Download presentation

Presentation is loading. Please wait.

1

Credit Card Numbers in the US

American Express: 38 million Visa: 109 million cards Discover: 49 million MasterCard: 82 million Total US credit Debt in 2014: $700 BILLION Market Share Visa MasterCard American Express Discover The definition of a brand is the sum total of the consumer experience that goes along with it: everything a company says, everything it does, and how it says and does it. American Express added 1.5 million cardholders in the quarter, giving it 72.5 million. Of these, about three-fifths are in the United States. Source: “American Express profit up 18 pct as cards rise,” April 24, 2006. Visa USA is the nation's leading payment brand and largest payment system. Through its 13,420 member financial institutions, more than 488 million Visa-branded cards have been issued to cardholders in the United States. Worldwide, cardholders in more than 150 countries carry more than 1 billion Visa-branded cards, accounting for more than $3 trillion in annual transaction volume. Source: April 2006. Discover Card is a credit card issued primarily in the United States, with 50 million cardholders. The Discover Card was originally introduced by Sears in 1985, and is today operated as a subsidiary of Morgan Stanley. Discover is headquartered in Riverwoods, Illinois. While Discover brand cards are not currently accepted in Europe, the company's presence continues to grow in Mexico, Costa Rica, Micronesia, the Marshall Islands, Belize, Palau, and many of the Caribbean Island nations. Source: Wikipedia, the free encyclopedia, “Discover Card,” April 2006. Founded as the Interbank Card Association (ICA) "Master Charge," purchased by the California Bank Association Renamed MasterCard to reflect a commitment to international growth MasterCard International manages a family of well-known, widely accepted payment cards brands including MasterCard®, Maestro® and Cirrus® and serves financial institutions, consumers and businesses in over 210 countries and territories. At year-end, MasterCard's almost 25,000 customer financial institutions around the world had issued million MasterCard-branded cards, a 10.5 percent increase over MasterCard cardholders can use their cards at more than 24 million acceptance locations around the world Source: April 2006

Master Charge, purchased by the California Bank Association Renamed MasterCard to reflect a commitment to international growth. MasterCard International manages a family of well-known, widely accepted payment cards brands including MasterCard®, Maestro® and Cirrus® and serves financial institutions, consumers and businesses in over 210 countries and territories. At year-end, MasterCard s almost 25,000 customer financial institutions around the world had issued million MasterCard-branded cards, a 10.5 percent increase over MasterCard cardholders can use their cards at more than 24 million acceptance locations around the world. Source: April")

2

The True Cost of Paying the Minimum Payment

Payment Schedule: If you start with a debt of and make the minimum payment each month it will take you 8 years and 1 month to be rid of your debt. In that time, you will pay $ in interest. Month Minimum Payment Interest Paid Principal Paid Remaining Balance 1 $14.25 $8.55 $5.70 $564.30 2 $14.11 $8.46 $5.64 $558.66 3 $13.97 $8.38 $5.59 $553.07 4 $13.83 $8.30 $5.53 $547.54 5 $13.69 $8.21 $5.48 $542.06 6 $13.55 $8.13 $5.42 $536.64 This is an amortization table that breaks down how slowly you make progress paying off the balance when you only make the minimum payment. Most important fact is to pay your credit card off every month and not pay interest. Source:

3

The Credit Card Industry

$40 billion in profits in 2010 $12 billion in fees Most credit card companies are more profitable than places like McDonalds and Microsoft Credit Card Industry is the most profitable sector of banking. 30% of profits come from fees. Annual Fee: Usually for mileage, etc. Late Fee: Small window to send out payment Over-the-limit fee Annual Fees Cash-advance fees Merchant Fees Source: Who has heard of MBNA yet it is 1.5X more profitable than McDonalds? Citibank more profitable than the world’s largest software company and retail store.

4

Market Control 5 companies control 65% of the market: American Express

Bank of America Citigroup JP Morgan Chase MBNA VISA A wave of mergers has ensued, consolidating power in the hands of a few players who set take-it or leave-it terms for consumers. Prior to 1978 the top 50 issuers represented 50 percent of the credit-card market, but by mid-2005 only five companies, American Express, Bank of America, Citigroup, JPMorgan Chase, and MBNA, controlled 65 percent of the market. “The impending marriage of MBNA and Bank of America will further narrow the circle of big players; consumers can expect to be squeezed even harder by rising rates and fees,” warns Robert D. Manning, professor of finance at Rochester Institute of Technology and author of “Credit Card Nation.” Source: “Credit cards: They really are out to get you,” Consumer Reports, November 2005

5

Affinity Cards A credit card offered by two groups, one a financial institution and the other a non-financial institution, such as a College Airline Non-profit group Tim Hortans West Jet Affinity Card: A credit card offered by two groups, one a financial institution and the other a non-financial institution, such as a college or an airline. Schools, nonprofit groups, pro wrestlers, popular singers and airlines are among those featured on affinity cards. Usually, use of the card entitles holders to special discounts or deals from the non-financial group.

6

What’s Next? Life After High School

Graph Source: Higher Education Coordinating Board Teacher note: Credit card companies target young adults to open credit cards either on a college campus or in many retail locations. No matter what you do after high school, most likely a credit card will be marketed to them. However, the focus of this presentation is for students going to a college campus. After years of saving for college, parents mail off the check for the first semester, and are ready to pack your budding scholar off to school. They think their college money worries are over. However, the real financial aid crisis may just be starting. After years of spending under their parents’ watchful eyes, students are heading off into uncharted, unsupervised economic territory, marked by unexpected expenses, easy access to credit cards and near-infinite temptations to squander money. It all adds up to perfect conditions for financial trouble--misadventures that often climax in phone calls home begging for a bailout. Source: Mannes, George “I Owe U,” Money – Online, September 2005.

7

Why Students Use Credit Cards

The rising costs of higher education, coupled with decreases in many families’ liquid savings, have led to increasing dependence on educational loans and other forms of borrowing. This contributes to a “cognitive disconnect” for students between the reality of their current incomes and what constitutes an affordable lifestyle. Source: Manning, Robert. “Living with Debt: A Life Stage Analysis of Changing Attitudes and Behaviors,” The post-World War II American Dream is based upon the twin pillars of higher education (vocational, junior college, university) and homeownership. Both entail personal sacrifice, long-term planning, and increasingly higher levels of debt. Over the past generation, however, these exalted accoutrements of middle-class status have become increasingly difficult to achieve. Today, baby boomers have found that homeownership requires two incomes rather than one and typically a 30-year rather than a 10 or 15-year mortgage. Furthermore, the modest cost of the boomers’ college education stands in sharp contrast to the pricey reality of their children’s. Source: Manning, Robert, Credit Card Nation, 2000, p 163. An increase in college costs and a decrease in families’ liquid savings leads to a dependence on loans & credit cards. Students have a cognitive disconnect between the: Reality of their current incomes vs. an affordable lifestyle

and homeownership. Both entail personal sacrifice, long-term planning, and increasingly higher levels of debt. Over the past generation, however, these exalted accoutrements of middle-class status have become increasingly difficult to achieve. Today, baby boomers have found that homeownership requires two incomes rather than one and typically a 30-year rather than a 10 or 15-year mortgage. Furthermore, the modest cost of the boomers’ college education stands in sharp contrast to the pricey reality of their children’s. Source: Manning, Robert, Credit Card Nation, 2000, p 163. An increase in college costs and a decrease in families’ liquid savings leads to a dependence on loans & credit cards. Students have a cognitive disconnect between the: Reality of their current incomes vs. an affordable lifestyle.")

8

More Reasons Why Students Use Credit Cards

Students want their parents’ lifestyle BUT don’t have the same financial resources. They depend on: Financial Aid Families Part-time work Credit Cards Students also rely on their families for money or financial aid/loans. When expenses exceed allowances, credit cards become the backup.

9

Consumption and Credit

Students don’t embrace “old school” financial values Consumption pressure and easy access to credit Increased social acceptance of debt Credit is a reward Students are not embracing the traditional or “old school” financial values of their parents and grandparents that place emphasis on: Saving Living on a budget Self-denial Instead, intense competitive consumption pressures on college campuses, which are exacerbated by increasingly easy access to consumer credit, has substantially increased the social acceptance of increasing levels of personal debt. Many students view use of consumer credit as a reward for their hard work at school. Source: Manning, Robert. “Living with Debt: A Life Stage Analysis of Changing Attitudes and Behaviors,”

10

Long-term Effects of Credit

Graduate with: Student loans Credit card debt Affect credit score Harder to get: Car loan or insurance Apartment lease Mortgage loan Job The lack of widespread or formal training/education about personal finance in high schools and colleges contributes to a sense of complacency among students, who are not aware of the long-term consequences of their reliance on credit, including its effect on their credit scores. Source: Manning, Robert. “Living with Debt: A Life Stage Analysis of Changing Attitudes and Behaviors,” FICO or credit score: Credit Card Issuers & Lenders Determine APR Auto Insurers Determine Premium Landlords Are you a reliable tenant? Employers Are you a worthy hire?

11

College Students’ Money Problems

College Students Often Have Problems with Money... Many students lack even the most basic money-management skills, say financial aid directors and other college administrators. Source: Chase Education Finance. Mannes, George “I Owe U,” Money – Online, September 2005.

12

Credit Card Use by Year The longer a student is in college, the more students turn to plastic. “Students double their average credit card debt and triple the number of credit cards in their wallets – from the time they arrive on campus until graduation.” College students use credit cards for a variety of reasons: dining, clothing, books, tuition, fees, and other entertainment expenses. Approximately half of colleges allow students to charge tuition and fees, as well as other services. One in five students reports using credit cards to pay for tuition and fees. NOTE: Figures include general-purpose credit cards as well as charge cards from gas stations and retail stores. Source: Nellie Mae. (2002)

")

13

Credit Cards: The “Other” Drug

Marketing of credit cards on campuses poses a greater threat to students future than almost anything else Students with high credit card debt are more likely to: Earn poorer grades Drop out of school Suffer from depression File for bankruptcy Work more hours to pay bills Credit card companies know that even without income, students can carry a balance until they have an income or their parents pay off the balance for them. Students with high consumer debt are more likely to earn poorer grades, drop out of school, suffer from depression, file for bankruptcy, and work more hours to pay their bills. Credit card debt also has been linked to a number of suicides by college students, according to The Journal of Consumer Affairs, Auburn University, Ala. No job? No income? No problem? If you are a student, you will be approved!

14

Preparing for Managing Credit on Your Own

Work income Allowance income Live on a budget at home Food Entertainment Clothing Teacher note: The excerpt below is written for parents, but when presenting this information to students, the emphasis should be on how they can ask their parents to help them prepare for managing money when they move out of the family home. In an ideal world, you would have been teaching your children the rudiments of personal finance from the time they were small, giving them an allowance to build budgeting and saving skills, helping them distinguish between needs and wants and, as they got older, imparting technical expertise, like how to balance a checkbook. At the least, teenagers ought to get a fixed weekly amount to buy their own food, entertainment and clothing, so they get used to living on a budget while still at home. "If you don't give your kid freedom to make choices with money, including stupid choices, he'll make plenty when he gets to college," says John Gardner, a senior fellow at the National Resource Center for the First-Year Experience, which focuses on freshman life. The biggest threats to budgets, say students and financial aid experts, are the innocuous little expenses that add up over time: snacks for the dorm room, dinner out with friends, a daily dose of caffeine. Imagine drinking a $4 latte five days a week, and spending $8 twice a week on pizza and drinks. That's $144 in one month--and your child hasn't even visited the laundry room. Mannes, George “I Owe U,” Money – Online, September 2005.

15

Managing Credit in College

Get one credit card Authorized user on parents’ card Ask parent to cosign card Secured Card Pay off the balance every month Don’t take cash advances Pay on time Given the challenge of keeping spending down, it's not surprising that many students end up with a mountain of credit-card debt. While your instinct may be to urge your child to just say no to plastic, a credit card can be a useful tool for a student--to buy a plane ticket home, for example. Paying the balance in full each month also helps your child establish a good credit record. A compromise: Greenlight a student card with a low limit, say $500. Source: Mannes, George “I Owe U,” Money – Online, September 2005. Another option is to add your child as an authorized user on your own credit card. The parent gets the credit card bill every month and can monitor the student’s spending. The student then writes a check to their parent for the amount they owe or the parent can deduct it from the student’s monthly allowance.

16

Why Credit is Important

FICO or credit score: Credit Card Issuers & Lenders Auto Insurers Determine Premium (Monthly payments) Employers Are you a worthy hire? Landlords Are you a reliable tenant? But these days auto insurers are using credit-based scores to calculate premiums. Employers are using credit checks to determine whether you’re a worthy hire. And landlords are using them to figure out whether you’ll be a reliable tenant. Some utility companies are linking credit scores to the size of the deposit you must pay to have your power turned on. Source: Consumer Reports, “Credit scores: What you don’t know can be held against you ,” August 2005. _________________________________________________________________________________________________________________________ Insurers to set rates. Auto and home insurers often use credit-scoring formulas to help determine premiums. Insurers and independent researchers have found a strong, although still unexplained, correlation between how well people handle their credit and how likely they are to cost the insurer money. Folks with the highest credit scores tend to file the fewest claims; as credit scores deteriorate, the propensity to file claims rises. The practice is controversial (for details, read "Is your insurer discriminating against you?") but widespread; only a few states, including California and Massachusetts, prohibit insurers from using credit information. Source: Pulliam-Weston, Liz, “Demand Your FICO Score Now!,” MSN Money, October 9, 2006.

Employers. Are you a worthy hire Landlords. Are you a reliable tenant But these days auto insurers are using credit-based scores to calculate premiums. Employers are using credit checks to determine whether you’re a worthy hire. And landlords are using them to figure out whether you’ll be a reliable tenant. Some utility companies are linking credit scores to the size of the deposit you must pay to have your power turned on. Source: Consumer Reports, Credit scores: What you don’t know can be held against you , August _________________________________________________________________________________________________________________________. Insurers to set rates. Auto and home insurers often use credit-scoring formulas to help determine premiums. Insurers and independent researchers have found a strong, although still unexplained, correlation between how well people handle their credit and how likely they are to cost the insurer money. Folks with the highest credit scores tend to file the fewest claims; as credit scores deteriorate, the propensity to file claims rises. The practice is controversial (for details, read Is your insurer discriminating against you ) but widespread; only a few states, including California and Massachusetts, prohibit insurers from using credit information. Source: Pulliam-Weston, Liz, Demand Your FICO Score Now!, MSN Money, October 9,")

18

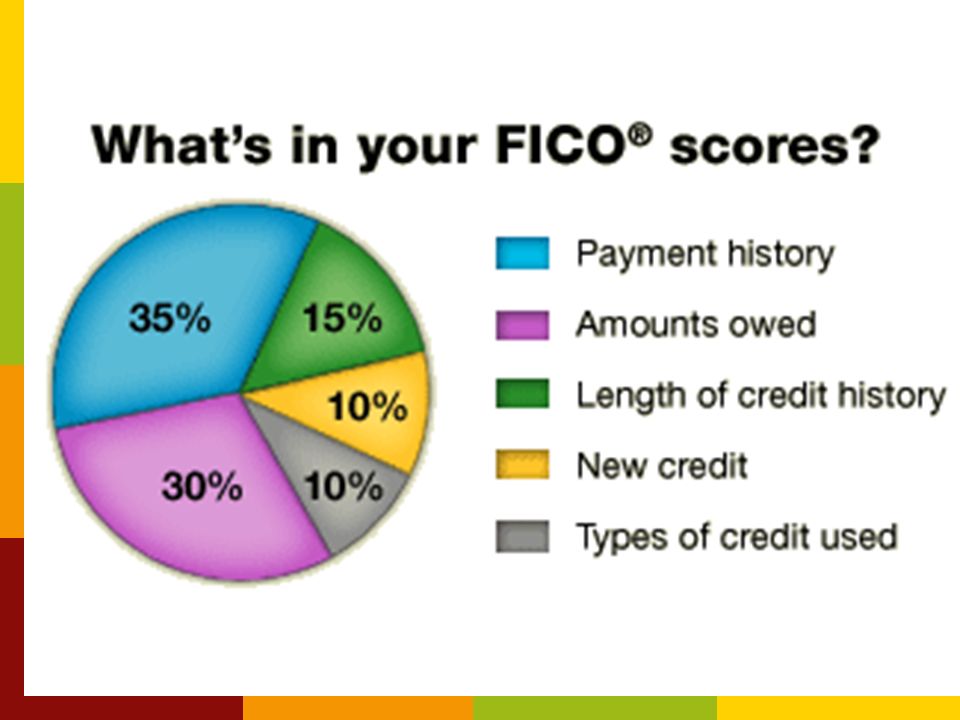

35% Payment History Late payments have the greatest negative impact.

Recency & frequency are important too. Payment history (35%) -Aside from extreme events, like bankruptcy or tax liens, late payments have the greatest negative impact on your score. Recency and frequency of late payments count too. In other words, even though a 60-day late payment is not as risky as a 90-day late payment in and of itself, a 60-day late payment made just a month ago will count more than a 90-day late payment from five years ago.

-Aside from extreme events, like bankruptcy or tax liens, late payments have the greatest negative impact on your score. Recency and frequency of late payments count too. In other words, even though a 60-day late payment is not as risky as a 90-day late payment in and of itself, a 60-day late payment made just a month ago will count more than a 90-day late payment from five years ago.")

19

30% Outstanding Balances

Total balance vs. total available credit. Are you overextended? Outstanding balances (30%) - Evaluation of your total balances in relation to your total available credit on revolving accounts is one of the most important factors in the FICO score. Owing a great deal of money on many accounts or "maxing out" on various credit cards can indicate that a person is overextended, and is more likely to make some payments late or not at all.

- Evaluation of your total balances in relation to your total available credit on revolving accounts is one of the most important factors in the FICO score. Owing a great deal of money on many accounts or maxing out on various credit cards can indicate that a person is overextended, and is more likely to make some payments late or not at all.")

20

15% Length of Credit History

Number of years you’ve used credit. How long since you’ve used certain accounts. Length of credit history (15%) -Your score takes into account how long your credit accounts have been established in general, how long specific credit accounts have been established, and how long it has been since you used certain accounts.

-Your score takes into account how long your credit accounts have been established in general, how long specific credit accounts have been established, and how long it has been since you used certain accounts.")

21

10% New Credit Number of new accounts.

Multiple requests reduce your score. New Credit (10%) -Research shows that opening several credit accounts in a short period of time does represent greater risk-especially for people who do not have a long-established credit history. Multiple requests will reduce your score because it looks like you are either trying to get a high amount of credit (possibly because of a cash flow problem) or that you are being rejected by lenders and having to apply elsewhere.

-Research shows that opening several credit accounts in a short period of time does represent greater risk-especially for people who do not have a long-established credit history. Multiple requests will reduce your score because it looks like you are either trying to get a high amount of credit (possibly because of a cash flow problem) or that you are being rejected by lenders and having to apply elsewhere.")

22

10% Types of Credit Mix of: Revolving Credit Installment Credit

Credit cards Installment Credit Car loan Home loan Types of credit (10%)-The score will consider your mix of credit cards, retail accounts, installment loans, finance company accounts and mortgage loans. Your score takes into account what kinds of credit accounts you have, and how many of each. The score also looks at the total number of accounts you have. Revolving Credit: Creditor places a credit limit for a given period, and the consumer can add charges as long as the credit limit is not exceeded and the account remains in good standing. Another name for open credit. Installment Credit: A loan that is paid in equal monthly installments with a fixed interest rate. Loan payments include principal and finance charges and are a form of closed credit.

-The score will consider your mix of credit cards, retail accounts, installment loans, finance company accounts and mortgage loans. Your score takes into account what kinds of credit accounts you have, and how many of each. The score also looks at the total number of accounts you have. Revolving Credit: Creditor places a credit limit for a given period, and the consumer can add charges as long as the credit limit is not exceeded and the account remains in good standing. Another name for open credit. Installment Credit: A loan that is paid in equal monthly installments with a fixed interest rate. Loan payments include principal and finance charges and are a form of closed credit.")

23

How to Improve Your Score

Pay all bills on time. Pay any delinquent bills. Lower your total credit card debt.

Similar presentations

596-0780 Crestline/Universal Lending.>")