Download presentation

Presentation is loading. Please wait.

1

http://standarderrors.org/Presentations/STTI2006Bradley&Cox.ppt Q:\Current\Prf\Present\STTI2006\Bradley&Cox.ppt

2

http://standarderrors.org/Presentations/STTI2006Bradley&Cox.ppt Managing Financial and Clinical Risk: Risk Theory and Operations Research for Nurse Administrators Sharon L. Bradley MSN, RN Spokane VA Medical Center, Spokane, WA, USA Thomas Cox, PhD, RN Gainesville, FL, USA Sigma Theta Tau International 17 th International Nursing Research Conference Focusing on Evidence Based Practice

3

http://standarderrors.org/Presentations/STTI2006Bradley&Cox.ppt Author Backgrounds Sharon Bradley Nursing Nursing Management Clinical Informatics Quality Improvement Thomas Cox PhD, RN Nursing Mathematics/Statistics Insurance

4

http://standarderrors.org/Presentations/STTI2006Bradley&Cox.ppt Improve the decision-making capabilities of nurse managers and executives Improve nurses’ awareness of and ability to deal with uncertain information in a straightforward and natural way, to achieve: More cogent analysis of HC financing relationships Improve service planning More anticipation & better responses to uncertainty Greater situational awareness Better assessment of available options Better nursing decision making processes will enable greater productivity from people, supplies, equipment, physical plant, machines in less time and with lower costs. General Objective

5

http://standarderrors.org/Presentations/STTI2006Bradley&Cox.ppt Learner Objectives Learner Objective #1: The learner will be able to describe financial and clinical risks that occur in nursing environments due to insurance risk assumption occurring with managed care, capitation, DRGs and budgeted nursing services. Learner Objective #2: The learner will be able to use tools derived from risk theory and operations research to improve their management of clinical and financial risks in nursing environments.

6

http://standarderrors.org/Presentations/STTI2006Bradley&Cox.ppt Background 1 The size, location, organizational placement, and financial strength of service units impact their ability to manage uncertain revenue streams resulting from managed care, capitation, prospective payment systems, and retrospective audits Uncertainty constrains capacity and may unfairly affect clinical and financial evaluations of small service units and their managers while these entities have little control over contracting and operations Unfair performance evaluations of personnel and units may further exacerbate these issues, leading managers and employees to overreact, further and further constrain services, and exacerbating disparities in access to or availability of much needed healthcare service capacities

7

http://standarderrors.org/Presentations/STTI2006Bradley&Cox.ppt Background 2 Pre-paid services constitute insurance risk transfers to health providers, a critical issue rarely discussed by nurse managers and nurse executives Understanding insurer pricing and risk management activities is critical if nurse managers and nurse executives are to participate in managing 21 st century health care environments

8

http://standarderrors.org/Presentations/STTI2006Bradley&Cox.ppt Insurance Pricing 1 Prospective payments to health care providers tend to be either inadequate or inefficient Insurers price their services by charging rates adequate to cover four principal components: Expected losses + loss adjustment expenses Non-loss related operating expenses Profits – Anticipated returns on equity adequate to retain old/attract new investments Risk loads adequate to cover unanticipated deviations from expected loss and loss adjustment costs based on each individual insurer’s surplus resources

9

http://standarderrors.org/Presentations/STTI2006Bradley&Cox.ppt Insurance Pricing 2 Insurers seek profitable operations consistent with long term financial solvency (P[Insolvency] < 0.001). Large insurers write more policies and hold more surplus (U/W capacity) than smaller insurers: Large insurers have more surplus (capacity): Better management of fluctuations in losses Lower loss loads to maintain solvency Lower risk loads more price competitive compared with smaller insurers Health care providers assuming insurance risks are inefficient insurers and should charge more, not less, than an efficient insurer, to fund identical services

![Insurance Pricing 2 Insurers seek profitable operations consistent with long term financial solvency (P[Insolvency] < 0.001).](http://images.slideplayer.com/27/9150148/slides/slide_9.jpg "Large insurers write more policies and hold more surplus (U/W capacity) than smaller insurers: Large insurers have more surplus (capacity): Better management of fluctuations in losses Lower loss loads to maintain solvency Lower risk loads more price competitive compared with smaller insurers Health care providers assuming insurance risks are inefficient insurers and should charge more, not less, than an efficient insurer, to fund identical services.")

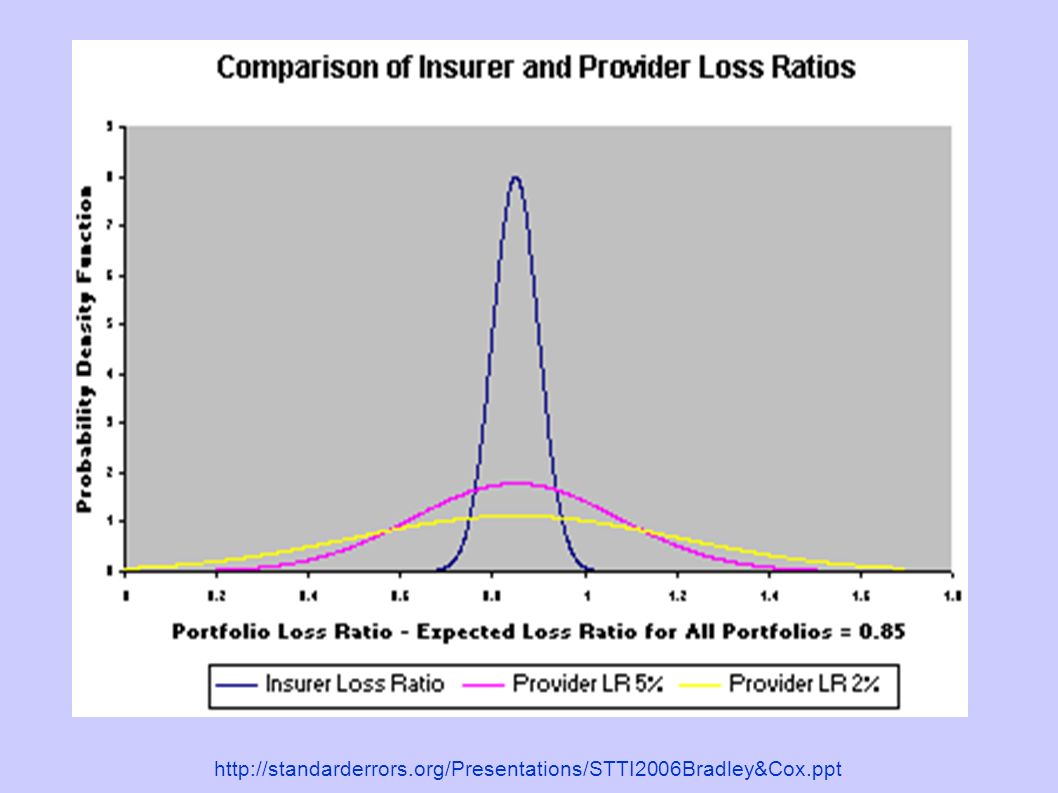

10

http://standarderrors.org/Presentations/STTI2006Bradley&Cox.ppt Insurance Pricing 3 For emphasis: In a perfectly efficient health care system, insurance risk transferring mechanisms (Managed Care, DRGs, Prospective Payment Systems) inefficiently or inadequately compensate health care providers compared to equally large, risk retaining, indemnity insurers The loss in insurance efficiency necessitates lower levels of service delivery – less care for the same cost – then is possible when insurers retain insurance risks

inefficiently or inadequately compensate health care providers compared to equally large, risk retaining, indemnity insurers The loss in insurance efficiency necessitates lower levels of service delivery – less care for the same cost – then is possible when insurers retain insurance risks")

11

http://standarderrors.org/Presentations/STTI2006Bradley&Cox.ppt

12

Professional Caregiver Insurance Risk 1 PCIR occurs when HCPs accept insurance risks in prospective payment systems, leading to: Portfolio size differential inefficiencies Higher conflagration risk exposures for HCPs Inadequate or inefficient payments Lack of access to internal/external fiscal resources Impacts of viscous resource transfers in moving assets between units, locations, and patients Violations of basic insurance principles Greater difficulties managing nursing environments

13

http://standarderrors.org/Presentations/STTI2006Bradley&Cox.ppt Professional Caregiver Insurance Risk 2 The Central Limit Theorem explains how insurer risk aggregation and retention reduces overall risk for insurers and policyholders – but insurance risk disaggregating eliminates the benefits of insurance and increases financial and clinical risks for providers and consumers No combination of increased management expertise and HC system efficiencies will compensate for the inefficiencies introduced by transferring insurance risks to HCPs, but…

14

http://standarderrors.org/Presentations/STTI2006Bradley&Cox.ppt Challenges and Implications Assumed insurance risks create new challenges Insurer inefficiencies result from: Small portfolio sizes Local conflagration risks (epidemics & natural disasters), Multiple confusing contractual relationships Variations in payment Adequacy Timing Dependability Nurses may mitigate but not overcome these effects with planning, cost analyses, using insurer’s pricing methods and better defining and articulating resource redundancy needs

, Multiple confusing contractual relationships Variations in payment Adequacy Timing Dependability Nurses may mitigate but not overcome these effects with planning, cost analyses, using insurer’s pricing methods and better defining and articulating resource redundancy needs")

15

http://standarderrors.org/Presentations/STTI2006Bradley&Cox.ppt Actuarial and Decision-Making Needs Probability theory, decision theory & utility theory Reducing the impact of missing information Improved efficiency in allocating time, supplies, personnel, equipment, and space Identify/Distinguish certain from uncertain information Better analytical, planning, and evaluation activities Framing problems for optimal understanding by nurses, managers, and executive decision makers Real time analysis, implementation, and evaluation of strategies for uncertainty management Automate analyses, decisions & implementations

16

http://standarderrors.org/Presentations/STTI2006Bradley&Cox.ppt Nurse Decision Makers Needs Forecasting staff, supply & equipment needs/supply Loss analysis: frequency, severity, loss development, Trends in specific contracts and involving specific units Monitor shifts and trends in costs and reimbursements on managed care and capitation contracts, and first and third party payers Optimal, real time, resource allocations practices Matching and discounting uncertain costs and revenues Risk compensated PCIR pricing Solvency and disaster preparedness

17

http://standarderrors.org/Presentations/STTI2006Bradley&Cox.ppt Actuarial and Decision Making Tools Time series analysis – trending costs to future levels Loss development analysis – ultimate costs Claim frequency and severity distribution models Operations Research/Linear Programming – resource optimization & portfolio management tools Theory of interest and time value of money Insurance pricing vs. manufacturing pricing models Reserving, redundancy planning, and liquidity preservation Insurer regulatory financial reporting forms and procedures

18

http://standarderrors.org/Presentations/STTI2006Bradley&Cox.ppt Summary Nurse executives/managers play critical roles in mediating institutional insurance risk assumption at bedside Risk theory, forecasting, game theory, and quantitative decision making tools enable managers and executives to improve their planning processes & optimize service quantity/quality with fixed constraints Identifying & managing inadequate reimbursements & higher than expected resources & services is critical Nurses using actuarial tools, statistical sampling theory, and game theory can analyze past/project future costs and needs, improving their decision making, contracting and budgeting activities, and resource management Better analyses and decisions will contribute to improved evaluations of staff and programs

19

http://standarderrors.org/Presentations/STTI2006Bradley&Cox.ppt References Cox, T. (2006). Professional Caregiver Insurance Risk: A Brief Primer for Nurse Executives and Decision-Makers. Nurse Leader, 4(2): 48-51. Cox, T. (2001). Risk theory, reinsurance, and capitation. Issues in Interdisciplinary Care, 3(3): 213- 218.

. Professional Caregiver Insurance Risk: A Brief Primer for Nurse Executives and Decision-Makers. Nurse Leader, 4(2): Cox, T. (2001). Risk theory, reinsurance, and capitation. Issues in Interdisciplinary Care, 3(3):")

20

http://standarderrors.org/Presentations/STTI2006Bradley&Cox.ppt More Information http://drtcbear.servebbs.net:81/PCIR

Similar presentations

Seminar on Ratemaking Nashville, TNRuss Bingham March 11-12, 1999Hartford Financial Services.>")

. Key Concepts Managerial Cognition Business Model Stakeholders The Balanced Scorecard.>")