Download presentation

Presentation is loading. Please wait.

1

GUE/NGL Parliamentary Group European Parliament 14 January 2016 ECB involvement in crisis management in Greece Marica Frangakis Member of SYRIZA Pol. Secretariat

2

Outline Where it all began – Steep increase in GG bond spreads The first Adjustment Programme, May 2010 The role of the ECB in 2010 The second Adjustment Programme, March 2012 The role of the ECB in 2012 - ‘preferred creditor status’ More ECB ‘unconventional measures’: OMT (2012-2014); negative interest rates (2014-2015); QE (2015-2017) Political realignments in Greece – the rise to power of SYRIZA The negotiations marathon The third Adjustment Programme, August 2015 The role of the ECB in 2015 – guardian of stability or enforcer of the creditors? Where we stand now – What role for the ECB?

3

Where it all began: 10-Year government bond spreads between Greece and Germany

4

The first Adjustment Programme, May 2010 Loan of €110 billion, of which €80 bn intergovernmental loans by the eurozone countries & €30 bn by the IMF; Until February 2012, €73bn disbursed. Of this, approx. 64% used to repay bonds and loans that matured between May 2010 - December 2011 & to support the Greek banking system through the HFSF 3.5% interest rate; maturities of 15-30 years; grace period of 10 years; seniority status (“the Borrower undertakes not to grant to any other creditor or hoder of its sovereign debt any priority over the Lenders”) Strictly conditional on implementation of severe austerity measures; Disbursement to be made in 13 tranches following review of fiscal developments of programme implementation

Strictly conditional on implementation of severe austerity measures; Disbursement to be made in 13 tranches following review of fiscal developments of programme implementation.")

5

The role of the ECB in 2010 ECB joins the Troika (Eur. Commission & IMF) - “The GC of the ECB welcomes the economic and financial adjustment programme which was approved today by the Greek government following the successful conclusion of the negotiations with the EC, in liaison with the ECB and the IMF” (Press Release, 2/5/2010 ) Securities Market Programme announced on 10/5/2010 – Purchases of government bonds in secondary markets to contain pressures from sovereign debt risk on banks, followed by sterilisation operations to avoid inflation (sterilised debt monetisation); in operation 2010-2012 Main ECB concern – risk of contagion; SMP allowed Eurozone banks to unload Greek & other Southern European countries’ government bonds on to ECB

- The GC of the ECB welcomes the economic and financial adjustment programme which was approved today by the Greek government following the successful conclusion of the negotiations with the EC, in liaison with the ECB and the IMF (Press Release, 2/5/2010 ) Securities Market Programme announced on 10/5/2010 – Purchases of government bonds in secondary markets to contain pressures from sovereign debt risk on banks, followed by sterilisation operations to avoid inflation (sterilised debt monetisation); in operation Main ECB concern – risk of contagion; SMP allowed Eurozone banks to unload Greek & other Southern European countries’ government bonds on to ECB.")

6

EZ bank exposure to S. Europe IMF: ‘Contagion from Greece was a major concern for euro area members given the considerable exposure of their banks to the sovereign debt of the euro area periphery’ (IMF,2013:8) Varoufakis: “None of the bailouts had the purpose of solving Greece’s problems. The original bailout was a cynical ploy for transferring losses from the books of the German and French banks onto the shoulders of the Greek, German and French taxpayers. The second bailout was merely an acknowledgment that the first bailout had imposed upon Greece conditions that it could never meet. Similarly with the one being prepared now.” (http://yanisvaroufakis.eu/2013/09/02/was- chancellor-merkel-about-greece/#more-4174

Varoufakis: None of the bailouts had the purpose of solving Greece’s problems. The original bailout was a cynical ploy for transferring losses from the books of the German and French banks onto the shoulders of the Greek, German and French taxpayers. The second bailout was merely an acknowledgment that the first bailout had imposed upon Greece conditions that it could never meet. Similarly with the one being prepared now. ( chancellor-merkel-about-greece/#more")

7

The second Adjustment Programme, March 2012 – Private Sector Involvement Troika forecast “GDP is expected to decline by 4% in 2010 and some 2,5% in 2011” failed completely; GDP declined by 5.3% and 8.9% while public debt ratio increased to 146% & 171% of GDP respectively New €133 bn loan and additional fiscal austerity measures Priority given to debt servicing payments; segregated account Obtaining political assurances from the leaders of the two major political parties PSI (debt restructuring) reduced value of GGB by 53%; this affected approx. 30% of debt while it absorbed 72% of bail out II (Euro 93.5 bn) Public debt ratio declined to 157% GDP in 2012 only to resume its upward climb in 2013 at 175% as GDP continued to fall

Public debt ratio declined to 157% GDP in 2012 only to resume its upward climb in 2013 at 175% as GDP continued to fall.")

8

The role of the ECB in 2012 - ‘preferred creditor status’ “Marketable debt instruments issued or fully guaranteed by the Hellenic Republic will become in principle eligible upon activation of … a number of measures aimed at assisting Greece in its adjustment programme. This is expected to take place by mid-March 2012” (ECB Press Release 28/2/2012) 2 nd Adjustment Programme signed on 2/3/2012: GGBs accepted as collateral in Eurosystem credit operations as of 8/3/2012 PSI did NOT reduce value of GGB held by ECB as part of its SM Programme; ECB enforced its ‘senior creditor status’ –ie, it should get its money back first in case of insolvency ‘Seniority’ is a source of instability as private investors react by selling bonds (P.de Grauwe, 2012)

2 nd Adjustment Programme signed on 2/3/2012: GGBs accepted as collateral in Eurosystem credit operations as of 8/3/2012 PSI did NOT reduce value of GGB held by ECB as part of its SM Programme; ECB enforced its ‘senior creditor status’ –ie, it should get its money back first in case of insolvency ‘Seniority’ is a source of instability as private investors react by selling bonds (P.de Grauwe, 2012).")

9

Financial instability: 2-year & 10-year maturity government bond yields of Spain, Italy, and Germany, 2010 - 2012

10

Draghi’s pledge ‘to do whatever it takes’ – Outright Monetary Transactions 2012-2015 Following Greece, Ireland (Dec. 2010) and Portugal (May 2011) also agreed on an Economic Adjustment Programme for a financial package of €85 bn and €78 bn respectively However financial stability spread across the financial markets; the Italian and Spanish government bonds came under pressure raising fears of imminent collapse ECB ‘Outright Monetary Transactions’ (OMT) programme: ECB makes purchases in secondary sovereign bond markets of bonds issued by EZ member-states, in order to prevent divergence in short-term bond yields; no ECB seniority claims OMT, limitless but subject to conditionalities - 1. existence of adjustment programme, 2. satisfactory compliance, 3. gaining access to bond markets, although 4. trading under stress

and Portugal (May 2011) also agreed on an Economic Adjustment Programme for a financial package of €85 bn and €78 bn respectively However financial stability spread across the financial markets; the Italian and Spanish government bonds came under pressure raising fears of imminent collapse ECB ‘Outright Monetary Transactions’ (OMT) programme: ECB makes purchases in secondary sovereign bond markets of bonds issued by EZ member-states, in order to prevent divergence in short-term bond yields; no ECB seniority claims OMT, limitless but subject to conditionalities - 1. existence of adjustment programme, 2. satisfactory compliance, 3. gaining access to bond markets, although 4. trading under stress.")

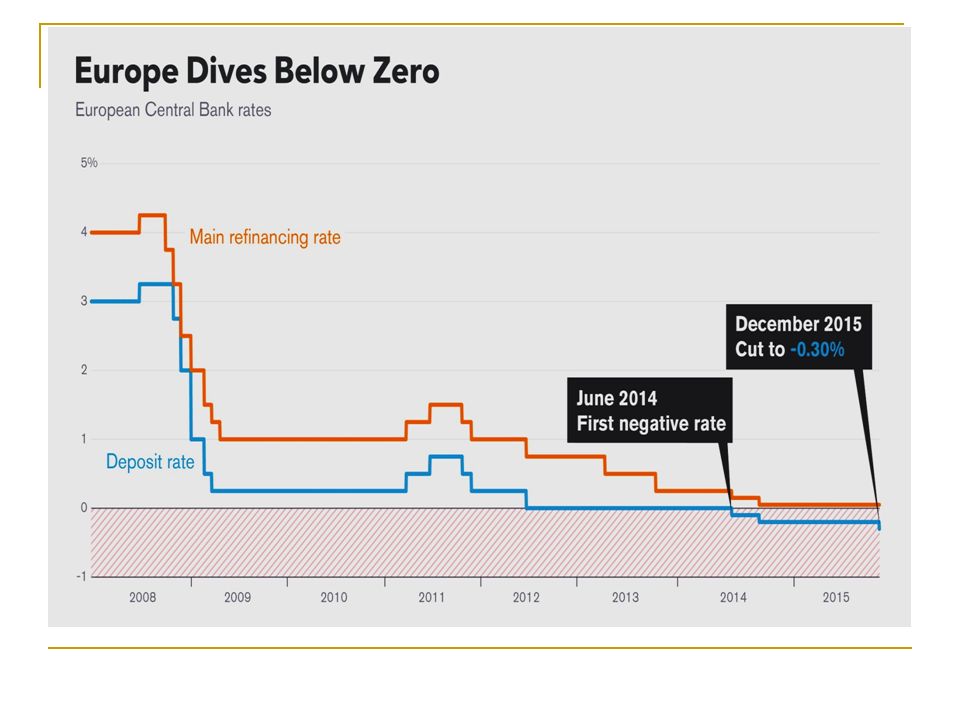

11

ECB worries over low inflation in Eurozone – ( Year-on-year % change in Consumer Prices) Shift in ECB main concern from halting contagion to getting inflation back to ‘below but close to 2%’ as per its mandate (consumer price index: <1% since 2014) ECB deposit rate turned negative in June 2014 & December 2015 (ECB charges banks 0.3% to hold their cash overnight) Rates below zero have never been used before in an economy as large as the euro area Liquidity trap: banks hoard the reserves they accumulate

Shift in ECB main concern from halting contagion to getting inflation back to ‘below but close to 2%’ as per its mandate (consumer price index: <1% since 2014) ECB deposit rate turned negative in June 2014 & December 2015 (ECB charges banks 0.3% to hold their cash overnight) Rates below zero have never been used before in an economy as large as the euro area Liquidity trap: banks hoard the reserves they accumulate")

13

More ECB ‘unconventional’ measures – ‘Asset Purchase Programme’ or QE, 2015 - 2017 The OMT instrument was never actually used even though it is considered to have been effective in stopping contagion It did however pave the way for APP in legal terms –OMT were challenged in German Fed Constitutional Court by German MPs; ECJ ruling (June 2015) declared OMT to be legal as they “do not exceed the powers of the ECB in relation to monetary policy and do not contravene the prohibition of monetary financing of EU nations” Asset Purchase Programme (APP): Announced on 22/1/2015, it consists of monthly purchases of public and private assets to the amount of Euro 60 bn; Euro 1.1 trillion to be allotted in proportion to the size of member states until March 2017 Dec 2015: APP Euro 650 bn (75,5% public assets); large countries benefit the most (Dec 2015: Germany 24%, France 19%, Italy:16%)

declared OMT to be legal as they do not exceed the powers of the ECB in relation to monetary policy and do not contravene the prohibition of monetary financing of EU nations Asset Purchase Programme (APP): Announced on 22/1/2015, it consists of monthly purchases of public and private assets to the amount of Euro 60 bn; Euro 1.1 trillion to be allotted in proportion to the size of member states until March 2017 Dec 2015: APP Euro 650 bn (75,5% public assets); large countries benefit the most (Dec 2015: Germany 24%, France 19%, Italy:16%)")

15

Political realignments – Electoral results 2009-2015 Per cent Share of votes 2009June 2012May 2014January 2015 September 2015 New Democracy33.529.622.727.828.1 SYRIZA (Radical Left)4.626.926.636.335.5 PASOK (Panhellenic socialist movement) 43.912.38.0 (ELIA) 4.76.3 (& DIMAR) Independent Greeks (split from ND) --7.53.54.83.7 Golden Dawn (fascists)--6.99.46.37.0 DIMAR (Democratic Left; split from SYRIZA) --6.31.20.5-- KKE (Communist Party)7.54.56.15.55.6 LAOS (extreme right)5.6-- POTAMI (centrist)-- 6.66.14.1 CENTRISTS (Leventis)-- 3.4

PASOK (Panhellenic socialist movement) (ELIA) (& DIMAR) Independent Greeks (split from ND) Golden Dawn (fascists) DIMAR (Democratic Left; split from SYRIZA) KKE (Communist Party) LAOS (extreme right)5.6-- POTAMI (centrist) CENTRISTS (Leventis)-- 3.4")

16

The negotiations marathon Government sworn in 27 th Jan; 2012 loan expiring in Dec 2014 extended by previous government to end Feb 2015 (Tsipras: ‘we were trapped’); outstanding tranches of loans (7.2 bn Euro) payable on completion of Troika review Tight repayments schedule: end April 2015: IMF, 2.937 bn Euro & roll over short-term T-bills bought by Greek banks, 11 bn; end August: IMF, 2.522 bn & ECB, 6.7 bn; end 2015: IMF, 3.247 bn Tsipras ( Le Monde, 31/5/2015): seeking ‘a mutually beneficial agreement that will set realistic goals regarding surpluses, while also reinstating an agenda of growth and investment’ 5 th July Referendum: Yes/No to creditors’ proposals; 61.3% No Tsipras (interviewed,14/7/2015): ‘The result of the Euro Summit and the Eurogroup was the result of a strong pressure on a country, which had democratically expressed itself, to satisfy the more financially powerful countries in Europe. That is the truth’

17

The third Adjustment Programme, August 2015 New loan Euro 86 bn, of which 54 bn for debt service (63%), 25 bn for Greek banks (29%) and 15 bn for arrears clearance & budget cash buffer (17%) Not included in above sum: expected primary surplus Euro 6 bn & expected proceeds from privatisation Euro 2.5 bn Loan maturity: 32.5 years; Interest rate: funding cost + fees, approx. 1% at present Conditionality: further fiscal consolidation; recapitalisation of Greek banks; structural/institutional reforms Deficit/GDP targets: 2015, -0.25%; 2016, +0.5%; 2017, +1.75%; 2018, +3.5%; primary surplus transferred to segregated account for debt service + 30% of any over-performance Privatisation – Fund “to manage valuable Greek assets & to maximise their value which it will monetize through privatisations and other means”; expected proceeds 50 bn by 2030, of which 75% for debt service and 25% for investment

18

Greek banking system – Deposit flight; increase in NPLs

19

The role of the ECB in 2015 - Guardian of stability or enforcer of the creditors? ECB intensified conditions of asphyxiation for the Greek banks and economy by (1) 4 th Feb: lifting waiver of min credit rating requirement for GGBs thus shifting banks to a costlier source of borrowing (ELA) (2) 26 th June: freezing amount of funding (at 89 bn euro) available to Greek banks after July referendum announced; (3) 6 th July: imposing a haircut on GGBs used as collateral Flight of deposits (15% in Jan-June 2015); steep increase in NPLs; capital controls (banks closed for three weeks after 28 th June); danger of collapse of banking system Paul de Grawe: “The correct announcement of the ECB should be that it will provide all the necessary liquidity to the Greek banks. Such an announcement will pacify depositors. The ECB has other objectives than stabilising the Greek banking system. These objectives are political. The ECB continues to put pressure on the Greek government to behave well.”

4 th Feb: lifting waiver of min credit rating requirement for GGBs thus shifting banks to a costlier source of borrowing (ELA) (2) 26 th June: freezing amount of funding (at 89 bn euro) available to Greek banks after July referendum announced; (3) 6 th July: imposing a haircut on GGBs used as collateral Flight of deposits (15% in Jan-June 2015); steep increase in NPLs; capital controls (banks closed for three weeks after 28 th June); danger of collapse of banking system Paul de Grawe: The correct announcement of the ECB should be that it will provide all the necessary liquidity to the Greek banks. Such an announcement will pacify depositors. The ECB has other objectives than stabilising the Greek banking system. These objectives are political. The ECB continues to put pressure on the Greek government to behave well. .")

20

Where we stand now – What role for the ECB Greek banks were stress-tested and recapitalised by end 2015; no bail-in of unsecured deposits; government contribution: <6 bn euro (25 bn budgeted in 3 rd loan) ELA funding reduced to 77 bn euro (Nov 2015) from cap of 89 bn euro (June 2015); Waiver of min credit rating requirement for GGBs has not been reinstated; Draghi: “still too early to reinstate a waiver that would give Greek banks access to the funding window … Athens would have to first comply with and “show strong ownership” of its bailout program” (Sept 2015) Capital controls still in place, albeit gradually relaxed The Greek economy remains in the clutch of a crushing public debt; negotiations on debt relief expected to take place in 2016 The ECB can play an important role in getting the Greek economy out of the debt-deflation deadlock: reinstating waiver, abolishing haircut, returning profits on SMP, admitting GGB to APP

ELA funding reduced to 77 bn euro (Nov 2015) from cap of 89 bn euro (June 2015); Waiver of min credit rating requirement for GGBs has not been reinstated; Draghi: still too early to reinstate a waiver that would give Greek banks access to the funding window … Athens would have to first comply with and show strong ownership of its bailout program (Sept 2015) Capital controls still in place, albeit gradually relaxed The Greek economy remains in the clutch of a crushing public debt; negotiations on debt relief expected to take place in 2016 The ECB can play an important role in getting the Greek economy out of the debt-deflation deadlock: reinstating waiver, abolishing haircut, returning profits on SMP, admitting GGB to APP")

Similar presentations

at a financial institution. Certificates of.>")