Download presentation

Presentation is loading. Please wait.

1

Increasing Impact through Evolving Mission and Process

2

How Did Opportunity Fund Scale to 1,600 Deals? Opportunity Fund loan program’s evolution over the years Your questions

3

Devin McAlpine Director of Microlending 11 Years at Opportunity Fund, covering four lending models

4

Phase One: Pre 2008 Mission/Lending motivation: → Provide access to capital coupled with TA Model: → 2-3 underwriters trolling the internet → Craig’s List, Google Ads, Bank referrals → About 120 - 150 loans per year, loan size almost exclusively under $10K → TA assessment required before a loan could be approved

5

Phase One, continued Annual Loan Volume: → 150 Loans, $1,500,000 Pluses to the model: → Deep connection to client and mission Limitations/Challenges: → Not scalable, too long to process a loan, hard to find appropriate clients

6

Phase Two: 2008-2010 Mission/Lending Motivation: → Increase lending, number of clients Model: → Added marketing person to previous model → Responsible for improving internet ad words → Partnership development → Community presentations: Restaurants, Comm. Centers, Partnership Offices Usually populated by partnerships Low turn over ~ 2 apps for 25 people, one loan

7

Phase Two continued Annual Loan Volume: → 200 loans / $1,750,000 Pluses to the model: → Marginally easier for loan consultants, out reach to community, brand recognition Limitations/Challenges: → Very slow (especially to partners) and new to marketing, limited impact

and new to marketing, limited impact")

8

Phase Three 2010 Mission/Lending Motivation: Speed, number of clients Hiring Sales Reps → Initially charged with application collecting, this overwhelmed Underwriting → Clients moved from Rep to Underwriter to Closer → Sales Reps frustrated they couldn’t make quota (about 2 or 3 loans per month) → Loan size exceedingly small ~ avg under $5K for reps

→ Loan size exceedingly small ~ avg under $5K for reps")

9

Phase Three continued Annual Loan Volume: → 300 loans / $3,000,000 Pluses to the model: → Number of clients greatly increased Limitations/Challenges: → Overwhelming paperwork without proper training of Sales Reps → Clients speak with too many people and drop out

10

Phase Four 2011 Mission/Lending Motivation: Move toward credit based TA / Increase loan size Hiring Sales Reps: 8 loans per consultant →Sales Reps report to Underwriting Manager →Focus on empowerment ~ title: Loan Consultant →Consultants do all: sell, underwrite, close and collect →Incorporate TA into service not separate process →No inside sales, all loans referred to Consultants →Marketing: Easy to Understand Eng & Spanish flyer

11

Phase Four continued Grew from 2 to 14 Loan consultants Defined territory ~ a base to focus and integrate They prepare 7 to 14 loans per month →Walking their neighborhoods →Meeting with Bankers (Wells Fargo, Chase excellent buy in) →Referral base from Mobile Food Manuf. Cornered the mkt. →Commercial car dealerships extremely successful →Periodic visits w Partners ~ local CDFI’s focusing on TA and access to capital.

12

Phase Four continued Incentivized compensation →Started hiring staff with sales background →~ 50% of compensation comes from salary →50%+ comes in the form of bonus →Bonus based on number of loans, dollar volume of loans and portfolio performance →Quality loan performance: 30 to 150 days late at 6% or less of Loan Consultant’s portfolio

13

Phase Four continued Annual Loan Volume: → 1,600 loans / $30,000,000 Pluses to the model: → Clients see OF as a long term solution, impact is strong Limitations/Challenges: → Scalability is again in question ~ LC in every area? → Reaching all possible clients is weak → Limited web presence (changing that now)

.")

14

Merger with Confianza Mission/Motivation: →Reach SoCal, Keep Confianza successes Practices that were improved in Nor Cal →Weekly collections call with Collector and LC →Understanding the mobile food unit industry →Value of personal references for borrowers →Speed and simplify our underwriting

15

Confianza Merger continued Practices that were improved in So Cal → Develop Banking Channel → Reach beyond Spanish speaking clients → Increase loan size (Confianza had been $8K) → Develop streamlined Sales to Collections model → Improve marketing outreach and use flyer

→ Develop streamlined Sales to Collections model → Improve marketing outreach and use flyer")

16

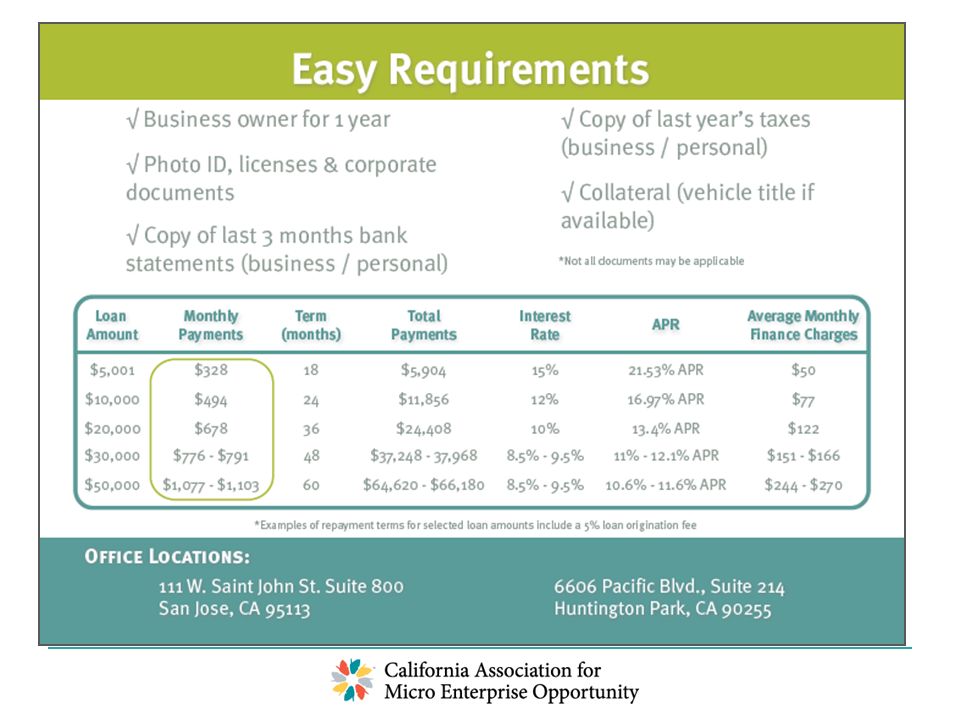

OF Offerings – All Term Loans Express Loan → $10K and under → Underwriting based on credit history (not FICO) → Proof in business Standard Business Loan → $10K - $100K Easy Pay Loan (any loan can be EasyPay) → Set up merchant services with OF → Loan payment: % of credit card sales → Much lower cost of funds & longer term than MCA

→ Proof in business Standard Business Loan → $10K - $100K Easy Pay Loan (any loan can be EasyPay) → Set up merchant services with OF → Loan payment: % of credit card sales → Much lower cost of funds & longer term than MCA")

17

Partnership with Lending Club Limited trial period in 2016 Credit box very finite and passed to Lending Club to match their clients requests In 2016 only applicants with a business in California. Final decision to award loan or not by OF Expected to be loans $50K to $100K.

20

Ongoing Challenges Consultants primarily speak Spanish and aren’t comfortable going to English speaking stores Competition for clients ~ Dealers/Manufacturers should spread the wealth throughout territories 8 new loans per month seems max with our current technology/marketing Developing employees after 2 years ~ finding something new and challenging Improving marketing for better loan yield

21

Questions?

22

Thanks!!

Similar presentations