Download presentation

Presentation is loading. Please wait.

1

Hua Haixing Refky Saputra Bradley Coyne Presented October 28, 2014

2

Investment Thesis Holding Information Macroeconomics & Industry Overview Company Overview & Business Segment Financial Performance Financial Projection & DCF Financial Conclusion

3

Weak medical devices performance in the past two years. We foresee medical devices market to decline Weak US Pharmaceutical business; whether the potential sell-off will bring decent reinvest return is undetermined Overvalued comparing with its peers: traded at 28x trailing P/E while its peers are traded at 22x Overvalued based on DCF valuation, despite the aggressive sales growth projection

4

As Per 10/27/2014: Currently own 400 shares @ $26.72 (9.4% of Portfolio) Cost of Position is $10,688 Current Share Price is $42.24 Value of Position is $16,896 Potential Gain $6,208 or 58% Abbott is a 125 years old global healthcare company with unique mix of businesses and broadly diversified portfolio of market-leading products is aligned with long-term healthcare trends in both developed and developing markets.

Cost of Position is $10,688 Current Share Price is $42.24 Value of Position is $16,896 Potential Gain $6,208 or 58% Abbott is a 125 years old global healthcare company with unique mix of businesses and broadly diversified portfolio of market-leading products is aligned with long-term healthcare trends in both developed and developing markets.")

5

New Environment in Health Industry (2011 – 2020) Economic Volatility Focus on Key Mature Markets and Growth Markets 7.6 % - 9.4% of global population aged 65 + Obesity Epidemic Social Media Specialist-Medicine business model (proteins with annual revebue of $1 Bn per product Treatment for rare/acute deseases Products marketed to healthcare payers Value based purchasing (using outcomes) Sources: http://www.pwc.com/gx/en/pharma-life-sciences/pharma2020/market-opportunities-and-outlook.jhtml

Economic Volatility Focus on Key Mature Markets and Growth Markets 7.6 % - 9.4% of global population aged 65 + Obesity Epidemic Social Media Specialist-Medicine business model (proteins with annual revebue of $1 Bn per product Treatment for rare/acute deseases Products marketed to healthcare payers Value based purchasing (using outcomes) Sources:")

6

Sell-off of developed market EPD business Source: Bloomberg ABT US Equity Financial Analysis

7

Sources: Data from Bloomberg ABT US Equity historical financial analysis FY201314Q114Q214Q3 Total Sales Growth-2.87%-6.7%-0.2% 11.5% (claimed) -37.6% (realized) Key Emerging Market GrowthN/A-9.23%4.41%5.06% 14Q3 -37.6% realized growth rate was due to sell-off of US EPD business to Mylan Inc. for 21% of its stake (Market Value approximately $4 bn or $2.57 per ABT share) Company claimed that the 14Q3 Sales grow for 11.5% because they only kept the most profitable emerging market business The past achieved emerging market growth was not as attractive The company kept changing their reporting methods to fool the investors

Company claimed that the 14Q3 Sales grow for 11.5% because they only kept the most profitable emerging market business The past achieved emerging market growth was not as attractive The company kept changing their reporting methods to fool the investors.")

8

Source: http://www.minyanville.com/trading-and-investing/stocks/articles/boomer-stocks-stocks-to-watch-stocks/6/18/2012/id/41797http://www.minyanville.com/trading-and-investing/stocks/articles/boomer-stocks-stocks-to-watch-stocks/6/18/2012/id/41797 Products portfolio: 55%Pediatric, 45% Adult Solid sales growth over the past three years; weak in first 2Q 2014 due to supplier issues; Infant formula: 40% of US market share (Top 2) Adult formula: Global market leader FY2011FY2012FY201314Q1-314Q3 Total Sales Growth8.57%7.74%4.16%2.20%9.30% Pediatric Growth10.75% 10.36%6.81%0.04% 8.69% Adult Growth6.97% 5.04%1.33%4.99% 10.01%

Adult formula: Global market leader FY2011FY2012FY201314Q1-314Q3 Total Sales Growth8.57%7.74%4.16%2.20%9.30% Pediatric Growth10.75% 10.36%6.81%0.04% 8.69% Adult Growth6.97% 5.04%1.33%4.99% 10.01%")

9

Core LaboratoryMolecularPoint of Care Main ProductsImmunoassay, Clinical Chemistry, Blood Screening, Hematology Infectious Disease, HCV, and HIV testing Abbott i-STAT Favorable TrendsAging global population, increasing emphasis on disease prevention, emerging market investments in healthcare, need for high-volume, standardized systems, and long, durable contract cycles Leadership Positions#1 Globally in Immunoassay and Blood Screening Best-in-class Infectious Disease Molecular Tests #1 Point of Care Platform in the US Sales Growth2010 – 6.0%; 2011 – 8.8%; 2012 – 4.0%; 2013 – 5.9% Growth TrendsCapturing growth in Emerging Markets Largest and fastest growing segment in emerging markets Expanding footprint and developing next generation system Risk FactorsCompetition, Rapid Product Obsolescence, and Regulatory Changes Source: Abbott Diagnostic Strategy - http://prod2.dam.abbott.com/en-us/documents/pdfs/investors/our-strategy/Diagnostics_March_2014.pdf

10

VascularDiabetes CareVision Care Main ProductsDrug-eluting Stents Bioresorbabl e Scaffolds Glucose Monitoring Meters & test strips Cataract & refractive laser surgery devices Risk FactorsDecreasing price, competition FDA approval, expensivenes s Fierce competition, global market to decline Acquisition of OptiMedica Favorable TrendsAging population; more diabetes, myopic & cataract patients; richer emerging market Market OutlookEuropean Market to decline,Glucose-Monitoring market peaked in 2011 Global Market to grow Sales Balance55% Vascular24% Diabetes21% Vision Sales GrowthFY2011: -2.3%; FY2012: -5.4%; FY2103: -0.6%; 2014 Q1-3: -0.3% Sources: http://www.allaboutvision.com/conditions/cataract-surgery.htm; http://www.ibj.com/articles/41392-report-roche-mulls-sale-of-blood-glucose-monitor- businesshttp://www.allaboutvision.com/conditions/cataract-surgery.htmhttp://www.ibj.com/articles/41392-report-roche-mulls-sale-of-blood-glucose-monitor- business ; http://www.fiercebiotech.com/press-releases/european-coronary-stent-market-decline-490-million-2016-despite-growth-numb-0

11

Threat of new entrant (Low) It is very expensive to entry the Industry Oligopolistic Industry Prolonged drug and medical device approval process Suppliers (medium) Suppliers are generally price takers Component suppliers for medical devices often has better bargaining power Buyer bargaining power (Low) Healthcare demands are inelastic Obama care made more people covered in insurance Substitute products (Medium) Generic drugs are competitive Have top of the Line Products Strong pipeline to consumers Rivalry among existing firms (Medium) Generic companies has been increasing focus in establishing global operations

It is very expensive to entry the Industry Oligopolistic Industry Prolonged drug and medical device approval process Suppliers (medium) Suppliers are generally price takers Component suppliers for medical devices often has better bargaining power Buyer bargaining power (Low) Healthcare demands are inelastic Obama care made more people covered in insurance Substitute products (Medium) Generic drugs are competitive Have top of the Line Products Strong pipeline to consumers Rivalry among existing firms (Medium) Generic companies has been increasing focus in establishing global operations")

12

Strengths Geographical diversity Diversified business operations Well Established Brands Weaknesses Lack of growth in certain segments Company is overly dependent upon mature products whose patents may expire in near future Opportunities Emerging market growth High Birth Rates Aging Population New developments in technology Threats Regulatory Changes Competitive landscape Uncertain R&D outcomes Product recalls 12

13

13 Source: http://marygardiner.wordpress.com/2013/05/28/product-cycles/

14

Profitability dropped after Abbvie spin-off Leverage increased slightly comparing with FY13 Better working capital management comparing with FY13

19

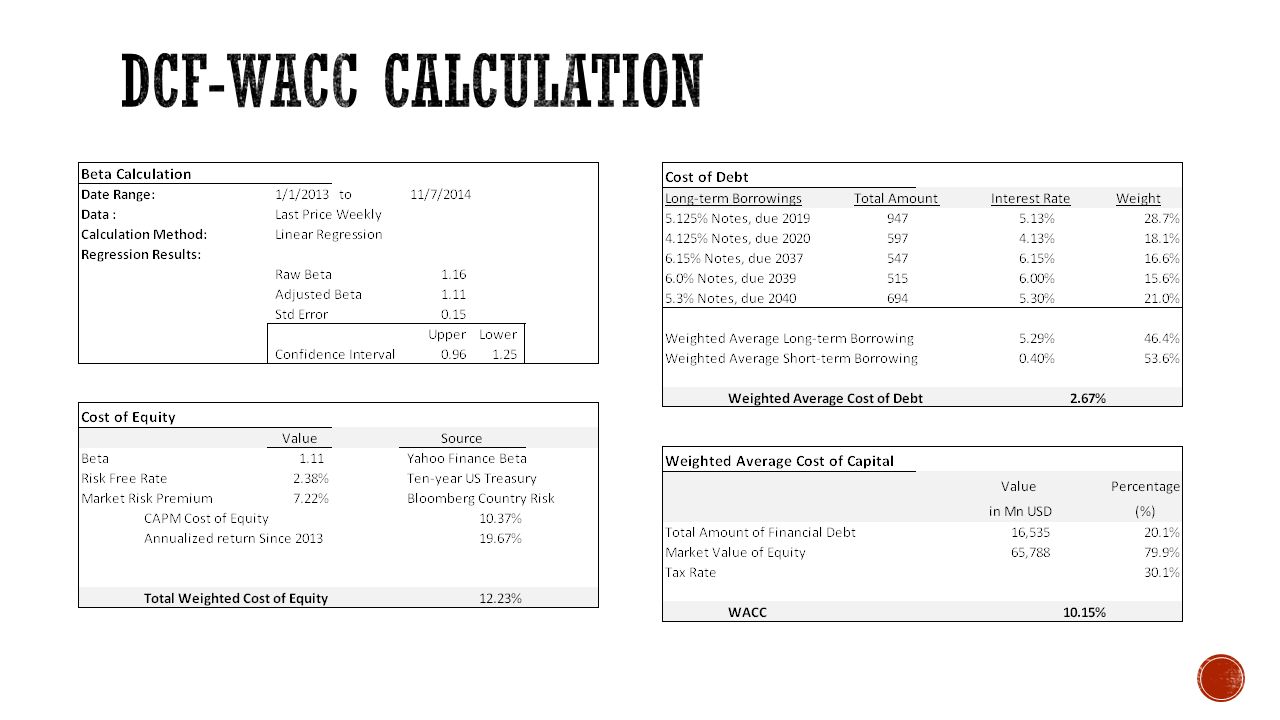

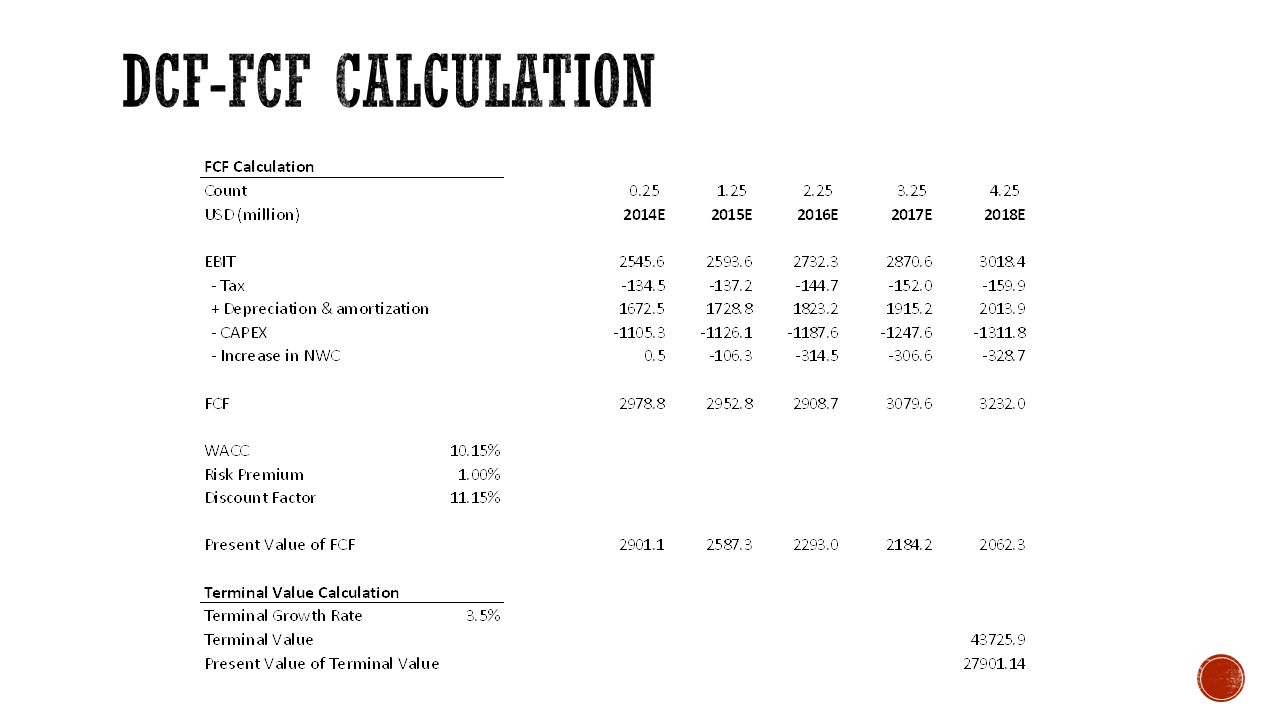

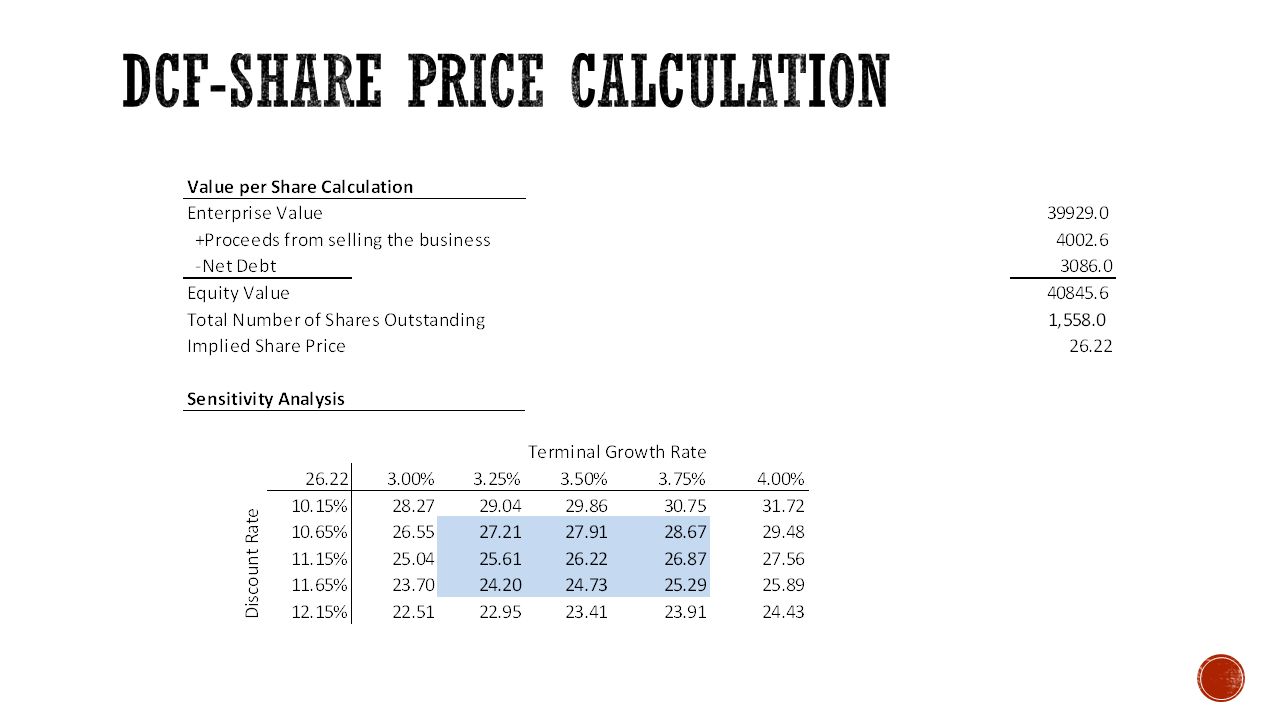

Sales Projection We cannot foresee the company to have any big change, so our sales growth projection is predominantly based on the past figures. Nutritionals: despite that the company only achieved an average growth rate of Although the company improve their Operating margin from 7.6% in 2011 to 12% in 2013, their first 3Q achieved operating margin maintained at 12%, so I cannot foresee a larger operating margin going forward. Beta Calculation We run regression for weekly close price since 2013-Jan-01 for several reasons: 1) By using weekly price we transpire the volatility of day-trading. 2) The ABBV spin- off took place at Jan 1 st, 2013, so using the data since 2013 can better reflect the current nature of business. DCF-Share Price Calculation The company will sell off its US Pharmaceutical business to Mylan Inc. for 21% of its stake. The sell-off will cause the FCF to decrease, while owning only 21% of stake will not have any influence on ABT’s income statement, so we directly added the Mylan’s value into the DCF resulted share price.

By using weekly price we transpire the volatility of day-trading. 2) The ABBV spin- off took place at Jan 1 st, 2013, so using the data since 2013 can better reflect the current nature of business. DCF-Share Price Calculation The company will sell off its US Pharmaceutical business to Mylan Inc. for 21% of its stake. The sell-off will cause the FCF to decrease, while owning only 21% of stake will not have any influence on ABT’s income statement, so we directly added the Mylan’s value into the DCF resulted share price..")

20

Selection criteria Comprehensive health care companies: after the spin-off of ABBvie, ABT is no longer a pharmaceutical company, so we try to avoid 100% pharmaceuticals. Global Presence: since ABT is gradually moving its focus to emerging market, we try to choose companies with global presence as comps.

21

Key Takeaways: ABT share price: $42.24 as of Oct. 27 th,2014 Trade at fair value based on EV/Revenue, overvalued based the other ratios even taking into account the value of Mylan Inc. ($2.57 per share) ABT has lower margin comparing with its peers

ABT has lower margin comparing with its peers.")

22

Current stock price $42.24 as of Oct 27, 2014 DCF $26.22 Comparables $32.09 We recommend to sell 100 shares at the market price

Similar presentations

Analysts: Chris Landqvist, Justin Pippitt, Kelli Coldiron & Wei Pi.>")

>")