Download presentation

Presentation is loading. Please wait.

1

2 nd European Microfinance Conference 2005 WORKSHOP « Scoring or not scoring your clients? » Barcelona 27 October 2005

2

Building and Implementing Credit Scorecards 2 nd European Microfinance Conference Thursday, 27 October 2005

3

Structure of Presentation 1.Presentation of Scoring Methodology 2.Conditions of Implementation 3.Lessons Learned in Eastern Europe 4.Things to Avoid

4

Presentation of Scoring Methodology

5

What is Credit Scoring? All credit scoring uses quantitative measures of the performance and characteristics of past loans to predict the future performance of loans with similar characteristics (Source: Mark Schreiner, Credit Scoring for Microfinance: Can it Work?, August 2004)

.")

6

How Does Application Credit Scoring Work? 1.Credit officer collects information from client 2.Credit officer enters information into scoring model 3.Model score recommends further action: Score RangeAction > 300Approve 200-300Review < 200Decline

7

The Scoring Process Client Interview, Document Collection Additional Review (if required) Credit Committee Reject Time in Minutes 20 15 10 Minutes Spent on Credit Decision: 30- 45 Enter data into user form Reject Scorecard

Credit Committee Reject Time in Minutes Minutes Spent on Credit Decision: Enter data into user form Reject Scorecard")

8

Benefits of Credit Scoring Increase Efficiency: –Reduce analysis time on small deals –Provide client with a quick decision Increase Consistency –Reduce subjectivity –Standardize evaluation across loan officers –Facilitate measurable adjustments to credit policy Improve Portfolio Risk Management –Risk rate portfolio –Prioritize collections strategies

9

Conditions of Implementation

10

Who Can Build a Scorecard? ANY BANK can mine its own institutional knowledge base and historical portfolio data to develop scorecards that suit its strategies for the small business segment

11

2 Main Types of Credit Scoring Models 1. Statistical 2. Judgmental (launch) ln[p/(1-p)] = a + BX + e

ln[p/(1-p)] = a + BX + e.")

12

Statistical Models –Empirically derived from past data –Need data on thousands of good and bad cases of same type of loans –Data sources: application data, financial statement data, internal payment history data –Score is a probability that the loan will go “bad” or be problematic

13

Judgmental Models –Used in cases where banks have little or no: historic data or access to credit bureau information. –Based on decision rules, experience, knowledge of local market –Build data pool to transform judgmental model into statistical model in future –Score ranks loans in terms of relative risk (ie 300 is less risky than 200 is less risky than 100, etc.)

.")

14

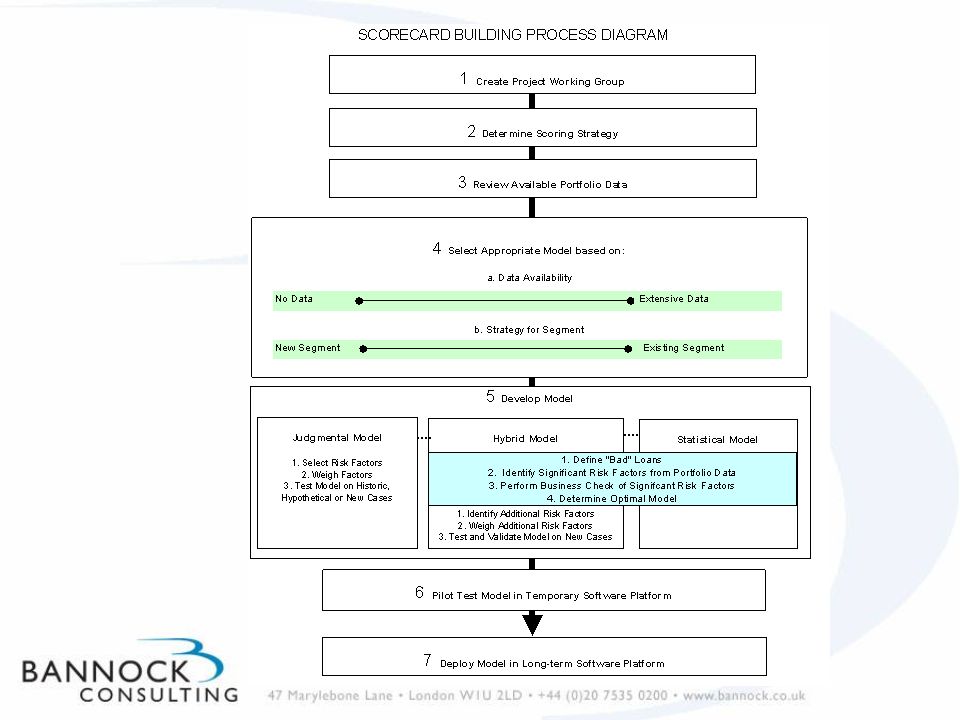

The Big Picture on Building Application Scorecards

16

Lessons Learned in Eastern Europe

17

Bannock’s Experience in Eastern Europe Type of Company (Country) Type of ModelSegmentYears in Use Bank (Latvia)Judgemental Secured loans up to EUR 30,000 4 + Bank (Lithuania)Judgemental Secured loans up to EUR 30,000 3 + Bank (Slovakia)Judgemental Secured loans up to EUR 30,000 1 + Bank (Bulgaria)Judgemental Secured loans up to EUR 25,000 2 + Bank (Slovakia)Judgmental Secured loans up to EUR 75,000 Pilot Testing Bank (Bulgaria)Statistical Secured loans up to USD 50,000 Under Development Leasing Company (Slovakia) Hybrid* Vehicle Leases to EUR150,000 <1 Leasing Company (Hungary) Hybrid* Equipment to EUR 150,000 Under Development

Type of ModelSegmentYears in Use Bank (Latvia)Judgemental Secured loans up to EUR 30, Bank (Lithuania)Judgemental Secured loans up to EUR 30, Bank (Slovakia)Judgemental Secured loans up to EUR 30, Bank (Bulgaria)Judgemental Secured loans up to EUR 25, Bank (Slovakia)Judgmental Secured loans up to EUR 75,000 Pilot Testing Bank (Bulgaria)Statistical Secured loans up to USD 50,000 Under Development Leasing Company (Slovakia) Hybrid* Vehicle Leases to EUR150,000 <1 Leasing Company (Hungary) Hybrid* Equipment to EUR 150,000 Under Development")

18

Positive Results Used over 3 years in 5 banks in CEE Well over 10,000 transactions scored Decision time reduced to one day Portfolio quality constant generally < 2% over 30 days past due

19

Other Lessons Learned Find a scoring “champion” to manage the model Provide on-going training Continue to monitor the model Capture data on rejects and policy overrides Over time, it is possible to transform a judgmental model into a statistical model

20

Things to Avoid

21

“0ff the shelf” models – better to put time and resources into a bespoke model Confusion between application scoring and Basel 2 probability of default models – these are not necessarily the same

22

QUESTIONS? Dean Caire, CFA dean_caire@bannock.co.uk +371 654 1404

Similar presentations

GAO’s Report on Electronic Disbursement of Federal Benefit Payments (GAO-08-645) Presented by Kay Kuhlman,>")