Download presentation

Presentation is loading. Please wait.

1

© 2016 OnCourse Learning California Real Estate Finance Fesler & Brady 10th Edition Chapter 11 Foreclosures and Other Lending Problems

2

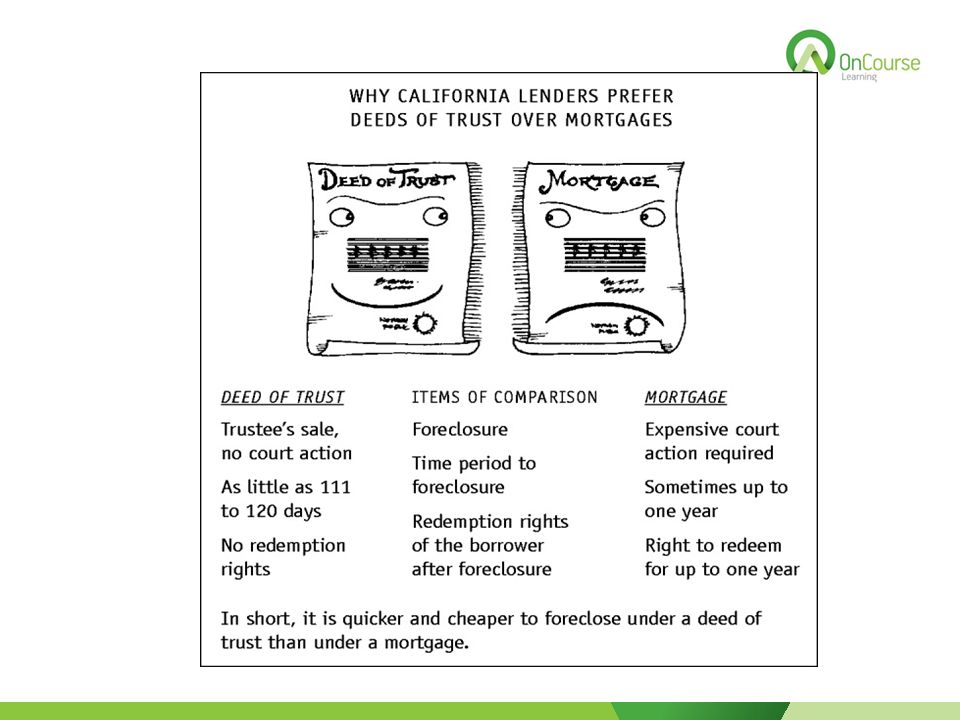

Objectives After completing this chapter, you should be able to: – Explain the major provisions outlined in a typical promissory note and deed of trust. – Outline the steps in a foreclosure procedure. – Demonstrate why lenders in California prefer trust deeds over mortgages as security for their loans. – List five ways a borrower and lender can minimize the possibility of a default and foreclosure. – Discuss how private and government mortgage insurance has reduced the lender’s risk in granting real estate loans. – Calculate the mechanics of insurance coverage under PMI for 90 percent loans. – Describe the controversial practice known as redlining. – Explain the role of the Community Reinvestment Act (CRA).

..")

3

Outline Collateral Provisions of Deeds of Trust Default and Foreclosure Minimizing Loan Defaults Other Lending Problems

4

Collateral Provisions of Deeds of Trust Maintenance of the property Hazard insurance – Fire – Windstorm Property taxes and other liens Assignment of rents – If borrower defaults, lender can lease and apply to loan

5

Default and Foreclosure (Slide 1 of 3) Trustee’s Sale – Allowed by power of sale clause in trust deed – Notice of Default (three months before sale) Send to trustor within 10 days Could reinstate by paying all back debts and resuming payments (right of reinstatement up to 5 days before sale) – Notice of sale (two weeks before sale) Post on property 20 days before – Final sale Highest bidder (except for trustee) – Cash or equivalent Surplus funds given to trustor (former owner) – No right of redemption

Trustee’s Sale – Allowed by power of sale clause in trust deed – Notice of Default (three months before sale) Send to trustor within 10 days Could reinstate by paying all back debts and resuming payments (right of reinstatement up to 5 days before sale) – Notice of sale (two weeks before sale) Post on property 20 days before – Final sale Highest bidder (except for trustee) – Cash or equivalent Surplus funds given to trustor (former owner) – No right of redemption")

6

Default and Foreclosure (Slide 2 of 3) Judicial Sale (foreclose as mortgage not trust deed) – Procedure Serve complaint Trial held Judgment entered Right of reinstatement – Sale Highest bidder Debtor has one year right of redemption (pay off all debt) if deficiency exists – Deficiency judgments If sale is not sufficient to pay loan, former owner still owes – California’s Anti-deficiency Law is the exception – Except for FHA and DVA

Judicial Sale (foreclose as mortgage not trust deed) – Procedure Serve complaint Trial held Judgment entered Right of reinstatement – Sale Highest bidder Debtor has one year right of redemption (pay off all debt) if deficiency exists – Deficiency judgments If sale is not sufficient to pay loan, former owner still owes – California’s Anti-deficiency Law is the exception – Except for FHA and DVA")

7

Default and Foreclosure (Slide 3 of 3) Deed in Lieu of Foreclosure – Or quitclaim deed from borrower to lender – No deficiency claim Voluntary conveyance from borrower to lender Any of these look bad on the credit report

Deed in Lieu of Foreclosure – Or quitclaim deed from borrower to lender – No deficiency claim Voluntary conveyance from borrower to lender Any of these look bad on the credit report")

9

Minimizing Loan Defaults (Slide 1 of 3) Impound accounts (aka escrow account or loan trust fund) – Property taxes – Insurance Forbearance – Moratorium on payments Waiver of principal payments Deferring of interest Partial payments Prior prepayments now used – Recasting Change in loan terms – Extended term – Increase of debt – Reduction of interest – Reduction of principal

Impound accounts (aka escrow account or loan trust fund) – Property taxes – Insurance Forbearance – Moratorium on payments Waiver of principal payments Deferring of interest Partial payments Prior prepayments now used – Recasting Change in loan terms – Extended term – Increase of debt – Reduction of interest – Reduction of principal")

10

Minimizing Loan Defaults (Slide 2 of 3) Mortgage Guaranty Insurance – Cost borne by borrower Through MIP or MMI – Government insured – FHA Indemnifies lender Takes over property Sells either refurbished or “as is” Or HUD takes over loan – DVA Pays lender up to insurance level Subrogates against borrower – FHLMC Three months to cure deficiency – California Veterans Farm and Home Purchase Act Assistance Life and disability insurance for borrowers – Private Mortgage Insurance (Discussed in Chapter 5)

Mortgage Guaranty Insurance – Cost borne by borrower Through MIP or MMI – Government insured – FHA Indemnifies lender Takes over property Sells either refurbished or as is Or HUD takes over loan – DVA Pays lender up to insurance level Subrogates against borrower – FHLMC Three months to cure deficiency – California Veterans Farm and Home Purchase Act Assistance Life and disability insurance for borrowers – Private Mortgage Insurance (Discussed in Chapter 5)")

11

Minimizing Loan Defaults (Slide 3 of 3) Automatic payment plans Consumer protection laws and regulations – Truth in Lending (aka Consumer Credit Protection Act Full disclosure of all borrowing charges – Home Warranties Cover major home components – Plumbing – Electrical – HVAC – Walls, roof & foundation Usually one year

Automatic payment plans Consumer protection laws and regulations – Truth in Lending (aka Consumer Credit Protection Act Full disclosure of all borrowing charges – Home Warranties Cover major home components – Plumbing – Electrical – HVAC – Walls, roof & foundation Usually one year")

12

Other Lending Problems (Slide 1 of 3) Usury – Max rate is 10% or – 5% above Federal Reserve discount rate – Not applied to seller carrybacks Redlining – Refuse loans in high risk areas – Illegal – Community Reinvestment Act Lenders must disclose lending data

Usury – Max rate is 10% or – 5% above Federal Reserve discount rate – Not applied to seller carrybacks Redlining – Refuse loans in high risk areas – Illegal – Community Reinvestment Act Lenders must disclose lending data")

13

Other Lending Problems (Slide 2 of 3) Community Reinvestment Act (CRA) and The Financial Institutions Reform, Recovery and Enforcement Act (FIRREA) – Lenders report on Race Gender Income Census tract – Grades each institution Home Mortgage Disclosure Act (HDMA) – Annual report of applications and loans granted

Community Reinvestment Act (CRA) and The Financial Institutions Reform, Recovery and Enforcement Act (FIRREA) – Lenders report on Race Gender Income Census tract – Grades each institution Home Mortgage Disclosure Act (HDMA) – Annual report of applications and loans granted")

14

Other Lending Problems (Slide 3 of 3) Short Sales – Upside down – The Mortgage Debt Forgiveness Act of 2007 Retroactive for sales from January 2007 Debt forgiveness for <$2M for personal residence Effective through 2012 – Eliminated 100% financing and other high LTV loans

Short Sales – Upside down – The Mortgage Debt Forgiveness Act of 2007 Retroactive for sales from January 2007 Debt forgiveness for <$2M for personal residence Effective through 2012 – Eliminated 100% financing and other high LTV loans")

15

Web Help www.hud.gov www.freddiemac.com www.ftc.gov www.mbaa.org www.mortgagemag.com

16

Questions and Comments?

Similar presentations

>")

–Commercial Larger apartments & non-residential.>")