Download presentation

Presentation is loading. Please wait.

2

NEW FRONTIERS FOR ARCH MODELS Prepared for Conference on Volatility Modeling and Forecasting Perth, Australia, September 2001 Robert Engle UCSD and NYU

3

The First ARCH Model Rolling Volatility or “Historical” Volatility Estimator – Weights are equal for j<N – Weights are zero for j>N – What is N?

4

1982 ARCH Paper Weights can be estimated ARCH(p)

")

5

WHAT ABOUT HETEROSKEDASTICITY?

6

EXPONENTIAL SMOOTHER Another Simple Model – Weights are declining – No finite cutoff – What is lambda? (Riskmetrics=.06)

.")

7

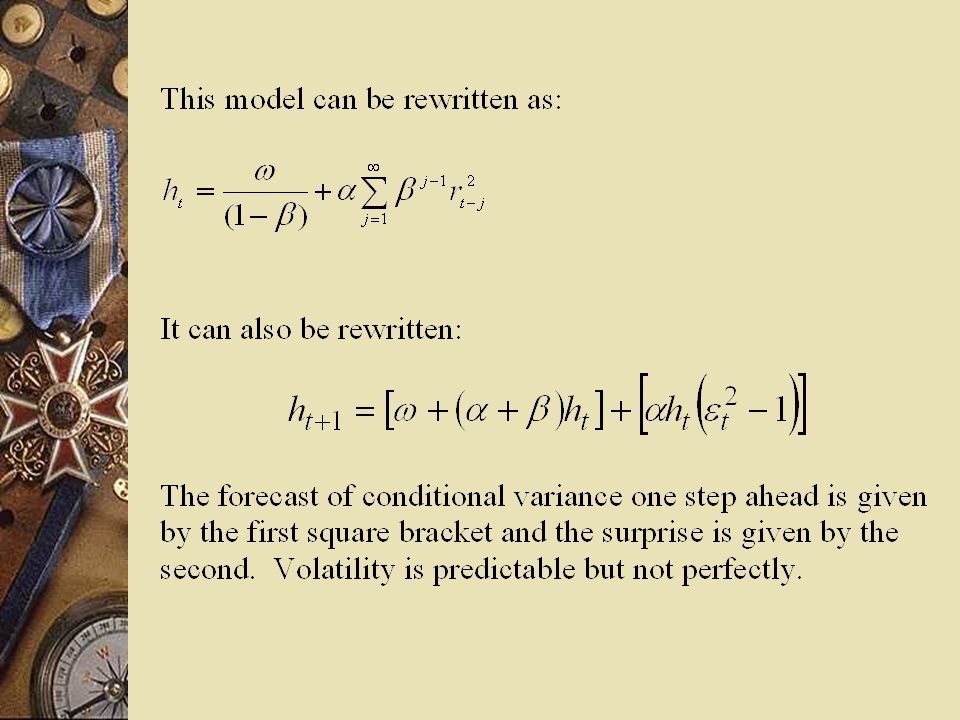

The GARCH Model The variance of r t is a weighted average of three components – a constant or unconditional variance – yesterday’s forecast – yesterday’s news

10

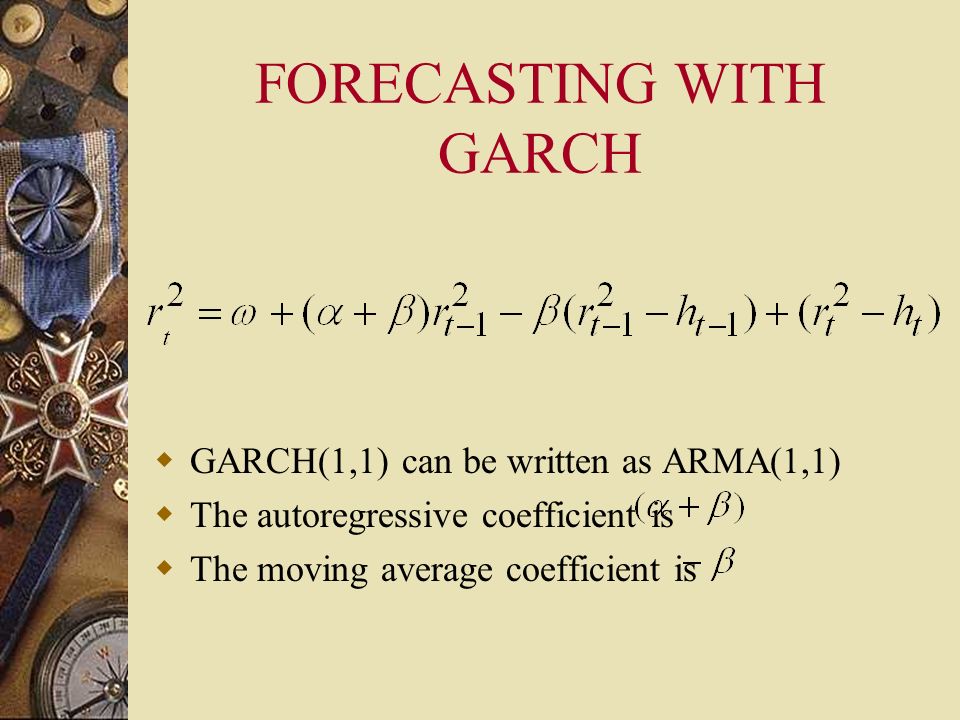

FORECASTING WITH GARCH GARCH(1,1) can be written as ARMA(1,1) The autoregressive coefficient is The moving average coefficient is

can be written as ARMA(1,1) The autoregressive coefficient is The moving average coefficient is")

11

GARCH(1,1) Forecasts

Forecasts")

12

Monotonic Term Structure of Volatility

13

FORECASTING AVERAGE VOLATILITY Annualized Vol=square root of 252 times the average daily standard deviation Assume that returns are uncorrelated.

14

TWO YEARS TERM STRUCTURE OF PORT

16

Variance Targeting Rewriting the GARCH model where is easily seen to be the unconditional or long run variance this parameter can be constrained to be equal to some number such as the sample variance. MLE only estimates the dynamics

17

The Component Model Engle and Lee(1999) q is long run component and (h-q) is transitory volatility mean reverts to a slowly moving long run component

q is long run component and (h-q) is transitory volatility mean reverts to a slowly moving long run component")

18

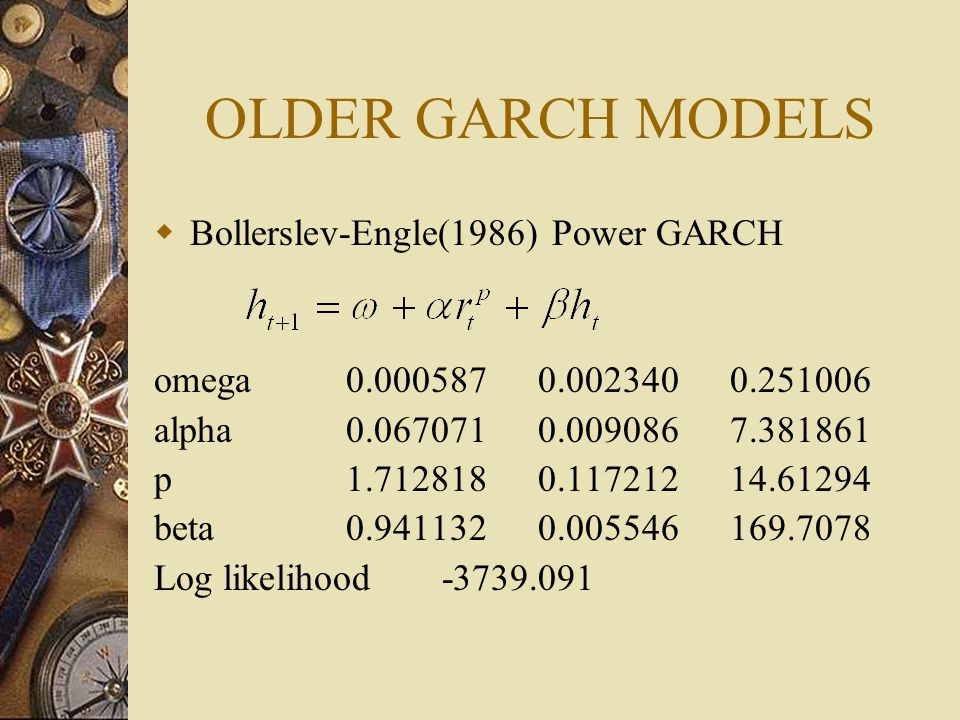

MORE GARCH MODELS CONSIDER ONLY SYMMETRIC GARCH MODELS ESTIMATE ALL MODELS WITH A DECADE OF SP500 ENDING AUG 2 2001 GARCH(1,1), EGARCH(1,1), COMPONENT GARCH(1,1) ARE FAMILIAR

, EGARCH(1,1), COMPONENT GARCH(1,1) ARE FAMILIAR")

20

OLDER GARCH MODELS Bollerslev-Engle(1986) Power GARCH omega0.0005870.0023400.251006 alpha0.0670710.0090867.381861 p 1.7128180.11721214.61294 beta0.9411320.005546169.7078 Log likelihood-3739.091

Power GARCH omega alpha p beta Log likelihood")

21

PARCH Ding Granger Engle(1993) omega0.0066800.0016534.041563 alpha 0.0649300.00560811.57887 gamma0.6656360.0828148.037719 beta 0.9416250.005211180.704 Log likelihood-3738.040

omega alpha gamma beta Log likelihood")

22

TAYLOR-SCHWERT Standard deviation model omega0.0076780.0016674.605529 alpha0.0652320.00521212.51587 beta 0.9425170.005104184.6524 Log likelihood-3739.032

24

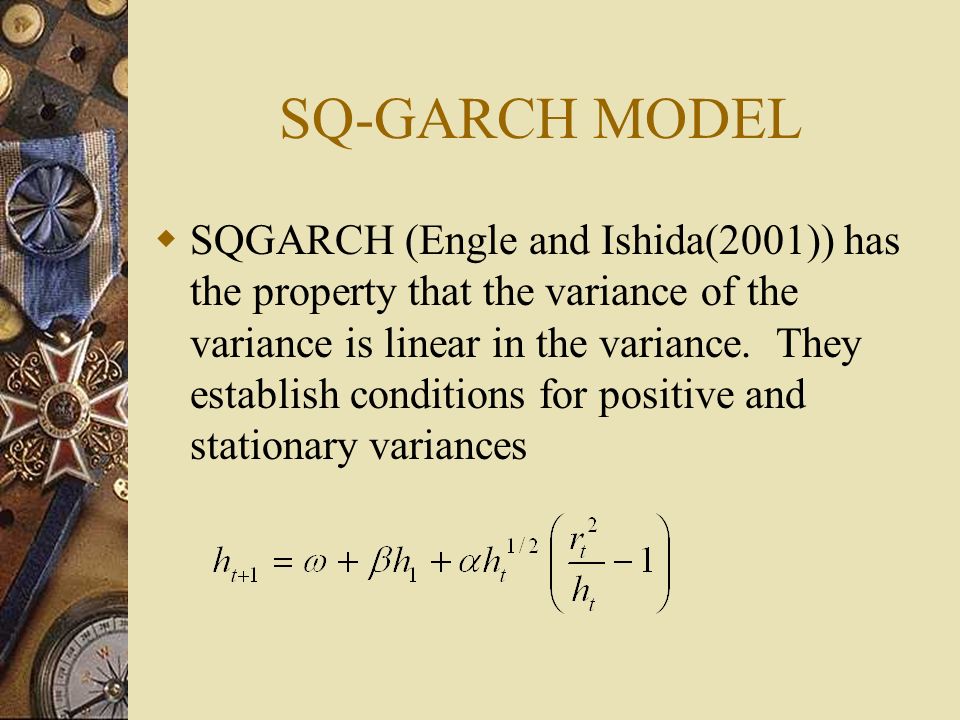

SQ-GARCH MODEL SQGARCH (Engle and Ishida(2001)) has the property that the variance of the variance is linear in the variance. They establish conditions for positive and stationary variances

25

SQGARCH LogL: SQGARCH Method: Maximum Likelihood (Marquardt) Date: 08/03/01 Time: 19:47 Sample: 2 2928 Included observations: 2927 Evaluation order: By observation Convergence achieved after 12 iterations Coefficient Std. Errorz-StatisticProb. C(1)0.0088740.0015965.5602360.0000 C(2)0.0418780.00368511.363830.0000 C(3)0.9900800.001990497.58500.0000 Log likelihood-3747.891 Akaike info criterion2.562960 Avg. log likelihood-1.280455 Schwarz criterion2.569090 Number of Coefs.3 Hannan-Quinn criter.2.565168

C(2) C(3) Log likelihood Akaike info criterion Avg. log likelihood Schwarz criterion Number of Coefs.3 Hannan-Quinn criter")

26

CEV-GARCH MODEL The elasticity of conditional variance with respect to conditional variance is a parameter to be estimated. Slight adjustment is needed to ensure positive variance forecasts.

27

NON LINEAR GARCH THE MODEL IS IGARCH WITHOUT INTERCEPT. HOWEVER, FOR SMALL VARIANCES, IT IS NONLINEAR AND CANNOT IMPLODE FOR

28

NLGARCH LogL: NLGARCH Method: Maximum Likelihood (Marquardt) Date: 08/18/01 Time: 11:27 Initial Values: C(2)=0.05464, C(4)=0.00035, C(1)=2.34004 Convergence achieved after 32 iterations CoefficientStd. Errorz-StatisticProb. alpha0.0541960.00474911.411580.0000 gamma0.0012080.0019350.6242990.5324 delta3.1940724.4712260.7143620.4750 Log likelihood-3741.520 Akaike info criterion2.558606 Avg. log likelihood-1.278278 Schwarz criterion2.564737 Number of Coefs.3 Hannan-Quinn criter.2.560814

30

Asymmetric Models - The Leverage Effect Engle and Ng(1993) following Nelson(1989) News Impact Curve relates today’s returns to tomorrows volatility Define d as a dummy variable which is 1 for down days

following Nelson(1989) News Impact Curve relates today’s returns to tomorrows volatility Define d as a dummy variable which is 1 for down days")

31

NEWS IMPACT CURVE

32

Other Asymmetric Models

33

PARTIALLY NON-PARAMETRIC ENGLE AND NG(1993)

")

34

EXOGENOUS VARIABLES IN A GARCH MODEL Include predetermined variables into the variance equation Easy to estimate and forecast one step Multi-step forecasting is difficult Timing may not be right

35

EXAMPLES Non-linear effects Deterministic Effects News from other markets – Heat waves vs. Meteor Showers – Other assets – Implied Volatilities – Index volatility MacroVariables or Events

36

STOCHASTIC VOLATILITY MODELS Easy to simulate models Easy to calculate realized volatility Difficult to summarize past information set How to define innovation

37

SV MODELS Taylor(1982) beta=.997 kappa=.055 Mu=0

beta=.997 kappa=.055 Mu=0")

38

Long Memory SV Breidt et al, Hurvich and Deo d=.47 kappa=.6

39

Breaking Volatility Randomly arriving breaks in volatility mu=-0.5 kappa=1 p=.99

Similar presentations

Material.>")

: Introduction to Financial Time Series May 2011 Instructor: Maksym Obrizan Lecture notes II.>")