Download presentation

Presentation is loading. Please wait.

1

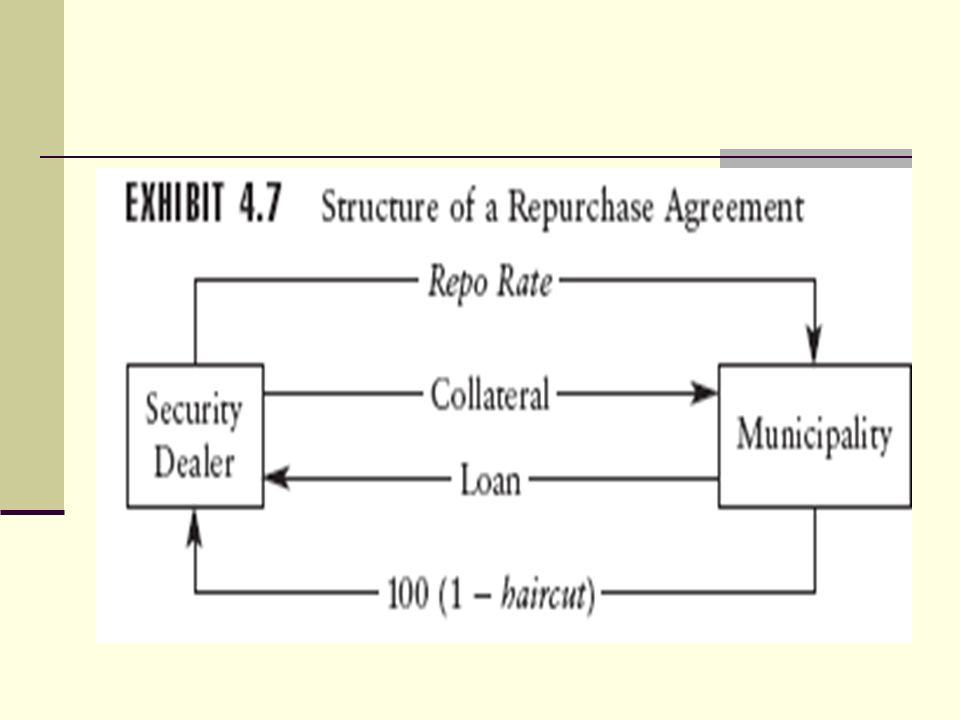

Repo rate 1. A Namura security dealer, who just purchased 3-month U.S. treasury security at the government weekly auction at $98.65, finances the purchase by selling the 3- month T-bill over a week at $98.65 and agrees to buy back the security at $98.75 per $100 face value. 2. What is the implied repo rate? What is the dealer’s profit (loss) on a $10 million Treasury purchase and financing in the above scenario?

on a $10 million Treasury purchase and financing in the above scenario .")

2

Example A hedge fund is contemplating an arbitrage opportunities for the on-the-run 30-year and off- the-run 29 ½ -year treasury securities respectively quoted to yield 5 ¼ and 5.31 percent. The hedge fund believes that the rates on the two securities will converge in 6 months. What types of trade the hedge fund undertakes to take advantage of mispricing? Suppose repo rates on borrowing (the repo rate paid) is 5.26 and in lending (the repo rate received) is 5.29 percent, is there an arbitrage profit?

is 5.26 and in lending (the repo rate received) is 5.29 percent, is there an arbitrage profit .")

4

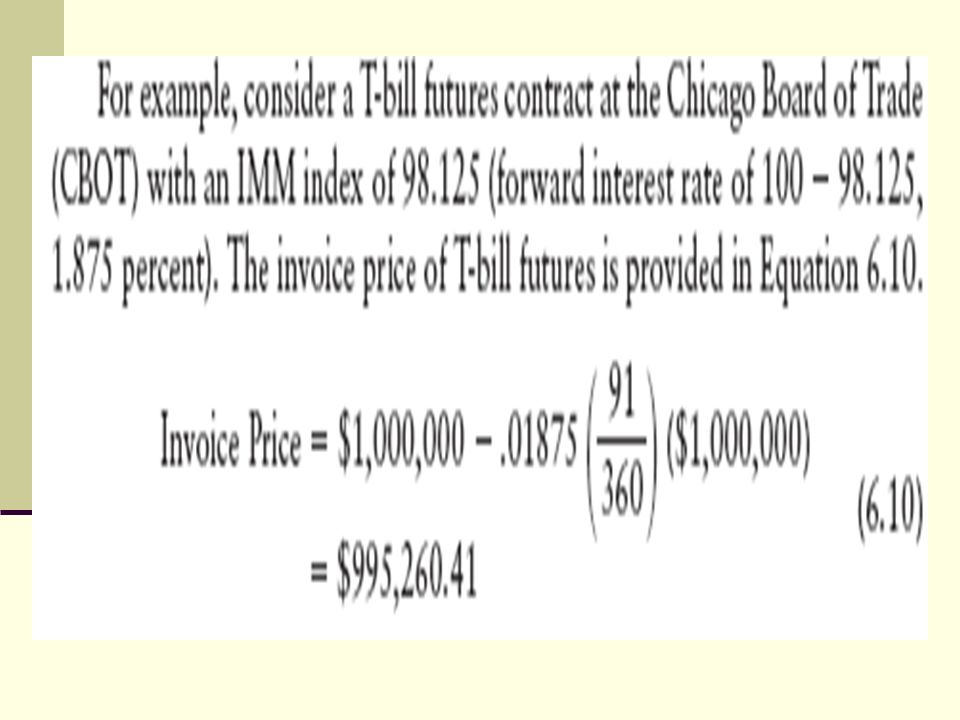

Treasury Futures Price = Face value - Discount Discount = f * t* F where f forward interest rate t time to expiration in year F face value of the futures as seen above

8

Example

9

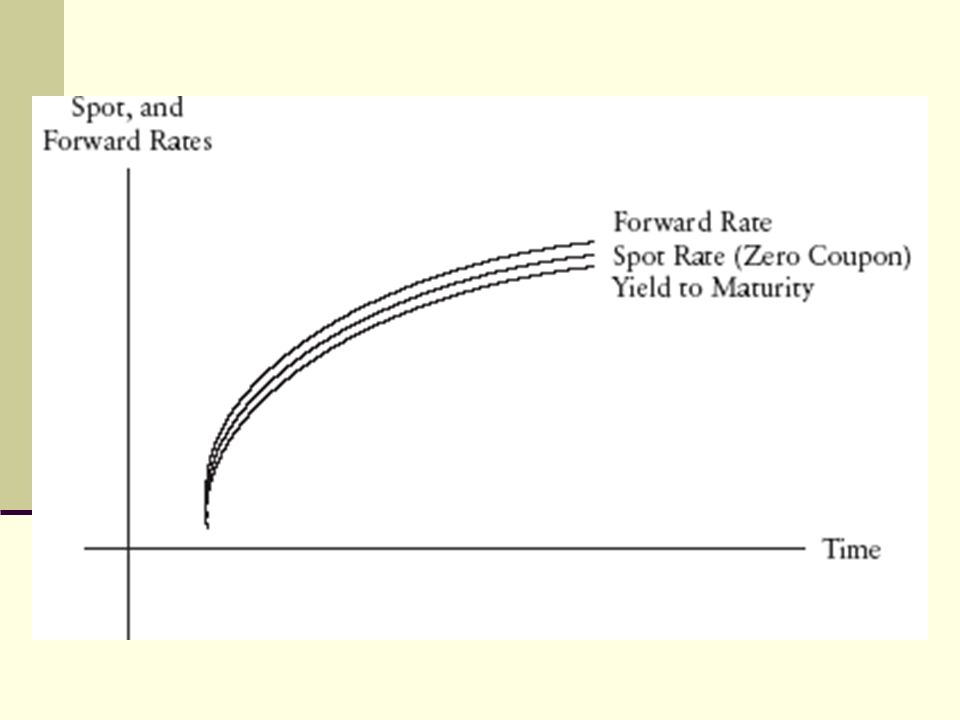

Zero Arbitrage Scenario Example: Consider an individual with a two-year investment horizon who is endowed with $5,000. This individual can invest in a two-year bond, or in two 1-year bonds. Option 1: Invest $5,000 in a two-year bond, $5,000 (1.055)2 $5,565.125 Option 2: Invest $5,000 in a one-year bond and at maturity roll over to another one-year bond at the forward rate of f (1,2) that is expected to prevail between years 1 and 2.

2 $5, Option 2: Invest $5,000 in a one-year bond and at maturity roll over to another one-year bond at the forward rate of f (1,2) that is expected to prevail between years 1 and 2..")

11

Measuring and Managing exposure

12

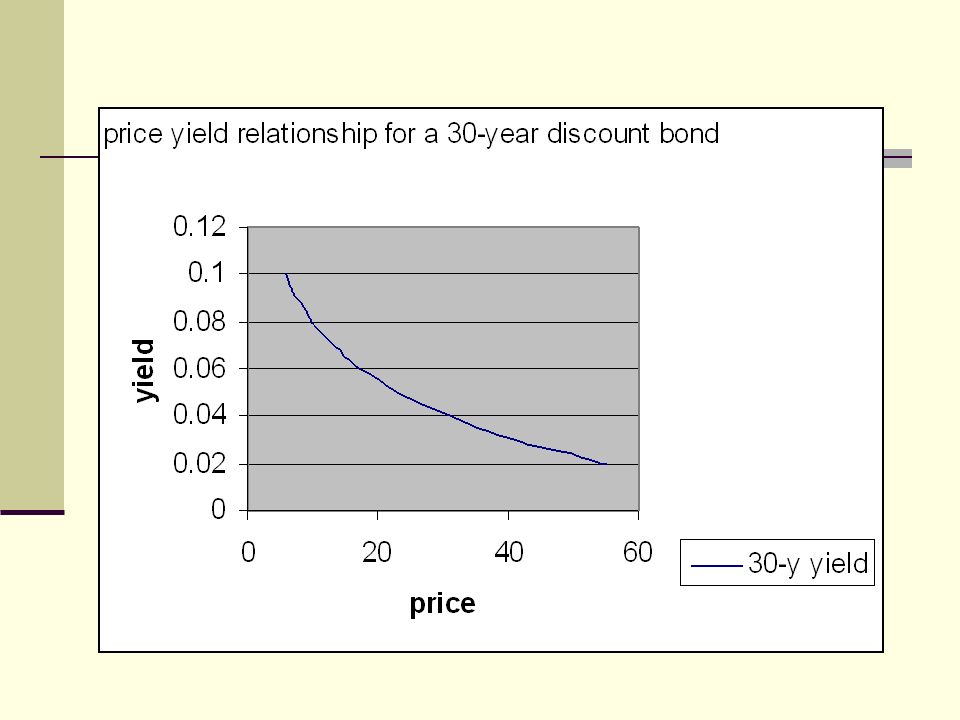

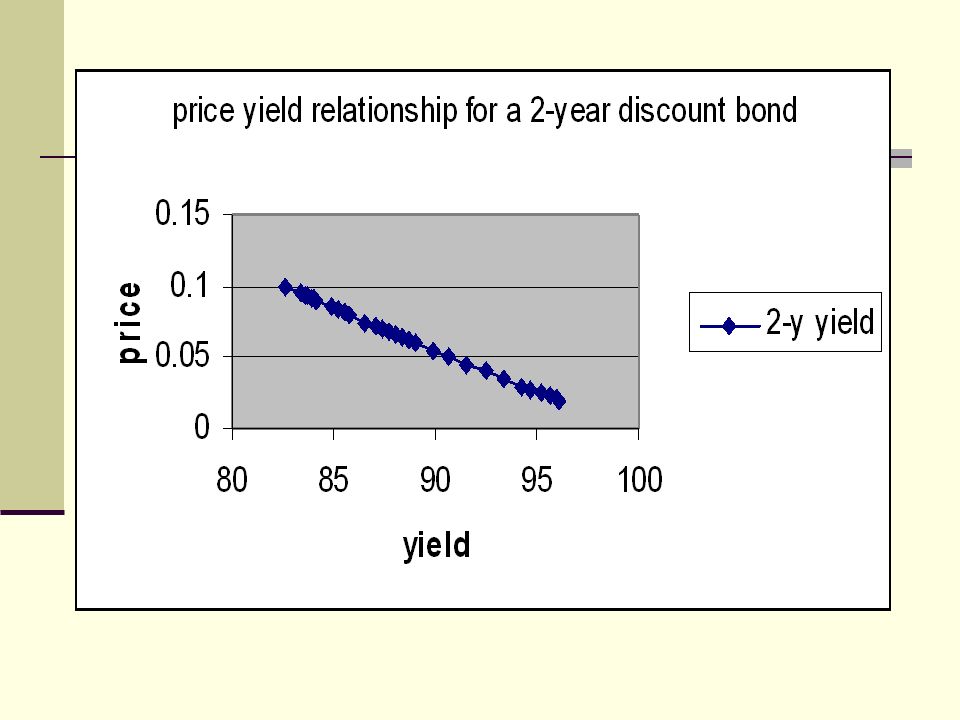

DVO1

15

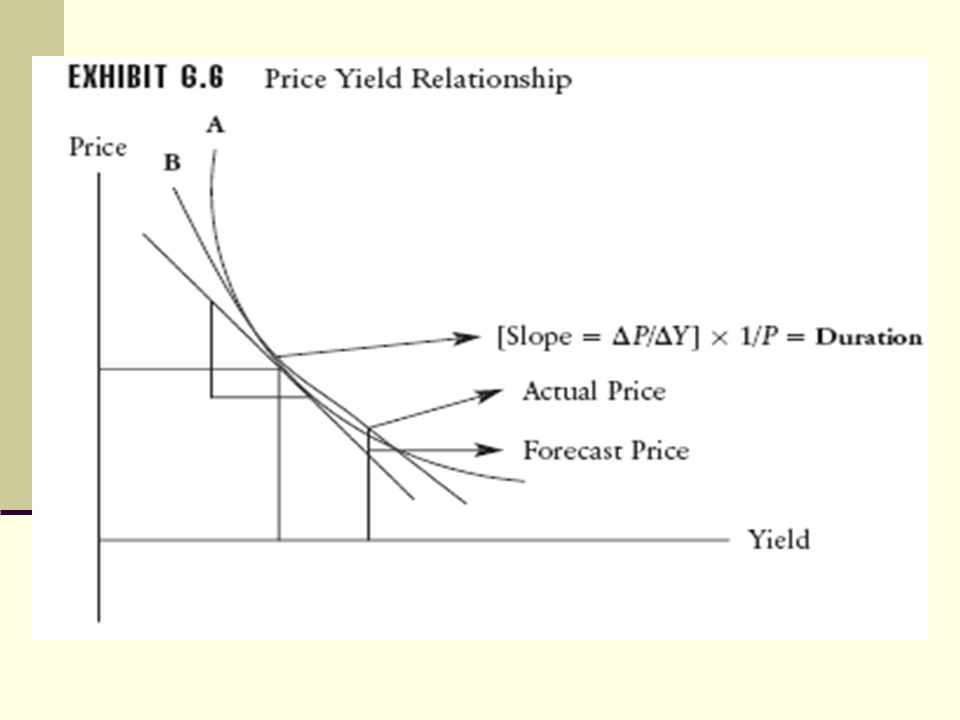

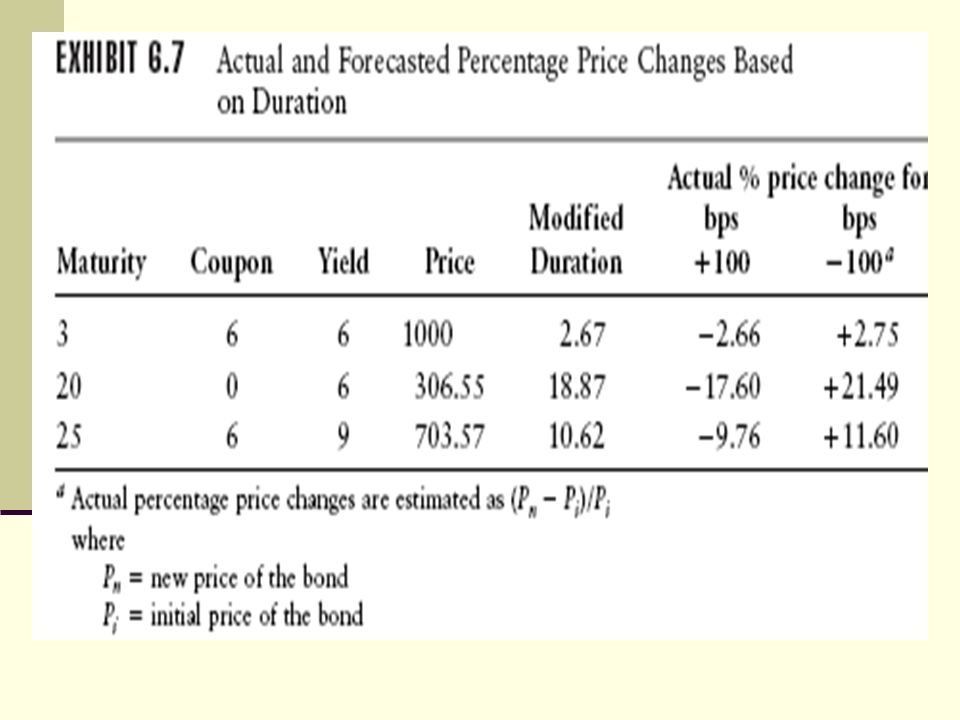

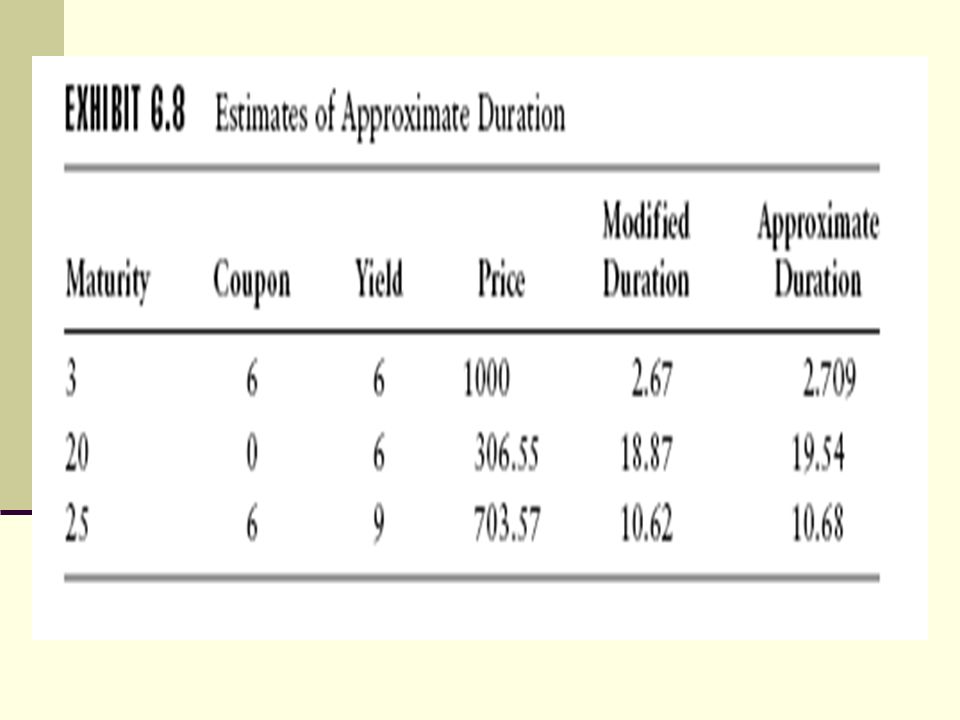

Duration & Convexity

16

Convexity

17

Example

18

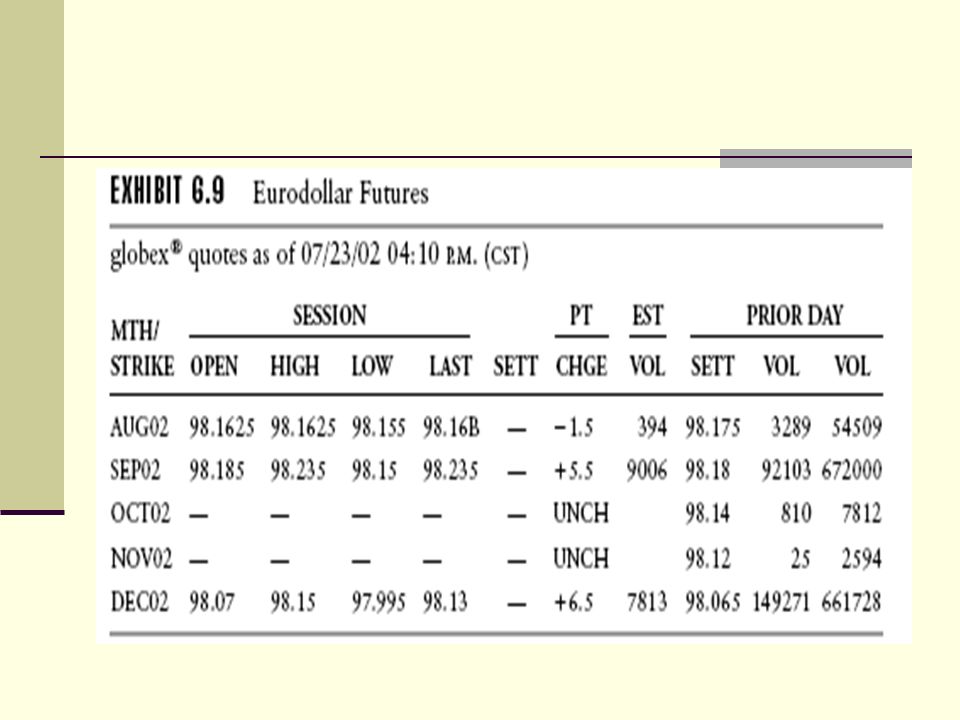

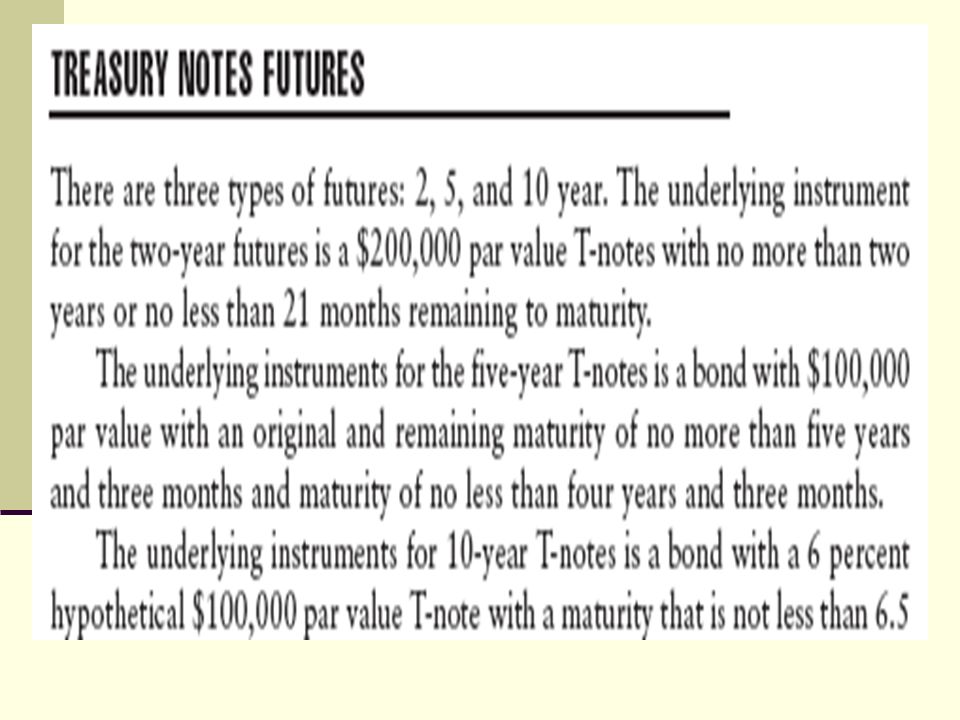

Eurodollar Futures The Eurodollar futures contract, developed by CME in 1981, represents a forward interest rate on a three-month deposit of $1 million. The Eurodollar futures contract is now the most actively traded futures contract in the world. The rate on these deposits serves as a benchmark interest rate for corporate funding.

20

Differences: T-bill & Euro$ futures T-bill futures contract price traded at IMM in Chicago at maturity approaches a $1 million face value of the underlying futures contract as if the party with long position (the party that purchased the T-bill futures) will take delivery of the T-bill at maturity. However, the Eurodollar futures is settled at maturity in cash based on the Eurodollar rate (R) prevailing on the second London business day before the third Wednesday of the month. For example, if the 90-day Eurodollar deposit rate at settlement date is equal to 2.125 percent, then the final marking to market will set the contract price by Equation 6.11: 10,000 (100 -.25 (R))

prevailing on the second London business day before the third Wednesday of the month. For example, if the 90-day Eurodollar deposit rate at settlement date is equal to percent, then the final marking to market will set the contract price by Equation 6.11: 10,000 ( (R)).")

21

Delivery process Day 1: The short serves notice to the clearinghouse to deliver, known as position day

24

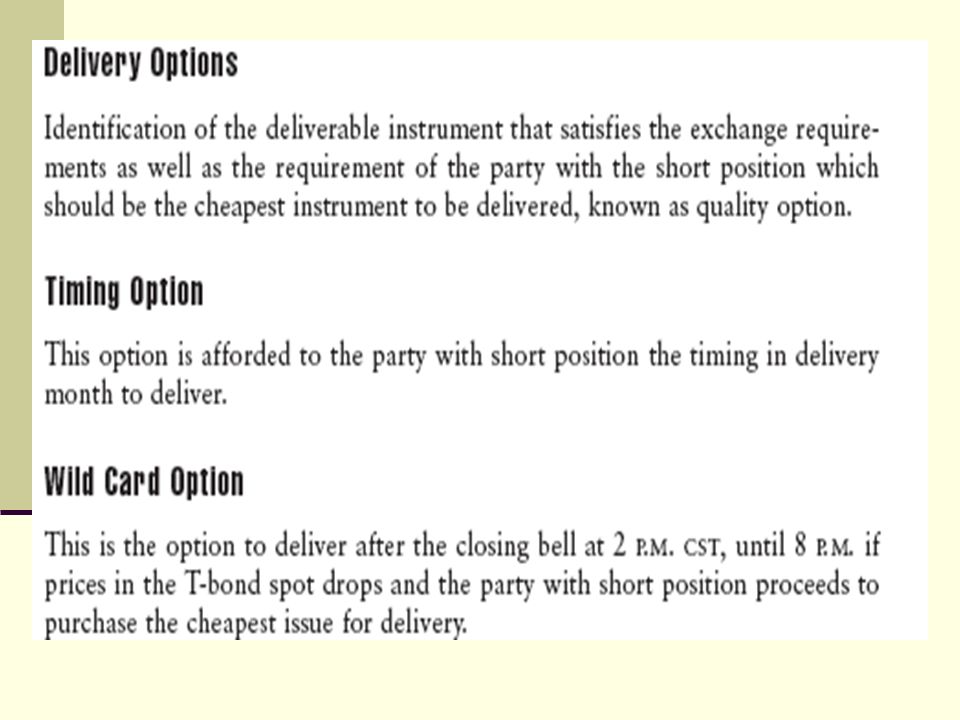

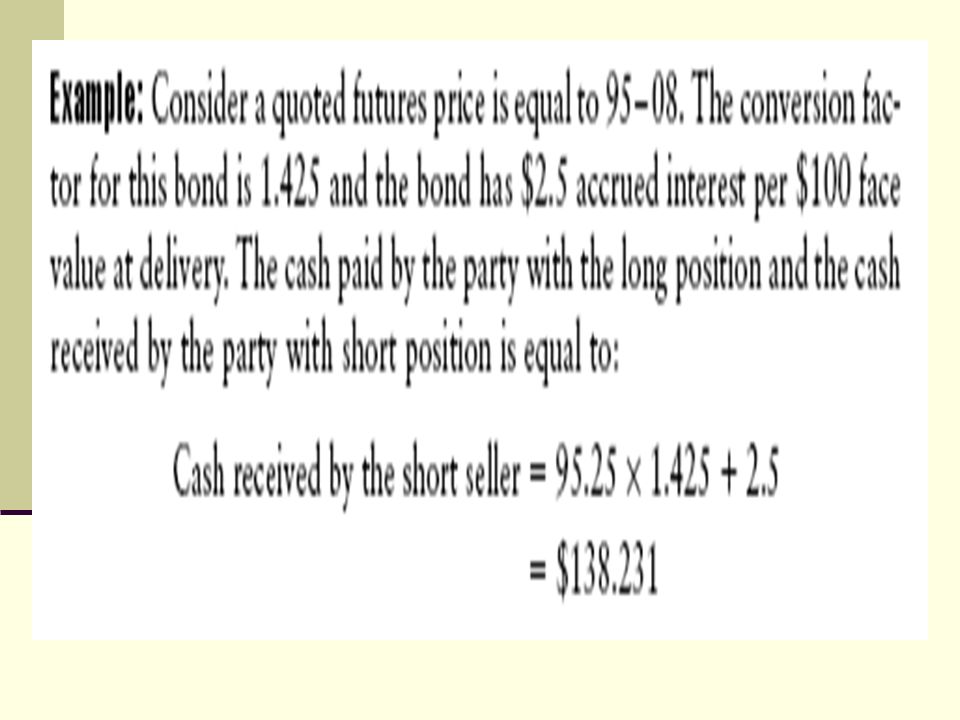

Cheapest to Deliver CTD

26

Example: CTD

Similar presentations

slope increases (long term R increases more than short term or short term even decreases) buy notes sell bonds.>")