Download presentation

Presentation is loading. Please wait.

1

Is Government Justified in Banning Futures Trade in Essential Commodities? Alka Parikh Department of Economics, University of Mumbai This paper has benefited from the comments by Dr. Abhay Pethe, Dr. Mala Lalvani and Dr. Romar Correa.

2

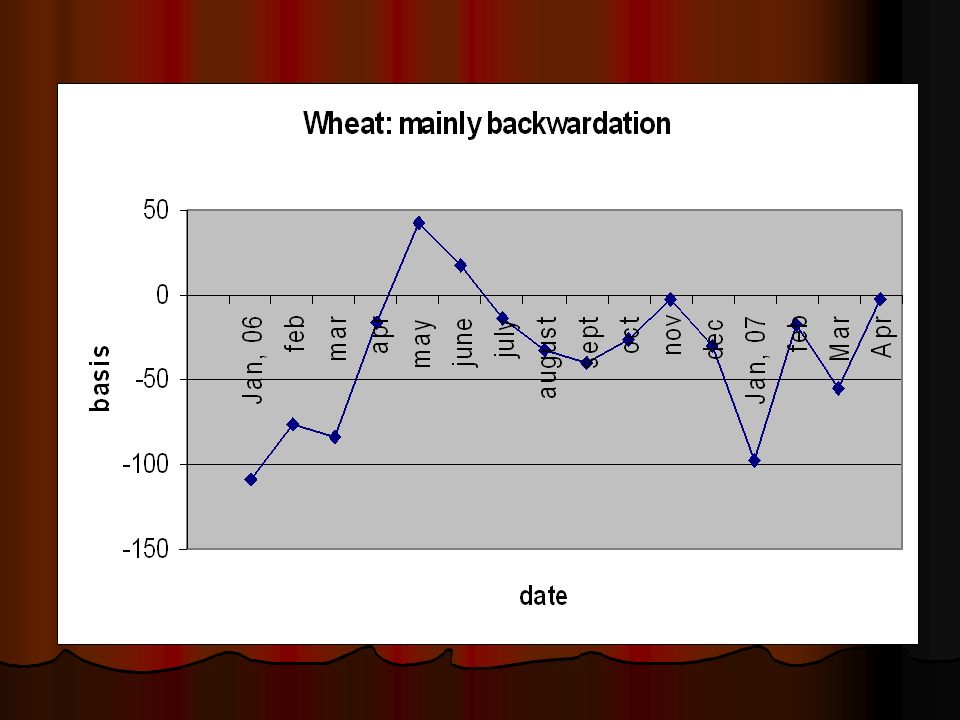

The key question Are the futures in essential commodities really responsible for the price rise? Do the commodity exchanges indeed affect the prices in the spot markets? Focus of the study: Wheat

3

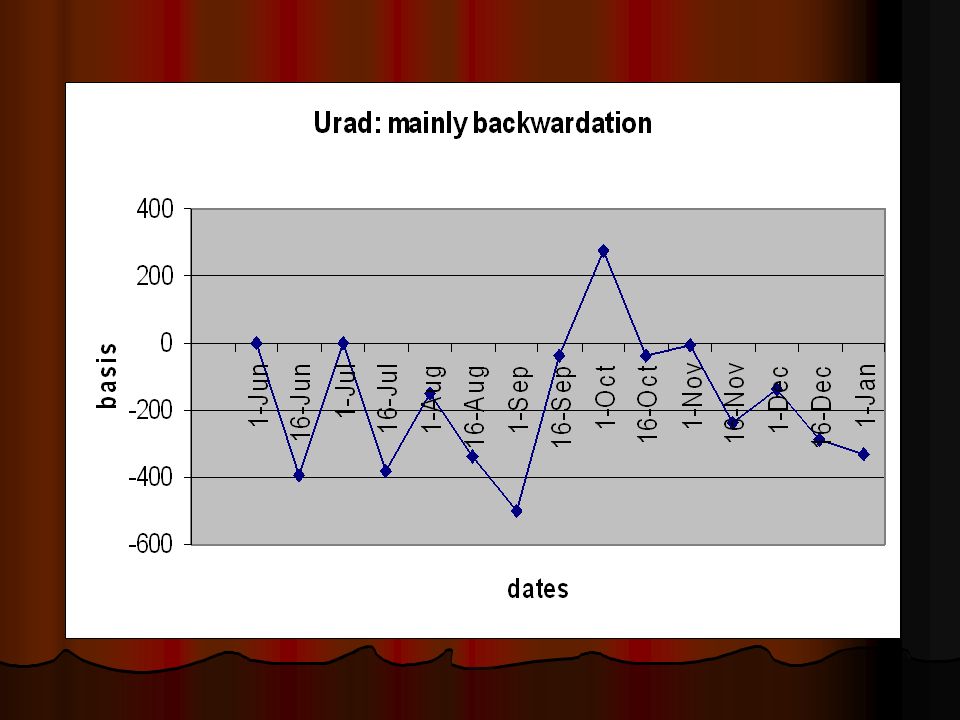

Volume Table 1: Production and Volumes traded of different commodities CommodityyearTrade volProduction (1)(2)(3)(4) (3)/(4) Urad 2005-67,31,73,050 10,85,00067.4 Wheat 2006-7 2,30,84,520 7,50,00,0000.31 Sugar (S) 2006-760,570 1,80,00,0000.003 Chana 2005-611,95,26,380 55,00,00021.7 Pepper 2005-67,05,529 50,00014.1 Source: FMC, India, www.indiastat.comwww.indiastat.com

(2)(3)(4) (3)/(4) Urad ,31,73,050 10,85, Wheat ,30,84,520 7,50,00, Sugar (S) ,570 1,80,00, Chana ,95,26,380 55,00, Pepper ,05,529 50, Source: FMC, India,")

4

Implication: The volumes traded are much higher for urad, chana and pepper. Wheat: Volumes traded are low. Little likelihood of impacting spot markets.

8

Implications: This could happen only in condition of excess supply. Wheat production reasonably high in last two years Hedgers seem to want to sell to cover their risks, but few speculators who want to buy No obvious proof of excessive speculation

9

Price Fluctuations Wheat: 10% around the mean both in spot and futures markets Chana: 12-13% around the mean in both spot and futures markets Pepper: 20% around the mean in both spot and futures markets Urad: 5% around the mean in futures and 10% around the mean in the spot markets Thus, no excessive volatility in wheat markets.

10

Statistical Tests Based on results of Gurpreet Singh Sahi Structural Test Chow test: No structural change in spot prices by introduction of future trade. Also, the coefficient of dummy variable for post futures years is insignificant for the tested commodities.

11

Grange Causality Test Unexpected trading volume and unexpected open interest Granger cause cash price volatility in wheat, turmeric, soy oil and raw jute. Decomposition Generalised forecast error variance decompositions: For all tested commodities, variation in cash price volatility is not explained by futures price volatility or unexpected trading volume or unexpected open interest.

12

In short, the causality is not strongly established. Although it is shown that the direction of influence is from futures to spots, the extent to which the futures influence spot markets seems to be statistically insignificant.

13

Conclusions Banning wheat markets: Not justified by the data. Further research questions: Pulses: Volumes traded are much higher than production -> Speculation might prove harmful in shortage economies. “Price discovery” should not become price determination. Spices: Need to examine whether too much price volatility discourages farmers as shown in the case of cardamom

14

Impact on farmers: Information should be available physically and functionally Studies show that direct participation of farmers is very low. Reasons: Low awareness Individual farmer does not have enough supplies to fulfill contract specifications Thus farmers benefit only indirectly. But is the purpose of the futures really to benefit the farmers? The farmer participation low even in USA. It is an upgradation of marketing system, let it happen.

Similar presentations