Download presentation

Presentation is loading. Please wait.

1

MDTA Subgroup Meeting Update of Macroeconomic Developments By IMF Dhaka office June, 2002 Do Not Quote For Background Purposes Only

2

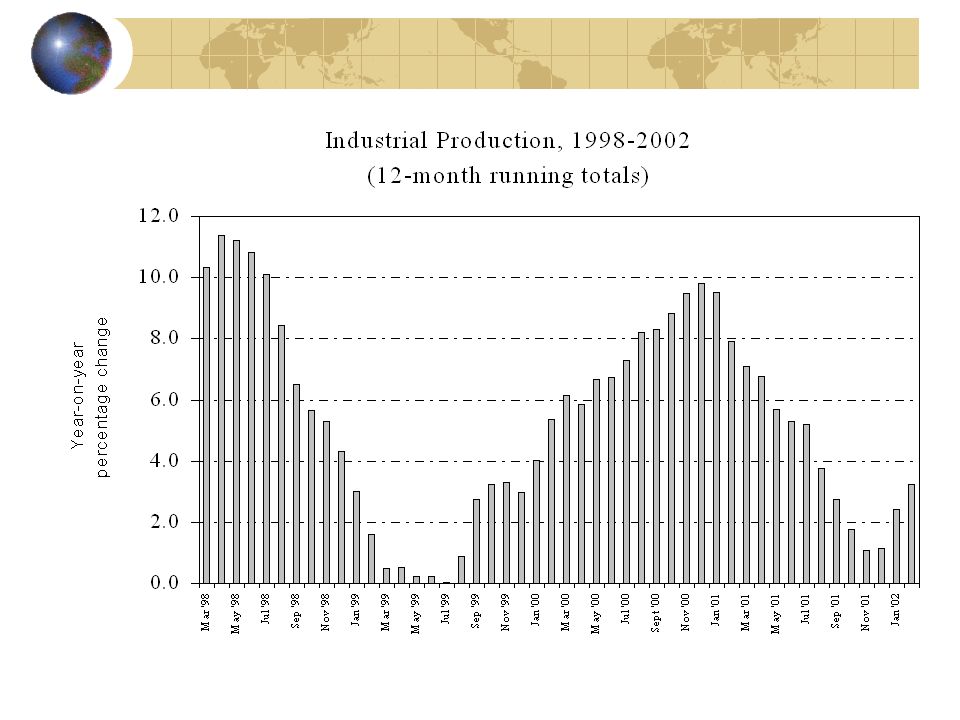

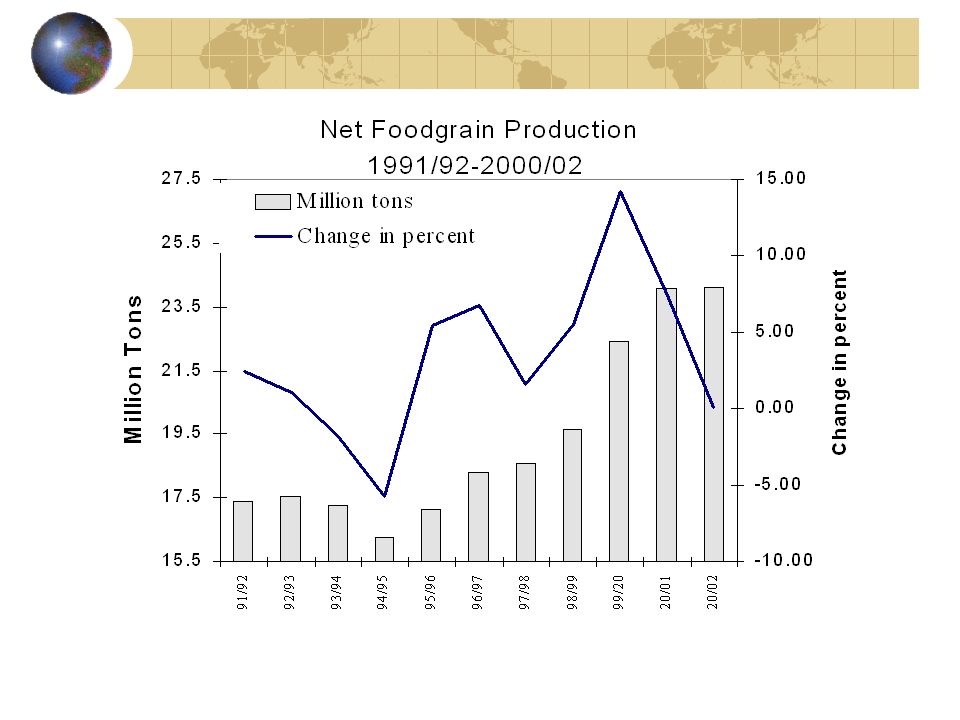

Production The decline in the growth rate of industrial production is bottoming out Cereal production is projected to remain flat in FY01/02

5

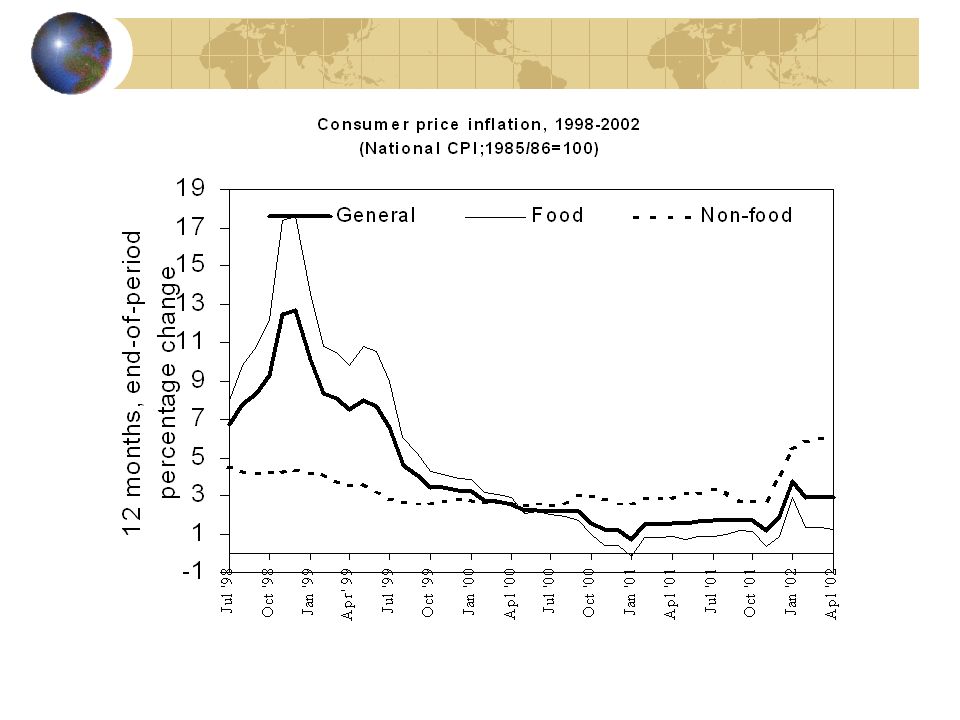

Inflationary pressures emerge? Overall consumer price inflation has increased, although it remains modest at 2.1 percent in the 12 months through April But nonfood inflation has accelerated to 6 percent

7

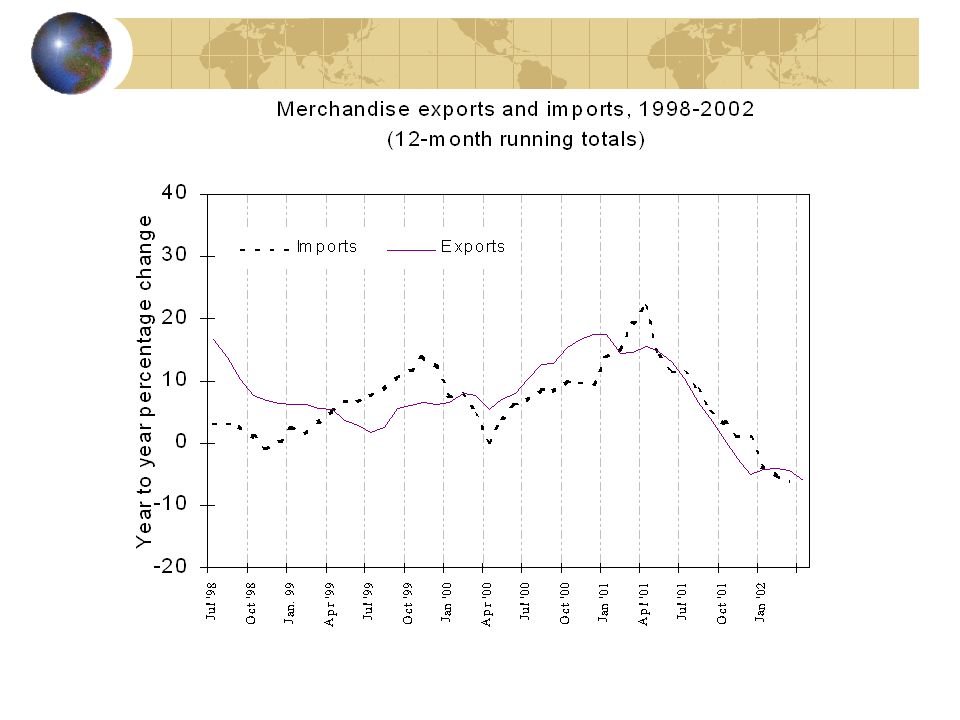

Exports and imports remain down Exports remain weak after a brief upturn early in 2002, but rates of decline seem to have slowed down RMG exports mirrors the pattern of overall export Imports move down with exports, but without a deceleration in the rate of decline

9

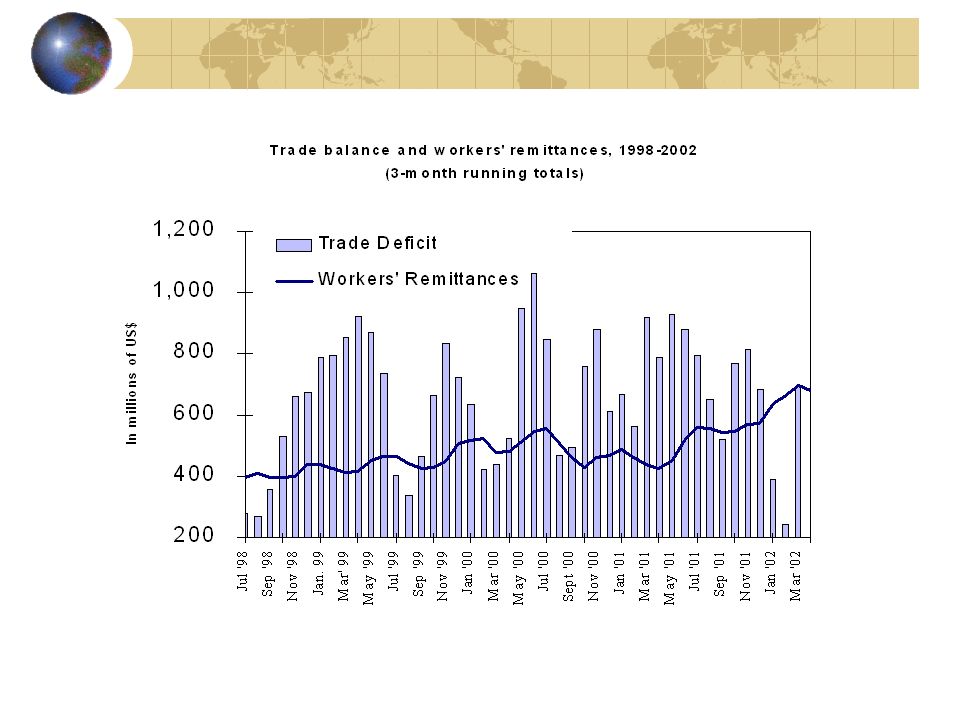

Remittances now cover trade deficit—but is this sustainable? The trade balance does not show a sustained improvement But remittances, which used to cover about half of the trade deficit, have surpassed the trade deficit during the 6 months months through March But registered workers leaving for abroad have declined by 17 ½ percent in the 12 months through March

11

Reserves remain up Gross reserves have crossed the $1.5 billion mark, but may fall below that level again when the next payment to the Asian Clearing Union is made This is equivalent to about 7 ½ weeks of imports

13

Reduced recourse to government borrowing… Since end-October, the Government has reduced borrowing from the banking system from Tk 27 billion (from end-June) to Tk 12 billion at end-April—since then, it has increased somewhat Total domestic borrowing (including savings certificates) increased from Tk 45 billion at end-October to Tk 54 billion at end-April—a marked deceleration

to Tk 12 billion at end-April—since then, it has increased somewhat Total domestic borrowing (including savings certificates) increased from Tk 45 billion at end-October to Tk 54 billion at end-April—a marked deceleration")

14

…through spending restraint In the 11 months through May, NBR revenue were Tk 176 billion—Tk 6 billion short of the target Cuts in ADP spending, the food account, and some savings in the revenue budget have helped to offset the impact on the deficit The deficit (on IMF cash basis) through April is estimated at just under 4 ½ percent of GDP—but, spending traditionally accelerates during the last few months of the year

through April is estimated at just under 4 ½ percent of GDP—but, spending traditionally accelerates during the last few months of the year")

15

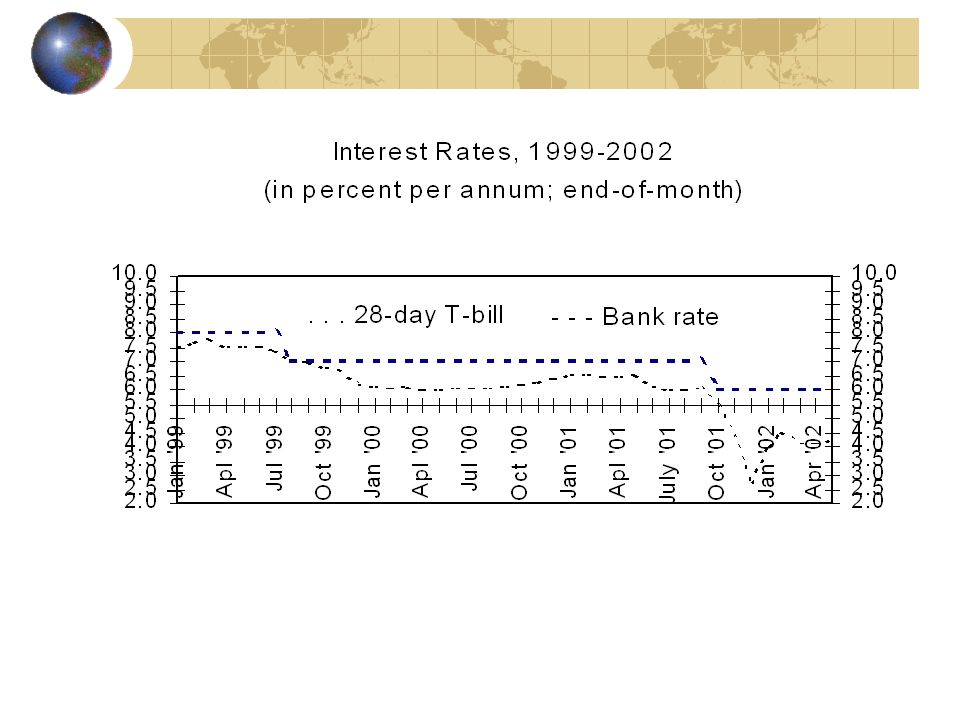

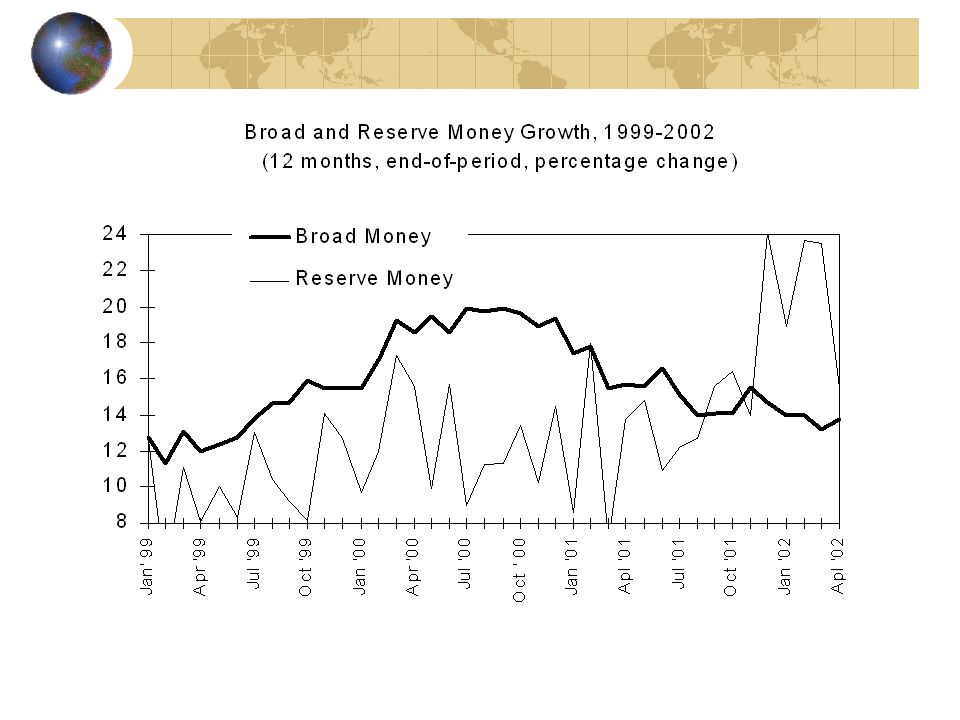

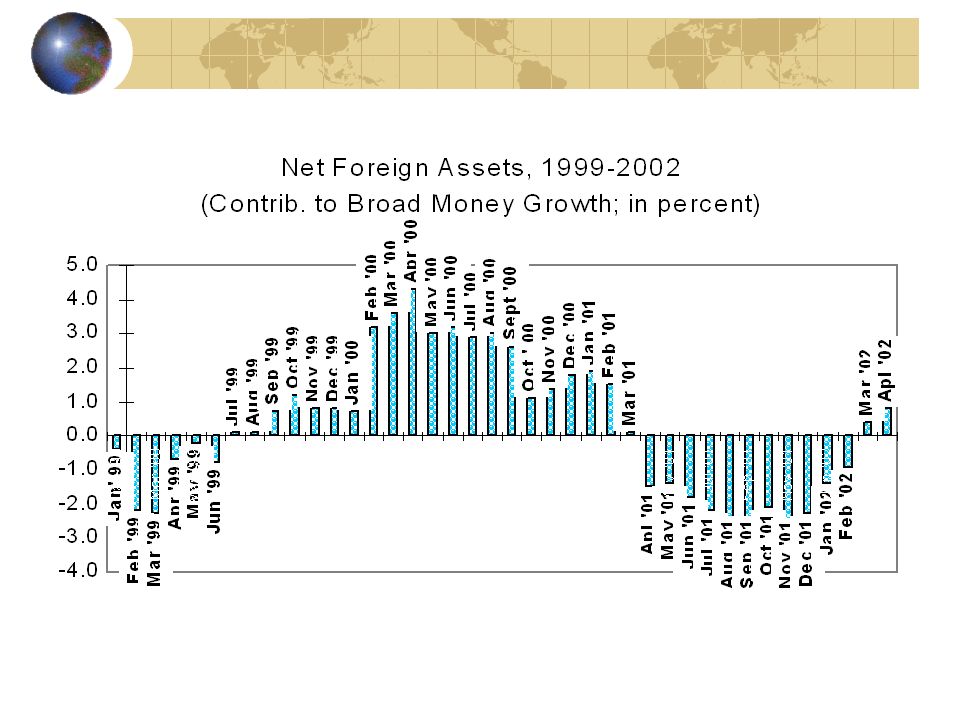

Monetary conditions remain loose… Reserve money increased by 14 percent in the 10 months through April This was mainly on account of increasing NFA of the Bangladesh Bank—the contribution of domestic credit expansion was marginal The call rate remains volatile, but has recently come down to under 4 percent— rates on 28 days T-bills are 4 ½ percent

17

…but money growth has come down somewhat Broad money growth has slowed from 15 percent in 2001 to 13 percent in the 12 months through April The money multiplier came down after the change in the CRR base in February, but returned to previous values in April Private sector credit growth was the main contributor to the increase in broad money

Similar presentations