Download presentation

Presentation is loading. Please wait.

1

Chapter 4 Budgeting and Balance Sheets

2

Terris walked into his new apartment and sat down. After completing a prestigious music program in New York, the day he had been working toward for years was finally here. In his hands was his first paycheck from his first real job! At long last, he could begin to live the life of his dreams. Immediately he began to think about the purchases he had been putting off for so long-a new car, a laptop, some nice clothes. Maybe he could buy season tickets for baseball or a new stereo system. Or perhaps he could finally make good on his promise to his friend Martin to take that road trip to Chicago. Now he had the income to afford these things – or, at least, to pay off his credit card bills. Just as he was getting excited, Terris seemed to hear a small voice in his head. It was his grandfather. “Use your head, Terris,” he could almost hear him say. “be sure to put something aside for a rainy day!” Terris sighed. He realized he probably could not afford to get all the things he wanted right away. He also knew he had to think about more than just spending his new paycheck. At the same time, he was ready to treat himself. He had worked hard to get to this point, and he felt he deserved to enjoy the rewards.

3

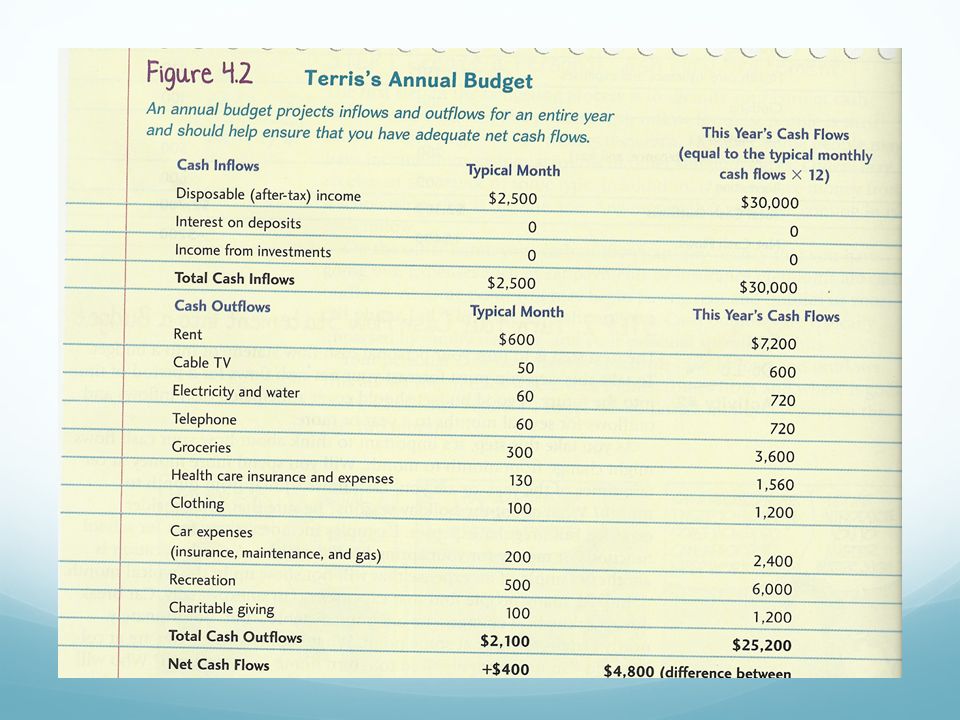

Creating a Budget A Budget is a forecast of future cash inflows and outflows. Step 1: Create a Personal Cash Flow Statement Cash inflows represent money coming in. It can include salary, scholarships, or any other money you have coming in. Cash outflows represent money that is going out. It can include car payments, insurance premiums, cell phone bills. The Personal Cash Flow Statement will include both of these.

5

Step 2: Turn your Cash Flow Statement into a Budget To create a budget you must forecast your net cash flows for a period of time into the future. A good budget should cover anticipated cash inflows and outflows for several months to a year or more. Example: My Electric bill this month is $120. Last month it was $130. It is higher in the summer because I use the air conditioner. I estimate that I should budget around $135 for my electrical bill each month to be sure I am covering the highest cost during this season.

6

Extra things to look out for in Budget Emergency Fund Remember that you need to start out with $500-$1000 and then gradually build up to 3-6 months of expenses. Holiday seasons How many people do you hope to get gifts for. You need to save up for this throughout the year to prepare. School activity fees Vacations you hope to take What are your plans for spring break? Is your family going on a vacation and you want some extra spending money?

8

Working with and Improving Your Budget One of the primary benefits of a budget is that it will help you anticipate future cash shortfalls. Think back to Terris. He has an older car which will cost $200 to get inspected every year. He also knows that on top of the cost of the inspection his car will usually need some kind of repairs to help it pass. Anticipating this, he will allocate a portion of his budget for car repairs. He can save up for this a little bit every month. He will of course be making some sacrifices by setting that money aside, but the benefit is that he won’t have a massive repair bill that he can’t afford come inspection time.

9

Assessing the Accuracy of the Budget To ensure that you are accurate in your budgeting, it is important to track and evaluate actual costs and compare them to what you have budgeted There are several ways to do this. Create an expense journal Track actual expenses on the same worksheet you have your budget. The second option is probably the easier one as it will allow you to see everything side by side.

10

This is an example of Terris’s Expense Journal

11

Accuracy of the Budget Forecast Error- a forecast error is the difference between what you forecast to happen and what actually happens. Terris obviously needs to revisit his budget. His actual cash outflows are $1,100 more than he budgeted. Question: Has Terris failed because his numbers didn’t line up? Should he give up on budgeting?

12

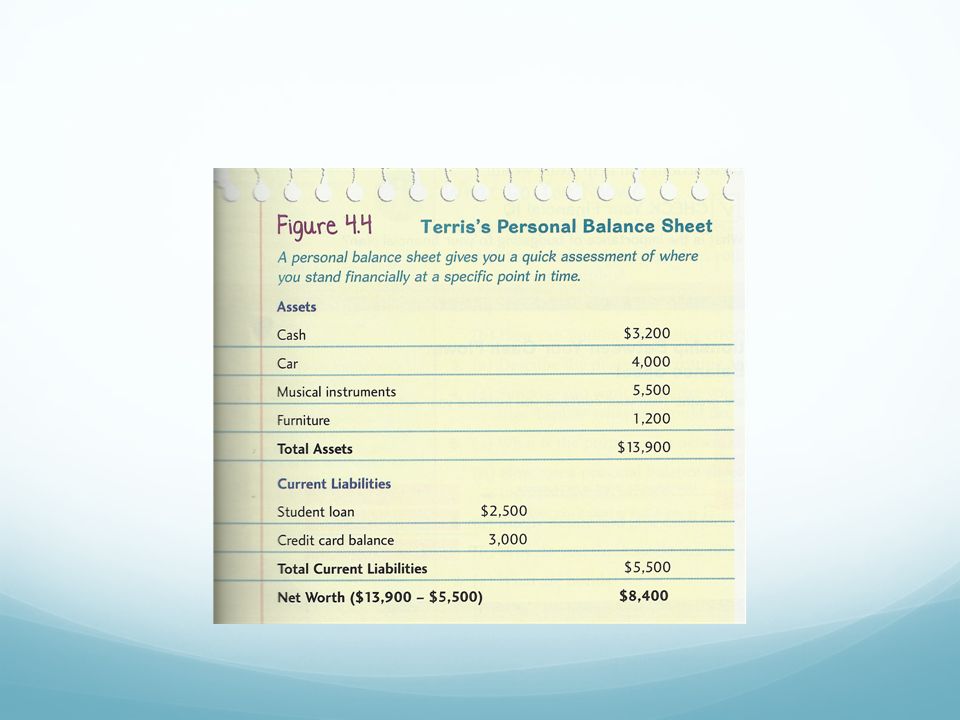

Personal Balance Sheet A Personal Balance Sheet is a summary of our assets, our liabilities, and our net worth at a point in time. It is important to your financial success to have an accurate accounting of your net worth. Assets, or things that you own, are divided into three main categories Liquid Assets Household Assets Investments

13

Liquid Assets These are financial assets that are either cash or can be quickly and easily converted into cash without significant loss in the value of the asset. All assets can be converted into cash, but the liquid assets won’t lose much value. Examples of this includes money in checking or savings accounts. Liquid assets are necessary for unexpected emergency expenses. (You will each have an emergency fund) Question: How much money should you have in an emergency fund to start? What amount are you saving up toward?

Question: How much money should you have in an emergency fund to start. What amount are you saving up toward .")

14

Household Assets These include those assets typically owned by a household Examples include: Cars, houses, and furniture. These items will typically take up the larger portion of your balance sheet than liquid assets. When creating a personal balance sheet, you will need to evaluate the true market value if you were to sell these items.

15

True Market Value True Market Value: the worth of something if you sold it today. Houses: This number would come from a realtor who would compare the value of your home to the value of similar homes in your neighborhood. Cars: The true market value of cars can usually be found on kbb.com. This is the Kelly Blue Book. On this website you can choose the model, make, year, condition, and features of your specific car. The website will then tell you what an individual or company would pay for your car. Furniture: For calculating this you would have to account for condition of the furniture and the age. The value of the furniture will typically go down each year. This is called depreciation. Your car will also depreciate each year that you own it.

16

Investments Investments are something you acquire with the ultimate goal of making money on it. There are many different types of investments. Money Market accounts CD accounts Bonds Stocks Mutual Funds Real Estate And many more

17

Money Market This is a type of bank account. The bank will take the money you put into this account and invest it into Mutual Funds. Although the company makes the majority of the money on this, you will have a small percentage of interest that will be returned to you. This is where you put your Emergency Fund!!! The emergency fund needs to go into a Money Market account so that it will earn some interest, but it will be very easy to take out.

18

CD Account A Certificate of Deposit Account is a type of savings account. Your money is locked in this account for a specified time period. It could be 6 months, 1 year, or 5 years. The bank will give you a certificate for your records. They will then invest your money and return a percentage to you as interest. This is not a good investment. The interest returned to you is not much higher than a Money Market account and you are penalized for taking your money out early.

19

Bonds Bonds are certificates that function like IOUs. Bonds can be purchased from companies, cities, states, and the federal government. This is similar to a CD Account in that they are purchased for a certain period of time and they accrue interest. Essentially, you are lending the company or government money to keep on their feet. This is a semi-risky investment as companies and even city governments have gone bankrupt and have not been able to pay the bonds back.

20

Stocks When you buy a stock, you will be given a certificate that represents a small piece of ownership of a company. Most companies have a large number of stocks that they sell, so your ownership in the company would be rather small. Single stock purchases are a risky choice because the company could crash at any time and for any reason. You could make some decent money if you know what you are doing, but with greater return comes greater risk.

21

Mutual Funds Mutual funds are created so that investors can pool their money in order to invest in a larger variety of financial assets, such as stocks or bonds from many companies. They are managed by Professional Portfolio Managers. Most require a minimum investment of $50-$3000. This is a safer type of investment. It should make up a larger portion of your investment portfolio. The risk is spread out because so many people invest in it and the money is spread out through different companies.

22

Real Estate Real Estate includes homes, rental properties, farms, and other land. This is a risky investment. You would regret adding this to your investment package unless you had a lot of money.

23

Liabilities Liabilities are the amount of debt that you owe. Current liabilities – Debts that must be paid off within one year. Examples: Credit card balances. Long-term Liabilities – They will take longer than one year to pay off Examples: Student loans, car loans, home mortgages.

24

Net Worth Net Worth is the difference between your assets and your liabilities. Figuring your net worth is an easy way to measure your wealth.

25

Changes in Your Personal Balance Sheet This will change as you acquire new assets or new liabilities. Be sure to update this regularly

26

Analyze Your Personal Balance Sheet Analyze where you are at on a regular basis and make needed changes. Below is an example of Terris’s Personal Balance Sheet.

Similar presentations

>")