Download presentation

Presentation is loading. Please wait.

1

Chapter 8

2

1. Saving 2. Commercial Bank 3. Savings Bank 4. Credit Union 5. Savings Account 6. Certificate of Deposit 7. Money Market Account 8. Annual Percentage Yield 9. Bond 10. Savings Bond 11. Face Value 12. Principal 13. Simple Interest 14. Compound Interest

3

1. What are some of the reasons to save? 2. How can having savings give you flexibility? 3. Why is rewarding yourself an effective saving strategy? 4. How do you think automatic deductions from your paychecks help you save? 5. Why is it important to having a saving strategy?

4

8.1

5

Saving is a tade-off You trade spending now for the ability to spend in the future The purpose of saving is to plan for the future and expenses you cant foresee Expected Vs. Unexpected expenses

6

Your future will include some unexpected expenses, it is a way of life Accidents happen, things break, and opportunities arise that you will need $$$$ for If you lose your job, your fixed expenses do not go away

7

Saving can allow you to take advantage of unexpected opportunities-Great deal on a car, vacation, investing, ect You never know what kind of options you may have, and saving will allow you to do that

8

Major purchases are expensive; homes, cars, boats all cost a lot of money Putting a little bit of money away each month and after gaining interest will help you afford what you want

9

Having savings can give you more flexibility in life You could possibly quit a job you don’t like for one that pays less, but you enjoy more

10

Your life goals will most likely cost a lot of money The sooner you start saving, the better!!!!!!! What are some of your life span goals?

11

Saving money is challenging, you must have a plan!

12

Use the note sheet to take notes on the saving strategies that we will talk about in class As we discuss think about which ones will work for you

13

Every time you pay your bills or cash a paycheck, make a deposit into your savings account. (You are paying yourself just as you pay your bills.) Consider this deposit to be a ‘required payment’, then leave it in the bank and don’t touch it. Since you don’t have this money in hand, you’re less likely to spend it.

Consider this deposit to be a ‘required payment’, then leave it in the bank and don’t touch it. Since you don’t have this money in hand, you’re less likely to spend it..")

14

Certain jobs especially part time jobs make different amounts of money each pay check If you have a job like this instead of saving the same amount each pay check, save a certain percent

15

You will continue your good habit of saving, if you reward yourself! Think of things that don’t cost that much money and reward yourself with them each time you put money in the bank Do not go overboard or you will ruin all your hard work!

16

You can decide not to buy an item now to get something you value later Example: Suppose you’re saving $20/week to have $400 for a vacation with friends. You see a jacket you love for $190. If you buy it, you’d be giving up the vacation you want later for the jacket you want now. If you value the vacation more, you won’t buy the jacket.

17

Payroll Deductions -Many companies will automatically deduct a certain amount of money from each of your pay check each month to be put into your savings account. Why is this a good strategy? Checking Account Transfers -You can authorize your bank to transfer a certain amount of money each month from your checking to your savings account. Be sure you record these transactions or your register will be off and you may over draw

18

Why is rewarding yourself an effective saving strategy? What is an effective way to save if you have an inconsistent income? How do personal values affect a savings plan?

19

8.2

20

You will be assigned a specific topic to read & become an expert on. You’ll teach the rest of the class about your subject area on Friday and Monday if necessary. You can: Write notes on chart paper, create a PPT presentation, make an interactive class game, create handouts/notes, design a group activity, etc. - - you must have some sort of visual! You will also be responsible for taking notes on other groups topics-collected and graded

21

1. Commercial Banks 2. Savings Banks 3. Savings & Loan Associations 4. Credit Unions (Not for profit) 5. Deposit Insurance 6. Savings Accounts 7. Interest Rates/Fees & Restrictions 8. Certificate of Deposit 9. Money Market Accounts 10. Annual Percentage Yield 11. Government Bonds & Treasury Securities 12. Savings Bonds (EE, HH, I)

5. Deposit Insurance 6. Savings Accounts 7. Interest Rates/Fees & Restrictions 8. Certificate of Deposit 9. Money Market Accounts 10. Annual Percentage Yield 11. Government Bonds & Treasury Securities 12. Savings Bonds (EE, HH, I).")

22

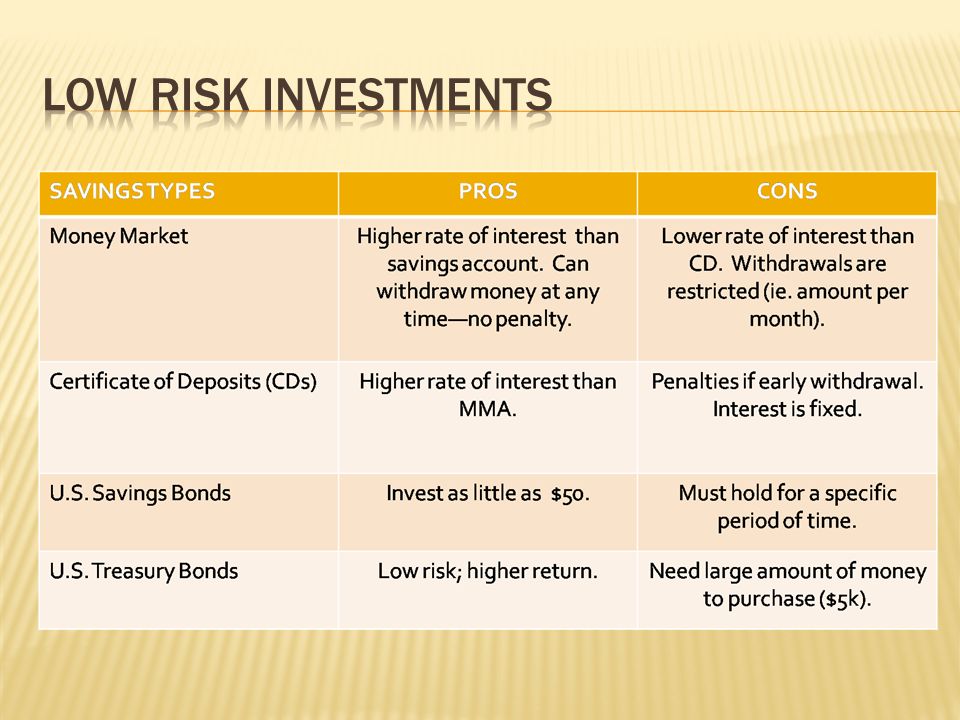

8.4

25

Corporate Bonds Mutual Funds Stocks Real estate (other than primary home) Coins and collectibles

Coins and collectibles")

26

Interest is money that is paid to you for making an investment decision. The way your bank calculates interest on your savings will determine how quickly your money will grow.

28

Is the money that you have on deposit in a savings account, CD or other savings option. (balance) Interest is calculated on the principal. Example: You have $100 in your savings account. That means your principal balance is $100. You earn 10% interest on your account every month. In order to calculate your interest payment you must multiply your principal balance ($100) by the interest rate (10%). After doing so, you can easily tell that you will receive $10 in interest income at the end of the month. So, your new principal balance becomes $110 ($100 balance + $10 interest).

Interest is calculated on the principal. Example: You have $100 in your savings account. That means your principal balance is $100. You earn 10% interest on your account every month. In order to calculate your interest payment you must multiply your principal balance ($100) by the interest rate (10%). After doing so, you can easily tell that you will receive $10 in interest income at the end of the month. So, your new principal balance becomes $110 ($100 balance + $10 interest)..")

29

YOU MUST REMEMBER AND UNDERSTAND THESE FORMULAS: To Calculate Interest: -Interest = Principal X Interest Rate To Calculate New Principal: -New Principal = Interest + Beginning Principal

30

Simple Interest: Interest paid once a year (at the end of the year) on the average balance in a savings account. It is the amount you earn on your deposits, not on any previous interest paid. Example: Following are your monthly account balances for 2008: At the end of the year, your bank will pay you 6% in simple interest. How much interest will you earn at the end of the year? What will your new principal balance be?

31

1. Compute the average monthly account balance: Add monthly balances = $1475 Divide monthly balances by 12 = $122.92 2. Multiply the average monthly account balance by the interest rate: $122.92 x 6%= $7.38 3. Add your interest payment to your last account balance to get your new principal balance: $7.38 + $100 = $107.38

32

Figure out your average account balance: -$760/12 = $63.33 Figure out your interest payment: -$63.33 x 10%= $6.33 Compute your NEW principal balance: -$40 + $6.33 = $46.33 Your bank is going to pay you 10% in simple interest at the end of the year. How much will they pay you in interest and what will your new principal balance be?

34

Compound Interest: Interest paid on the principal plus any previous earned interest (which is left in the account). “Interest on Interest” Interest can be compounded in several ways: Annually – every year Semi-Annually – every 6 months Quarterly – every 3 months Monthly Daily *The more often interest is compounded, the more interest your money earns!

35

At the end of year one, you have a $100 principal balance. You earn 10% in interest, so your principal balance is $110. At the end of year two, your principal balance is the same $110. You still earn 10% in interest (which is compounded annually). What is the interest and your new principal balance? $110 x 10% = $11 is the interest $11 + $110 = $121 is the new principal balance What is the interest & principal balance at end of year 3? $121 x 10% = $12.10 $121 + $12.10 = $133.10 What is the interest & principal balance at end of year 4? $133.10 x 10% = $13.31 $133.10 + $13.31 = $146.41 What is the interest & principal balance at end of year 5? 146.41 x 10% = $14.64 $146.41 + $14.64 = $161.05

. What is the interest and your new principal balance. $110 x 10% = $11 is the interest $11 + $110 = $121 is the new principal balance What is the interest & principal balance at end of year 3. $121 x 10% = $12.10 $121 + $12.10 = $ What is the interest & principal balance at end of year 4. $ x 10% = $13.31 $ $13.31 = $ What is the interest & principal balance at end of year 5. x 10% = $14.64 $ $14.64 = $")

36

Interest rates are always stated in annual terms. In order to figure out the semi-annual rate, you have to divide the interest rate by 2. Example – 6% interest rate compounded semi-annually= 3% every 6 months If your principal balance is $100 and you earn 6% interest, compounded semi-annually, what is your balance at the end of year 1? $100 x 3% = $3 interest for first ½ year $103 principal balance after 6 months $103 x 3% = $3.09 interest for second ½ year $106.09 is principal balance after one year What is the interest & principal balance at end of year 2? $106.09 x 3% = $3.18 interest $109.27 principal balance after 18 months $109.27 x 3% = $3.28 interest $112.55 is principal balance after year two *Note: Compounding semi-annually results in more earned interest as compared to annual compounding.

37

With daily compounding, your savings will grow the fastest!!! Banks use computer programs to calculate compound interest – you can simplify your calculations by using a compound interest table. The table lists the value of one dollar at several percentage rates, compounded daily for different periods of time.

38

Example 1: Suppose you deposit $1,000 at 10% compounded daily. You plan to withdraw the money in four years. How much money will you have in your account after 4 years? Find the corresponding figure on the table and multiply it by the balance. $1,000 x 1.49 = $1,490 Example 2: You deposit $100 at 6% compounded daily. You plan to withdraw in five years. How much money will you have in your account after 5 years? $100 x 1.35 = $135

39

How long will it take for an investment to double? Use the Rule of 72! 72 DIVIDED BY the interest rate = the number of years it will take for money to double in value. Example: If you have $1,000 to invest. How long will it take to DOUBLE your money with an 8% interest rate? 72/8 = 9 years

40

Know the benefits of saving your money. Know the 5 savings strategies – reward yourself, savings & values, automatic transfer, pay yourself first, save by the numbers. Also keep in mind which one works best for you right now.

41

Why do you have a better chance of achieving long-term financial goals if you start saving when you’re young? Commercial banks vs. Credit unions CDs & Bonds (face value)

.")

42

Money Market accounts – How are the different from other financial accounts (CDs, Savings accounts)? Why does the interest rate change over time? Define Principal, Simple Interest & Compound Interest

43

Know ways interest can be compounded (daily, annually). Annual Percentage Yield (APY)—what is it? Be able to compute interest compounded annually, simple interest & new principal balances.

—what is it. Be able to compute interest compounded annually, simple interest & new principal balances..")

Similar presentations