Download presentation

Presentation is loading. Please wait.

1

Mutual Funds and Other Investment Companies

CHAPTER 4 Mutual Funds and Other Investment Companies

2

Table of Contents Mutual funds: Basics Fund fee structures

Type of funds Fund performance Closed funds Exchange-Traded Funds

3

Mutual funds: basics

4

Mutual Funds: Overview

Our goal in this chapter is to understand the different types of mutual funds, their risks, and their returns. Around 1980, 5 million Americans owned mutual funds. However, by 2010, 89 million Americans in 51 million households owned mutual funds. In 2009 investors added $390 billion in net new funds to mutual funds. In 2009, mutual fund assets totaled $11.1 trillion.

5

Ten Largest Mutual Fund Companies By Assets

1 The Vanguard Group $957 Billion 2 American Funds $931.5 Billion 3 Fidelity $717 Billion 4 Barclays Global Investors $287 Billion 5 Franklin Templeton Investments $256.7 Billion 6 Pimco Funds $218.7 Billion 7 T Rowe Price Investments $192.1 Billion 8 State Street Global Investors $176.8 Billion 9 Oppenheimer Funds $129.9 Billion 10 Dodge & Cox $118.2 Billion

6

Ten Largest Mutual Funds By Fund Size

7

U.S. Mutual Funds by Investment Classification

8

Mutual Funds: Overview, Cont.

Mutual funds are simply a means of combining or pooling the funds of a large group of investors to invest in a wide range of securities. You are investing in a portfolio, or basket, of securities. With only $2,000 to invest, you can easily own shares in MSFT, MCD, IBM, and others. The buy and sell decisions for the resulting pool are then made by a fund manager, who is compensated for the service provided. Indirect investing: You have someone else “pick” stocks for you. They are created and marketed to the public in ways that are intended to promote buyer appeal: diversification, “value” and “growth” strategy, large-cap and small-cap strategy, etc. Mutual funds are increasingly important for YOU because soon you will be investing on them through employee pension plan or retirement account.

9

Mutual Funds: Overview, Cont.

Advantages Diversification & divisibility Professional management Administration & record keeping Minimum initial investment – as low as $1,000 or $2,500 Reduced transaction costs Drawbacks Risk – You could “lose” money unlike bank deposits. Costs – Some professional managers charge a hefty fee. Taxes – You will pay federal income tax on distributions (dividends and capital gains made by the fund) and profits you make when you sell mutual funs shares.

and profits you make when you sell mutual funs shares.")

10

Net Asset Value Calculation: Market Value of Assets - Liabilities

Shares Outstanding Investopedia explains Net Asset Value - NAV In the context of mutual funds, NAV per share is computed once a day based on the closing market prices of the securities in the fund's portfolio. All mutual funds' buy and sell orders are processed at the NAV of the trade date. However, investors must wait until the following day to get the trade price. Mutual funds pay out virtually all of their income and capital gains. As a result, changes in NAV are not the best gauge of mutual fund performance, which is best measured by annual total return. Because ETFs and closed-end funds trade like stocks, their shares trade at market value, which can be a dollar value above (trading at a premium) or below (trading at a discount) NAV.

or below (trading at a discount) NAV.")

11

Investment Companies and Fund Types, I

An Investment company is business that specializes in pooling funds from individual investors and making investments. All mutual funds are in fact investment company, but not all investment companies are mutual funds. An Open-end fund is an investment company that stands ready to buy and sell shares in itself to investors, at any time. Issuance: The fund simply issues new shares and then invest the money received. Redemption: The fund sells some of its assets and uses the cash to redeem the shares. As a result, the number of shares outstanding fluctuates through time. More popular. Priced at NAV A Closed-end fund is an investment company with a fixed number of shares that are bought and sold by investors, only in the open market. You must buy (or sell) from (or to) another investor. Listed in stock exchanges just like any other ordinary stocks. Priced at premium or discount to NAV

from (or to) another investor. Listed in stock exchanges just like any other ordinary stocks. Priced at premium or discount to NAV.")

12

Investment Companies and Fund Types, II

13

Mutual Funds Some open-end funds “close their doors” to new investors become a closed-end fund if a fund becomes “too big.” Strictly speaking, the term “mutual fund” actually refers only to an open-end investment company. Therefore, the phrase, “open-end mutual fund” is an unnecessary repetition, or restatement. Investment companies are now generally called mutual funds. Several well-known mutual funds in U.S. include Fidelity, Vanguard, State Street Global Advisor, and others.

14

Information on Mutual Funds

Fund’s prospectus describes: investment objectives Fund investment adviser and portfolio manager Fees and costs Statement of Additional Information (SAI) Fund’s annual report Some web sites Wiesenberger’s Investment Companies Morningstar ( Yahoo (biz.yahoo.com/funds) Investment Company Institute ( Directory of Mutual Funds

Fund’s annual report. Some web sites. Wiesenberger’s Investment Companies. Morningstar ( Yahoo (biz.yahoo.com/funds) Investment Company Institute ( Directory of Mutual Funds.")

17

Net Asset Value (NAV) Market Value of Assets - Liabilities

Net asset value (NAV) is equal to Mutual fund calculates the NAV at the end of each trading day. All buy or sell order arriving during the day are executed at that NAV following the market close. NAV changes every day because the value of the assets held by the fund changes every day. Notice that this measure of the rate of return ignores any commissions such as front-end loads paid to purchase the fund. Shares in an open-end fund are worth their NAV, because the fund stands ready to redeem their shares at any time. In contrast, share value of closed-end funds may differ from their NAV. Market Value of Assets - Liabilities Shares Outstanding

is equal to. Mutual fund calculates the NAV at the end of each trading day. All buy or sell order arriving during the day are executed at that NAV following the market close. NAV changes every day because the value of the assets held by the fund changes every day. Notice that this measure of the rate of return ignores any commissions such as front-end loads paid to purchase the fund. Shares in an open-end fund are worth their NAV, because the fund stands ready to redeem their shares at any time. In contrast, share value of closed-end funds may differ from their NAV. Market Value of Assets - Liabilities. Shares Outstanding.")

18

Fees and Mutual Fund Returns: An Example

Initial NAV = $20 Income distributions of $.15 Capital gain distributions of $.05 Ending NAV = $20.10:

19

Mutual Fund Operations Organization and Creation

A mutual fund is simply a corporation. It is owned by shareholders, who elect a board of directors. Most mutual funds are created by investment advisory firms (say Fidelity Investments), or brokerage firms with investment advisory operations (say Merrill Lynch or Charles Schwab). Investment advisory firms earn fees for managing mutual funds. Although mutual funds often belong to a large “family” of funds, every fund is a separate company owned by its shareholders. In theory, the directors of a mutual fund in a particular family, acting on behalf of the fund shareholders, could vote to fire the investment advisory firm and hire a different one, but in reality, this rarely occurs.

, or brokerage firms with investment advisory operations (say Merrill Lynch or Charles Schwab). Investment advisory firms earn fees for managing mutual funds. Although mutual funds often belong to a large family of funds, every fund is a separate company owned by its shareholders. In theory, the directors of a mutual fund in a particular family, acting on behalf of the fund shareholders, could vote to fire the investment advisory firm and hire a different one, but in reality, this rarely occurs.")

20

Mutual Fund Operations Taxation of Investment Companies, I

A “regulated investment company” does not have to pay taxes on its investment income. Instead, the fund passes through all realized investment income to fund shareholders, who then pay taxes on these distributions as though they owned the securities directly. That is, taxes are paid only by the investor The pass-through feature is an important disadvantage of owning mutual fund because investors cannot time capital gains/losses to efficiently manage tax liabilities.

21

Mutual Fund Operations Taxation of Investment Companies, II

To qualify, an investment company must: Hold almost all its assets as investments in stocks, bonds, and other securities, Use no more than 5% of its assets when acquiring a particular security (diversification rule), and Pass through all realized investment income to fund shareholders High portfolio turnover leads to tax inefficiency Average turnover = 60%

, and. Pass through all realized investment income to fund shareholders. High portfolio turnover leads to tax inefficiency. Average turnover = 60%")

22

Mutual Fund Operations The Fund Prospectus and Annual Report

Mutual funds are required by law to supply a prospectus to any investor who wishes to purchase shares. Prospectus contains investment objectives, investment strategy, fee and expenses, performance information and others. Mutual funds must also provide an annual report to their shareholders.

23

Fund fee structure

24

Mutual Fund Costs and Fees Expense Reporting

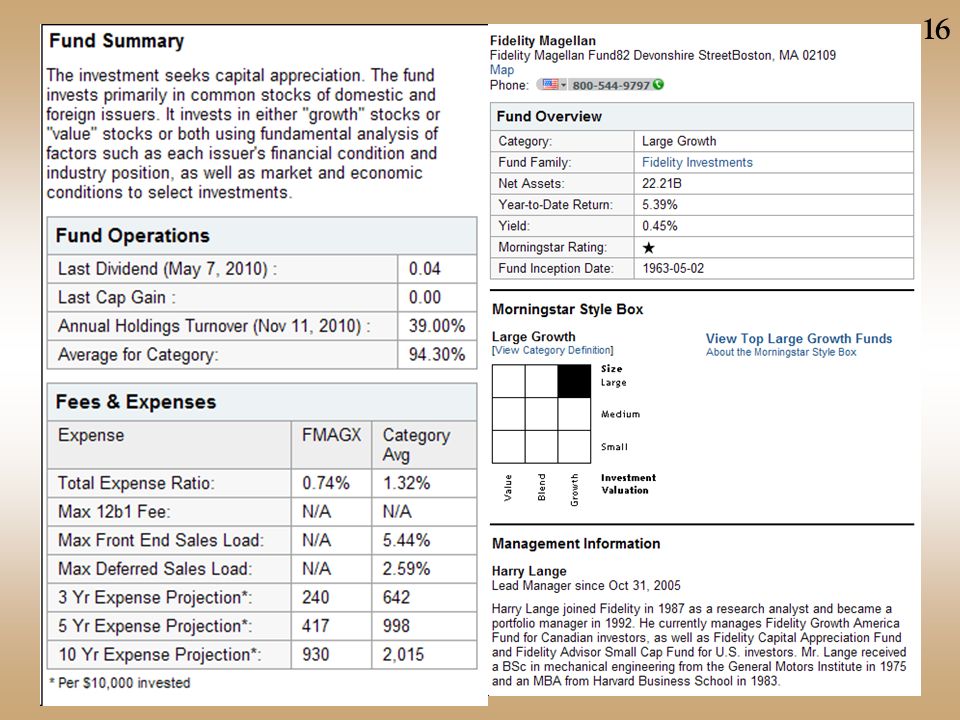

Mutual funds are required to report expenses in a fairly standardized way in their prospectus. Shareholder transaction expenses - loads and deferred sales charges. Fund operating expenses - management and 12b-1 fees, legal, accounting, and reporting costs, director fees. Hypothetical example showing the total expenses paid by investors through time per $10,000 invested.

25

Mutual Fund Costs and Fees Types of Expenses and Fees

Sales charges or “loads” Front-end loads are charges levied on purchases. Back-end loads are charges levied on redemptions. Load in $ = offering price – NAV, or load in % = load in $ / offering price Vary from 2% to 9%, on average, 5% is typical. Why pay load when there are plenty of no-load fund available? 12b-1 fees. SEC Rule 12b-1 allows funds to spend up to 1% of fund assets annually to cover distribution and marketing costs. Management fees Usually range from 0.25% to 1.00% of the fund’s total assets each year. Are usually based on fund size and/or performance. Trading costs Not reported directly Funds must report "turnover," which is related to the amount of trading. The higher the turnover, the more trading has occurred in the fund. The more trading, the higher the trading costs.

26

Costs of Investing in Mutual Funds

Fee Structure: Operating expenses Front-end load Back-end load 12 b-1 charge Fees must be disclosed in the prospectus Share classes with different fee combinations

27

An Example of Front-End Loads

28

Fees for Various Classes

29

An Example of Turnover

30

Expense Ratio The expense ratio is the annual fee that all funds or ETFs charge their shareholders. It expresses the percentage of assets deducted each fiscal year, including 12b-1 fees, management fees, administrative fees, operating costs, and all other asset based costs incurred by the fund. Trading costs including brokerage costs, as well as initial or deferred sales charges are not included in the expense ratio. If the fund's assets are small, its expense ratio can be quite high. Conversely, as the net assets of the fund grow, the expense percentage should ideally diminish as expenses are spread across the wider asset base.

31

Example: Fee Table

32

Mutual Fund Costs and Fees Why Pay Loads and Fees?

After all, many good no-load funds exist. But, you may want a fund run by a particular manager. Then, those funds you want may be load funds. Or, you may want a specialized type of fund. Perhaps one that specialized in Italian companies Loads and fees for specialized funds tend to be higher, because there is little competition among them.

33

Impacts of Costs on Investment Performance

34

How Funds Are Sold Direct-marketed funds Sales force distributed

Revenue sharing on sales force distributed Potential conflicts of interest Financial Supermarkets

35

Types of funds

36

Short-Term Funds Short-term funds are collectively known as money market mutual funds. Money market mutual funds (MMMFs) are mutual funds specializing in money market instruments. MMMFs maintain a $1.00 net asset value to make them resemble bank accounts. Depending on the type of securities purchased, MMMFs can be either taxable or tax-exempt. Most banks offer what are called “money market” deposit accounts, or MMDAs, which are much like MMMFs. The distinction is that a bank money market account is a bank deposit and offers FDIC protection.

are mutual funds specializing in money market instruments. MMMFs maintain a $1.00 net asset value to make them resemble bank accounts. Depending on the type of securities purchased, MMMFs can be either taxable or tax-exempt. Most banks offer what are called money market deposit accounts, or MMDAs, which are much like MMMFs. The distinction is that a bank money market account is a bank deposit and offers FDIC protection.")

37

Long-Term Funds There are many different types of long-term funds, i.e., funds that invest in long-term securities. Historically, mutual funds were classified as stock funds, bond funds, or income funds. Today, the investment objective of the fund is the major determinant of the fund type.

38

Stock Funds, I Some stock funds trade off capital appreciation and dividend income. Capital appreciation Growth Growth and Income Equity income Some stock funds focus on companies in a particular size range. Small company Mid-cap Large-cap Some stock funds invest in different parts of the world. Global : includes world plus U.S. International: includes world but no U.S. Regional Country Emerging markets

39

Stock Funds, II Sector funds specialize in specific sectors of the economy, such as: Biotechnology Internet Energy Other fund types include: Index funds: very important Social conscience, or “green,” funds “Sin” funds (i.e., tobacco, liquor, gaming) Tax-managed funds

Tax-managed funds.")

40

Bond Funds Bond funds may be distinguished by their

Maturity range Credit quality Taxability Bond type Issuing country Bond fund types include: Short-term and intermediate-term funds General funds High-yield funds Mortgage funds World funds Insured funds Single-state municipal funds

41

Stock and Bond Funds Funds that do not invest exclusively in either stocks or bonds are often called “blended” or “hybrid” funds. Examples include: Balanced funds Asset allocation funds Convertible funds Income funds

42

U.S. Mutual Funds by Investment Classification

42

43

Mutual Fund Objectives: Recent Developments, I

A mutual fund “style” box is a way of visually representing a fund’s investment focus by placing the fund into one of nine boxes: Growth Blend Value Large Medium Small Size Style

44

Mutual Fund Objectives: Recent Developments, II

In recent years, there has been a trend toward classifying a mutual fund’s objective based on its actual holdings. For example, the Wall Street Journal classifies most general purpose funds based on the market “cap” of the stocks they hold, and also on whether the fund tends to invest in “growth” or “value” stocks (or both).

.")

45

P/E Ratio

46

Value versus Growth, I Growth-oriented investor will:

focus on EPS (i.e., the denominator) and its economic determinants look for companies expected to have rapid EPS growth in the future assumes constant P/E ratio over the near term, meaning that the stock price will rise as forecasted earnings growth is realized.

and its economic determinants. look for companies expected to have rapid EPS growth in the future. assumes constant P/E ratio over the near term, meaning that the stock price will rise as forecasted earnings growth is realized.")

47

Value versus Growth, II Value-oriented investor will:

focus on the price component (i.e., the numerator). assume that the current stock price is low or stock is “cheap.” not care much about current earnings assume the P/E ratio is below its natural level and that the market will soon “correct” this situation by increasing the stock price with little or no change in earnings.

. assume that the current stock price is low or stock is cheap. not care much about current earnings. assume the P/E ratio is below its natural level and that the market will soon correct this situation by increasing the stock price with little or no change in earnings.")

48

Sometimes, value wins. Sometimes, growth wins.

49

A growth strategy is riskier.

50

Mutual Fund Objectives

51

Mutual Fund Selection (www.morningstar.com)

52

Fund performance

53

Mutual Fund Performance

Mutual fund performance is very closely tracked by a number of organizations. Financial publications of all types periodically provide mutual fund data. The Wall Street Journal is particularly timely print source. has a “Fund Selector” that provides performance information

54

Mutual Fund Performance: Yardsticks

55

Mutual Fund Performance: Online Version of The Wall Street Journal, I.

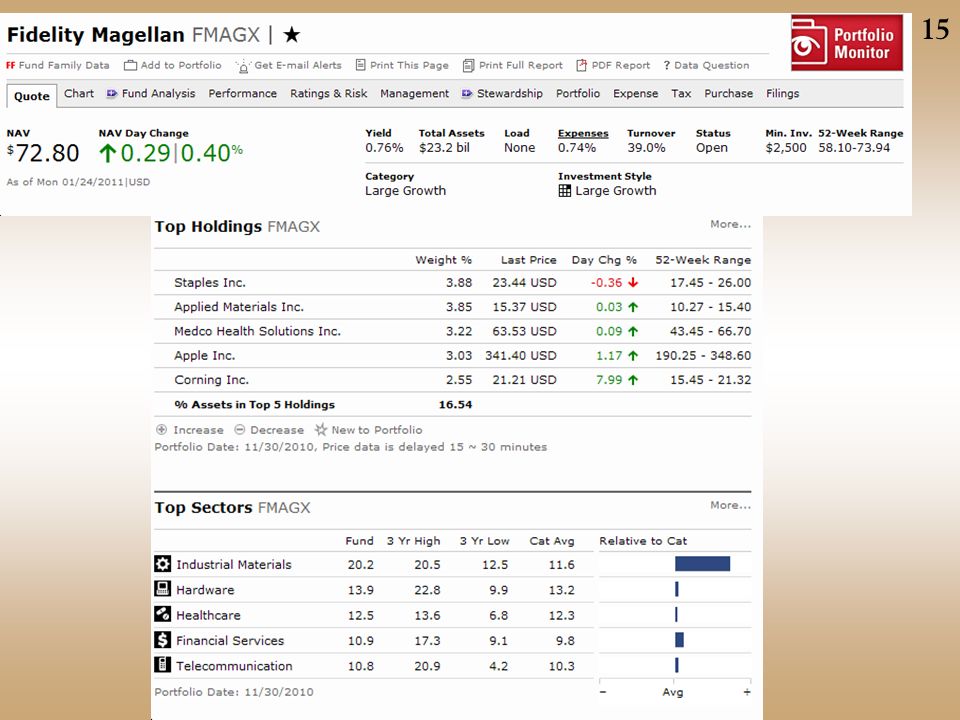

Note the fund with symbol: FBGRX Mutual fund ticker symbols are usually alphanumeric and end with the letter X to differentiate them from stock symbols.

56

Mutual Fund Performance: Online Version of The Wall Street Journal, II

Result of clicking on “BluCh”

57

Mutual Fund Investment Performance: A First Look

A question: How does the performance of actively managed fund compare to the performance of a passively managed fund that replicates the composition of a broad index? Wilshire 5000 index holds essentially all actively traded stocks in U.S. Vanguard Total stock Market Portfolio is an replication of Wilshire 5000. Performance of actively managed funds: Below the return on the Wilshire index in 25 of the 41 years from 1971 to 2011 Evidence for persistent superior performance (due to skill and not just good luck) is weak, but suggestive Bad performance is more likely to persist

is weak, but suggestive. Bad performance is more likely to persist.")

58

Diversified Equity Funds versus Wilshire 5000 Index

59

Consistency of Investment Results

60

Mutual Fund Performance: Cautions

While looking at historical returns, the riskiness of the various fund categories should also be considered. Whether historical performance is useful in predicting future performance is a subject of ongoing debate. Some of the poorest-performing funds are those with very high costs. Ratings by reputable research firm such as Morningstar are as good indicator for the future performance as anyone’s guess.

61

Closed funds

62

Closed Funds Sometimes a fund will choose to close.

This means that the fund will no longer sell shares to new investors. The use of the word “close” here should not be confused with “closed-end.” The number of shares in a closed fund can still fluctuate as existing owners buy and sell. Why would a fund choose to close? When a fund grows rapidly, the fund manager may feel that the incoming cash is more than the fund can invest profitably. Funds that close often reopen at a later date.

63

Closed-End Funds A closed-end fund has a fixed number of shares.

These shares are traded on stock exchanges. There are about 600 closed-end funds that have their shares listed on U.S. Stock Exchanges. There are about 8,000 long-term open-end mutual funds.

64

Mutual Fund Performance: Closed-End Funds

65

The Closed-End Funds Discount

Most closed-end funds sell at a discount relative to their net asset values. The discount is sometimes substantial. The typical discount fluctuates over time. Example: Suppose a closed-end fund owns $100 million worth of stocks. It has 10 million shares outstanding, so the NAV is clearly $10. However, the share is sold at, say, $9. (9-10)/10 = -10% Despite a great deal of academic research, the closed-end fund discount phenomenon remains largely unexplained.

/10 = -10% Despite a great deal of academic research, the closed-end fund discount phenomenon remains largely unexplained.")

66

etfs

67

Exchange Traded Funds, ETFs

An exchange traded fund, or ETF, A relatively recent innovation – since 1993. Is basically an index fund but it is not a mutual fund. Trades like a closed-end fund (without the discount phenomenon). An area where ETFs seem to have an edge over the more traditional index funds is the more specialized indexes. A well-known ETF is the “Standard and Poor’s Depositary Receipt” or SPDR. This ETF mimics the S&P 500 index. It is commonly called “spider." Another well-known ETF mimics the Dow Jones—it is called "Diamond.“ A list of ETFs can be found at SPY, DIA, QQQQ, VNQ, EWZ, EFA, FXI, and others Major sponsors include Barclays Global Investors, State Street Global Advisor, PowerShares, Vanguard, and others.

. An area where ETFs seem to have an edge over the more traditional index funds is the more specialized indexes. A well-known ETF is the Standard and Poor’s Depositary Receipt or SPDR. This ETF mimics the S&P 500 index. It is commonly called spider. Another well-known ETF mimics the Dow Jones—it is called Diamond. A list of ETFs can be found at SPY, DIA, QQQQ, VNQ, EWZ, EFA, FXI, and others. Major sponsors include Barclays Global Investors, State Street Global Advisor, PowerShares, Vanguard, and others.")

68

ETFs Creation An ETF sponsors files a plan with the SEC.

Arranges to set aside the shares representing the basket of securities that forms the ETF index. These few million shares are placed into a trust. Create an unit shares that represent claims on the bundles of shares held in the trust. These unit shares are then traded in exchanges.

69

ETFs Characteristics ETF is like an index fund but not exactly a mutual fund because Advantage Can be sold short or purchased on margin It can have options. Can be bought and sold continuously during the day like stocks or closed-end funds. Generally have very low expense: .10% or one-tenth of 1 percent. Tax efficient Disadvantage Prices can depart by small amounts from NAV Must be purchased from a broker. Must pay a commission.

70

Growth of U.S. ETFs over time

71

Growth of U.S. ETFs over Time

72

Investment Company Assets Under Management, 2011 ($ Billion)

")

73

ETF Sponsors and Products

74

Exchange Traded Funds, Performance

75

Hedge Funds Like mutual funds, hedge funds collect pools of money from investors. Some funds are limited to no more than “high net worth investors.” Traditionally, hedge funds were only lightly regulated. Despite protests from the hedge fund industry, the SEC recently initiated some regulations. Like mutual funds, hedge funds are generally required to register with the SEC. But: Hedge funds are not required to maintain any particular degree of diversification or liquidity. Hedge fund managers have considerably more freedom to follow various investment strategies, or styles. Hedge fund fees: General management fee of 1-2% of fund assets Excessive performance fee of 20-40% of profits

76

Information on Mutual Funds

Morningstar ( Yahoo (biz.yahoo.com/funds) Investment Company Institute ( Directory of Mutual Funds

Investment Company Institute ( Directory of Mutual Funds.")

Similar presentations

>")