Download presentation

Presentation is loading. Please wait.

2

Credit Cards are a part of most American’s lives, but if you don’t know how to use them, they can really make your life more difficult Credit cards don’t give a person “free money” They are short term loans from companies that are looking to make profits

3

Credit Card Customers are divided into two categories Those that pay off their balances every month Those that carry a balance for months at a time This is also called a “revolving balance” Revolving accounts are charged interest known as….

4

Debit Cards these withdraw money from a personal savings or checking account They are NOT the same as a credit card Once you run out of funds in your account, you are unable to buy anything else Automated Teller Machines (ATM) are used to dispense cash for debit card users, ATMs usually charge a fee if the user’s bank is from a different bank from the ATMAutomated Teller Machines (ATM) are used to dispense cash for debit card users, ATMs usually charge a fee if the user’s bank is from a different bank from the ATM Many debit cards are sponsored as Visa or MasterCard and can be used as a point-of- sale purchase by typing in a PIN numberMany debit cards are sponsored as Visa or MasterCard and can be used as a point-of- sale purchase by typing in a PIN number This is usually a 4 digit number that the cardholder must type in order for the transaction to be completedThis is usually a 4 digit number that the cardholder must type in order for the transaction to be completed

are used to dispense cash for debit card users, ATMs usually charge a fee if the user’s bank is from a different bank from the ATMAutomated Teller Machines (ATM) are used to dispense cash for debit card users, ATMs usually charge a fee if the user’s bank is from a different bank from the ATM Many debit cards are sponsored as Visa or MasterCard and can be used as a point-of- sale purchase by typing in a PIN numberMany debit cards are sponsored as Visa or MasterCard and can be used as a point-of- sale purchase by typing in a PIN number This is usually a 4 digit number that the cardholder must type in order for the transaction to be completedThis is usually a 4 digit number that the cardholder must type in order for the transaction to be completed")

5

Immediate access to money to purchase goods Convenience Use for emergencies Establishment of a good credit history Consolidation of debts Identification

6

Costs more if unpaid balance is not paid monthly Ties up to future income Tempts one to overspend Decreases future buying power

7

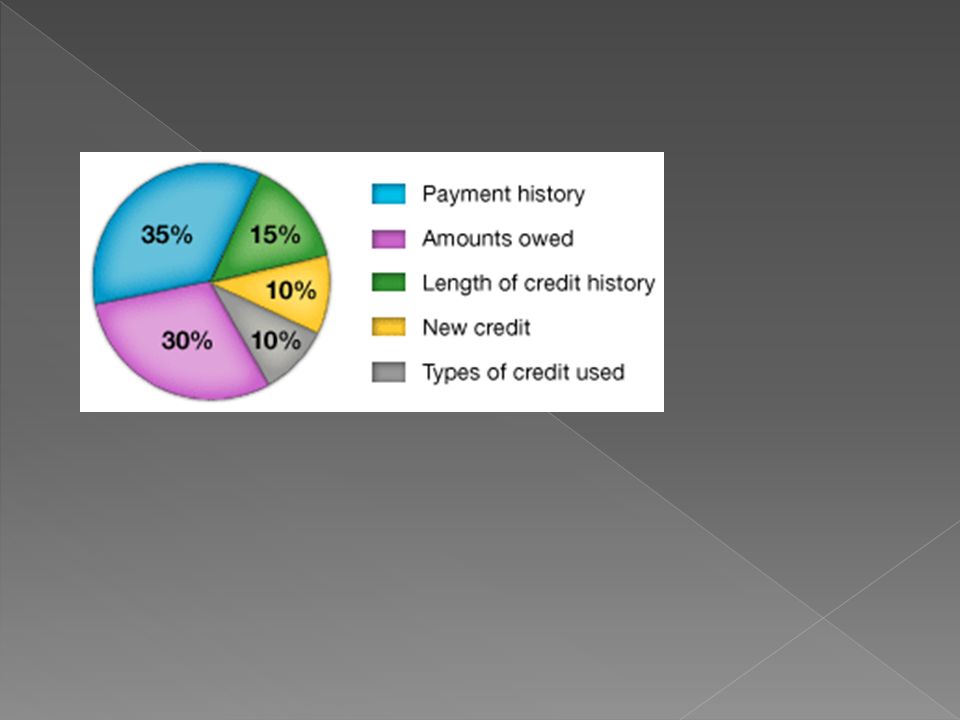

Capacity › Your ability to pay back the loan Collateral › Your assets used as a guide to determine your ability to repay the debt Character › Your reputation as a reliable and trustworthy person

8

Interest = Principal x Rate x Time (I=PxRxT) Interest is a charge on a loan Principal is the amount of the loan Rate is the percentage of interest charged on the loan to the borrower Time is the length of time in years or fractions of years taken to pay off the loan

Interest is a charge on a loan Principal is the amount of the loan Rate is the percentage of interest charged on the loan to the borrower Time is the length of time in years or fractions of years taken to pay off the loan")

9

Sharon purchased this 2003Jaguar for 28,000 at an interest rate of 7.5% to be paid back in 36 months. What is the $ amount of interest Sharon will pay on this loan? What is the total amount of the car with interest?

10

DEBIT AND ATM CARDS If you report your card lost or stolen, this law limits your liability for unauthorized charges and withdrawals › If you report within 2 days, loss limited to $50 › If you report between 3and 60 days, loss limited to $500 › If you wait more than 60 days, you can lose all your money

11

BORROWING MONEY Creditors must disclose terms of credit in simple terms Annual Percentage Rate (APR) must be stated All credit terms must be mentioned CREDIT CARDS Protects credit cards against unauthorized use If lost or stolen, you are liable for no more than $50 of the unauthorized charges before you notify issuer

must be stated All credit terms must be mentioned CREDIT CARDS Protects credit cards against unauthorized use If lost or stolen, you are liable for no more than $50 of the unauthorized charges before you notify issuer")

12

Why does the APR matter? A higher APR means the interest rate is higher If you were to make a purchase of $200 on a credit card with an APR of 12% If you pay off your balance within the grace period (20- 25 days) Amount of Purchase: 200 Interest Charged: 0 Total Cost of Purchase: 200 If you carry a revolving balance Amount of Purchase: 200 If you make the minimum payment of $10, it will take 22 months to pay off this credit card Interest Charged: 24 Total Cost of Purchase: 224

Amount of Purchase: 200 Interest Charged: 0 Total Cost of Purchase: 200 If you carry a revolving balance Amount of Purchase: 200 If you make the minimum payment of $10, it will take 22 months to pay off this credit card Interest Charged: 24 Total Cost of Purchase: 224.")

13

Every credit card offer comes with a disclosure statement that outlines the terms and fees that are associated with the card However, this doesn’t mean that these statements are easy to read They often have lots of “fine print” and use terms that most consumers are not familiar with

14

Annual Percentage Rate (APR): the amount of interest charge on unpaid credit card debt. Divide by 12 to find the monthly charge the amount of interest charge on unpaid credit card debt. Divide by 12 to find the monthly charge

15

Penalty APR: ( also known as Default Rate ) A much higher, punitive interest rate that credit card companies may apply to cardholders who have exceeded their credit limits, made one or more late payments, or are otherwise in "bad standing." A much higher, punitive interest rate that credit card companies may apply to cardholders who have exceeded their credit limits, made one or more late payments, or are otherwise in "bad standing." Penalty APRs are, on average, about 52% higher than regular APRs. Penalty APRs are, on average, about 52% higher than regular APRs.

16

Grace Period: The time during which a transaction does not accrue interest. The time during which a transaction does not accrue interest. Grace periods range from 0-30 days, with an average of 23 days, and they often apply only to purchases, not cash advances or other transactions. Grace periods range from 0-30 days, with an average of 23 days, and they often apply only to purchases, not cash advances or other transactions. On most cards, grace periods only apply if the previous month’s balance is paid in full and on time. On most cards, grace periods only apply if the previous month’s balance is paid in full and on time.

17

Membership Fees a charge (usually annually) for the card. Many companies do not charge a membership fee.

18

Late Fees The charge for a payment that is received by the credit card issuer after the due date

19

Transaction Fee: The fee (charged on charges other than purchases) is usually a percentage of the transaction, but a minimum fee may apply Balance Transfer: Using one credit card to pay another credit card or debt. Consumers usually transfer balances when applying for a new card, to take advantage of low introductory APRs. Balance transfers usually incur transaction fees. Cash Advance: An immediate cash loan from a consumer's credit card account. › Cash advances may carry a higher APR than purchases, and often are assessed transaction fees. › Grace periods may not apply to cash advances.

20

Condo Condo George purchased this 3BR/2 bath condo near the lakefront on the north side of Chicago for $350K. After putting 20% of the price down, he financed the remainder of the cost in a 30 fixed rate mortgage of 5%. What is the amount of interest that he will pay? What is the total amount of the loan plus the interest?

22

Credit Limit: the maximum amount you can charge on your card without receiving a penalty charge

24

Universal Default If you are late on a payment, the credit card company will increase your APR to a higher rate as a penalty Some credit card companies share this information with other companies….. and you may have your APR raised on a card that you have NEVER had a late payment This is called

Similar presentations