Download presentation

Presentation is loading. Please wait.

1

© 2016 OnCourse Learning California Real Estate Finance Fesler & Brady 10th Edition Chapter 9 Qualifying the Borrower

2

Objectives After completing this chapter, you should be able to: – Discuss income requirements to qualify for different types of loans. – Explain what effect debts have on a prospective borrower’s qualifications. – Describe how lenders analyze stability of income. – Explain why lenders are concerned about borrowers’ credit history and credit score. – Draw up a list of things that real estate agents can do to help clients to obtain financing.

3

Outline How Lenders Qualify Prospective Borrowers Ability or Capacity to Pay: A Case History Capacity to Pay Qualifying Under Government-Backed Loans What is Income? Co-Borrowing After Income, What Then? Desire to Pay Working with Lenders

4

How Lenders Qualify Prospective Borrowers Ability or capacity to pay – Earn enough – Steady source – Enough cash – Other assets Desire or willingness to pay – Continue making payments? – Credit Score – Fannie Mae’s Desktop Underwriting – Freddie Mac’s Loan Prospector

5

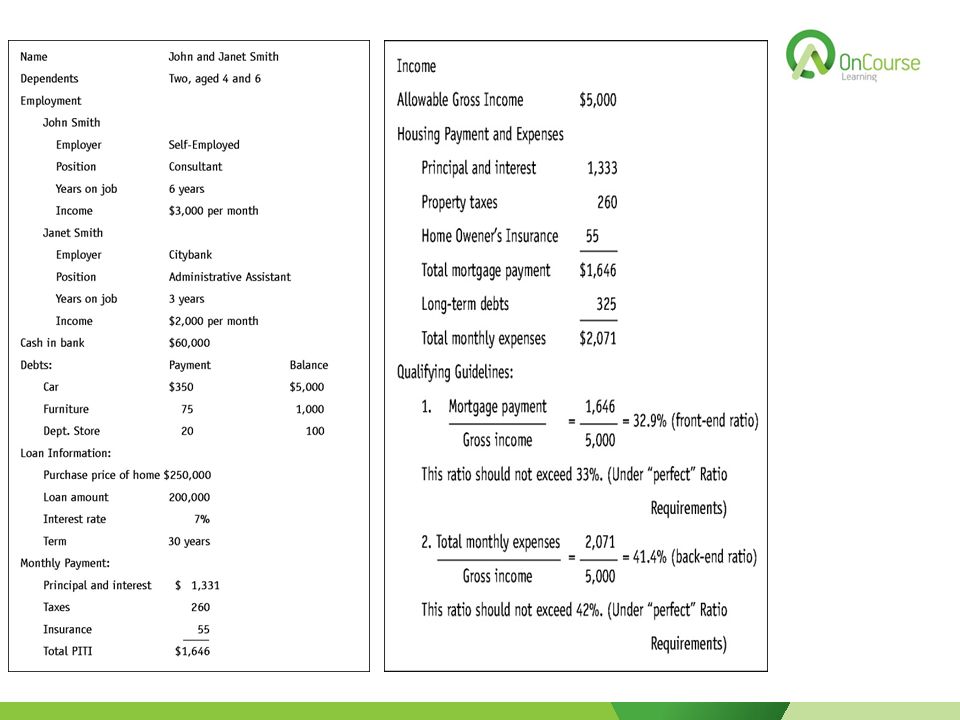

Ability or Capacity to Pay: A Case History See Case on pp. 236-237. Why qualify borrowers? – Just take back house – Lenders are in money business, not real estate business – High LTV ratios – Borrower could get “upside down” – If a loan is not sound for the borrower, it is not sound for the lender

6

Capacity to Pay Income ratios – Include PITI (FHA wants UFMIP & MMI also, Condos need HOA) – < 33% of gross income (See next slide for calculations) – But some go 45-50% Compensating factors – Substantial cushion/reserve – Co-borrower – Higher earnings potential – Large down payment – Currently making rent payments at same level Debts – Short term debts ignored – Long term (10 months or longer to pay off) Includes alimony and child support

– < 33% of gross income (See next slide for calculations) – But some go 45-50% Compensating factors – Substantial cushion/reserve – Co-borrower – Higher earnings potential – Large down payment – Currently making rent payments at same level Debts – Short term debts ignored – Long term (10 months or longer to pay off) Includes alimony and child support")

8

Qualifying Under Government- Backed Loans (FHA) Same procedure as conventional lenders Except front-end ratio <29% And back-end ratio <41%

Same procedure as conventional lenders Except front-end ratio <29% And back-end ratio <41%")

9

Qualifying Under Government- Backed Loans (DVA) Residual Income Method – Start with gross income – Subtract all taxes – To get Net Take-Home Pay – Subtract housing payment and fixed obligations – Remainder is Residual Income See next slide for example Figure 9.3 – Is this enough to provide for the needs of the family? Family size Geographic area Price of home and neighborhood Living pattern Income Ratio Application – PITI – Long term debt – All divided by gross monthly income Should be < 41% Compensating factors – Down payment – No vehicle payments – Few credit cards – Substantial net worth – Stable work history

10

Allowable gross income$5,300 Less: Federal income tax 677 State income tax 172 Social Security or retirement 382 Net take-home pay$4,069 Housing payment and fixed obligations Principal and interest$ 1,288 Property taxes 312 Homeowner’s insurance 66 Total mortgage payment$1,666 Maintenance/utilities (@14 cents/sq. ft.) 140 Total housing expense$1,806 Alimony and child support 0 Long-term debts $ 375 Job-related expense 0 Total housing and fixed obligations$2,181 Analysis Net take-home pay$4,069 Less: Housing and fixed expenses 2,181 Residual income$1,888 Figure 9.3 Summary of DVA qualifying procedure

140 Total housing expense$1,806 Alimony and child support 0 Long-term debts $ 375 Job-related expense 0 Total housing and fixed obligations$2,181 Analysis Net take-home pay$4,069 Less: Housing and fixed expenses 2,181 Residual income$1,888 Figure 9.3 Summary of DVA qualifying procedure.")

11

Qualifying Under Government- Backed Loans (Cal Vet) Adjusted Gross Income – Gross income – Less federal and state income taxes – Less Social Security – Equals AGI Remaining Income – Less house payments (PITI plus maintenance and utilities) – Less long term debts (> 1 year to pay off) – Equals RI RI/AGI = Residual – Should be >50% of AGI

Adjusted Gross Income – Gross income – Less federal and state income taxes – Less Social Security – Equals AGI Remaining Income – Less house payments (PITI plus maintenance and utilities) – Less long term debts (> 1 year to pay off) – Equals RI RI/AGI = Residual – Should be >50% of AGI")

12

What is Income? Salaries Commissions less expenses Overtime (not usually) Bonuses Part-Time Work Spousal/Alimony and Child Support – Need not be revealed or questioned – Payment can be questioned Pensions and Social Security Extra military pay (including free medical) Income from real estate Self-Employment All these need at least two year history

Bonuses Part-Time Work Spousal/Alimony and Child Support – Need not be revealed or questioned – Payment can be questioned Pensions and Social Security Extra military pay (including free medical) Income from real estate Self-Employment All these need at least two year history.")

13

Co-Borrowing Co-mortgagors might help with income Co-signers are on note, but not on title – Lenders do not like this

14

After Income, What Then? Length of time on job – > 2 years Type of job Age of borrower – No longer a factor Other assets – Gifts from parents for down payment Supply “gift letter”

15

Desire to Pay Past payment record Bankruptcy – Chapter 13 better than Chapter 7 – Wait 3-4 years Credit scores (Range from 300 - 900) – 720 required to get best loan terms and rates – Equifax – Experian – TransUnion – Affected by Late payments Collections Judgments Write offs Number of credit inquiries Too many unused accounts – Under Federal Fair and Accurate Credit Transaction (FACT) Act, everyone is entitled to a free copy of their credit report once a year

– 720 required to get best loan terms and rates – Equifax – Experian – TransUnion – Affected by Late payments Collections Judgments Write offs Number of credit inquiries Too many unused accounts – Under Federal Fair and Accurate Credit Transaction (FACT) Act, everyone is entitled to a free copy of their credit report once a year")

16

Motivation Down payment Reason for buying

17

Working with Lenders Possibility Honesty Cooperation Lender input Government-backed loans Exceptions and cover letters See www.myfico.com for more informationwww.myfico.com

18

Questions and Comments?

Similar presentations

Analyze the various sources of borrowing available to a client and.>")