Download presentation

Presentation is loading. Please wait.

1

Multi Disciplinary Questions ACCOUNTANCY CLASS 12

2

QUESTION NO-1 A and B are partners sharing profits in the ratio of 3:2 with capitals of Rs. 3,20,000 and Rs. 2,60,000.On 1 st April,2013,they admit C into the partnership. A surrenders 1/5 th of his share and B surrenders 2/5 th of his share in favor of C.C brings in Rs. 1,40,000 for goodwill and the proportionate amount of Capital in cash. Partner’s are entitled to interest on capital @5% p.a. Profits for the year ending 31 st March,2014 before allowing interest on capitals amounted to Rs. 3,00,000. Pass journal entries for the above mentioned transactions.

3

DateParticularsL.F.Dr.(R.s)Cr.(Rs.) 2013 Apr-01Bank A/c Dr. 4,20,000 To C's Capital A/c 2,80,000 To premium for goodwill A/c 1,40,000 (the amount of capital and goodwill/premium brought in cash) Apr-01Premium for Goodwill A/c Dr. 1,40,000 To A's Capital A/c 60,000 To B's Capital A/c 80,000 (Goodwill credited to old partners in sacrificing ratio i.e., 3 : 4)

Apr-01Premium for Goodwill A/c Dr. 1,40,000 To A s Capital A/c 60,000 To B s Capital A/c 80,000 (Goodwill credited to old partners in sacrificing ratio i.e., 3 : 4).")

4

2014 Mar-31Profit & loss A/c Dr. 3,00,000 To Profit and Loss appropriation A/c 3,00,000 (Transfer of profit & loss to appropriation A/c) Mar-31Interest on Capital A/c Dr. 50,000 To A's Capital A/c 19,000 To B's Capital A/c 17,000 To C's Capital A/c 14,000 (Interest on partner's Capitals) Mar-31Profit and Loss Appropriation A/c Dr. 50,000 To interest on Capital A/c 50,000 (Transfer of interest on capital to appropriation A/c) Mar-31Profit and Loss Appropriation A/c Dr. 2,50,000 To A's Capital A/c 1,20,000 To B's Capital A/c 60,000 To C's Capital A/c 70,000 Transfer of balance of appropriation A/c to capital accounts in the profit sharing ratio i.e., 12 : 6: 7)

Mar-31Interest on Capital A/c Dr. 50,000 To A s Capital A/c 19,000 To B s Capital A/c 17,000 To C s Capital A/c 14,000 (Interest on partner s Capitals) Mar-31Profit and Loss Appropriation A/c Dr. 50,000 To interest on Capital A/c 50,000 (Transfer of interest on capital to appropriation A/c) Mar-31Profit and Loss Appropriation A/c Dr. 2,50,000 To A s Capital A/c 1,20,000 To B s Capital A/c 60,000 To C s Capital A/c 70,000 Transfer of balance of appropriation A/c to capital accounts in the profit sharing ratio i.e., 12 : 6: 7).")

5

Working notes 1. share surrendered by A: 1/5 th of 3/5 =3/25 Share surrendered by B : 2/5 th of 2/5 = 4/25 Sacrificing ratio 3/25 : 4/25 = 3 : 4 A’s new share = 3/5 – 3/25 = 15-3/25 =12/25 B’s new share = 2/5 – 4/25 = 10-4/ 25 = 6/25 C’s share = 3/25 +4/25 = 7/25 hence., new ratios of A, B and C = 12 : 6 : 7

6

2. adjusted capital of A = Rs. 3,20,000 + share of goodwill Rs. 60,000 = Rs. 3,80,000 adjusted capital of B = Rs. 2,60,000 + share of goodwill Rs. 80,000 = Rs. 3,40,000 Total adjusted capital of A and B for 18/25 th share = Rs. 3,80,000 + Rs. 3,40,000 = Rs. 7,20,000 total capital of new firm : Rs. 7,20,000 × 25/18 = Rs. 10,00,000 Proportionate capital of C = Rs. 10,00,000 × 7/25 = Rs. 2,80,000 3. interest on capitals : A 5% on Rs. 3,80,000 = Rs. 19,000 B 5% on Rs. 3,40,000 = Rs. 17,000 C 5% on Rs. 2,80,000 = Rs. 14,000 Rs. 50,000 4. net profit after interest on capital = Rs. 3,00,000 –Rs. 50,000 = Rs. 2,50,000

7

QUESTION NO-2 The partners of a firm distributed the profits for the year ended 31 st March,2013,Rs. 7,50,000 equally without providing for the following adjustments: (1) A and B were entitled to a salary of Rs. 10,000 each per month. (2) B was entitled to a commission of Rs. 60,000. (3) Profits were to be shared in the ratio of 3:2:1. Partners decided to pass an adjusting entry on 1 ST April,2013 rectifying the same. On the same date, they admitted D as a new partner for 1/7 th share in the profits. The new profit sharing ratio will be 2:2:2:1respectively. D brought Rs. 3,00,000 for his capital and Rs. 45,000 for his 1/7 th share of goodwill. Showing your workings clearly, pass the necessary journal entries in the books of the firm for the above mentioned transactions.

A and B were entitled to a salary of Rs. 10,000 each per month. (2) B was entitled to a commission of Rs. 60,000. (3) Profits were to be shared in the ratio of 3:2:1. Partners decided to pass an adjusting entry on 1 ST April,2013 rectifying the same. On the same date, they admitted D as a new partner for 1/7 th share in the profits. The new profit sharing ratio will be 2:2:2:1respectively. D brought Rs. 3,00,000 for his capital and Rs. 45,000 for his 1/7 th share of goodwill. Showing your workings clearly, pass the necessary journal entries in the books of the firm for the above mentioned transactions..")

8

DATEPARTICULARL.F.Dr.(RS)Cr.(RS) 2013 APRIL 1 C’s Capital A/c Dr. To A’s Capital A/c To B’s Capital A/c (Adjustment for wrong appropriation of profit) 1,75,000 95,000 80,000 APRIL 1Bank A/c Dr. To D’s Capital A/c To Premium for Goodwill A/c (The amount of capital and goodwill/premium brought in cash) 3,45,000 3,00,000 45,000 April 1Premium for Goodwill A/c Dr. C’s Capital A/c To A’s Capital A/c To B’s Capital A/c (Premium for goodwill brought in D credited to A and B along with 5/45 of the goodwill to be contributed by C due to gain in his profit sharing ratio) 45,000 37,500 67,500 15,000

1,75,000 95,000 80,000 APRIL 1Bank A/c Dr. To D’s Capital A/c To Premium for Goodwill A/c (The amount of capital and goodwill/premium brought in cash) 3,45,000 3,00,000 45,000 April 1Premium for Goodwill A/c Dr. C’s Capital A/c To A’s Capital A/c To B’s Capital A/c (Premium for goodwill brought in D credited to A and B along with 5/45 of the goodwill to be contributed by C due to gain in his profit sharing ratio) 45,000 37,500 67,500 15,000.")

9

PARTICULAR A (RS) B (RS) C (RS) TOTAL (RS) Salary (Cr.) Commission (Cr.) Remaining profit i.e., 7,50,000-2,40,000-60,000=4,50,000 will be divided in 3 : 2 : 1 (Cr.) Less : Profit already distributed equally 1,20,000 2,25,000 3,45,000 2,50,000 (Cr.) 95,000 1,20,000 60,000 1,50,000 3,30,000 2,50,000 (Cr.) 80,000 75,000 2,50,000 (Dr.) 1,75,000 2,40,000 60,000 4,50,000 7,50,000 -- TABLE SHOWING ADJUSTMENTS Working Notes :

B (RS) C (RS) TOTAL (RS) Salary (Cr.) Commission (Cr.) Remaining profit i.e., 7,50,000-2,40,000-60,000=4,50,000 will be divided in 3 : 2 : 1 (Cr.) Less : Profit already distributed equally 1,20,000 2,25,000 3,45,000 2,50,000 (Cr.) 95,000 1,20,000 60,000 1,50,000 3,30,000 2,50,000 (Cr.) 80,000 75,000 2,50,000 (Dr.) 1,75,000 2,40,000 60,000 4,50,000 7,50, TABLE SHOWING ADJUSTMENTS Working Notes :")

12

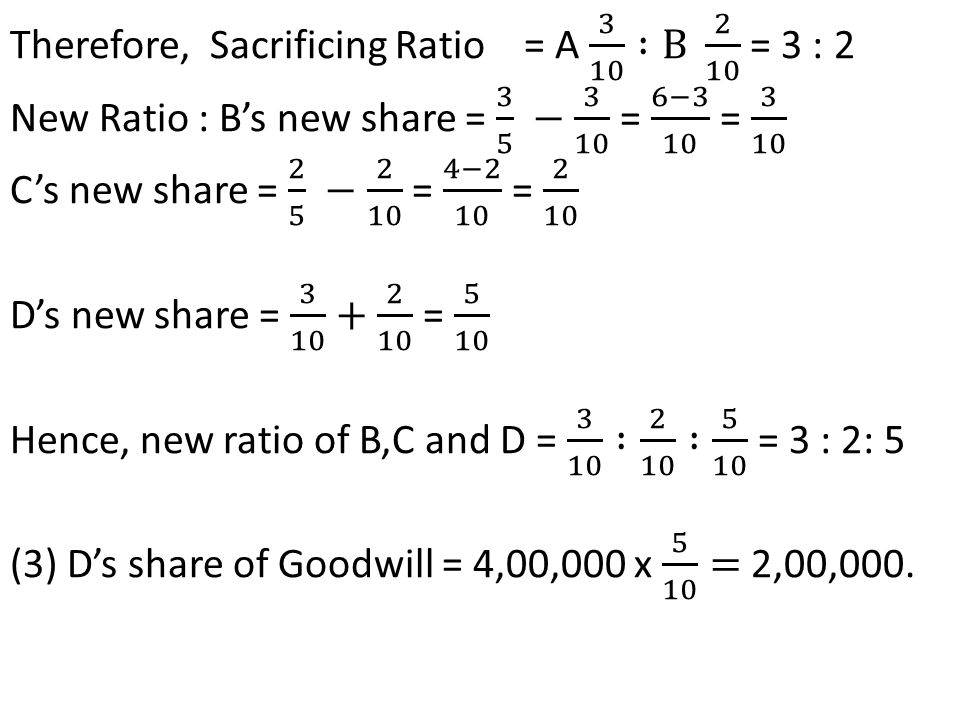

QUESTION NO-3 A,B and C were partners in a firm sharing profits in the ratio of 1:2:2. On 1 st July,2014 A retired and the new profit sharing ratio of B and C was 3:2. Goodwill of the firm was valued at Rs. 4,00,000. D is admitted as a partner. B and C surrenders ½ of their respective share in favor of D. D is to bring his share of premium for the goodwill in cash. Pass necessary entries for the record of goodwill in the above case. Also calculate the sacrificing ratios and new ratios.

13

JOURNAL DATEPARTICULARL.F. Dr. (Rs) Cr. (Rs) 2014 July 1 80,000 July 1Bank A/c Dr. To Premium for Goodwill A/c (Premium for Goodwill brought in cash by D) 2,00,000 July 1Premium for Goodwill A/c Dr. To B’s Capital A/c To C’s Capital A/c (Premium brought in by D credited to B and C in the sacrificing ratio of 3 : 2) 2,00,000 1,20,000 80,000

2,00,000 July 1Premium for Goodwill A/c Dr. To B’s Capital A/c To C’s Capital A/c (Premium brought in by D credited to B and C in the sacrificing ratio of 3 : 2) 2,00,000 1,20,000 80,000.")

14

Working Notes :

16

Q.4. A,B and C were in partnership sharing profits and losses in the proportions of 3 : 2 : 1. On 1 st April,2011,B retires from the firm. On that date, their Balance Sheet was as follows : Liabilities (Rs) Assets (Rs) Trade Creditors Expenses owing Reserve Fund Workmen’s Compensation Reserve Capitals : A : 1,95,000 B : 1,57,000 C : 81,000 69,000 45,000 1,05,000 48,000 4,33,000 7,00,000 Cash in hand Debtors 1,60,000 Less : Provision 10,000 Stock Factory Premises Investments Loose Tools 85,000 1,50,000 1,20,000 2,25,000 80,000 40,000 7,00,000

Assets (Rs) Trade Creditors Expenses owing Reserve Fund Workmen’s Compensation Reserve Capitals : A : 1,95,000 B : 1,57,000 C : 81,000 69,000 45,000 1,05,000 48,000 4,33,000 7,00,000 Cash in hand Debtors 1,60,000 Less : Provision 10,000 Stock Factory Premises Investments Loose Tools 85,000 1,50,000 1,20,000 2,25,000 80,000 40,000 7,00,000.")

17

The terms were : (1)Goodwill of the firm to be valued at 2 times of Average Super Profits of last three years. Taking into consideration the risk of the business, normal profits of the firm are estimated at 5,00,000 every year. But actual profits three years ending 31 st march were as 2009 : 6,00,000, 2010 : 5,50,000, 2011 : 5,75,000. (2)Expenses owing to be brought down to 37,500. (3)Investments are valued at 72,000.A took over investments at this value. (4)Factory premises is to be revalued at 2,43,000;and Loose tools at 36,000. (5)Provision for doubtful Debt to be increased by 19,500. (6)Claim on account of workmen’s compensation is 18,000. (7)B be paid 50,000 in cash and balance due to him treated as a loan carrying interest @ 6% per annum.

Expenses owing to be brought down to 37,500. (3)Investments are valued at 72,000.A took over investments at this value. (4)Factory premises is to be revalued at 2,43,000;and Loose tools at 36,000. (5)Provision for doubtful Debt to be increased by 19,500. (6)Claim on account of workmen’s compensation is 18,000. (7)B be paid 50,000 in cash and balance due to him treated as a loan carrying 6% per annum..")

18

As per partnership deed, partners are allowed 6% p.a. interest on their capitals. Profits for the year ending 31 st march 2012 before allowing interest on the loan and capitals amounted to 22,000. Show Journal entry for goodwill adjustments, prepare Revaluation Account and Capital Accounts as on 1 st April 2011 and the distribution of profit for the year ended 31 st March,2012.

20

JOURNAL ENTRY FOR GOODWILL DATEPARTICULARL.F. Dr. (Rs) Cr. (Rs.) 2011 April 1A’s Capital A/c Dr. C’s Capital A/c Dr. To B’s Capital A/c (B’s share of goodwill adjusted to the accounts of continuing partners in their gaining ratio 3 : 1) 37,500 12,500 50,000

Cr. (Rs.) 2011 April 1A’s Capital A/c Dr. C’s Capital A/c Dr. To B’s Capital A/c (B’s share of goodwill adjusted to the accounts of continuing partners in their gaining ratio 3 : 1) 37,500 12,500 50,000.")

21

REVALUATION ACCOUNT PARTICULAR (Rs.) PARTICULAR (Rs.) To Investments To Loose Tools To Provision for doubtful debts 8,000 4,000 19,500 31,500 By Expenses owing A/c By Factory Premises By Loss transferred to : A 3,000 B 2,000 C 1,000 7,500 18,000 6,000 31,500

PARTICULAR (Rs.) To Investments To Loose Tools To Provision for doubtful debts 8,000 4,000 19,500 31,500 By Expenses owing A/c By Factory Premises By Loss transferred to : A 3,000 B 2,000 C 1,000 7,500 18,000 6,000 31,500")

22

CAPITAL ACCOUNTS PARTICULAR A (Rs.) B (Rs.) C (Rs.) PARTICULAR A (Rs.) B (Rs.) C (Rs.) 1 st April 2011 To Revaluation A/c To B’s capital A/c To Investments A/c To cash A/c To B’s loan A/c To Balance c/d 3,000 37,500 72,000 0 1,50,000 2,62,000 2,000 0 50,000 2,00,000 0 2,52,000 1,000 12,500 0 90,000 1,03,500 1 st April 2011 By Balance b/d By Reserve Fund A/c By Workmen’s Compensation Reserve A/c By A’s Capital A/c By C’s Capital A/c 1,95,000 52,500 15,000 0 2,62,000 1,57,000 35,000 10,000 37,500 12,500 2,52,000 81,000 17,500 5,000 0 1,03,500

B (Rs.) C (Rs.) PARTICULAR A (Rs.) B (Rs.) C (Rs.) 1 st April 2011 To Revaluation A/c To B’s capital A/c To Investments A/c To cash A/c To B’s loan A/c To Balance c/d 3,000 37,500 72, ,50,000 2,62,000 2, ,000 2,00, ,52,000 1,000 12, ,000 1,03,500 1 st April 2011 By Balance b/d By Reserve Fund A/c By Workmen’s Compensation Reserve A/c By A’s Capital A/c By C’s Capital A/c 1,95,000 52,500 15, ,62,000 1,57,000 35,000 10,000 37,500 12,500 2,52,000 81,000 17,500 5, ,03,500")

23

PROFIT & LOSS ACCOUNT for the year ended 31 st march, 2012 PARTICULAR (Rs.) PARTICULAR (Rs.) To Interest on B’s Loan ( 6% on 2,00,000) To Profit transferred to P & L Appropriation A/c 12,000 10,000 22,000 By Profit (before interest) 22,000 Since partnership deed is silent in treating on capital as a charge or appropriation it will be treated as appropriation of profits.

PARTICULAR (Rs.) To Interest on B’s Loan ( 6% on 2,00,000) To Profit transferred to P & L Appropriation A/c 12,000 10,000 22,000 By Profit (before interest) 22,000 Since partnership deed is silent in treating on capital as a charge or appropriation it will be treated as appropriation of profits.")

24

PROFIT AND LOSS APPROPRIATION A/C PARTICULAR(Rs.)PARTICULAR(Rs.) 6,250 3,750 10,000 By Profit & Loss A/c10,000

PARTICULAR(Rs.) 6,250 3,750 10,000 By Profit & Loss A/c10,000")

25

Interest on A’s Capital 6% on 1,50,000 9,000 Interest on A’s Capital 6% on 90,000 5,400 14,400 The available profit is 10,000 whereas the interest due on capitals is 14,400. Since the profit is less than interest, the available profit will be distributed in the ratio of interest, i.e., 9,000 : 5,400 or 5 : 3.

Similar presentations

Advantageous location.>")