. If the stated rate is less than the market rate, the bonds will sell below maturity value–a discount. Conversely, if the stated rate is greater than the market rate, bonds will be issued above maturity value–a premium. This is because the bonds are paying better interest than the market indicates; the market pays more because the bond is paying more interest.")

20

Interest rates and bond prices Example

Stated Rate = MKT Bond Sells at Face value

21

Interest rates and bond prices Example

Stated Rate > MKT Bond Sells at Premium 1.08 1.08

22

Interest rates and bond prices Example

Stated Rate < MKT Bond Sells at Discount 1.12 1.12

23

Bond Price Components Previous slides used to demo concept of sale of bond at: Face Premium Discount Pricing of bonds is more complex than illustration on previous slides Bond price a function of 2 items Present value of the lump sum(principal) PLUS Present value of the annuity interest payments

PLUS. Present value of the annuity interest payments.")

24

S11-3: Determining bond prices

Bond prices depend on the market rate of interest, stated rate of interest, and time. Determine whether the following bonds payable will be issued at maturity value, at a premium, or at a discount. The market interest rate is 6%. Boise, Corp., issues bonds payable with a stated rate of 5 3/4%. Dallas, Inc., issued 8% bonds payable when the market rate was 7 1/4%. Discount Short Exercise 11-3 reviews how to determine bond prices. Premium

25

S11-3: Determining bond prices

(Continued) Cleveland Corporation issued 7% bonds when the market interest rate was 7%. d. Atlanta Company issued bonds payable that pay stated interest of 7 1/2%. At issuance, the market interest rate was 9 1/4%. Par value The exercise continues on this slide. Discount

Cleveland Corporation issued 7% bonds when the market interest rate was 7%. d. Atlanta Company issued bonds payable that pay stated interest of 7 1/2%. At issuance, the market interest rate was 9 1/4%. Par value. The exercise continues on this slide. Discount.")

26

Compute the price of the following 7% bonds of United Telecom.

S11-4: Pricing bonds Bond prices depend on the market rate of interest, stated rate of interest, and time. Compute the price of the following 7% bonds of United Telecom. $500,000 issued at $500,000 issued at $500,000 issued at $500,000 issued at $383,750 $523,750 Short Exercise 11-4 reviews pricing bonds. $478,750 $521,259

27

Issuing Bonds Payable at Maturity (Par) Value

Maturity value equals 100% bond value Cash received equals principal amount of bond Issuing journal entry Interest payments–semi-annually $100,000 x 9% x 6/12 = $4,500 The journal entry to record issuing a bond payable at maturity value includes a debit to Cash and a credit to Bonds payable. In this example, maturity value is $100,000 and the interest rate is 9%. These bonds pay interest semi-annually as do most bonds. Every six months, the company pays interest of $4,000 to the bondholders. This is computed by the interest formula—$100,000 x 9% x 6/12. Interest expense is debited and Cash is credited.

29

Issuing Bonds Payable at Maturity (Par) Value

Interest payments continue over the bond’s life Every 6 months interest is paid At maturity date, the principal is paid back When the bonds mature, Bonds payable is debited, which will zero out the account. Cash is credited to record payment to the bondholders.

31

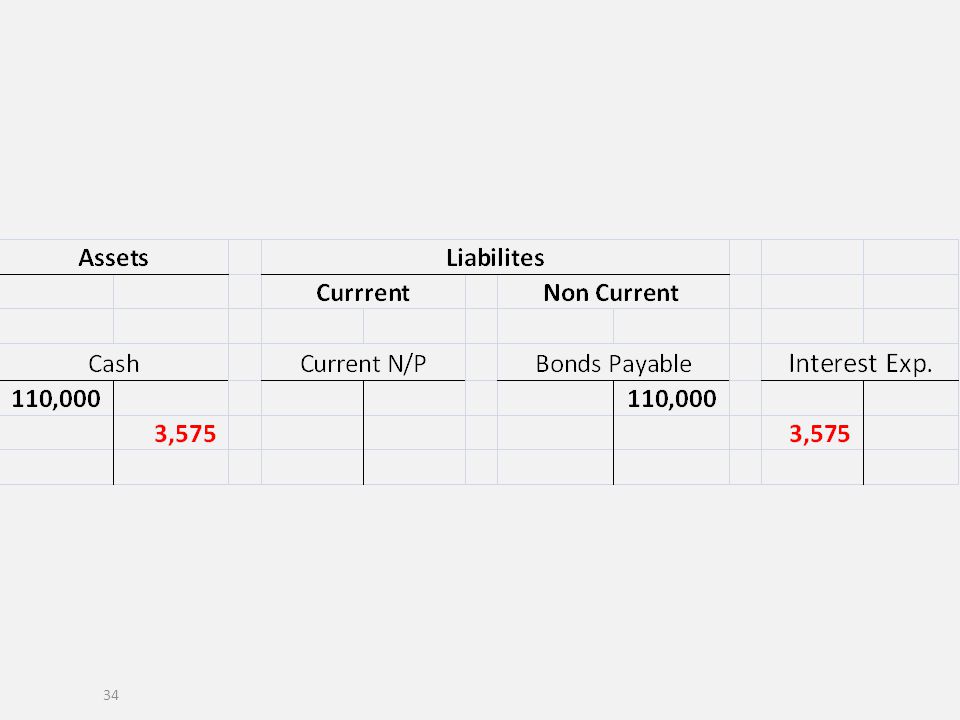

S11-5: Journalizing bond transactions

Vernon Corporation issued a $110,000, 6.5%, 15-year bond payable. Journalize the following transactions for Vernon and include an explanation for each entry Issuance of the bond payable at par on January 1, 2012 Journal Entry DATE ACCOUNTS DEBIT CREDIT Jan 1 Cash 110,000 Bonds payable Issued bonds payable. Short Exercise 11-5 reviews your knowledge of journalizing bond transactions.

33

S11-5: Journalizing bond transactions

Vernon Corporation issued a $110,000, 6.5%, 15-year bond payable Journalize the following transactions for Vernon and include an explanation for each entry: b. Payment of semiannual cash interest on July 1, 2012 Journal Entry DATE ACCOUNTS DEBIT CREDIT Jul 1 Interest expense 3,575 Cash Paid semiannual interest. The exercise continues on this slide.

35

S11-5: Journalizing bond transactions

(Continued) Journalize the following transactions for Vernon and include an explanation for each entry: c. Payment of the bond payable at maturity. (Give the date.) Journal Entry DATE ACCOUNTS DEBIT CREDIT Jan Bonds payable 110,000 Cash Paid off bonds payable at maturity. The exercise continues.

Journalize the following transactions for Vernon and include an explanation for each entry: c. Payment of the bond payable at maturity. (Give the date.) Journal Entry. DATE. ACCOUNTS. DEBIT. CREDIT. Jan Bonds payable. 110,000. Cash. Paid off bonds payable at maturity. The exercise continues.")

36

Issuing Bonds Payable at a Discount

Market interest 10%, bond stated rate 9% Cash received is less than the principal amount The journal entry Bond account balances Market conditions may force a company to accept a discount price for its bonds. Suppose a company issues $100,000 of its 9%, five year bonds that pay interest semiannually when the market interest rate is 10%. The market price of the bonds drops to , which means % of par value. The company receives $96,149 ($100, ) at issuance and makes this journal entry—debit Cash for the amount received, and credit Bonds payable for the maturity value of the bond. The difference of $3,851 is the discount and has its own account. Discount on bonds payable is a contra account to Bonds payable.

at issuance and makes this journal entry—debit Cash for the amount received, and credit Bonds payable for the maturity value of the bond. The difference of $3,851 is the discount and has its own account. Discount on bonds payable is a contra account to Bonds payable.")

37

Issuing Bonds Payable at a Discount

Balance sheet presentation Immediately after issuance Interest payments–semi-annually $100,000 X 9% X 6/12 = $4,500 What happens to the $3,851 discount? Bonds payable minus the discount gives the carrying amount of the bonds (known as carrying value). The balance sheet presents the carrying value of the bonds. It displays the maturity value of the bonds, less any bond discount, to arrive at the carrying value.

. The balance sheet presents the carrying value of the bonds. It displays the maturity value of the bonds, less any bond discount, to arrive at the carrying value.")

38

Issuing Bonds Payable at a Discount

The discount is amortized Gradual reduction of over time Dividing into equal amounts for each interest period The discount becomes additional interest expense Straight-line amortization Similar to straight-line depreciation Bond life yields the interest periods 5 year life at 2 times a year = 10 periods Discount divided by periods = amortized amount What happens to the $3,851 discount? The discount is additional interest expense to Smart Touch. The discount raises the company’s true interest expense on the bonds to the market interest rate of 10%. The discount becomes interest expense for the company through the process called amortization, the gradual reduction of an item over time. Amortize a bond discount by dividing it into equal amounts for each interest period. This method is called straight-line amortization and it works very much like the straight-line depreciation method. Therefore, 1/5 years (1 year out of 5 year life) times 6/12 of the year (semi-annually) or 1/10 of the $3,851 bond discount ($385, rounded) is amortized each interest period. Cash payment equals the regular stated interest payment. Interest expense of $4,885 for each six-month period is the sum of the stated interest ($4,500, which is paid in cash) plus the amortization of discount, $385.

times 6/12 of the year (semi-annually) or 1/10 of the $3,851 bond discount ($385, rounded) is amortized each interest period. Cash payment equals the regular stated interest payment. Interest expense of $4,885 for each six-month period is the sum of the stated interest ($4,500, which is paid in cash) plus the amortization of discount, $385.")

39

Issuing Bonds Payable at a Discount

Interest payments continue over the bond’s life Every 6 months, interest is paid Discount is amortized each payment period, reducing the account At maturity, the Discount account is zero and the carrying value is equal to maturity value At maturity date, the principal is paid back This same entry would be made again on December 31, So, the bond discount balance would be: $3,851 – $385 (from June 30 entry) – $385 (from December 31 entry) = $3,081 balance in the Discount on bonds payable account on December 31, 2013. Discount on bonds payable has a debit balance. Therefore, we credit the Discount on bonds payable account to amortize (reduce) its balance. Ten amortization entries will decrease the Discount to zero (with rounding). Then the carrying amount of the bonds payable will be $100,000 at maturity.

– $385 (from December 31 entry) = $3,081 balance in the Discount on bonds payable account on December 31, Discount on bonds payable has a debit balance. Therefore, we credit the Discount on bonds payable account to amortize (reduce) its balance. Ten amortization entries will decrease the Discount to zero (with rounding). Then the carrying amount of the bonds payable will be $100,000 at maturity.")

40

S11-7: Journalizing bond transactions

Origin, Inc. issued a $40,000, 5%, 10-year bond payable at a price of 90 on January 1, 2012. 1. Journalize the issuance of the bond payable on January 1, 2012. Journal Entry DATE ACCOUNTS DEBIT CREDIT Jan 1 Cash 36,000 Discount on bonds payable 4,000 Bonds payable 40,000 Short Exercise 11-7 reviews journalizing bond transactions.

41

S11-7: Journalizing bond transactions

(Continued) 2. Journalize the payment of semiannual interest and amortization of the bond discount or premium on July 1, 2012, using the straight-line method to amortize the bond discount or premium. Journal Entry DATE ACCOUNTS DEBIT CREDIT Jan 1 Interest expense 1,200 Discount on bonds payable 200 Cash 1,000 The exercise continues on this slide.

2. Journalize the payment of semiannual interest and amortization of the bond discount or premium on July 1, 2012, using the straight-line method to amortize the bond discount or premium. Journal Entry. DATE. ACCOUNTS. DEBIT. CREDIT. Jan 1. Interest expense. 1,200. Discount on bonds payable Cash. 1,000. The exercise continues on this slide.")

42

Issuing Bonds Payable at a Premium

Market interest 8%, bond stated rate 9% Investors pay a premium to acquire them Cash received is more than the principal amount Issuing journal entry Bond account balances To illustrate a bond premium, assume that the market interest rate is 8% when the company issues its 9%, five-year bonds. These 9% bonds are attractive in an 8% market, and investors will pay a premium to acquire them. The Bonds payable account and the Premium on bonds payable account each carries a credit balance. The Premium is an adjunct account to Bonds payable. Adjunct accounts are related accounts that have the same normal balance and that are reported together on the balance sheet.

43

Issuing Bonds Payable at a Premium

Balance Sheet presentation Immediately after issuance Interest payments–semi-annually $100,000 X 9% X 6/12 = $4,500 What happens to the $4,100 premium? The balance sheet presents the carrying value of the bonds. It displays the maturity value of the bonds, plus any bond premium, to arrive at the carrying value. The 1% difference between the bonds’ 9% stated interest rate and the 8% market rate creates the $4,100 premium ($104,100 – $100,000 face). The company borrows $104,100, but must pay back only $100,000 at maturity. The premium is like a saving of interest expense. The premium cuts the cost of borrowing and reduces interest expense to 8%, the market rate. The amortization of bond premium decreases interest expense over the life of the bonds.

. The company borrows $104,100, but must pay back only $100,000 at maturity. The premium is like a saving of interest expense. The premium cuts the cost of borrowing and reduces interest expense to 8%, the market rate. The amortization of bond premium decreases interest expense over the life of the bonds.")

44

Issuing Bonds Payable at a Premium

The premium is amortized Gradual reduction of over time Dividing into equal amounts for each interest period The premium reduces Interest expense Straight-line amortization Similar to straight-line depreciation Bond life yields the interest periods 5 year life at 2 times a year = 10 periods Premium divided by periods = amortized amount In our example, the beginning premium is $4,100, and there are 10 semiannual interest periods during the bonds’ five-year life. Therefore, 1/5 years times 6/12 months or 1/10 of the $4,100 (410) of bond premium is amortized each interest period. Interest expense of $4,090 is the stated interest ($4,500, which is paid in cash) minus the amortization of the premium of $410.

of bond premium is amortized each interest period. Interest expense of $4,090 is the stated interest ($4,500, which is paid in cash) minus the amortization of the premium of $410.")

45

Issuing Bonds Payable at a Premium

Interest payments continue over the bond’s life Every 6 months, interest is paid Premium is amortized each payment period, reducing the account At maturity, the Premium account is zero and the carrying value is equal to maturity value At maturity date, the principal is paid back This same entry would be made again on December 31, So, the bond discount balance would be $3,851 – $385 (from June 30 entry) – $385 (from December 31 entry) = $3,081 balance in the Discount on bonds payable account on December 31, 2013. Discount on bonds payable has a debit balance. Therefore we credit the Discount on bonds payable account to amortize (reduce) its balance. Ten amortization entries will decrease the Discount to zero (with rounding). Then the carrying amount of the bonds payable will be $100,000 at maturity.

– $385 (from December 31 entry) = $3,081 balance in the Discount on bonds payable account on December 31, Discount on bonds payable has a debit balance. Therefore we credit the Discount on bonds payable account to amortize (reduce) its balance. Ten amortization entries will decrease the Discount to zero (with rounding). Then the carrying amount of the bonds payable will be $100,000 at maturity.")

46

S11-8: Journalizing bond transactions

Worthington Mutual Insurance Company issued a $50,000, 5%, 10-year bond payable at a price of 108 on January 1, 2012. 1. Journalize the issuance of the bond payable on January 1, 2012. Journal Entry DATE ACCOUNTS DEBIT CREDIT Jan 1 Cash 54,000 Premium on bonds payable 4,000 Bonds payable 50,000 Short Exercise 11-8 focuses on journalizing bond transactions.

47

S11-8: Journalizing bond transactions

(Continued) 2. Journalize the payment of semiannual interest and amortization of the bond discount or premium on July 1, 2012, using the straight-line method to amortize the bond discount or premium. Journal Entry DATE ACCOUNTS DEBIT CREDIT Jul 1 Interest expense 1,050 Premium on bonds payable 200 Cash 1,250 The exercise continues.

2. Journalize the payment of semiannual interest and amortization of the bond discount or premium on July 1, 2012, using the straight-line method to amortize the bond discount or premium. Journal Entry. DATE. ACCOUNTS. DEBIT. CREDIT. Jul 1. Interest expense. 1,050. Premium on bonds payable Cash. 1,250. The exercise continues.")

48

Adjusting Entries for Bonds Payable

Interest payments seldom occur at year-end Interest must be accrued at year-end A payable account is credited for the liability Each interest entry must include amortization of discount or premium Actual interest payment date October, November, and December Companies may issue bonds payable when they need cash. The interest payment dates rarely are set on December 31, so interest expense must be accrued at year-end. The accrual entry records the interest expense and amortizes any bond discount or premium. January, February, and March

49

Bonds Issued Between Interest Payment Dates

Interest accrues from stated issue date Payments occur on stated interest payment dates Full payment to bondholders, regardless of their purchase date Payments cannot be split, full payments are made Interest accrued prior to issuance is collected at actual issue date Journal entry Corporations can also issue bonds between interest dates. If they do so, however, they must account for the accrued interest. Companies cannot split interest payments. They pay in either six-month or annual amounts as stated on the bond certificate. On the next interest date, Smart Touch will pay six months’ interest to whomever owns the bonds at that time. But the company will have interest expense only for the three months the bonds have been outstanding (April, May, and June).

.")

50

Bonds Issued Between Interest Payment Dates

Next interest payment date Interest payment recorded for normal six months Interest expense is equal to three months issued Interest payable decreased for the cash received at issue date Cash payment is always equal to the six month period On the next interest date, a company will pay six months’ interest to whomever owns the bonds at that time. But the company will have interest expense only for the three months the bonds have been outstanding. Remove the interest payable recorded at the bonds’ issuance, record interest expense for the time the bonds were held, and record payment.

51

1. Journalize the issuance of the bonds payable on May 1, 2012.

S11-10: Journalizing bond transactions—issuance between interest payment dates Silk Realty issued $300,000 of 8%, 10-year bonds payable at par value on May 1, 2012, four months after the bond’s original issue date of January 1, 2012. 1. Journalize the issuance of the bonds payable on May 1, 2012. Journal Entry DATE ACCOUNTS DEBIT CREDIT May 1 Cash 308,000 Bonds payable 300,000 Interest payable 8,000 Short Exercise reviews journalizing bond transactions, when issued between interest payment dates.

52

S11-10: Journalizing bond transactions—issuance between interest payment dates

(Continued) 2. Journalize the payment of the first semiannual interest amount on July 1, 2012. Journal Entry DATE ACCOUNTS DEBIT CREDIT May 1 Interest payable 8,000 Interest expense 4,000 Cash 12,000 The exercise continues on this slide.

2. Journalize the payment of the first semiannual interest amount on July 1, Journal Entry. DATE. ACCOUNTS. DEBIT. CREDIT. May 1. Interest payable. 8,000. Interest expense. 4,000. Cash. 12,000. The exercise continues on this slide.")

53

Liabilities on the Balance Sheet

Reports all current and long-term liabilities * Amounts assumed Payroll liabilities recorded Current portion of long-term liabilities At the end of each period, a company reports all of its current and long-term liabilities on the balance sheet. As we have seen throughout, there are two categories of liabilities—current and long-term. Long-term liabilities

54

S11-12: Preparing the liabilities section of the balance sheet

Blue Socks’ account balances at June 30, 2014, include the following: Prepare the liabilities section of Blue Socks’ balance sheet at June 30, 2014. Short Exercise reviews preparation of the liabilities section of the balance sheet.

55

S11-12: Preparing the liabilities section of the balance sheet

The solutions to the exercise is presented on this slide.

59

Retiring Bonds Payable

Why? Remove the cash responsibility Lower market interest rates Low value of the bonds How? Callable bonds—the company may call, or pay off, the bonds at a specified price. Price is usually at 100% or higher as incentive to buy originally Issuer has flexibility to payoff at will Purchases by market purchase or direct with bondholder involve same journal entry Normally, companies wait until maturity to pay off, or retire, their bonds payable. The basic retirement entry debits Bonds payable and credits Cash, as we saw in the chapter. But companies sometimes retire their bonds prior to maturity. The main reason for retiring bonds early is to relieve the pressure of paying the interest payments. Some bonds are callable, which means the company may call, or pay off, the bonds at a specified price. The call price is usually 100 or a few percentage points above maturity value, perhaps 101 or 102 to provide an incentive to the bond holder. Callable bonds give the issuer the flexibility to pay off the bonds when it benefits the company. An alternative to calling the bonds is to purchase them in the open market at their current market price. Whether the bonds are called or purchased in the open market, the journal entry is the same.

60

Retiring Bonds Payable

Assume: $100,000 bonds Discount $3,081 Current bond market price $95 Call price $100 Suppose on December 31, 2013, a company has $100,000 of bonds payable outstanding with a remaining discount balance of $3,081 (the original discount of $3,851 [$100,000 - $96,149] less the straight-line amortization of $385 in June and less the amortization of $385 in December). Lower interest rates have convinced management to pay off these bonds now. These bonds are callable at 100. If the market price of the bonds is 95, should the company call the bonds at 100 or purchase them in the open market at 95? The market price is lower than the call price, so the company should buy the bonds on the open market at their market price. Retiring the bonds on December 31, 2013, at 95 results in a gain of $1,919

. Lower interest rates have convinced management to pay off these bonds now. These bonds are callable at 100. If the market price of the bonds is 95, should the company call the bonds at 100 or purchase them in the open market at 95 The market price is lower than the call price, so the company should buy the bonds on the open market at their market price. Retiring the bonds on December 31, 2013, at 95 results in a gain of $1,919.")

61

Retiring Bonds Payable

Journal entry Close Bond payable and any discount or premium account Credit Cash for the amount paid A difference between carry value and purchase costs results in a gain or loss Carrying value exceeds purchase price = gain Purchase value exceeds carrying value = loss The journal entry removes the bonds from the books and records a gain on retirement. Any existing premium would be removed with a debit. If a company retired only half of these bonds, it would remove only half the discount or premium. A difference between carry value and purchase costs results in a gain or loss. If the carry value exceeds purchase price then a gain is recorded for the difference. If the purchase value exceeds carry value then a loss is recorded for the difference.

Similar presentations