Download presentation

Presentation is loading. Please wait.

1

Swap Markets

2

What is a swap agreement/contract; An Interest Rate Swap An agreement between two organizations (e.g. a bank and a client) to exchange cash flows in the future according to a pre-specified plan For example, Company B agrees to pay to Company A a fixed interest rate once a year on a nominal principal for a specified period (e.g. 1 to 15 years) At the same time A agrees to pay to B a floating interest rate on the same principal and for the same duration

to exchange cash flows in the future according to a pre-specified plan For example, Company B agrees to pay to Company A a fixed interest rate once a year on a nominal principal for a specified period (e.g. 1 to 15 years) At the same time A agrees to pay to B a floating interest rate on the same principal and for the same duration.")

3

What is a swap agreement/contract; A Currency Swap An agreement between two organizations (e.g. a bank and a client) to exchange principal and cash flows in the future according to a pre-specified plan For example, Company B agrees to pay to Company A a fixed interest rate on the British Pound once a year on a principal for a specified period (e.g. 1 to 15 years) At the same time A agrees to pay to B a floating interest rate on the US$ for the same principal and for the same duration

to exchange principal and cash flows in the future according to a pre-specified plan For example, Company B agrees to pay to Company A a fixed interest rate on the British Pound once a year on a principal for a specified period (e.g. 1 to 15 years) At the same time A agrees to pay to B a floating interest rate on the US$ for the same principal and for the same duration.")

4

Swap markets The first swap was organized in 1981 between IBM and the World Bank; the global swap market expanded rapidly due to technological innovations, capital market liberalization and financial engineering innovations Most swaps are traded over-the-counter (OTC), "tailor-made" for the counterparties.over-the-counter Some types of swaps are also exchanged on futures markets such as the Chicago Mercantile Exchange Holdings Inc., the largest U.S. futures market, the Chicago Board Options Exchange, IntercontinentalExchange and Frankfurt-based Eurex AG. The Bank for International Settlements (BIS) publishes statistics on the notional amounts outstanding in the OTC derivatives market. At the end of 2006, this was USD 415.2 trillion, more than 8.5 times the 2006 gross world product.Bank for International Settlementsnotional amountsderivatives market2006 gross world product Note that in 1985 ISDA (International Swaps and Derivatives Association) estimated the notional size of the market to approximately $ 865.6 billion In 2004 ISDA (International Swaps and Derivatives Association) estimated the notional size of the market to approximately $ 127 trillion In 2004 ISDA estimated the average daily trading volume to $ 600 billion

publishes statistics on the notional amounts outstanding in the OTC derivatives market. At the end of 2006, this was USD trillion, more than 8.5 times the 2006 gross world product.Bank for International Settlementsnotional amountsderivatives market2006 gross world product Note that in 1985 ISDA (International Swaps and Derivatives Association) estimated the notional size of the market to approximately $ billion In 2004 ISDA (International Swaps and Derivatives Association) estimated the notional size of the market to approximately $ 127 trillion In 2004 ISDA estimated the average daily trading volume to $ 600 billion.")

5

Swap markets

6

Swaps are nowadays standardized financial instrument to a high degree and have a large number of underlying assets; they are traded in many platforms electronically. Short-term swaps (up to 2 years) are usually interbank instruments while long-term swaps are often attractive to businesses and other organizations A usual distinction is between simple swaps («vanilla swaps») and more complex deals («exotic swaps»). Vanilla swaps (the most common) are usually agreements to swap fixed with floating interest rate on the same currency Exotic swaps are less standardized and more “tailor made”

are usually interbank instruments while long-term swaps are often attractive to businesses and other organizations A usual distinction is between simple swaps («vanilla swaps») and more complex deals («exotic swaps»). Vanilla swaps (the most common) are usually agreements to swap fixed with floating interest rate on the same currency Exotic swaps are less standardized and more tailor made .")

7

Swap markets Another type of swap is the «asset swap», where an investor buys an asset (e.g. a fixed rate bond) and at the same time agrees an interest rate swap (fixed for floating) with the same duration of the bond. The investor uses the coupon of the bond to pay the fixed payments and receives the floating payments. In this case we usually say that the fixed rate return has been transformed to a “synthetic” floating rate product; if the bond rate is higher than the fixed swap rate the investor could benefit Equity swap, example: I agree with bank X to receive the returns of S&P500 for five years in monthly installments and pay the bank an interbank yield

and at the same time agrees an interest rate swap (fixed for floating) with the same duration of the bond. The investor uses the coupon of the bond to pay the fixed payments and receives the floating payments. In this case we usually say that the fixed rate return has been transformed to a synthetic floating rate product; if the bond rate is higher than the fixed swap rate the investor could benefit Equity swap, example: I agree with bank X to receive the returns of S&P500 for five years in monthly installments and pay the bank an interbank yield.")

8

Swap markets Swap buyer: the party that has agreed to pay the Fixed rate Swap seller: the party that has agreed to pay the Floating rate

9

Interest rate arbitrage Co A wants to borrow for 10 years at a floating rate Co Β wants to borrow for 10 years at a fixed rate Assume they want to borrow the same amount FixedFloating Co A (ΑΑΑ) 9.5%LIBOR + 0.25% Co Β (ΒΒΒ) 11%LIBOR + 0.75%

9.5%LIBOR % Co Β (ΒΒΒ) 11%LIBOR %")

10

Comparative advantage Difference between fixed ΑΑΑ and ΒΒΒ: 1.5% Difference between floating ΑΑΑ and ΒΒΒ: 0.5% Co A has a comparative advantage for fixed rate loans Co B has a comparative advantage for floating rate loans BUT Co A wants to borrow for 10 years at a floating rate Co Β wants to borrow for 10 years at a fixed rate

11

Motive for swap – Profit If: α = difference between fixed rates (1.5%) β = difference between floating rates (0.5%) The profit from a swap is: | α-β | =| 1.5 – 0.5 | = 1%

β = difference between floating rates (0.5%) The profit from a swap is: | α-β | =| 1.5 – 0.5 | = 1%")

12

The swap

13

Result for Co A (wants floating; would pay LIBOR + 0,25%) Pays Fixed9.5% (Loan) Pays Floating Libor (swap) Receives Fixed 9.75% (swap) ------------------------------------------------------------ Pays floating Libor – 0.25% Improved by 0.5%

Pays Fixed9.5% (Loan) Pays Floating Libor (swap) Receives Fixed 9.75% (swap) Pays floating Libor – 0.25% Improved by 0.5%")

14

Result for Co B (wants fixed; would pay 11%) Pays Floating Libor+0.75%(Loan) Pays Fixed 9.75% (swap) Receives Floating Libor (swap) ------------------------------------------------------------ Pays fixed 105% Improved by 0.5%

Pays Floating Libor+0.75%(Loan) Pays Fixed 9.75% (swap) Receives Floating Libor (swap) Pays fixed 105% Improved by 0.5%")

15

Another example Co A wants to borrow for 10 years at a floating rate Co Β wants to borrow for 10 years at a fixed rate Assume they want to borrow the same amount FixedFloating Co A (ΑΑΑ) 10%LIBOR + 0.3% Co Β (ΒΒΒ) 11.2%LIBOR + 1%

10%LIBOR + 0.3% Co Β (ΒΒΒ) 11.2%LIBOR + 1%")

16

Comparative advantage Difference between fixed ΑΑΑ and ΒΒΒ: 1.2% Difference between floating ΑΑΑ and ΒΒΒ: 0.7% Co A has a comparative advantage for fixed rate loans Co B has a comparative advantage for floating rate loans BUT Co A wants to borrow for 10 years at a floating rate Co Β wants to borrow for 10 years at a fixed rate

17

Comparative advantage Profit:| α-β | =| 1.2 – 0.7 | = 0.5%

18

Result for Co A (wants floating; would pay LIBOR + 0.30%) Pays Fixed10% (Loan) Pays Floating Libor (swap) Receives Fixed 9.95% (swap) ------------------------------------------------------------ Pays floating Libor + 0.05% Improved by 0.25%

Pays Fixed10% (Loan) Pays Floating Libor (swap) Receives Fixed 9.95% (swap) Pays floating Libor % Improved by 0.25%")

19

Result for Β (wants fixed; would pay 11.2%) Pays Floating Libor+1%(Loan) Pays Fixed 9.95% (swap) Receives floating Libor (swap) ------------------------------------------------------------ Pays Fixed 10.95% Improved by 0.25%

Pays Floating Libor+1%(Loan) Pays Fixed 9.95% (swap) Receives floating Libor (swap) Pays Fixed 10.95% Improved by 0.25%")

20

Cash Flows: Example; Co B

21

Use of interest rate swap (i) Transform the nature of a liability Assume that Co A has issued a Loan (or bond) of $100 million at a floating rate of Libor+0.8%. Co A is afraid that interest rates will increase in the future and would prefer fixed installments One solution would be to retire the loan (if possible) and issue a new one (expensive solution)

and issue a new one (expensive solution).")

22

A cheaper solution would be to find a Co B that has the opposite expectations and swap cash flows E.g. Co A pays fixed 5% and receives Libor What is the result?

23

Result Pays Libor + 0.8% (Loan) Receives Libor (swap) Pays 5% (swap) -------------------------------------------------------- Pays 5.8% (Fixed) Transformed a floating rate liability to a fixed rate liability

Receives Libor (swap) Pays 5% (swap) Pays 5.8% (Fixed) Transformed a floating rate liability to a fixed rate liability")

24

Use of interest rate swap (i) Transform the nature of an asset Assume that Co A has invested in a fixed rate bond $100 million at a rate of 4.7% Co A is afraid that interest rates will increase in the future and would prefer floating cash flows One solution would be to sell the fixed rate bond (if possible) and buy a new one with a floating rate (expensive solution)

Transform the nature of an asset Assume that Co A has invested in a fixed rate bond $100 million at a rate of 4.7% Co A is afraid that interest rates will increase in the future and would prefer floating cash flows One solution would be to sell the fixed rate bond (if possible) and buy a new one with a floating rate (expensive solution)")

25

A cheaper solution would be to find a Co B that has the opposite expectations and swap cash flows E.g. Co A pays fixed 5% and receives Libor What is the result?

26

Αποτέλεσμα Receives 4.7% (Investment) Receives Libor (swap) Pays 5% (swap) -------------------------------------------------------- Receives Libor - 0.3% (Floating) Transformed a fixed rate investment to a floating rate investment

Receives Libor (swap) Pays 5% (swap) Receives Libor - 0.3% (Floating) Transformed a fixed rate investment to a floating rate investment")

27

The role of banks In practice it is difficult for two companies to meet They will use a bank which will do two transactions, one with each company

28

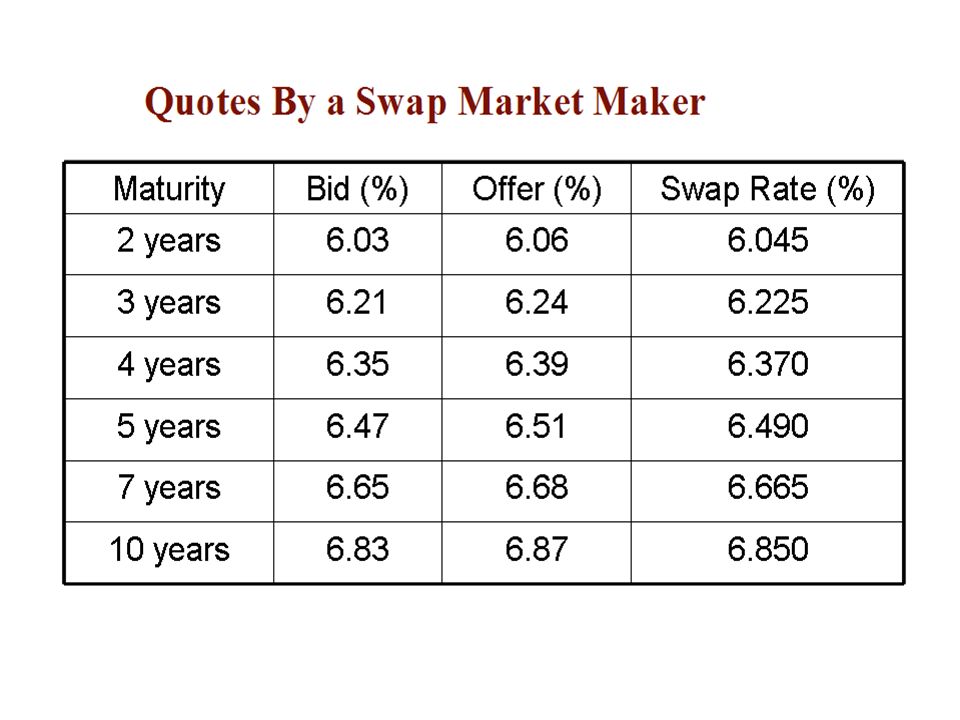

The role of banks Investment banks that are active in this market will prepare quotation tables with indicative prices at which they are willing to buy/sell swaps Traders will use these tables for pricing Tables will change constantly in order to incorporate changing market conditions Prices are expressed in the form of interest rates in basis points (1 bp = 0.1%)

")

30

The role of banks Example: the next Table presents the prices in spreads over the US Treasury Note (TN) rates This is common for interest rate swaps on the US $. Assume that the current 2-year ΤΝ is 8.55%; then the hypothetical bank is willing to pay for 2 year swap a fixed rate of 8.75% (8.55% + 20 bps) and receive a floating rate (e.g. LIBOR).

and receive a floating rate (e.g. LIBOR)..")

31

The role of banks

32

Structured Bonds Another example (2007, Hellenic Republic): Decision 2/8449/0023Α/6 Feb 2007 (Ministry of Finance and Defense) Issue price: 100% Maturity:12 years (Issue date: Feb 2007) Coupon rate: For the first two years 6,25% For the remaining ten years →if the difference between the 10-year interbank Euroswap rate and the 2-year interbank Euroswap rate is below 1% it will pay the product of this difference times five → If the difference between the 10-year interbank Euroswap rate and the 2-year interbank Euroswap rate is above 1% it will pay the 3-month Euribor+1.5%

: Decision 2/8449/0023Α/6 Feb 2007 (Ministry of Finance and Defense) Issue price: 100% Maturity:12 years (Issue date: Feb 2007) Coupon rate: For the first two years 6,25% For the remaining ten years →if the difference between the 10-year interbank Euroswap rate and the 2-year interbank Euroswap rate is below 1% it will pay the product of this difference times five → If the difference between the 10-year interbank Euroswap rate and the 2-year interbank Euroswap rate is above 1% it will pay the 3-month Euribor+1.5%")

33

Structured Bonds Assume that 10-year interbank Euroswap rate = 3% 2-year interbank Euroswap rate = 2.5% Difference: 0.5% Coupon = 0.5% times 5 = 2.5% Assume that 10-year interbank Euroswap rate = 3% 2-year interbank Euroswap rate = 1.5% Difference: 1.5% Coupon = 3-month Euribor + 1.50 %

34

Structured Bonds, Pension Funds, Swaps With the same decision the Hellenic Republic decided an interest rate swap with JΡ Μorgan: a)JΡ Μorgan pays the interest of the bond that the issuer has to pay to investors (i.e. the Pension Funds) for 12 years b) The issuer pays to JP Μorgan the annual Εuribor-0.16%, for 12 years

for 12 years b) The issuer pays to JP Μorgan the annual Εuribor-0.16%, for 12 years.")

35

The swap

36

A Currency Swap An agreement between two organizations (e.g. a bank and a client) to exchange principal and cash flows in the future according to a pre-specified plan For example, Company B agrees to pay to Company A a fixed interest rate on the British Pound once a year on a principal for a specified period (e.g. 1 to 15 years) At the same time A agrees to pay to B a floating interest rate on the US$ for the same principal and for the same duration

to exchange principal and cash flows in the future according to a pre-specified plan For example, Company B agrees to pay to Company A a fixed interest rate on the British Pound once a year on a principal for a specified period (e.g. 1 to 15 years) At the same time A agrees to pay to B a floating interest rate on the US$ for the same principal and for the same duration.")

37

Example 5-year swap between A and B agreed on February 1999. A pays fixed 11% on British Pounds (BP) and B pays fixed 8% on US $. Payments take place on an annual basis an dteh par values are 15 million $ and 10 million BP

and B pays fixed 8% on US $. Payments take place on an annual basis an dteh par values are 15 million $ and 10 million BP.")

38

Cash flows for A Date$ (million)£(million) Feb 1999-15+10 Feb 2000+1.2-1.1 Feb 2001+1.2-1.1 Feb 2002+1.2-1.1 Feb 2003+1.2-1.1 Feb 2004+16.2-11.1

£(million) Feb Feb Feb Feb Feb Feb")

39

Motive for a currency swap $Α$ Co A (ΑΑΑ) 4%11.6% Co Β (ΒΒΒ) 6%12% Α wants 4-year $ Australia B wants 4-year $ USA

4%11.6% Co Β (ΒΒΒ) 6%12% Α wants 4-year $ Australia B wants 4-year $ USA")

40

Comparative advantage Difference $ ΑΑΑ and $ ΒΒΒ: 2% Difference Α$ ΑΑΑ and Α$ ΒΒΒ: 0.4% Β has a Comparative advantage on Α$ Α has Comparative advantage on US$ Α wants Α$ Β wants US$

41

Profit: | α-β | =| 2 – 0.4 | = 1,6% Assume bank organizes and keeps 0.2% Profit: 1.6 – 0.2 = 1.4% (from 0.7% each)

")

42

The Swap

43

Result for Α (wantsΑ$, would pay 11.6%) Pays$4% (Loan) Pays Α$10.9%(swap) Receives $4% (swap) ----------------------------------------------------------- Pays Α$ 10.9% Improved by 0.7%

Pays$4% (Loan) Pays Α$10.9%(swap) Receives $4% (swap) Pays Α$ 10.9% Improved by 0.7%")

44

Result for Β (wants US$, would pay 6%) Pays Α$12% (Δάνειο) Pays $5.3%(swap) Receives Α$12% (swap) ----------------------------------------------------------- Pays $ 5.3% Improved by 0.7%

Pays Α$12% (Δάνειο) Pays $5.3%(swap) Receives Α$12% (swap) Pays $ 5.3% Improved by 0.7%")

45

Result for Bank Receives Α$10.9%(swap) Pays Α$12% (swap) Pays $5.3%(swap) Receives $4%(swap) ----------------------------------------------------------- Receives 0.2% Currency risk to be hedged

Pays Α$12% (swap) Pays $5.3%(swap) Receives $4%(swap) Receives 0.2% Currency risk to be hedged")

46

Uses of currency swaps (a)Transform liabilities 7 years ago Co A issued 10-year bond with a Par of $30 million and coupon rate = 7% Today Co Α believes that a bond in British Pounds would be more preferable What can A do?

Transform liabilities 7 years ago Co A issued 10-year bond with a Par of $30 million and coupon rate = 7% Today Co Α believes that a bond in British Pounds would be more preferable What can A do")

47

Retire the $ bond and issue a new one (expensive solution) Alternatively, Co A could find another Co B and exchange cash flows Assume a Par of $30 million and BP15 million

Alternatively, Co A could find another Co B and exchange cash flows Assume a Par of $30 million and BP15 million")

48

Result for Co A Pays $2.1 million annually on Bond Receives $2.1 million annually on swap Pays ΒΡ1.5 million annually on swap -------------------------------------------------------- Pays ΒΡ1.5 million annually to Co B Transformed a $ liability (bond) to a BP liability without the cost of restructuring the portfolio

to a BP liability without the cost of restructuring the portfolio")

49

Uses of currency swaps (a)Transform assets Assume Co A has a 3-year investment worth of BP15 million with a rate of return of 10% Today Co Α believes that an investment in US $ would be more preferable What can A do?

Transform assets Assume Co A has a 3-year investment worth of BP15 million with a rate of return of 10% Today Co Α believes that an investment in US $ would be more preferable What can A do")

50

Sell the BP investment and buy a new one in US $ (expensive solution) Alternatively, Co A could find another Co B and exchange cash flows Assume a Par of $30 million and BP15 million

Alternatively, Co A could find another Co B and exchange cash flows Assume a Par of $30 million and BP15 million")

51

Result for Co A ReceivesΒΡ1.5 mil annually from investment Receives $2.1 million annually on swap Pays ΒΡ1.5 million annually on swap -------------------------------------------------------- Receives $2.1 million annually from Co B Transformed a BP asset to a $ asset without the cost of restructuring the portfolio

52

Valuation of Swaps The value of the swap will change on a daily basis for both parties Present value of future cash flows (with continuous compounding) E.g. an interest rate or a currency swap is may be viewed as: Two positions (long/short) on two different bonds A position in a series of forward contracts

on two different bonds A position in a series of forward contracts.")

53

Interest rate swaps V Swap = Present Value of the swap Β Fix = Present value of the fixed rate bond Β Float = Present value of the floating rate bond

54

Interest rate swaps When we receive fixed and pay floating : V Swap = B Fix – B Float When we receive floating and pay fixed: V Swap = B Float – B Fix

55

Continuous compounding Present Value (once a year): PV = FV / (1+r) n Present Value (m times a year): PV = FV / (1+r/m) nm Present Value (continuous): PV = FV / e r n = FV e –r n e= 2,71828 (constant)

: PV = FV / (1+r) n Present Value (m times a year): PV = FV / (1+r/m) nm Present Value (continuous): PV = FV / e r n = FV e –r n e= 2,71828 (constant)")

56

For a series of cash flows Present Value (once a year): PV=[C 1 / (1+r)] + ………… +[C n / (1+r) n ] + [P / (1+r) n ] Present Value (continuous): PV =C 1 e -rt +.....+ C n e -rt + P e -rt

![For a series of cash flows Present Value (once a year): PV=[C 1 / (1+r)] + ………… +[C n / (1+r) n ] + [P / (1+r) n ] Present Value (continuous): PV =C 1 e -rt C n e -rt + P e -rt](http://images.slideplayer.com/27/8939258/slides/slide_56.jpg "For a series of cash flows Present Value (once a year): PV=[C 1 / (1+r)] + ………… +[C n / (1+r) n ] + [P / (1+r) n ] Present Value (continuous): PV =C 1 e -rt C n e -rt + P e -rt")

57

For a series of cash flows For a fixed rate bond B Fix = C 1 e -rt +....+ C n e -rt + P e -rt For a floating rate bond discount the only known cash flows: B Float = (P + c 1 ) e -r1t1 C 1 = the next cash flow

e -r1t1 C 1 = the next cash flow")

58

Example interest rate swap Consider a bank that has a swap where the bank pays Libor and receives 8% on a principal of $100 million, twice a year There are 1.25 years left to maturity and the 3-month, 9- month, 15-month discount rates are 10%, 10.5%, 11%, respectively During the last payment the Libor was 10.2% What is the value of the swap for the bank?

59

The value of the swap The bank receives fixed and pays floating, thus: V Swap = B Fix – B Float B Fix = C 1 e -rt +....+ C n e -rt + P e -rt B Float = (P + c 1 ) e -r1t1

e -r1t1")

60

Let’s find B Fix The fixed is 8% on $100m, i.e. $4m semi-annually C 1 = C 2 = C 3 = $4 million P = $100 million r 1 = 0.10r 2 = 0.105r 3 = 0.11 t 1 = (3/12) t 2 = (9/12) t 3 = (15/12) B Fix =4 e -0.10(3/12) + 4 e -0.105(9/12) + (104) e -0.11(15/12) = $98.2 million

t 2 = (9/12) t 3 = (15/12) B Fix =4 e -0.10(3/12) + 4 e (9/12) + (104) e -0.11(15/12) = $98.2 million.")

61

Let’s find B Float B Float = (P + c 1 ) e -r1t1 To find the floating payment look at the Libor oat the last exchange (10.2%), i.e. 5.1% on $100 million, $5.1 million P = $100 million r 1 = 0,10 t 1 = (3/12) B Float = (100 + 5.1) e -0.10(3/12) = $102.51 million

B Float = ( ) e -0.10(3/12) = $ million.")

62

The Value of the Swap today V Swap = B Fix – B Float B Fix =$98.2 million B Float =$102.51 million V Swap = $98.2 – $102.5 = -$4.27 million

63

Valuation of a Currency Swap V Swap = The Present Value of the swap in domestic currency Β D = The Present Value of the bond in domestic currency Β F = The Present Value of the swap in foreign currency S 0 = The current exchange rate

64

Valuation of a Currency Swap When we receive domestic currency and pay foreign currency: V Swap = B D – S 0 B F When we receive foreign currency and pay domestic currency : V Swap =S 0 B F – B D

65

Example Consider a US Bank that has a 3-year swap from which the bank receives 4% in ¥ and pays 7% in $, annually The principal is $20 million and και 2,400 million ¥ The current exchange rate is ¥115=$1 (S 0 = 1/115) The discount rates are: 3.5%, 4%, 4.5% in Japan and 9%, 9.5%, 10% in the US What is the current value of the swap for the bank?

The discount rates are: 3.5%, 4%, 4.5% in Japan and 9%, 9.5%, 10% in the US What is the current value of the swap for the bank")

66

Let’s find B D Payment 7% on $20 million, thus $1.4 million C 1 = C 2 = C 3 = $1.4 million P = $20 million. r 1 = 0.09r 2 = 0.095r 3 = 0.10 t 1 = 1 t 2 = 2 t 3 = 3 B D =1,4 e -0.09(1) + 1,4 e -0.095(2) +(21,4) e -0.10(3) = $18.3 εκ

+ 1,4 e (2) +(21,4) e -0.10(3) = $18.3 εκ.")

67

Let’s find B F Payment 4% on ¥2,400 million, thus ¥96 million C 1 = C 2 = C 3 = ¥96 million P = ¥2.400 million. r 1 = 0,035r 2 = 0,04r 3 = 0,045 t 1 = 1 t 2 = 2 t 3 = 3 B F =96 e -0.035(1) + 96 e -0.04(2) + (2.496) e -0.045(3) = 2.362,5 εκ

+ 96 e -0.04(2) + (2.496) e (3) = 2.362,5 εκ.")

68

Swap Value Bank receives foreign currency and pays domestic V Swap =S 0 B F – B D B F = ¥ 2,362.5 million B D = $18.3 million S 0 = (1/115) V Swap =(1/115) (2,362.5) – (18.3) = $2.25 million

V Swap =(1/115) (2,362.5) – (18.3) = $2.25 million")

Similar presentations