Download presentation

Presentation is loading. Please wait.

1

Topic:Costs and Budgets (2) Learning Outcomes: By the end of the session, all students should be able to: Identify business costs items associated with budgets and most learners will be able to classify costs and some learners, explain why costs are important to businesses. Identify types of budgets and most learners will be able to explain the purpose of budgeting. Construct a business related budget. Some learners should be able to calculate variances without help. Calculate budget variances and some learners should be able to recommend options that businesses could use to control adverse variances.

2

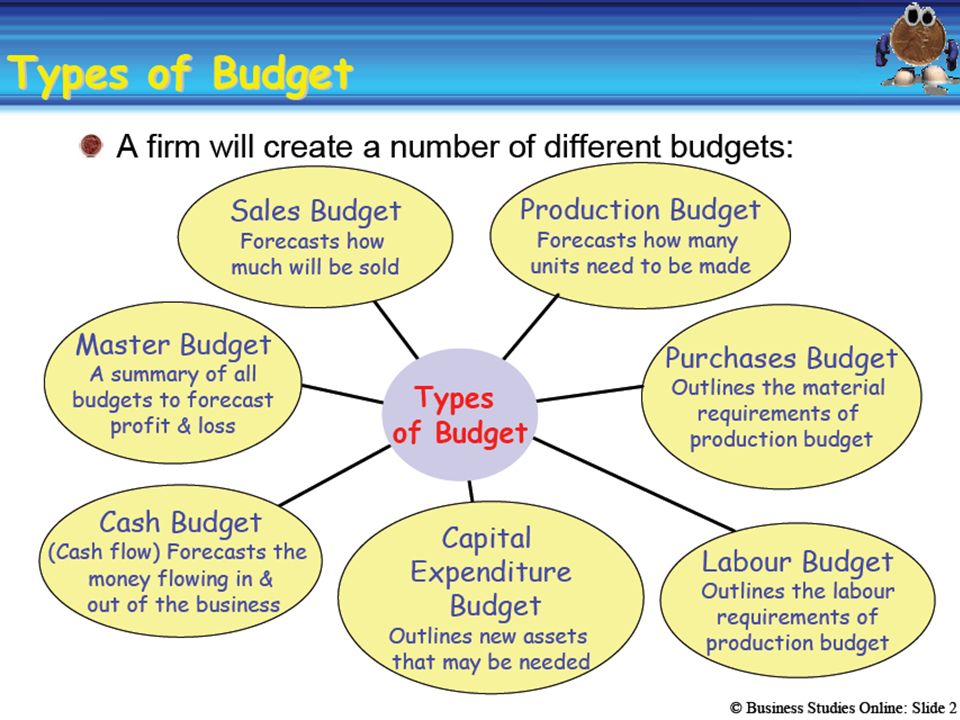

What is a budget? A plan which outlines expenses (costs) and income (revenues) over a stated period of time i.e. 1 - 5yrs. It also identifies the sum of money allocated towards a business expense. Businesses often use budgets to help achieve their overall goals and monitor and control their costs.

and income (revenues) over a stated period of time i.e yrs. It also identifies the sum of money allocated towards a business expense. Businesses often use budgets to help achieve their overall goals and monitor and control their costs..")

4

Importance of budgets? Establishes priorities and sets targets Turn objectives into practical reality Provide direction and co- ordination Help assign responsibilities Allocate resources Communicate targets Improve efficiency Motivate staff Forecast outcomes Monitor performance Control income and expenses Manage costs better Delegate without loss of control

5

Example of a Budget

6

Example of Budget Variances

7

Budget Variances The difference between actual and budgeted figures. Favourable - actual figure better than budgeted figure e.g. where costs are lower than expected. where revenue are higher than expected. Adverse – actual figure is worse than budgeted figure e.g. where costs are higher than expected. where revenue are lower than expected.

8

Why do variances occur? Internal matters: performance of individuals (ordering) wastage of materials slow working equipment faults. External issues: change in supply and demand shortage of materials and labour change in economic conditions. Incorrect budgets: Where budgets are based on incorrect information. Variances are differences between actual expenses and the planned budget. There are numerous reasons for variances in a budgets, which could include:

wastage of materials slow working equipment faults. External issues: change in supply and demand shortage of materials and labour change in economic conditions. Incorrect budgets: Where budgets are based on incorrect information. Variances are differences between actual expenses and the planned budget. There are numerous reasons for variances in a budgets, which could include:.")

9

Approaches to Budgeting Historical budgeting Use last year’s figures as the basis for the budget Seen as realistic as it is based on actual results Issues Change in circumstances Does not encourage efficiency Zero-based budgeting Budgeted costs & revenues are set to zero. Budget is based on new proposals for sales and costs. Issues Makes budgeting more complicated and time- consuming, but potentially more realistic

10

Benefits and Limitations of budgeting Advantages May motivate staff by providing them with targets Helps cash flow planning Helps coordinate activities Enables managers to see the consequences of their actions Performs a co-coordinating role Provides a control facility Creates a framework Acts as a plan Limitations Budgets are only estimates They may be restrictive if managers feel they have to follow them too closely Can de-motivate if targets are too hard to meet Targets can be set too low if this makes them easier to achieve Time consuming Inflexible Can meet with resistance Increased paperwork

Similar presentations

: Demonstrate understanding of how internal factors interact within a business that operates in a global context.>")

- LTD/PLC can.>")