Download presentation

Presentation is loading. Please wait.

1

Process Costing

2

PROCESS COSTING Weighted Average FIFO Cost flow

3

Finished Goods AssemblingAssemblingCuttingCutting Sequential Processing Parallel Product Flow Selective Product Flow

4

Five Steps in Process Costing Step 1: Summarize the flow of physical units of output. Step 1: Summarize the flow of physical units of output. Step 2: Compute output in terms of equivalent units. Step 2: Compute output in terms of equivalent units. Step 3: Compute equivalent unit costs. Step 4: Summarize total costs to account for. Step 5: Assign total costs to units completed and to units in ending work in process inventory. Step 5: Assign total costs to units completed and to units in ending work in process inventory.

5

Weighted average method

6

Step 1: Summarize the flow of physical units of output. CUTTINGASSEMBLING Work in process, beginning 100180 Started during current period in Cutting Dept. 600 Completed and transferred out during current period to Assembling Dept. 500 Started during current period in Assembling Dept. 500 Completed and transferred out during current period to Finish Goods. 580 Work in process, ending 200100

7

Concept: 100 units completed = 100 equivalent units 200 units, 50% completed = 100 equivalent units = = Step 2: Compute output in terms of equivalent units.

8

Step 2: Compute output in terms of equivalent units (Cont’d) CUTIING DEPT.DMDLFOH Work in process, beginning80%40%60% Work in process, ending60%20%40% ASSEMBLING DEPT.DMDLFOH Work in process, beginning40%20% Work in process, ending100%70%

CUTIING DEPT.DMDLFOH Work in process, beginning80%40%60% Work in process, ending60%20%40% ASSEMBLING DEPT.DMDLFOH Work in process, beginning40%20% Work in process, ending100%70%")

9

Step 2: Compute output in terms of equivalent units (Cont’d) Equivalent Units:DMDLFOH Completed and transferred out 500 Work in process, ending 1204080 Total Equivalent Units 620540580 CUTTING DEPT.

Equivalent Units:DMDLFOH Completed and transferred out 500 Work in process, ending Total Equivalent Units CUTTING DEPT.")

10

Step 3: Compute equivalent unit costs Cost ($)CUTTINGASSEMBLING WIP, Begining: Cost From Previous Dept: 8,320 Direct Materials 1,892830 Direct Labor 400475 Factory Overhead 796518 Cost Aded During Current Periods: Direct Materials 13,6087,296 Direct Labor 5,0009,210 Factory Overhead 7,90411,052

CUTTINGASSEMBLING WIP, Begining: Cost From Previous Dept: 8,320 Direct Materials 1, Direct Labor Factory Overhead Cost Aded During Current Periods: Direct Materials 13,6087,296 Direct Labor 5,0009,210 Factory Overhead 7,90411,052")

11

Step 3: Compute equivalent unit costs (Cont’d) CUTTING DEPT. Equivalent Units:DMDLFOH Cost From Beginning WIP Invent. 1,892400796 Cost Aded During Current Periods 13,6085,0007,904 Total Cost To Accounted For 15,5005,4008,700 Devided: Equivalent Units 620540580 Cost per Equivalent Units ($) 251015

")

12

Step 4 & 5: Summarize and Assign Total Costs CUTTING DEPT. Step 4: Total costs to account for: $29,600 Step 5: Assign total costs: Completed and transferred out: 500 × $50$25,000 Work in process, ending (200 units): Direct materials120 × $25 3,000 Direct labor 40 × $10 400 FOH 80 × $15 1,200 Total $29,600 Completed and transferred out: 500 × $50$25,000 Work in process, ending (200 units): Direct materials120 × $25 3,000 Direct labor 40 × $10 400 FOH 80 × $15 1,200 Total $29,600

: Direct materials120 × $25 3,000 Direct labor 40 × $ FOH 80 × $15 1,200 Total $29,600 Completed and transferred out: 500 × $50$25,000 Work in process, ending (200 units): Direct materials120 × $25 3,000 Direct labor 40 × $ FOH 80 × $15 1,200 Total $29,600.")

14

Step 1: Summarize the flow of physical units of output. CUTTINGASSEMBLING Work in process, beginning 100180 Started during current period in Cutting Dept. 600 Completed and transferred out during current period to Assembling Dept. 500 Started during current period in Assembling Dept. 500 Completed and transferred out during current period to Finish Goods. 580 Work in process, ending 200100

15

Concept: 100 units completed = 100 equivalent units 200 units, 50% completed = 100 equivalent units = = Step 2: Compute output in terms of equivalent units.

16

Step 2: Compute output in terms of equivalent units (Cont’d) CUTIING DEPT.DMDLFOH Work in process, beginning80%40%60% Work in process, ending60%20%40% ASSEMBLING DEPT.DMDLFOH Work in process, beginning40%20% Work in process, ending100%70%

CUTIING DEPT.DMDLFOH Work in process, beginning80%40%60% Work in process, ending60%20%40% ASSEMBLING DEPT.DMDLFOH Work in process, beginning40%20% Work in process, ending100%70%")

17

Step 2: Compute output in terms of equivalent units (Cont’d) Equivalent Units:Cost from Prev. Dept. DMDLFOH Completed and transferred out 580 Work in process, ending 100 70 Total Equivalent Units 680 650580 ASSEMBLING DEPT.

18

Step 3: Compute equivalent unit costs Cost ($)CUTTINGASSEMBLING WIP, Begining: Cost From Previous Dept: 8,320 Direct Materials 1,892830 Direct Labor 400475 Factory Overhead 796518 Cost Aded During Current Periods: Direct Materials 13,6087,296 Direct Labor 5,0009,210 Factory Overhead 7,90411,052

CUTTINGASSEMBLING WIP, Begining: Cost From Previous Dept: 8,320 Direct Materials 1, Direct Labor Factory Overhead Cost Aded During Current Periods: Direct Materials 13,6087,296 Direct Labor 5,0009,210 Factory Overhead 7,90411,052")

19

Step 3: Compute equivalent unit costs (Cont’d) ASSEMBLING DEPT. Equivalent Units:Cost from Prev. Dept. DMDLFOH Cost From Beginning WIP Invent. 8,320830475518 Cost Aded During Current Periods 25,0007,2969,21011,052 Total Cost To Accounted For 33,3208,1269,68511,570 Devided: Equivalent Units 680 650580 Cost per Equivalent Units ($) 49.0011.9514.9017.80

")

20

Step 4 & 5: Summarize and Assign Total Costs CUTTING DEPT. Step 4: Total costs to account for: $62,701 Step 5: Assign total costs: Completed and transferred out: 580 × $93.65$54,317 Work in process, ending (100 units): Cost from prev Dept.100 × $49.00 4,900 Direct materials100 × $11.95 1,195 Direct labor 70 × $14.90 1,043 FOH 70 × $17.80 1,246 Total $62,701 Completed and transferred out: 580 × $93.65$54,317 Work in process, ending (100 units): Cost from prev Dept.100 × $49.00 4,900 Direct materials100 × $11.95 1,195 Direct labor 70 × $14.90 1,043 FOH 70 × $17.80 1,246 Total $62,701

: Cost from prev Dept.100 × $ ,900 Direct materials100 × $ ,195 Direct labor 70 × $ ,043 FOH 70 × $ ,246 Total $62,701 Completed and transferred out: 580 × $93.65$54,317 Work in process, ending (100 units): Cost from prev Dept.100 × $ ,900 Direct materials100 × $ ,195 Direct labor 70 × $ ,043 FOH 70 × $ ,246 Total $62,701.")

21

FIFO method

22

Notes Dalam asumsi aliran biaya FIFO, biaya unit pertama yang ditransfer keluar dari satu departemen dianggap berasal dari persediaan awal. Jika unit dari persediaan awal belum sepenuhnya selesai, unit tersebut harus diselesaikan terlebih dahulu dengan biaya periode berjalan sebelum dapat ditransfer keluar dari departemen tersebut. Total unit ekuivalen dari periode berjalan merupakan jumlah dari jumlah unit ekuivalen untuk biaya ditambahkan di periode berjalan guna menyelesaikan unit di persediaan awal ditambah unit yang dimulai dan diselesaikan selama periode berjalan serta unit ekuivalen di persediaan akhir. Untuk unit ekuivalen dari biaya periode berjalan yang diperlukan guna menyelesaikan unit di persediaan awal, tingkat penyelesaian di persediaan awal harus diketahui.

23

Step 1: Summarize the flow of physical units of output. CUTTINGASSEMBLING Work in process, beginning 100180 Started during current period in Cutting Dept. 600 Completed and transferred out during current period to Assembling Dept. 500 Started during current period in Assembling Dept. 500 Completed and transferred out during current period to Finish Goods. 580 Work in process, ending 200100

24

Step 2: Compute output in terms of equivalent units (Cont’d) CUTIING DEPT.DMDLFOH Work in process, beginning80%40%60% Work in process, ending60%20%40% ASSEMBLING DEPT.DMDLFOH Work in process, beginning40%20% Work in process, ending100%70%

CUTIING DEPT.DMDLFOH Work in process, beginning80%40%60% Work in process, ending60%20%40% ASSEMBLING DEPT.DMDLFOH Work in process, beginning40%20% Work in process, ending100%70%")

25

Step 2: Compute output in terms of equivalent units (Cont’d) Equivalent Units:DMDLFOH Work in process, begining 206040 Started & Completed during current period’s 400 Work in process, ending 1204080 Total Equivalent Units 540500520 CUTTING DEPT.

Equivalent Units:DMDLFOH Work in process, begining Started & Completed during current period’s 400 Work in process, ending Total Equivalent Units CUTTING DEPT.")

26

Alternative for Step 2: Compute output in terms of equivalent units (Cont’d) Equivalent Units:DMDLFOH Completed & Transfered Out 500 Work in process, ending 1204080 Ekuivalent Units (total) 620540580 (-) Work in process, begining 804060 Total Equivalent Units 540500520 CUTTING DEPT.

Equivalent Units:DMDLFOH Completed & Transfered Out 500 Work in process, ending Ekuivalent Units (total) (-) Work in process, begining Total Equivalent Units CUTTING DEPT.")

27

Step 3: Compute equivalent unit costs Cost ($)CUTTINGASSEMBLING WIP, Begining: Cost From Previous Dept: 8,320 Direct Materials 1,892830 Direct Labor 400475 Factory Overhead 796518 Cost Aded During Current Periods: Direct Materials 13,6087,296 Direct Labor 5,0009,210 Factory Overhead 7,90411,052

CUTTINGASSEMBLING WIP, Begining: Cost From Previous Dept: 8,320 Direct Materials 1, Direct Labor Factory Overhead Cost Aded During Current Periods: Direct Materials 13,6087,296 Direct Labor 5,0009,210 Factory Overhead 7,90411,052")

28

Step 3: Compute equivalent unit costs (Cont’d) CUTTING DEPT. Equivalent Units:DMDLFOH Cost Aded During Current Periods 13,6085,0007,904 Devided: Equivalent Units 540500520 Cost per Equivalent Units ($) 25.2010.0015.20

")

29

Step 4 & 5: Summarize and Assign Total Costs CUTTING DEPT. Step 4: Total costs to account for: $29,600 Step 5: Assign total costs: Work In Process, Beginning (100 units): From previous period’s $3,088 Aded during current period’s Direct materials20 × $25.20 504 Direct labor60 × $10.00 600 FOH40 × $15.20 608 Started & Completed durring current period’s: 400 × $50.40$20,160 Work in process, ending (200 units): Direct materials120 × $25.20 3,024 Direct labor 40 × $10.00 400 FOH 80 × $15.20 1,216 Total $29,600 Work In Process, Beginning (100 units): From previous period’s $3,088 Aded during current period’s Direct materials20 × $25.20 504 Direct labor60 × $10.00 600 FOH40 × $15.20 608 Started & Completed durring current period’s: 400 × $50.40$20,160 Work in process, ending (200 units): Direct materials120 × $25.20 3,024 Direct labor 40 × $10.00 400 FOH 80 × $15.20 1,216 Total $29,600

: From previous period’s $3,088 Aded during current period’s Direct materials20 × $ Direct labor60 × $ FOH40 × $ Started & Completed durring current period’s: 400 × $50.40$20,160 Work in process, ending (200 units): Direct materials120 × $ ,024 Direct labor 40 × $ FOH 80 × $ ,216 Total $29,600 Work In Process, Beginning (100 units): From previous period’s $3,088 Aded during current period’s Direct materials20 × $ Direct labor60 × $ FOH40 × $ Started & Completed durring current period’s: 400 × $50.40$20,160 Work in process, ending (200 units): Direct materials120 × $ ,024 Direct labor 40 × $ FOH 80 × $ ,216 Total $29,600.")

31

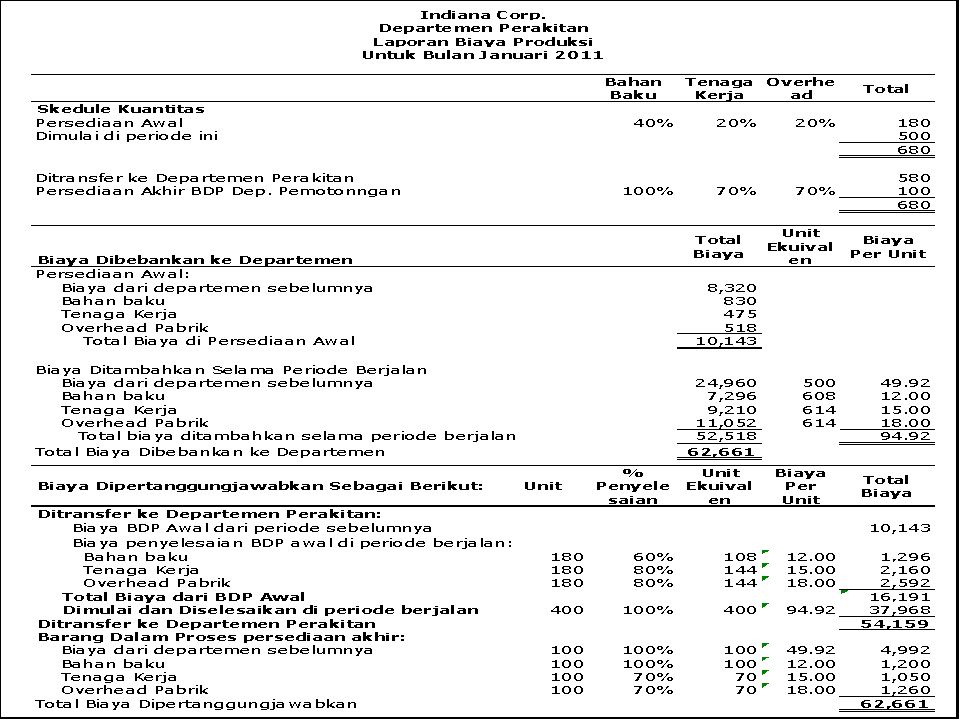

Step 1: Summarize the flow of physical units of output. CUTTINGASSEMBLING Work in process, beginning 100180 Started during current period in Cutting Dept. 600 Completed and transferred out during current period to Assembling Dept. 500 Started during current period in Assembling Dept. 500 Completed and transferred out during current period to Finish Goods. 580 Work in process, ending 200100

32

Step 2: Compute output in terms of equivalent units (Cont’d) CUTIING DEPT.DMDLFOH Work in process, beginning80%40%60% Work in process, ending60%20%40% ASSEMBLING DEPT.DMDLFOH Work in process, beginning40%20% Work in process, ending100%70%

CUTIING DEPT.DMDLFOH Work in process, beginning80%40%60% Work in process, ending60%20%40% ASSEMBLING DEPT.DMDLFOH Work in process, beginning40%20% Work in process, ending100%70%")

33

Step 2: Compute output in terms of equivalent units (Cont’d) Equivalent Units:Cost from Prev. Dept. DMDLFOH Work in process, begining 0108144 Started & Completed during current period’s 400 Work in process, ending 100 70 Total Equivalent Units 500608614 ASSEMBLING DEPT.

34

Step 3: Compute equivalent unit costs Cost ($)CUTTINGASSEMBLING WIP, Begining: Cost From Previous Dept: 8,320 Direct Materials 1,892830 Direct Labor 400475 Factory Overhead 796518 Cost Aded During Current Periods: Direct Materials 13,6087,296 Direct Labor 5,0009,210 Factory Overhead 7,90411,052

CUTTINGASSEMBLING WIP, Begining: Cost From Previous Dept: 8,320 Direct Materials 1, Direct Labor Factory Overhead Cost Aded During Current Periods: Direct Materials 13,6087,296 Direct Labor 5,0009,210 Factory Overhead 7,90411,052")

35

Step 3: Compute equivalent unit costs (Cont’d) ASSEMBLING DEPT. Equivalent Units:Cost from Prev. Dept. DMDLFOH Cost Aded During Current Periods 24,9607,2969,21011,052 Devided: Equivalent Units 500608614 Cost per Equivalent Units ($) 49.9212.0015.0018.00

")

36

Step 4 & 5: Summarize and Assign Total Costs ASSEMBLING DEPT. Step 4: Total costs to account for: $62,661 Step 5: Assign total costs: Work In Process, Beginning (180 units): From previous period’s $10,143 Aded during current period’s Direct materials108 × $12.00 1,296 Direct labor144 × $15.00 2,160 FOH144 × $18.00 2,592 Started & Completed durring current period’s: 400 × $94.92$37,968 Work in process, ending (200 units): Cost from prev. dept. 100 x $49.92 $4,992 Direct materials120 × $12.00 1,200 Direct labor 40 × $15.00 1,050 FOH 80 × $18.00 1,260 Total $62,661 Work In Process, Beginning (180 units): From previous period’s $10,143 Aded during current period’s Direct materials108 × $12.00 1,296 Direct labor144 × $15.00 2,160 FOH144 × $18.00 2,592 Started & Completed durring current period’s: 400 × $94.92$37,968 Work in process, ending (200 units): Cost from prev. dept. 100 x $49.92 $4,992 Direct materials120 × $12.00 1,200 Direct labor 40 × $15.00 1,050 FOH 80 × $18.00 1,260 Total $62,661

: From previous period’s $10,143 Aded during current period’s Direct materials108 × $ ,296 Direct labor144 × $ ,160 FOH144 × $ ,592 Started & Completed durring current period’s: 400 × $94.92$37,968 Work in process, ending (200 units): Cost from prev. dept. 100 x $49.92 $4,992 Direct materials120 × $ ,200 Direct labor 40 × $ ,050 FOH 80 × $ ,260 Total $62,661 Work In Process, Beginning (180 units): From previous period’s $10,143 Aded during current period’s Direct materials108 × $ ,296 Direct labor144 × $ ,160 FOH144 × $ ,592 Started & Completed durring current period’s: 400 × $94.92$37,968 Work in process, ending (200 units): Cost from prev. dept. 100 x $49.92 $4,992 Direct materials120 × $ ,200 Direct labor 40 × $ ,050 FOH 80 × $ ,260 Total $62,661.")

Similar presentations

Process Costing Elaborate on the process of process costing Understand the concept of equivalent units Talk about costs to account.>")