Download presentation

Presentation is loading. Please wait.

1

1 Individual Account Investment Options and Portfolio Choice: Behavioral Lessons from 401(k) Plans

Plans")

2

2 The Growing Importance of Asset Accumulation U.S. is witnessing a shift toward increasing self- reliance in retirement planning Shift from DB to DC pension plans Potential for personal accounts as part of Social Security Individual accounts put more emphasis on creating financial wealth for retirement, rather than relying on a formula-based pension approach Portfolio choice one key determinant of retirement wealth (allocation, location, expenses)

.")

3

3 Plan Design and Behavior Plan design can have important effects on retirement wealth accumulation in cross section Default options for participation Madrian & Shea (2001); Choi, Laibson, Madrian, & Metrick (2002) Number and type of investment options available Benartzi & Thaler (2001) Match Policy Benartzi (2001); Brown, Liang, & Weisbenner (2006)

; Choi, Laibson, Madrian, & Metrick (2002) Number and type of investment options available Benartzi & Thaler (2001) Match Policy Benartzi (2001); Brown, Liang, & Weisbenner (2006)")

4

4 Differing Views on Value of Large Number of Options Standard economics view: “More options are good, or at worst, unnecessary” Constraints are either not binding or bad, never good Portfolio theory: only need one risky asset (the “market” portfolio) and one riskless asset Behavioral view: “More choice is potentially bad” Information overload if too many options Huberman, Iyengar, & Jiang (2007); Agnew & Szykman (2004)

and one riskless asset Behavioral view: More choice is potentially bad Information overload if too many options Huberman, Iyengar, & Jiang (2007); Agnew & Szykman (2004)")

5

5 Our Focus Does the share of investment options in a particular asset class influence portfolio allocations to that asset class? More specifically, how has growth in actively-managed equity funds affected 401(k) allocations?

allocations .")

6

6 What Do We Add? Our data enable us to exploit both cross- sectional AND time-series variation in the number and type of options offered to identify how retirement-plan parameters affect portfolio allocations Enables us to control for sorting effects that may confound cross-sectional results

7

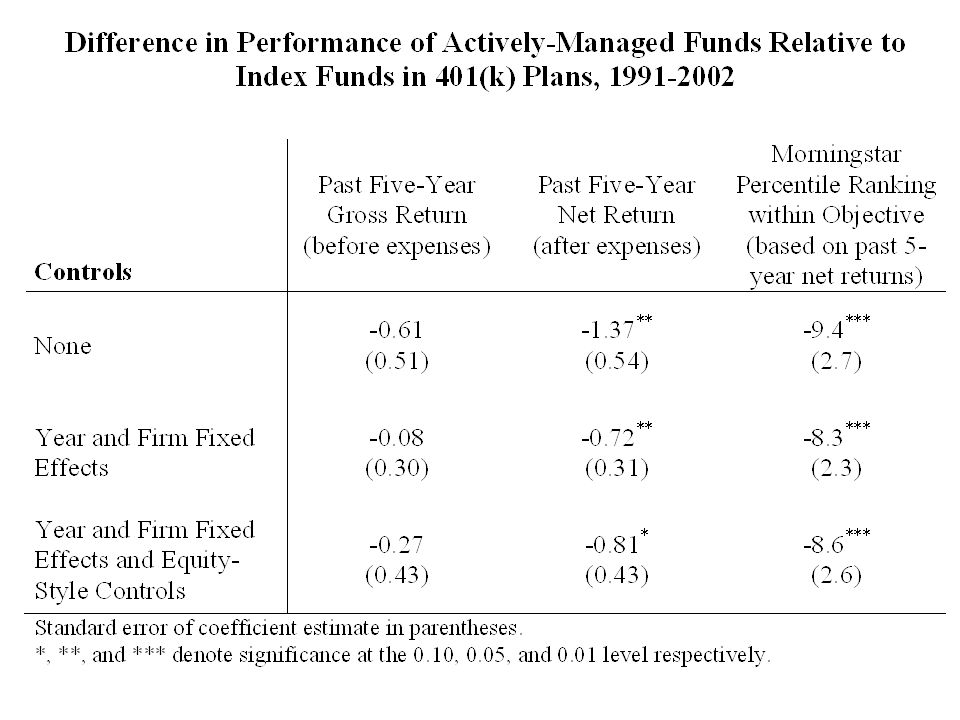

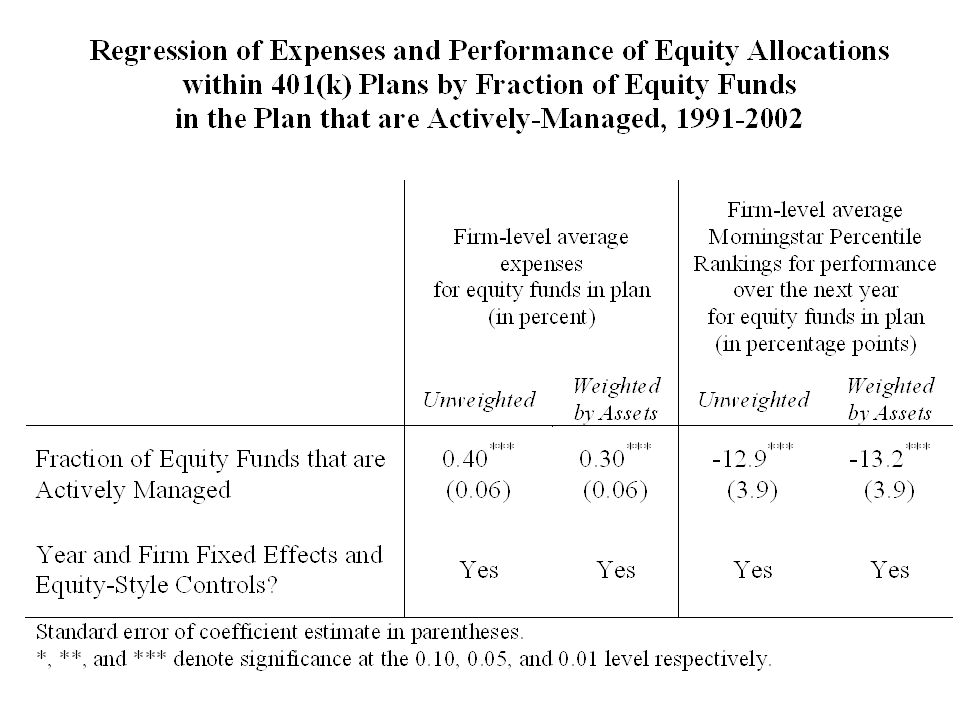

7 Key Findings 1.Evidence that both plan parameters and firm-level heterogeneity important 2.Mix of options across equities and bonds is a strong determinant of allocations across these asset classes 3.Growth in number of actively-managed equity funds (with high expenses) leads to a smaller share of assets in low-cost index funds, resulting in higher expenses and worse performance

leads to a smaller share of assets in low-cost index funds, resulting in higher expenses and worse performance")

8

DATA

9

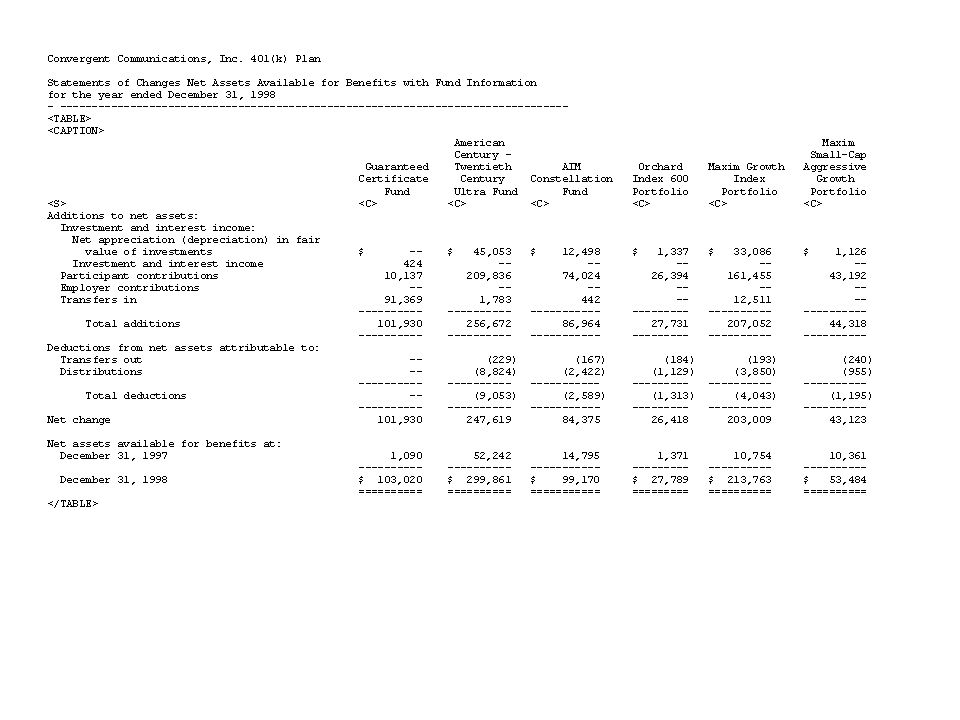

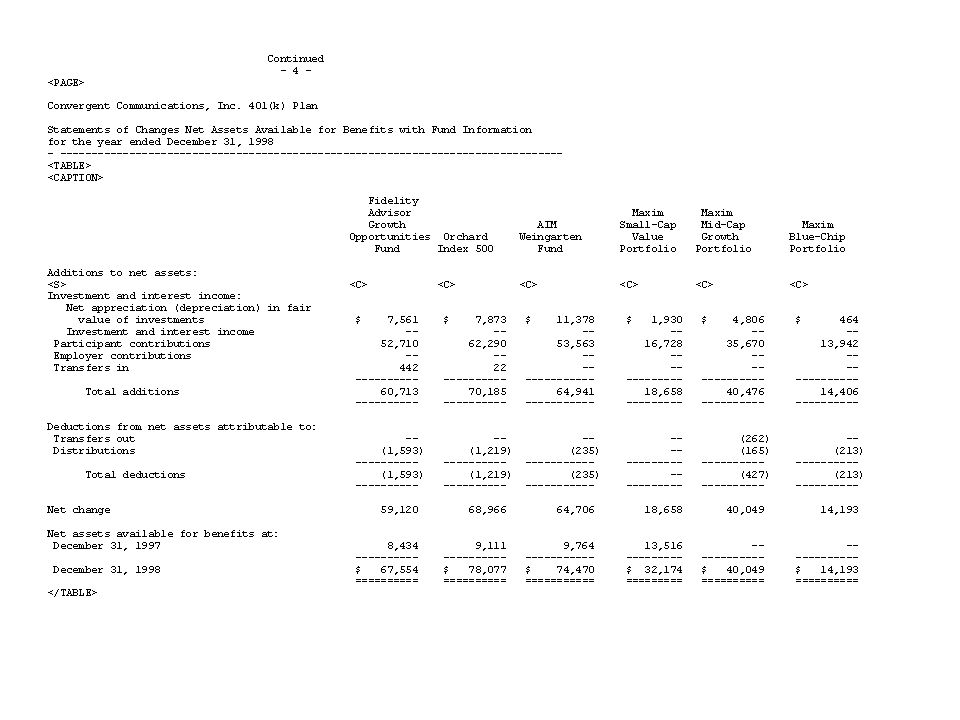

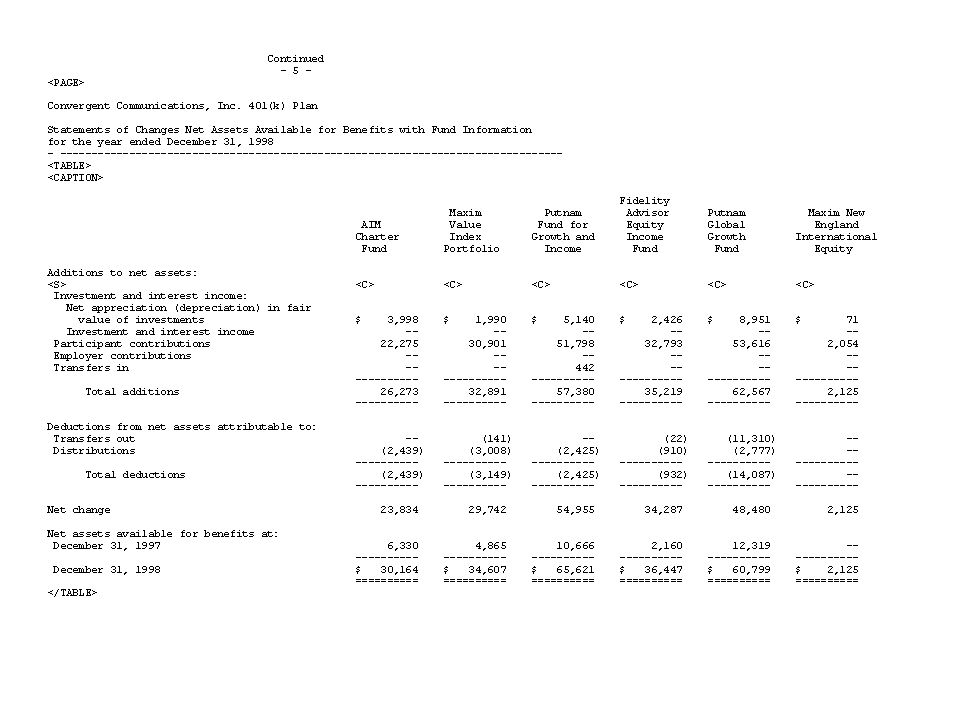

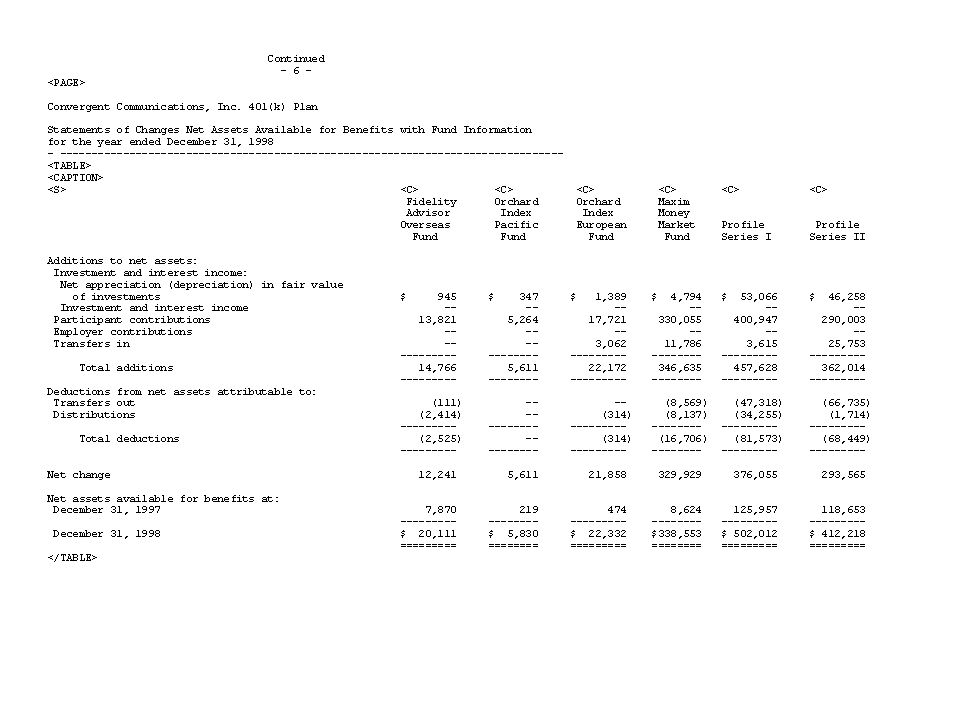

9 Retirement-Plan Data 11-k filings with the SEC is the key data source Filed by firms with 401(k) plans that offer employer stock as an investment option (and it is deemed new equity issuance) Detailed information on specific plan investment 1993-1998 information on contributions and balances for each plan option (some firms report 1991 & 1992 data in 1993 report) 1999+ reporting requirements change, only statement of end-of-year balances provided for each plan option (contribution data reported by just a few firms)

plans that offer employer stock as an investment option (and it is deemed new equity issuance) Detailed information on specific plan investment information on contributions and balances for each plan option (some firms report 1991 & 1992 data in 1993 report) reporting requirements change, only statement of end-of-year balances provided for each plan option (contribution data reported by just a few firms)")

18

18 Our Sample(s) Collect data on employee contributions and balances across five asset classes (company stock, domestic equity, international, fixed income, and balanced funds) This sample primarily covers the period 1993-1998 891 firms in the sample just over 3 years on average Broad cross section Represent roughly 1/3 of 401(k) assets/contributions of publicly-traded firms in 1998 Good representation across industries About 1/5 belong to S&P 500

Collect data on employee contributions and balances across five asset classes (company stock, domestic equity, international, fixed income, and balanced funds) This sample primarily covers the period firms in the sample just over 3 years on average Broad cross section Represent roughly 1/3 of 401(k) assets/contributions of publicly-traded firms in 1998 Good representation across industries About 1/5 belong to S&P 500")

19

19 Our Sample(s) We later augment this earlier-period data by following the firms that filed an 11-k in 1998 over next 4 years (1999 – 2002) Limited to looking at asset balances (not contributions)

We later augment this earlier-period data by following the firms that filed an 11-k in 1998 over next 4 years (1999 – 2002) Limited to looking at asset balances (not contributions)")

20

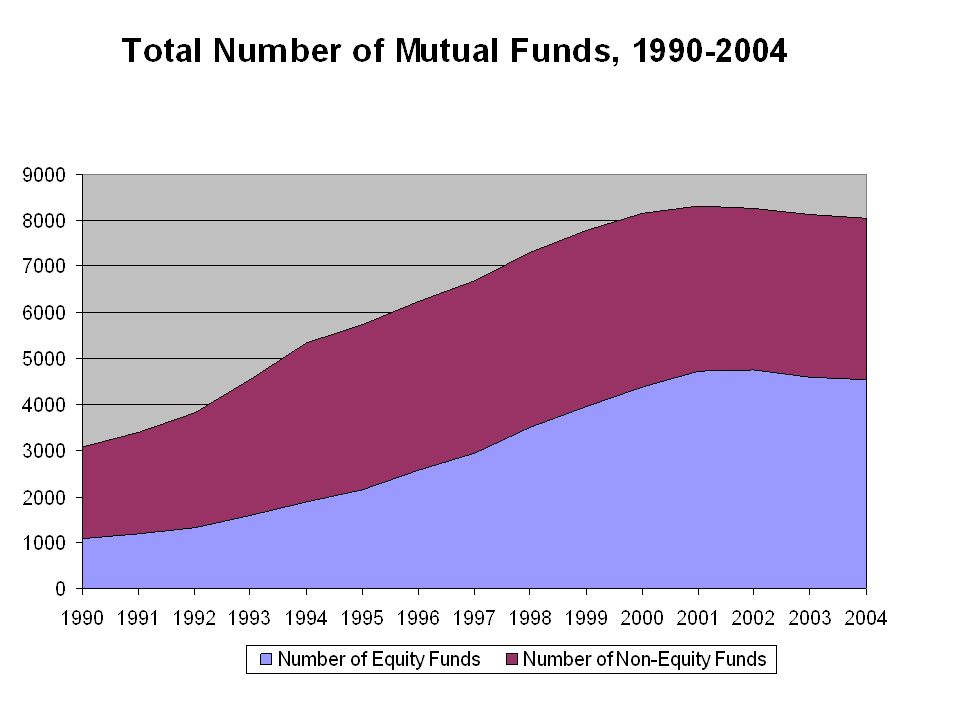

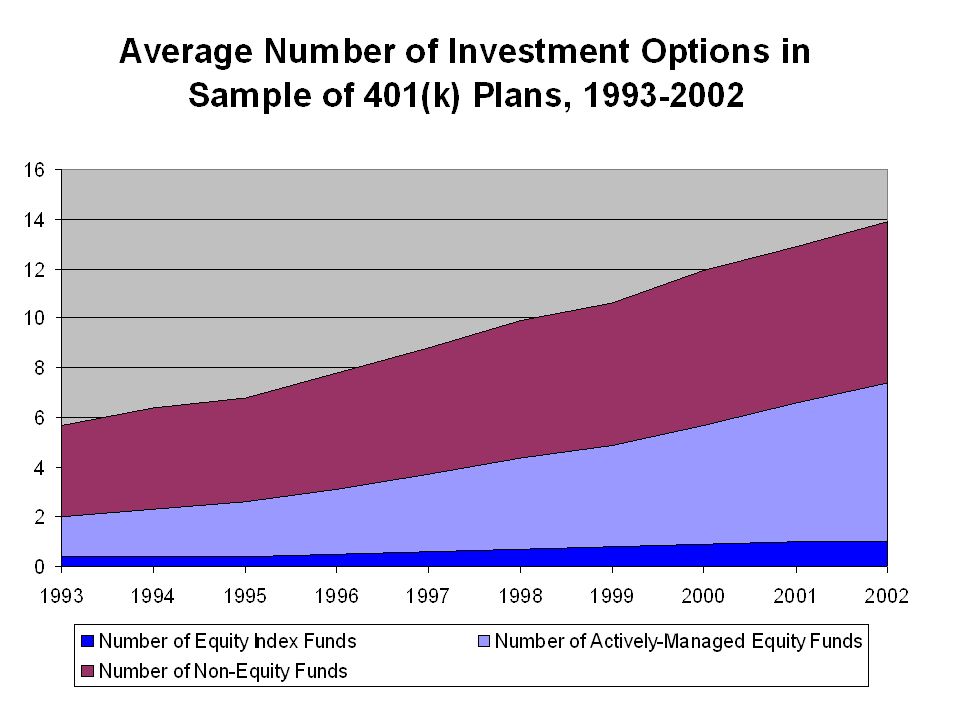

Background: Number of Mutual Funds and 401(k) Options

Options")

24

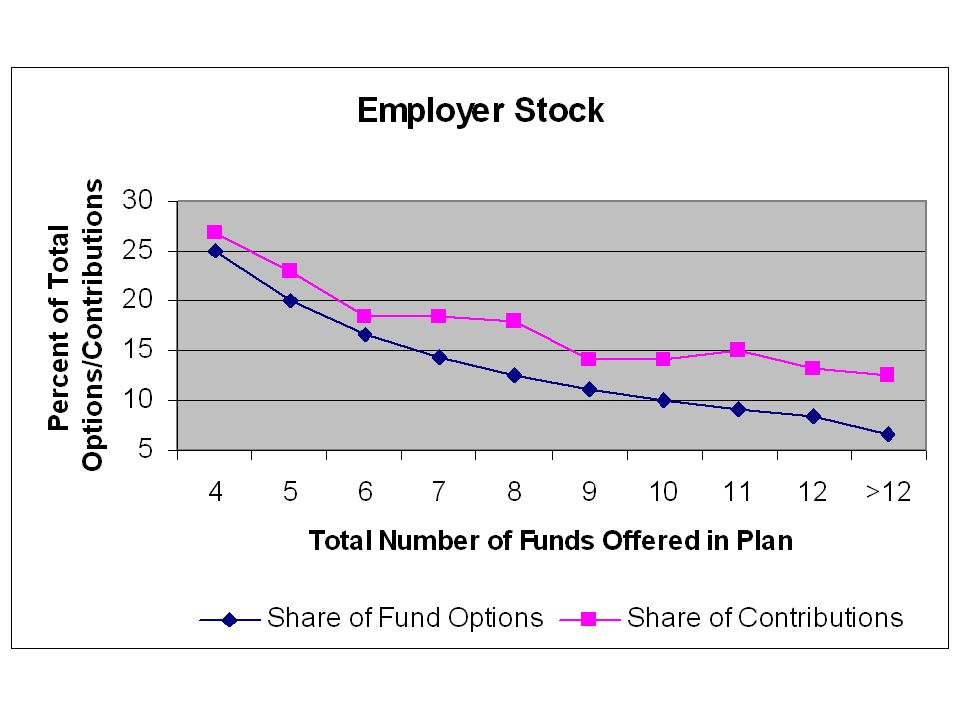

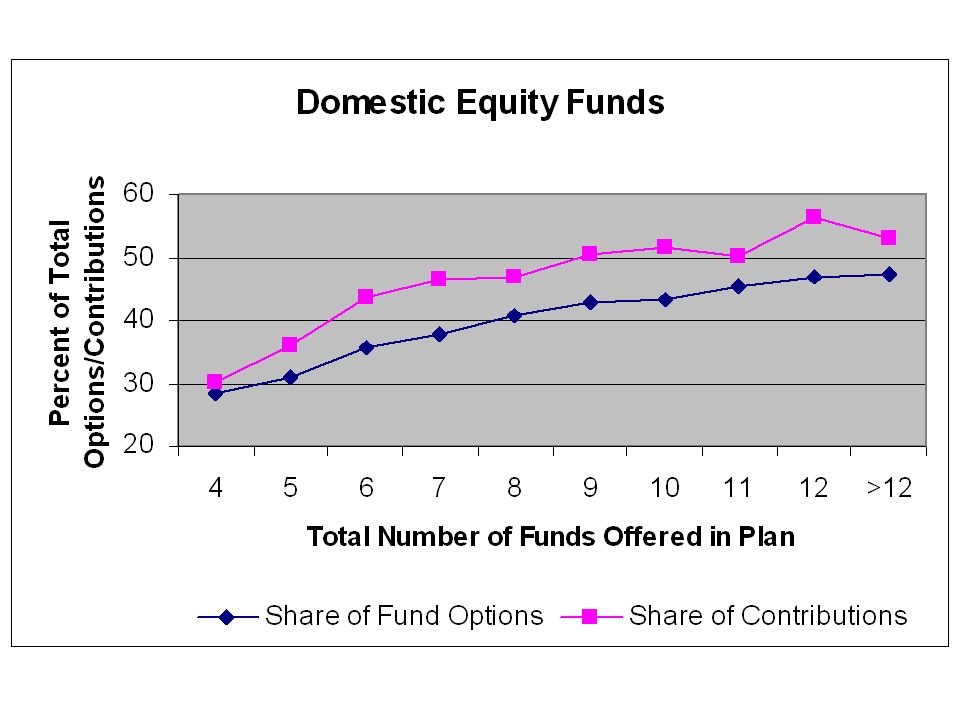

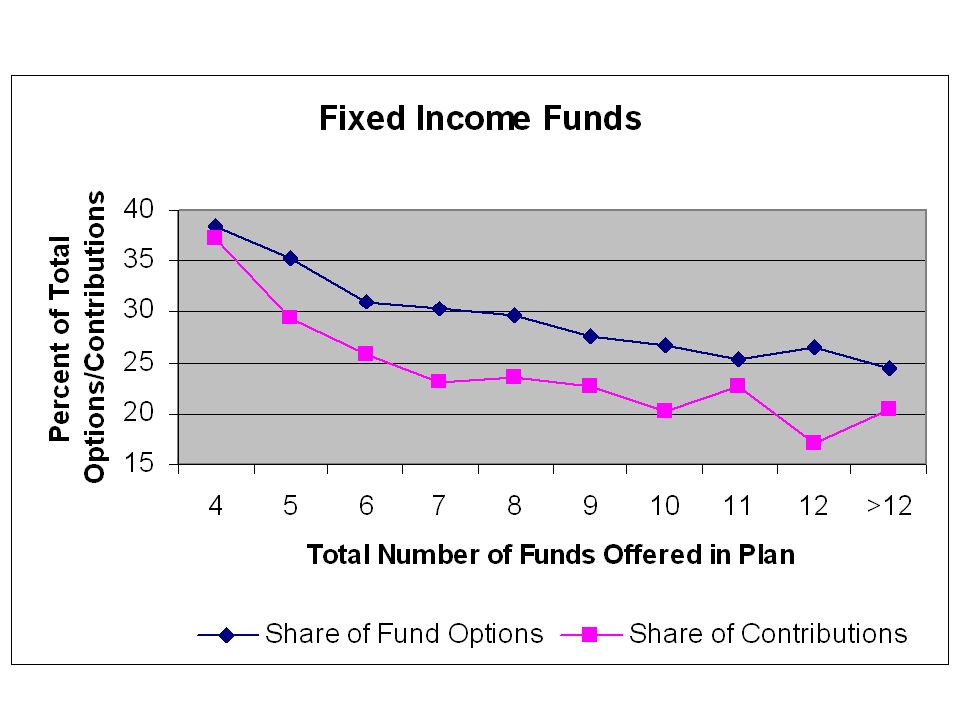

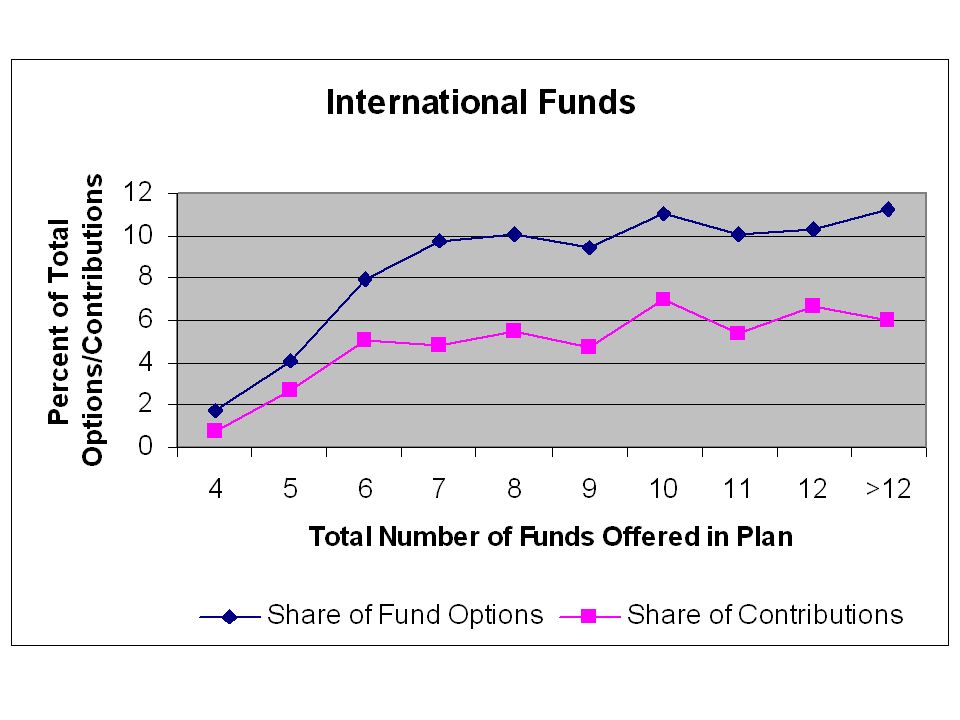

Mix of Options and Allocation of Contributions

30

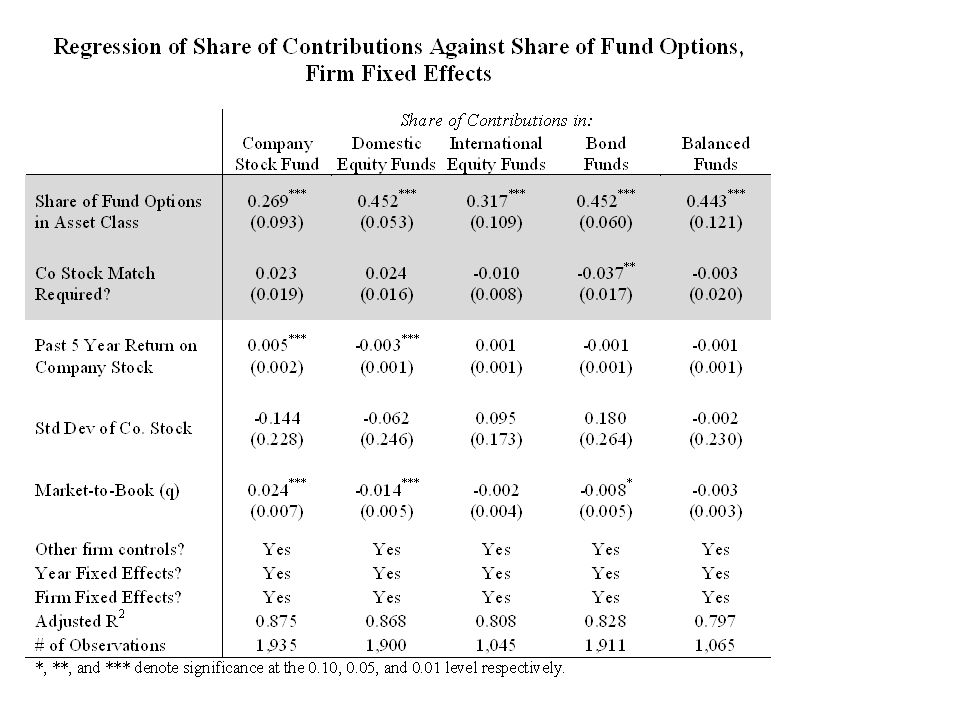

Regression Analysis: Relating Allocation of Contributions to Mix of Options

32

32 Firm-level Heterogeneity Concern with any cross-sectional regression is that correlations obtained may reflect differences across firms in unobserved characteristics (such as risk tolerance of workers) that manifest themselves both in pension plan parameters and participant investment decisions SOLUTION: Exploit the panel data!

that manifest themselves both in pension plan parameters and participant investment decisions SOLUTION: Exploit the panel data!")

34

34 Economic Magnitude Coefficient on share of equity options is 0.45 From 1993 to 2002 the share of equity options in the average 401(k) plan increased from 0.35 (2.0/5.7) to 0.53 (7.4/13.9) This implies that contributions to equity funds increased by 8 percentage points (0.45*0.18) Nearly all of this increase in equity funds was the result of the explosion of actively-managed funds in 401(k) plans

plan increased from 0.35 (2.0/5.7) to 0.53 (7.4/13.9) This implies that contributions to equity funds increased by 8 percentage points (0.45*0.18) Nearly all of this increase in equity funds was the result of the explosion of actively-managed funds in 401(k) plans")

35

35 Interpretation Even after controlling for firm-fixed effects (i.e., relating changes in plan parameters to changes in contributions) the composition of equity and bond funds still “matter” Two Possibilities (Jiang and Huberman, 2006; Benartzi and Thaler, 2001; Holden and Vanderhei, 2001) 1.As number of options increases, each investor more likely to spread assets over greater number of funds 2.Each investor concentrates assets in small number of funds; as increase number of options, likelihood of concentrating investment in any one fund decreases

the composition of equity and bond funds still matter Two Possibilities (Jiang and Huberman, 2006; Benartzi and Thaler, 2001; Holden and Vanderhei, 2001) 1.As number of options increases, each investor more likely to spread assets over greater number of funds 2.Each investor concentrates assets in small number of funds; as increase number of options, likelihood of concentrating investment in any one fund decreases")

36

36 Another Result However, firm-level heterogeneity appears to be important in the context of company stock investment Firms that match with company stock or that offer few investment options may do so because their workers have a preference for company stock Inertia in response to plan parameters may also be important

37

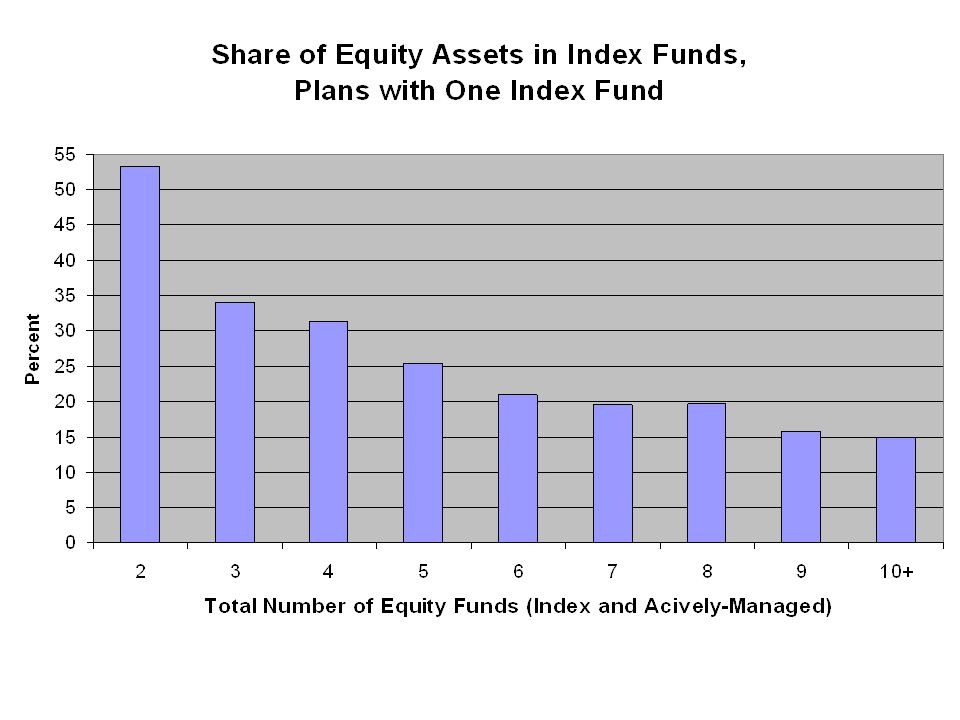

37 Does Type of Equity Mutual Fund Matter for 401(k) Participants? Do participants “find” the index fund offered in the plan (if any)? Or are participants just as likely to contribute to an high-cost actively-managed fund as they are a low-cost index fund?

. Or are participants just as likely to contribute to an high-cost actively-managed fund as they are a low-cost index fund .")

39

EXTENSION: INDEX vs. ACTIVELY- MANAGED FUNDS

40

40 Game Plan Augment contribution-based 11-k data used earlier with data from the 1999-2002 period Link mutual fund names to Morningstar database Examine characteristics (i.e., expenses, fund return, Morningstar percentile ranking) of the equity funds in the 401(k) plan Nearly 18,000 fund-year observations and nearly 4,000 firm-year observations

of the equity funds in the 401(k) plan Nearly 18,000 fund-year observations and nearly 4,000 firm-year observations")

51

51 Does it Matter? Consider a worker who starts at age 22 earning $30,000 per year and experiences 4% nominal annual earnings growth until they retire at age 62. Suppose this worker saves 6% of salary per year in a 401(k) and receives a matching contribution equal to 3% of salary.

and receives a matching contribution equal to 3% of salary..")

52

52 Does it Matter? If this individual earns an 8% nominal net return on their investments, she would have $1.142 million at retirement. If, instead, this individual received nominal annual net returns that were 35 basis points lower than this, or 7.65%, she would receive roughly $80,000 less. In short, due to the power of compounding, a 0.35% per year difference in annual returns accumulates to a nontrivial 7.5% difference in terminal wealth at retirement.

54

54 Bottom-Line Conclusions “Design Matters” – individuals are clearly influenced by the choice set in ways that are not explained by standard models Behavioral response coupled with influx of high- cost actively-managed funds into 401(k) plans leads to worse performance on average (i.e., increasingly harder for participants to find that one index fund)

plans leads to worse performance on average (i.e., increasingly harder for participants to find that one index fund)")

55

55 Plans Sponsors Starting to “Get It”, Gov’t Still “A Step Behind” Roughly 20% of 401(k) plans have the default that you are in the plan (many of these are setting the default to something riskier than the money market fund) Reflects understanding by plan sponsors of the crucial role of plan design and inertia Recent government mandates for pension plans seem to lack this understanding

plans have the default that you are in the plan (many of these are setting the default to something riskier than the money market fund) Reflects understanding by plan sponsors of the crucial role of plan design and inertia Recent government mandates for pension plans seem to lack this understanding")

56

56 Policy Implications of Research Pension Protection Act (2006) Employee contributions to company stock must be immediately diversifiable Employer contributions to company stock must be diversifiable after three years What is likely result of legislation?

Employee contributions to company stock must be immediately diversifiable Employer contributions to company stock must be diversifiable after three years What is likely result of legislation")

57

57 401(k) Fair Disclosure for Retirement Security Act of 2007 Plans that allow workers to control their investments would have to offer at least one market-based index fund What will be the likely result of this legislation if passed?

Fair Disclosure for Retirement Security Act of 2007 Plans that allow workers to control their investments would have to offer at least one market-based index fund What will be the likely result of this legislation if passed")

Similar presentations

Retirement Plan Transamerica Insurance & Investments.>")

OECD/IOPS GLOBAL FORUM ON.>")

contribute a limited yearly.>")