Download presentation

Presentation is loading. Please wait.

1

Microeconomics Course E John Hey

2

Chapter 26 Because we are all enjoying risk so much, I have decided....... not to cover Chapter 26 (on the labour market) this year...... and so there will be no examination questions on Chapter 26 this year. (Not that there were anyhow!)

this year and so there will be no examination questions on Chapter 26 this year. (Not that there were anyhow!).")

3

Chapters 23, 24 (and 25) CHOICE UNDER RISK Chapter 23: The Budget Constraint. Chapter 24: The Expected Utility Model. (Chapter 25: Exchange in Insurance Markets.) (cf. Chapters 20, 21 and 22)

(cf. Chapters 20, 21 and 22).")

4

Contingent Goods (chapter 23) Notation: m 1 and m 2 : incomes in the two states. c 1 and c 2 : consumption in the two states. Good 1: income contingent on state 1. Good 2: income contingent on state 2. p 1 and p 2 : the prices of the two goods. For every unit of Good i that you have bought you receive an income of 1 if state i occurs. For every unit of Good i that you have sold you have to pay 1 if state i occurs.

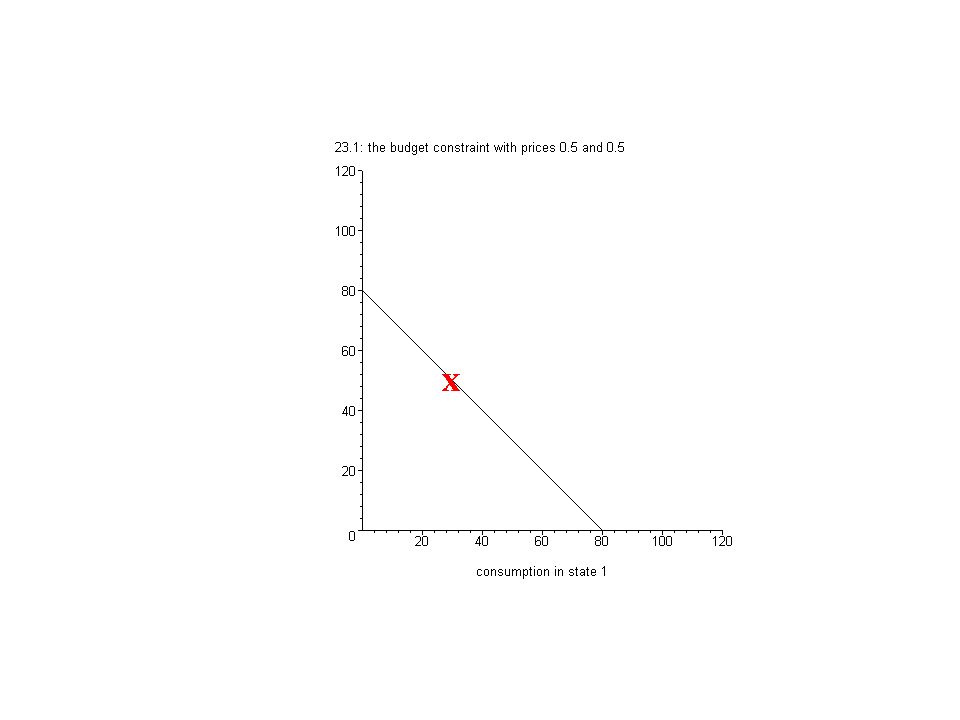

5

Budget Constraint (ch 23) The budget constraint in a perfect insurance market is...... p 1 c 1 + p 2 c 2 = p 1 m 1 + p 2 m 2......where p 1 = π 1 and p 2 = π 2 Hence… … π 1 c 1 + π 2 c 2 = π 1 m 1 + π 2 m 2 Expected consumption is equal to expected income. Has slope = -π 1 /π 2

6

An example Two states of the world: 1 an accident (theft, etc.): 2 no accident (theft, etc.) Let us suppose each has probability 0.5. Suppose m 1 = 30 and m 2 = 50 and p 1 = 0.5 and p 2 = 0.5

8

Expected Utility Model (ch 24) Now we need to put in preferences. Chapter 24 is difficult. You do not need to know the detail......only the principles. The utility of a lottery that yields c 1 with probability π 1 and yields c 2 with probability π 2 is given by…... U(c 1,c 2 ) = π 1 u(c 1 )+ π 2 u(c 2 ) This is the Expected Utility model.

= π 1 u(c 1 )+ π 2 u(c 2 ) This is the Expected Utility model..")

9

Remember this bet? I intend to sell this bet to the highest bidder. We toss a fair coin...... if it lands heads I give you 50 euros... If it lands tails I give you nothing. We will do an “English Auction” – the student who is willing to pay the most wins the auction, pays me the price at which the penultimate person dropped out of the auction, and I will play out the bet with him or her.

10

The Expected Utility Model U(c 1,c 2 ) = π 1 u(c 1 )+ π 2 u(c 2 ). … where (c 1,c 2 ) indicates a risky bundle which yields c 1 with probability π 1 and c 2 with probability π 2. Suppose your wealth is w and the most that you are willing to pay for the bet is m. Then you are indifferent between w for sure and a 50-50 bet between 50+w-m and w-m. Hence: u(w)=0.5 u(50+w-m) + 0.5 u(w-m) Note: Expected Profit = 0.5(50+w-m)+0.5(w-m)-w = 25-m The implications for u(.) depend upon m.

indicates a risky bundle which yields c 1 with probability π 1 and c 2 with probability π 2. Suppose your wealth is w and the most that you are willing to pay for the bet is m. Then you are indifferent between w for sure and a bet between 50+w-m and w-m. Hence: u(w)=0.5 u(50+w-m) u(w-m) Note: Expected Profit = 0.5(50+w-m)+0.5(w-m)-w = 25-m The implications for u(.) depend upon m..")

11

Suppose m = 19 (<25) (risk-averse) and w=30 u(30)=0.5 u(61) + 0.5 u(11)

(risk-averse) and w=30 u(30)=0.5 u(61) u(11)")

12

Suppose m = 25 (risk-neutral) and w=30 u(30)=0.5 u(55) + 0.5 u(5)

and w=30 u(30)=0.5 u(55) u(5)")

13

Suppose m = 29 (>25) (risk-loving) and w=30 u(30)=0.5 u(51) + 0.5 u(1)

(risk-loving) and w=30 u(30)=0.5 u(51) u(1)")

14

Hence the form of the utility function is important If u(.) is concave the individual is risk- averse. If u(.) is linear the individual is risk- neutral. If u(.) is convex the individual is risk- loving. Obviously the function may be concave in some parts and convex in others.

is linear the individual is risk- neutral. If u(.) is convex the individual is risk- loving. Obviously the function may be concave in some parts and convex in others..")

15

The Expected Utility Model U(c 1,c 2 ) = π 1 u(c 1 )+ π 2 u(c 2 ) An indifference curve is given by π 1 u(c 1 )+ π 2 u(c 2 ) = constant If the function u(.) is concave (linear,convex) the indifference curves in the space (c 1,c 2 ) are convex (linear, concave). The slope of every indifference curve on the certainty line = -π 1 /π 2

16

Risk neutral U(c 1,c 2 ) = π 1 u(c 1 )+ π 2 u(c 2 ) u(c)= c : the utility function is linear An indifference curve is given by π 1 c 1 + π 2 c 2 = constant Hence the indifference curves in the space (c 1,c 2 ) are linear. The slope of every indifference curve = -π 1 /π 2

17

Optimal choice π 1 = π 2 = 0.5

18

Risk-averse U(c 1,c 2 ) = π 1 u(c 1 )+ π 2 u(c 2 ) u(.) is concave An indifference curve is given by π 1 u(c 1 )+ π 2 u(c 2 ) = constant Hence the indifference curves in the space (c 1,c 2 ) are convex. The slope of every indifference curve on the certainty line = -π 1 /π 2

19

Optimal choice π 1 = π 2 = 0.5

20

Optimal choice π 1 = 0.6,π 2 =0.4

21

Risk-loving U(c 1,c 2 ) = π 1 u(c 1 )+ π 2 u(c 2 ) u(.) is convex An indifference curve is given by π 1 u(c 1 )+ π 2 u(c 2 ) = constant Hence the indifference curves in the space (c 1,c 2 ) are concave. The slope of every indifference curve on the certainty line = -π 1 /π 2

22

Optimal choice π 1 = 0.6,π 2 =0.4

23

The Certainty Equivalent Consider the lottery (c 1,c 2 ) with probabilities = π 1 and π 2 The certainty equivalent, EC, is defined by: u(EC) = π 1 u(c 1 )+ π 2 u(c 2 ) It is a certainty which gives the same utility as the lottery. The value of EC depends upon the function u(.). The individual considers the lottery and the certainty equivalent as equivalent.

. The individual considers the lottery and the certainty equivalent as equivalent..")

24

The concavity indicates the risk aversion With the Expected Utility Model: If the function u(.) is concave the individual is risk-averse. The more concave is the function the more risk- averse is the individual – hence the lower the certainty equivalent and the more convex are the indifference curves.

25

Appello 2 (traccia 1) In the next two questions you will be asked to consider an individual, taking decisions under conditions of risk, with Expected Utility preferences and utility function u(x) = x^0.5 (that is, the utility of x is the square root of x). Suppose the individual is faced with two lotteries P and Q as specified below. A lottery is denoted by (a,b;p,1-p) and means that the outcome is a with probability p and b with probability 1-p. The lotteries are: P = (25,16;0.25,0.75) Q = (1,36;0.25,0.75) Question 14: Does the individual prefer P or Q? P Q We cannot tell The individual is indifferent. Question 15: What is the individual's certainty equivalent for P? 27.25 18.25 22.5625 18.0625

and means that the outcome is a with probability p and b with probability 1-p. The lotteries are: P = (25,16;0.25,0.75) Q = (1,36;0.25,0.75) Question 14: Does the individual prefer P or Q. P Q We cannot tell The individual is indifferent. Question 15: What is the individual s certainty equivalent for P")

26

Appello 2 (traccia 2) In the next two questions you will be asked to consider an individual, taking decisions under conditions of risk, with Expected Utility preferences and utility function u(x) = x^0.5 (that is, the utility of x is the square root of x). Suppose the individual is faced with two lotteries P and Q as specified below. A lottery is denoted by (a,b;p,1-p) and means that the outcome is a with probability p and b with probability 1-p. The lotteries are: P = (4,36;0.5,0.5) Q = (1,36;0.75,0.25) Question 14: Does the individual prefer P or Q? P Q The individual is indifferent We cannot tell Question 15: What is the individual's certainty equivalent for P? 16 5.0625 20 9.75

and means that the outcome is a with probability p and b with probability 1-p. The lotteries are: P = (4,36;0.5,0.5) Q = (1,36;0.75,0.25) Question 14: Does the individual prefer P or Q. P Q The individual is indifferent We cannot tell Question 15: What is the individual s certainty equivalent for P")

27

Summary A risk-averse individual in a perfect insurance market always chooses to be completely insured.

28

Chapter 24 Goodbye!

Similar presentations

>")

L 1 ’: 2,500,000 (0.1), 500,000 (0.89), 0 (0.01) Which one would you choose? Another two.>")

: You.>")