Download presentation

Presentation is loading. Please wait.

1

SEPTIAN BAYU K. (0806479080) Detecting Earnings Management Dechow, Sloan, Sweeney (1995)

Detecting Earnings Management Dechow, Sloan, Sweeney (1995)")

2

Outline Introduction Statistical Background Measuring DA Experimental Design Data Analysis Empirical Results Conclusions Implications

3

Introduction (1) Analysis of earnings management focuses on discretionally accruals (DA) Separate total accruals to DA & NDA The aim of research Finding the sophisticated model(s) to measure to detect earnings management with DA/NDA Research gap Modified Jones Model

Analysis of earnings management focuses on discretionally accruals (DA) Separate total accruals to DA & NDA The aim of research Finding the sophisticated model(s) to measure to detect earnings management with DA/NDA Research gap Modified Jones Model")

4

Introduction (2) Prior research DA: Healy (1995), DeAngelo (1996), Jones (1991) Accounting procedure changes: Healy (1985), Healy & Palepu (1990), Sweeney (1994) Specific components of DA: McNichols & Wilson (1988), DeAngelo et al (1994) Components of Discretionary Cash Flow (Dechow & Sloan (1991)

Prior research DA: Healy (1995), DeAngelo (1996), Jones (1991) Accounting procedure changes: Healy (1985), Healy & Palepu (1990), Sweeney (1994) Specific components of DA: McNichols & Wilson (1988), DeAngelo et al (1994) Components of Discretionary Cash Flow (Dechow & Sloan (1991)")

5

Statistical Background McNichols & Wilson (1988) Problems: Incorrectly attributing earnings management to PART Unintentionally extracting earnings management caused by PART Low power test

Problems: Incorrectly attributing earnings management to PART Unintentionally extracting earnings management caused by PART Low power test")

6

Measuring DA (1) The Healy model (Healy, 1985) The DeAngelo model (DeAngelo, 1986) NDAτ = TAτ-1 The Jones model (Jones, 1991)

The Healy model (Healy, 1985) The DeAngelo model (DeAngelo, 1986) NDAτ = TAτ-1 The Jones model (Jones, 1991)")

7

Measuring DA (2) The Modified Jones model The Industry model (Dechow & Sloan, 1991) NDA τ = γ 1 + γ 2 median 1 (TA τ)

The Modified Jones model The Industry model (Dechow & Sloan, 1991) NDA τ = γ 1 + γ 2 median 1 (TA τ)")

8

Experimental Design Randomly 1000 firm-years (1950-1991) Firm-years experiencing extreme financial performance Firm-years with accrual manipulation Expense manipulation Revenue manipulation Margin manipulation 32 firms that are subject to SEC enforcement actions

Firm-years experiencing extreme financial performance Firm-years with accrual manipulation Expense manipulation Revenue manipulation Margin manipulation 32 firms that are subject to SEC enforcement actions")

9

Data Analysis Total accruals (TA) CFO = Earnings – TA Using Z-statistic

CFO = Earnings – TA Using Z-statistic")

10

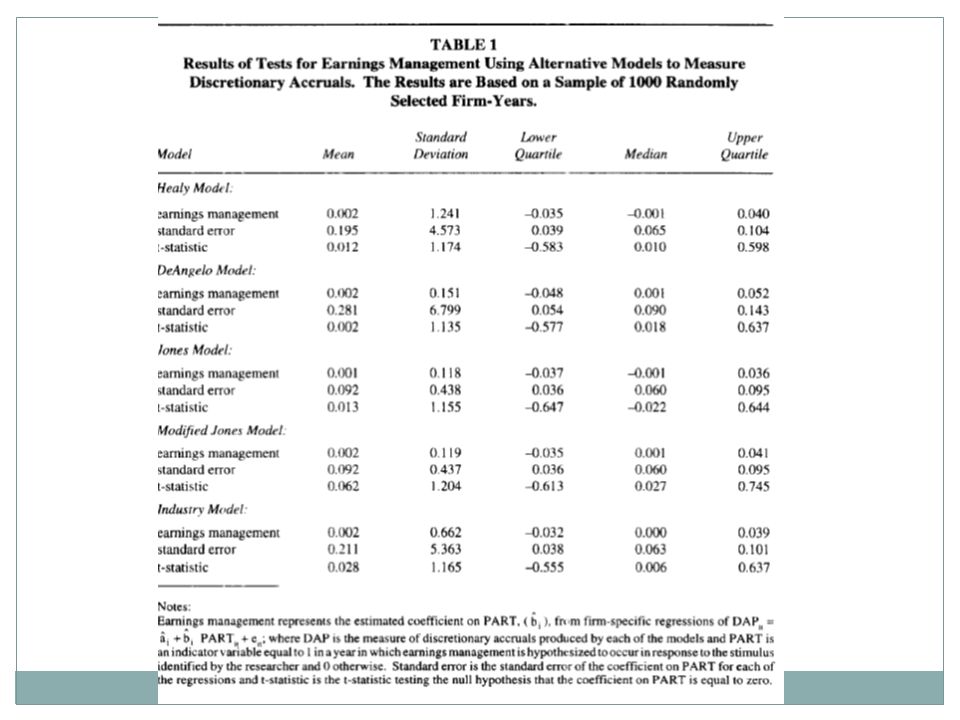

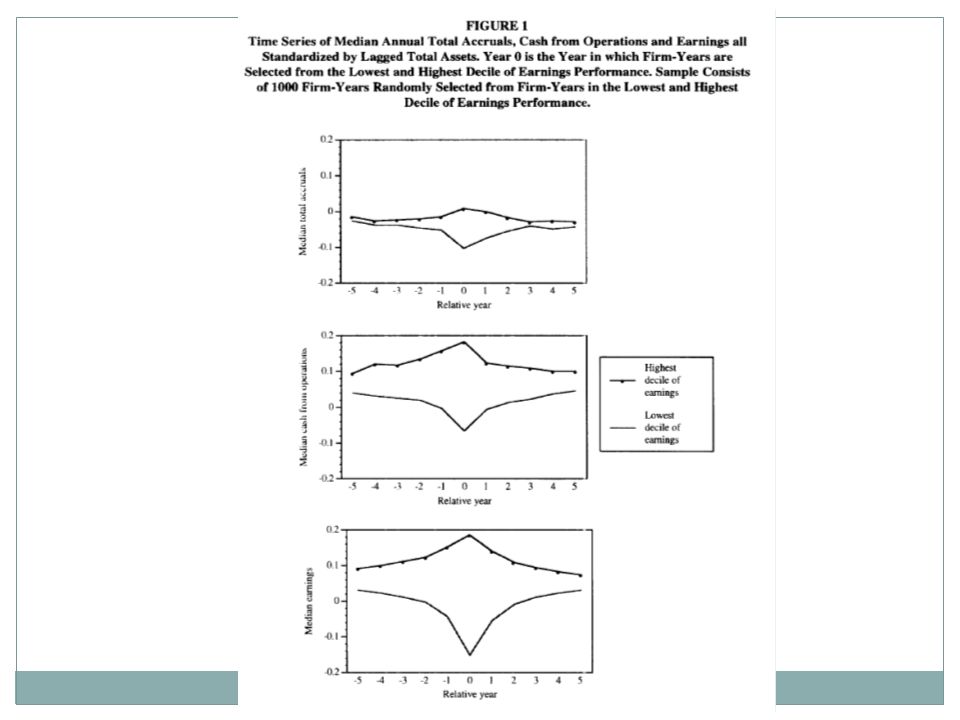

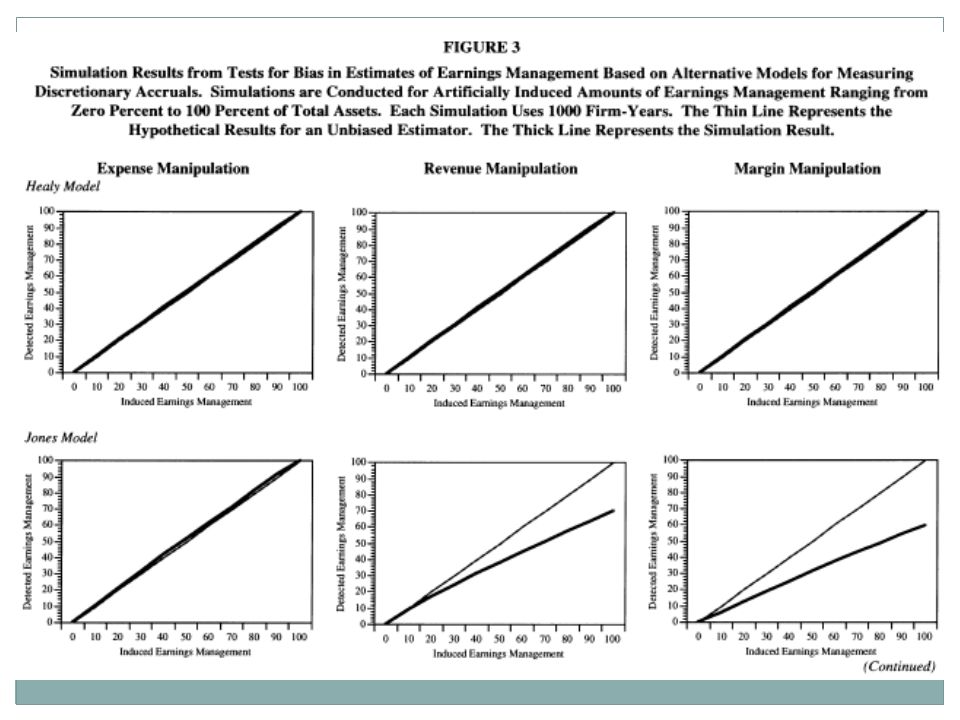

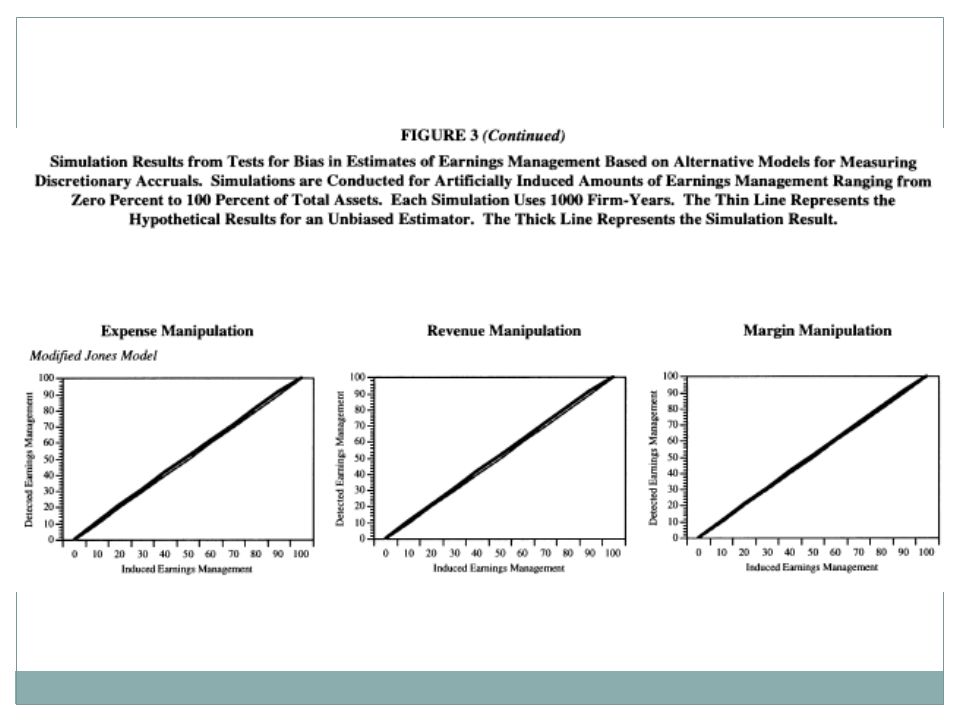

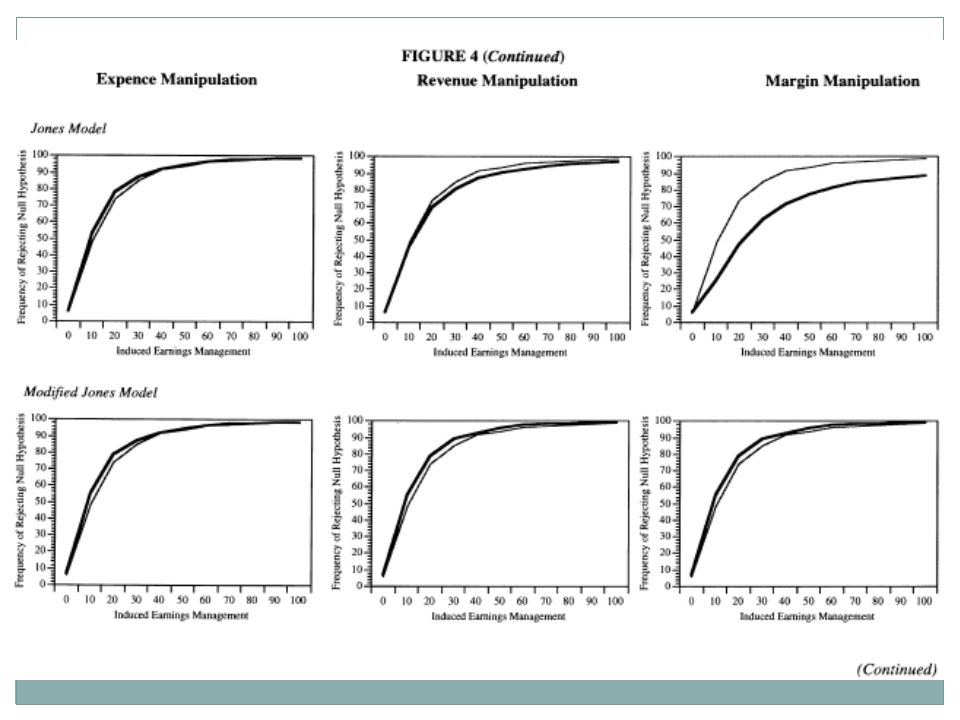

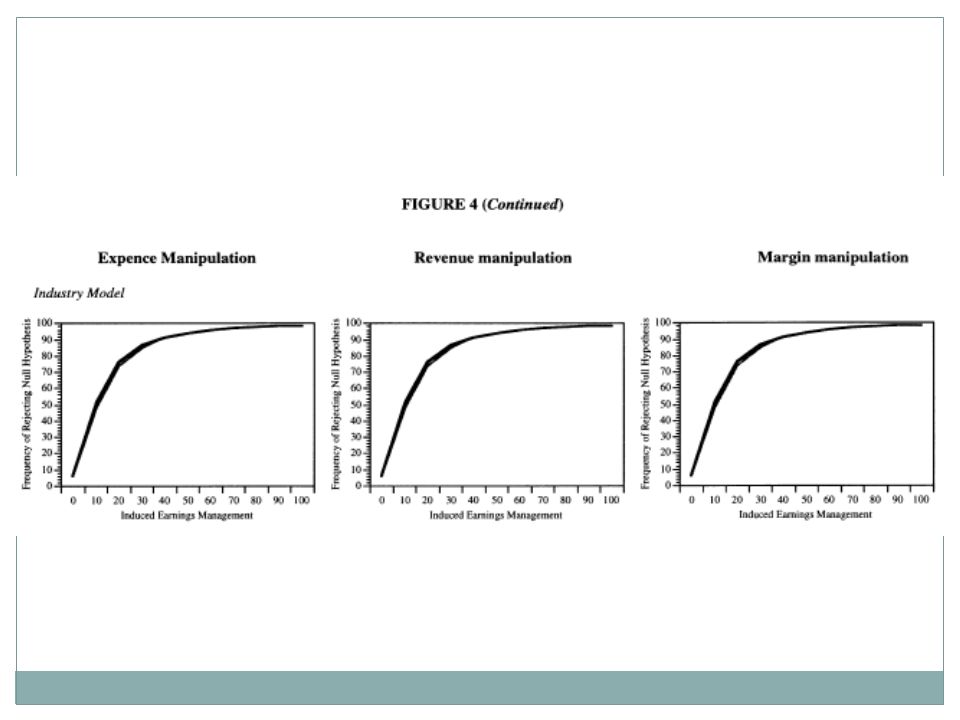

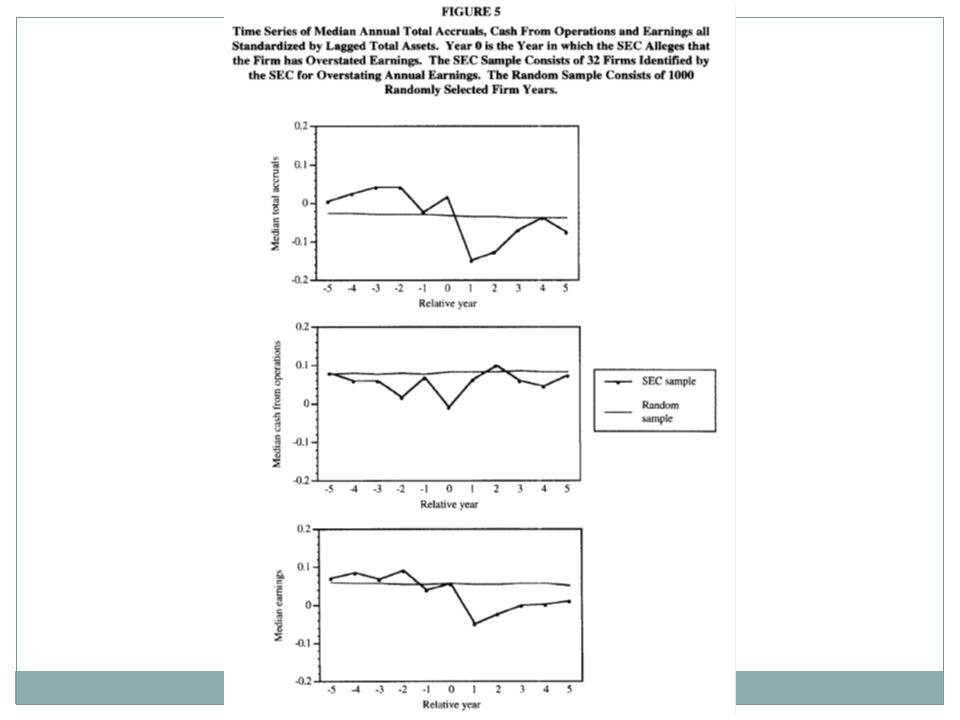

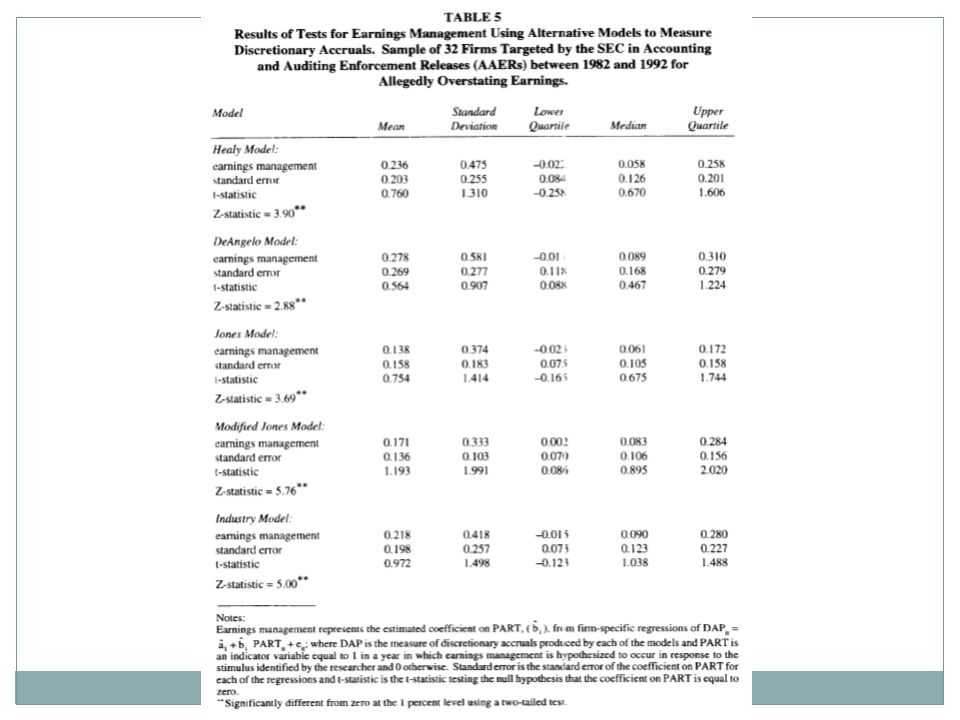

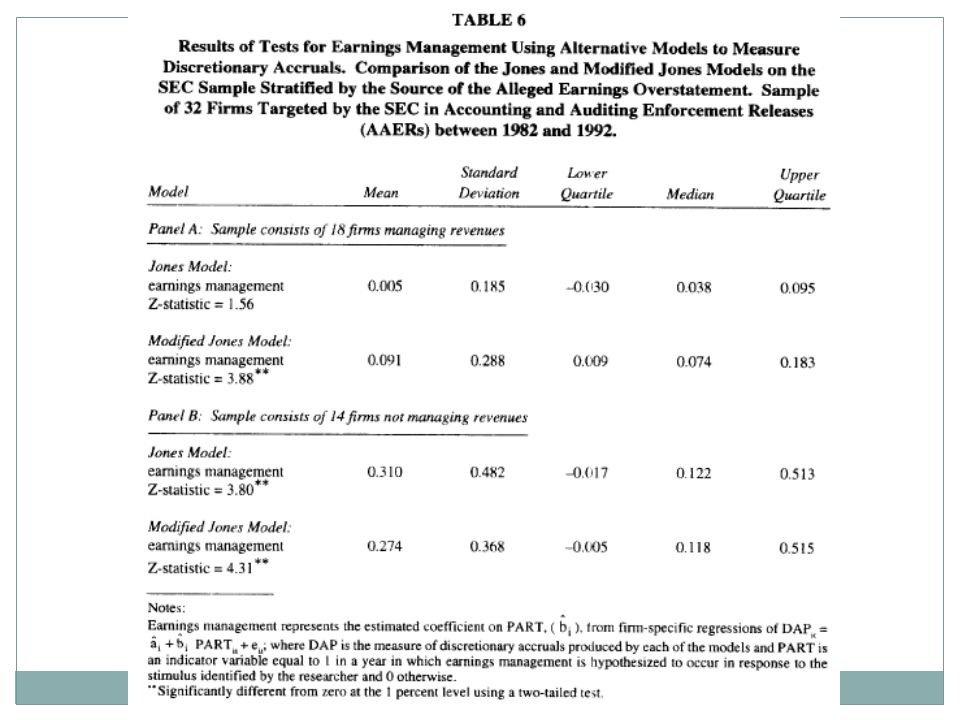

Empirical Results Random sample of firm-years Table 1, table 2 Samples of firm-years experiencing extreme financial performance Figure 1, table 3, figure 2, table 4 Samples of firm-years with artificially induced earnings management Figure 3, figure 4 Sample of firm-years in which of the SEC alleges earnings are overstated Figure 5, table 5, table 6, table 7

26

Conclusions All of models appear well specified when applied to random sample of the firm-years The models all generate test of low power of earnings management All models reject the null hypothesis of no earnings management Modified Jones model generate the revenue –based earnings management

27

Implications Regardless of the model used to detect earnings management Further research: develop new model with more powerful test to detect earnings management Correlation between PART ad firm performance, considered the models Consider about earnings management context

Similar presentations