Download presentation

Presentation is loading. Please wait.

1

Cost of Production Chapter 5 Section 2

2

Objectives Explain how firms decide how much labor to hire to produce a certain level of output. Analyze the production costs of a firm. Understand how a firm chooses to set output. Explain how a firm decides to shut down and unprofitable business. Key Terms Marginal product of labor Increasing marginal returns Diminishing marginal returns Fixed cost Variable cost Total cost Marginal cost Marginal revenue Operating cost

3

Labor and Output

4

Labor and Output Marginal Product of Labor Increasing Marginal Returns

The change in output from hiring one more worker Measures the change in output at the margin; increase in output added by the last unit of labor Increasing Marginal Returns Output goes up when a worker is added for production Workers can specialize, therefore production increases A.K.A. rising marginal product of labor

5

Labor and Output Diminishing Marginal Returns

When adding more workers increases total output, but at a decreasing rate Less and less output from each additional unit of labor Negative Marginal Returns The stage where output decreases due to the added labor; workers get in each others’ way and disrupt the production process

6

Paper Chain Gang Labor (# of Workers) Output (Paper links per minute)

Marginal Product of Labor

7

Production Costs

8

Production Costs Fixed Costs Variable Costs

A cost that does not change no matter how much of a good is produced Examples: facilities, rent, machinery repairs, property taxes, salaries What are fixed costs for a high school? Variable Costs Costs that rise or fall depending on the quantity produced Examples: raw materials, some labor (since it changes with the # of workers), heat, electricity What are some variable costs for a high school?

, heat, electricity. What are some variable costs for a high school")

9

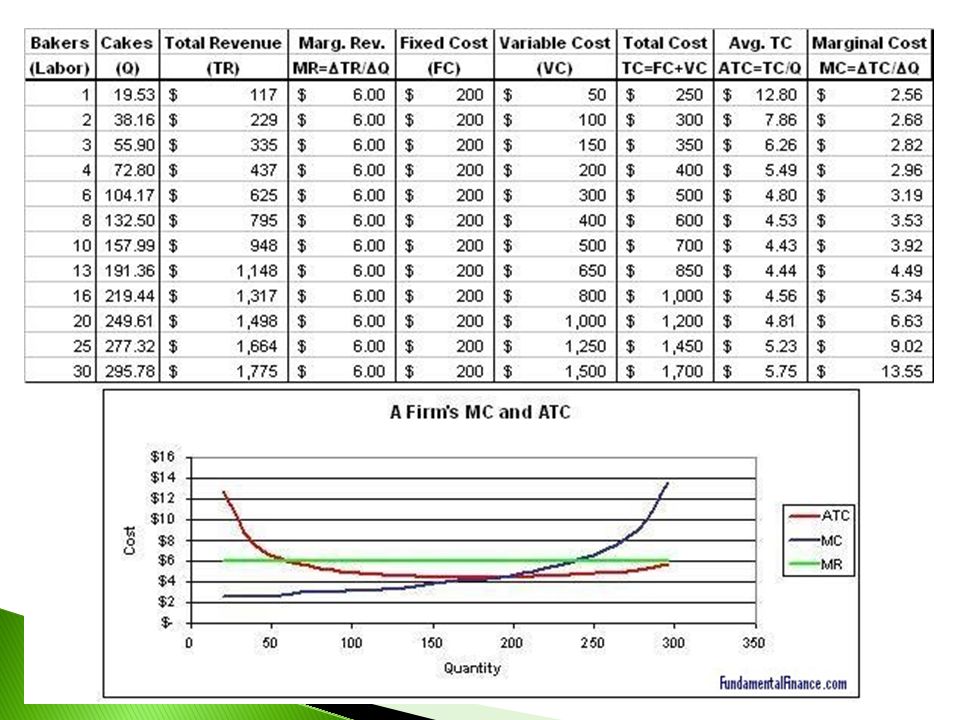

Production Costs Total Cost Marginal Cost

Fixed Costs plus the variable costs Marginal Cost The cost of producing one more unit of a good

10

Setting Output A company’s goal is to make profit.

Profit= Total Revenue-Total Cost Revenue= Price X Quantity Total Cost= Fixed costs + Variable costs ***To find the level of output with the highest profit, look for the biggest gap between total revenue and total cost.***

11

Marginal Revenue and Marginal Cost Responding to Price Changes

Setting Output Marginal Revenue and Marginal Cost Responding to Price Changes Marginal Revenue Additional income from selling one more unit Is the market price for the good When marginal revenue =marginal cost, then pure profit results (ideal) Profit results when the company receives more for the last product than it cost to produce This is where the law of supply goes into ACTION! If the market price increases, then marginal revenue increases, thus increasing production so that the firm can capture profits. See figure 5.11 pg 113

Profit results when the company receives more for the last product than it cost to produce. This is where the law of supply goes into ACTION! If the market price increases, then marginal revenue increases, thus increasing production so that the firm can capture profits. See figure 5.11 pg 113.")

13

The Shutdown Decision When the market price is so low that the factory’s total revenue is less than the total cost, the firm looses money! A factory owner must determine if the profit-maximizing level is sufficient to cover the operating costs (cost of running the facility) Operating costs include variable costs to keep the factory running, but do not include fixed costs that will need to be paid regardless of production. When might a factory decide to stop production? What could a factory do to pay it’s fixed costs if it closes?

Operating costs include variable costs to keep the factory running, but do not include fixed costs that will need to be paid regardless of production. When might a factory decide to stop production What could a factory do to pay it’s fixed costs if it closes")

Similar presentations