Download presentation

Presentation is loading. Please wait.

1

Switching from NEST to PFG Retirement Plan David Berry Group Pensions Manager

2

Welcome to the PFG Retirement Plan The PFG Retirement Plan (the Plan) could be an employee’s biggest asset and their main source of income in retirement. Membership is by invitation (valid for 3 months only) to employees on completion of 2 years’ membership of the NEST Scheme. Management colleagues will receive an invitation to join the Plan shortly after employment (valid until the 1st of the month following the completion of 2 months’ Company service). Employees are only be able to join the Plan by invitation as described above.

to employees on completion of 2 years’ membership of the NEST Scheme. Management colleagues will receive an invitation to join the Plan shortly after employment (valid until the 1st of the month following the completion of 2 months’ Company service). Employees are only be able to join the Plan by invitation as described above..")

3

Agenda What the Plan can offer you How the Plan works Contributions and SmartPension Investments Taking benefits/Pensions Flexibility Where to get more information

4

What The Plan Can Offer You? (1) Tax-Free Contributions into the Plan A Company pension contribution of up to 10.6% of your basic salary Tax-free contributions into the Plan Contributions that are exempt from National Insurance if paid by SmartPension (a more efficient way of paying contributions) Up to 25% of your fund value as tax free lump sum when you take your pension

Tax-Free Contributions into the Plan A Company pension contribution of up to 10.6% of your basic salary Tax-free contributions into the Plan Contributions that are exempt from National Insurance if paid by SmartPension (a more efficient way of paying contributions) Up to 25% of your fund value as tax free lump sum when you take your pension.")

5

What The Plan Can Offer You? (2) Protection For Your Family Your fund is payable to your dependants on death before retirement The option to secure a dependant’s income when you take your benefits Life assurance equal to 3 x your basic salary Group Income Protection scheme which has a benefit of 50% of salary payable after 26 weeks illness up to State Pension Age

Protection For Your Family Your fund is payable to your dependants on death before retirement The option to secure a dependant’s income when you take your benefits Life assurance equal to 3 x your basic salary Group Income Protection scheme which has a benefit of 50% of salary payable after 26 weeks illness up to State Pension Age.")

6

Personal Ownership Your Pension Policy and all contributions belong to you, not the Company You can cease your membership at any time but will not have a right to rejoin the Plan at a later date You do not need to stop working to start receiving your benefits The Plan includes all of the Pensions Flexibility options introduced by the Government in April 2015 – more later Your fund is transferable to other suitable pension arrangements If you leave the scheme or retire whilst in employment the Company may be required to automatically re-enrol you into NEST

7

How the Plan Works (1) EMPLOYER CONTRIBUTION (up to 10.6%) MEMBER CONTRIBUTION (up to 8%) Investment Return Tax Relief MEMBER’S ACCOUNT

EMPLOYER CONTRIBUTION (up to 10.6%) MEMBER CONTRIBUTION (up to 8%) Investment Return Tax Relief MEMBER’S ACCOUNT")

8

How the Plan Works (2) INCOME IN RETIREMENT INCLUDING FLEXIBLE OPTIONS POST APRIL 2015 …... TAX FREE CASH * MEMBER’S ACCOUNT

9

Contributions as percentage of salary Member Contribution or Salary Exchanged Company Contribution Non SmartPension Company Contribution with SmartPension 3%5%5.1% + 3% = 8.1% 4%6%6.2% + 4% = 10.2% 5%7%7.3% + 5% = 12.3% 6%8%8.4% + 6% = 14.4% 7%9%9.5% + 7% = 16.5% 8% (Maximum)10%10.6% + 8% = 18.6%

10%10.6% + 8% = 18.6%")

10

SmartPension (1) SmartPension is the way contributions are made to the plan. SmartPension benefits you in two ways: - You pay less NI, resulting in an increase in your take-home pay. - A higher rate of Company contributions is paid into your pension fund

11

SmartPension (2) Taking an example of someone earning £1,000 per month who pays a 5% personal contribution. Without SmartPensionUsing SmartPension Monthly basic salary£1,000.00£950.00 Income Tax £23.33 £13.33 National Insurance £39.40 £33.40 Pension Deduction £40.00 £0.00 Take home pay £897.26 £903.27 Total Invested £120.00 £123.00

12

SmartPension (3) Your salary before SmartPension is known as your Reference Salary and will be used in the calculation of all Company benefits and pay reviews. The reduction in salary is a change to your contractual salary and so any State benefits to which you may be entitled will be based on the lower amount. You are not required to contribute via SmartPension. If you choose not to use SmartPension, you will continue to pay tax and NI on your gross pay. Your contributions will be deducted from your take home pay, net of basic rate tax, and will automatically receive basic rate tax relief once invested.

13

Investment Options (1) How hands-on do you wish to be? The Plan’s investment fund range has been structured to help make it accessible to all members, regardless of how hands-on they wish to be with their investment decision. We have shown the investment options in the pyramid below: Top Tier - Default Option Second Tier - Alternative Option Third Tier - Core Funds Fourth Tier - Full Fund Range Full information on all of the funds can be found on the pension website at www.pfpensions.co.uk www.pfpensions.co.uk

14

Investment Options (2) Top tier – the default option The Balanced II Lifestyle Profile is designed for those members with a medium attitude to investment risk and little desire to be hands on with their investments. This option is most suitable for those looking to take tax free cash and purchase an annuity when they retire. Second tier – alternative option The MyFolio Market IV Pension Fund is an alternative to the default lifestyle option designed for those members who wish to take marginally more investment risk, and does not include lifestyling as retirement approaches.

15

Investment Options (3) Third tier – core funds A core list of some of Standard Life’s pension funds has been selected following advice from an Independent Financial Adviser. Fourth tier – the full fund range You are not restricted to the above options. The full range of Standard Life’s funds is also available for those who wish to be very hands on.

16

Investment Options (4) If you do not make an investment decision, you will be invested in the Default Option. The Plan’s investment fund range has been selected following advice from an Independent Financial Adviser to help members decide on suitable investments. Ultimately, you must be comfortable that the investment choice you have made is right for you, whichever tier you opt for, or even if you do not make an active decision. The default options are currently being reviewed in light of recent government proposals and may change in the future.

17

Default Investment Option

20

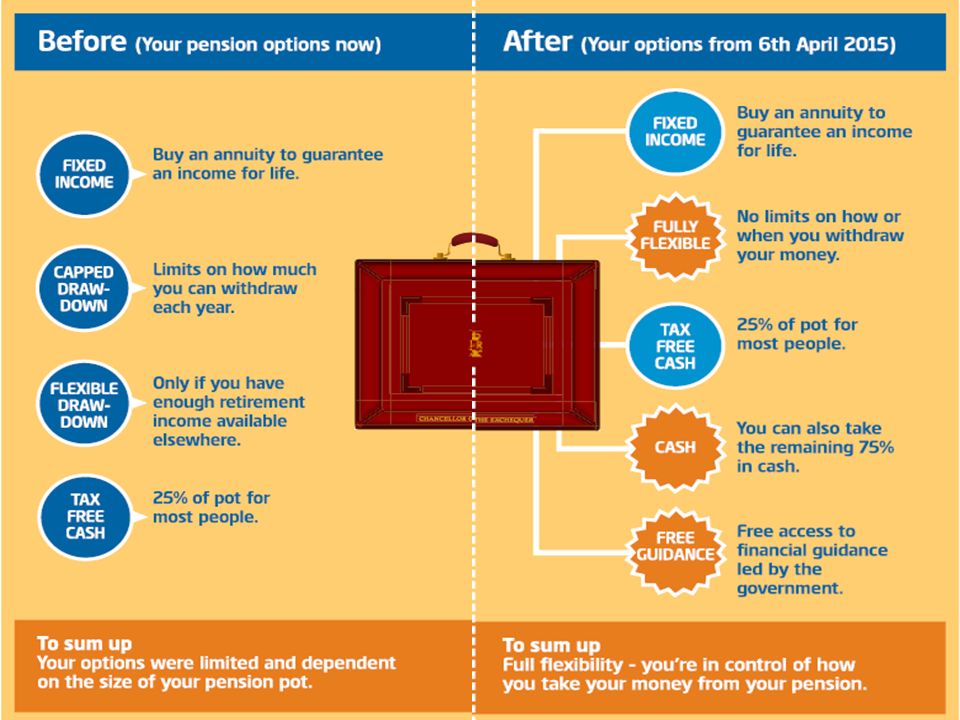

New Retirement Choices From April 2015 Pensions Freedom and Choice or Pensions Flexibility was introduced The PFG Retirement Plan offers all the Flexibility options

22

The PFG Retirement Plan is simply a Tax-Effective Retirement Savings Account When you join the Plan, an Account is opened in your name You and the Company make payments into your Account The money in your Account is invested tax- efficiently £ ££ From age 55 you can choose how to use the fund – cash it in, take a series of cash payments, keep the funds invested and draw down an income or buy an annuity or a mixture.

23

What if you don’t join? If you do not join the Plan at your first opportunity you will have no right to join at a later date and you will reduce the level of protection should you die or fall ill. Non pension scheme members are covered for a reduced level of life assurance of 1 x basic salary and are not covered by the Group Income Protection scheme. If you choose not to join you loose valuable benefits provided by the Company (and the Company saves the cost of those benefits).

..")

24

Contributions cost less than you think Employee paid £1,000 per month pays 3% contribution through SmartPension. The weekly cost is: Tax relief£1.38 NI Smart saving £0.83 Cost to you£4.71 Contribution£6.92

25

More Information Read the Provident Pensions Website http://www.pfpensions.co.uk/ http://www.pfpensions.co.uk/ Read the Member and Investment Guide Read the Standard Life micro-site Read the Standard Life Investment Guide Ask questions – now or later via HR or: pensionenquiries@providentfinancial.com Telephone: 01274 351351

Similar presentations

>")