Download presentation

Presentation is loading. Please wait.

1

NIH Salary Cap Department Examples Elizabeth Richardson 02.18.2010

2

Committed effort refers to effort % listed in proposal Budgeted salary costs are based on the cap in effect at time of proposal When awarded: ◦ make any needed adjustments ◦ determine $ amounts for cost sharing ◦ submit on the PS friendly: complete cost-share budget and provide non-sponsored account strings

3

Once combo codes are available, provide payroll with per pay period costs for the project and for cost share Cost-share column will be populated on effort statement once the payroll is posted Timing: Maintain cost-share distributions on an ongoing basis As needed, process HSAs during open effort period

4

Project sPayrollCost-sharingEffortSalary CapActual Salary Project $/pay period Cost-share $/Pay period 0663631523%6%29% 199,700 253,7762227.42603.16 0663645712%3%15% 199,700 253,7761152.12311.98 000064058%2%10% 199,700 253,776767.88207.93 0001306012%3%15% 199,700 253,7761152.12311.98 0663652713%3%16% 199,700 253,7761228.91332.77 000002730%1% 253,77697.61 091160006%2%8% 199,700 253,776614.47166.39 subtotal73%21%94% 7,142.911934.21 Non- sponsored 27% -21%6% 253,776585.90 Total100%0%100% 9,760.62

6

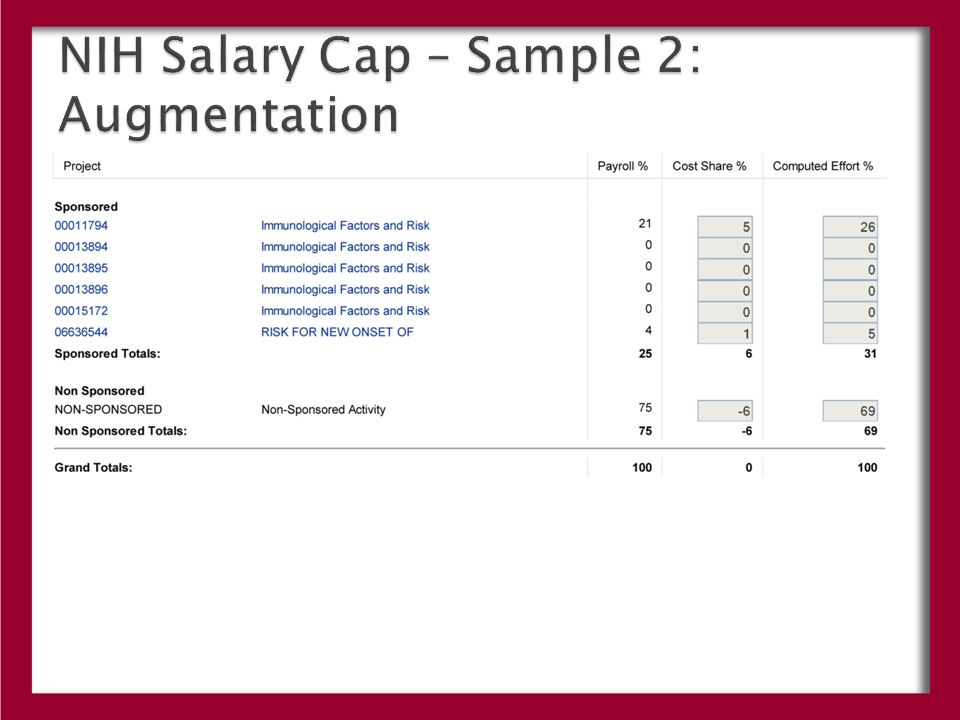

Committed effort is determined as a percentage of all appointments. Include all sources of pay which are associated with job duties There may be a need to communicate effort/payroll percentages BOTH in terms of the “regular” appointment and the full appointment including the Augmentation In the example, the employee’s annual base is $222,113 and their augmentation is $22,500, for a total of $244,613. The cost share represents the difference between $199,700 and $244,613. Cost-sharing can take place from any job record as long as it has non-sponsored funds

7

Projects Payroll- REG Payroll with AUG Cost- sharing REG Cost- sharing AUGEffort Salary cap REG Salary Salary with AUG Project $/pay period Cost- share $/Pay period 0001179423.38%21.23%5.26%4.77%26.00% 199,700 222,113 244,613 1,997.00449.13 cost-share5.26%4.77%-5.26%-4.77%0.00% Non- sponsored [dept. funds]71.37%64.80%0.00% 64.80% 222,113 244,613 6,096.68 Non- sponsored [Aug]0.00%9.20%0.00% 9.20% 222,113 244,613 865.38 total100.00% 0.00% 100.00% 9,408.19

9

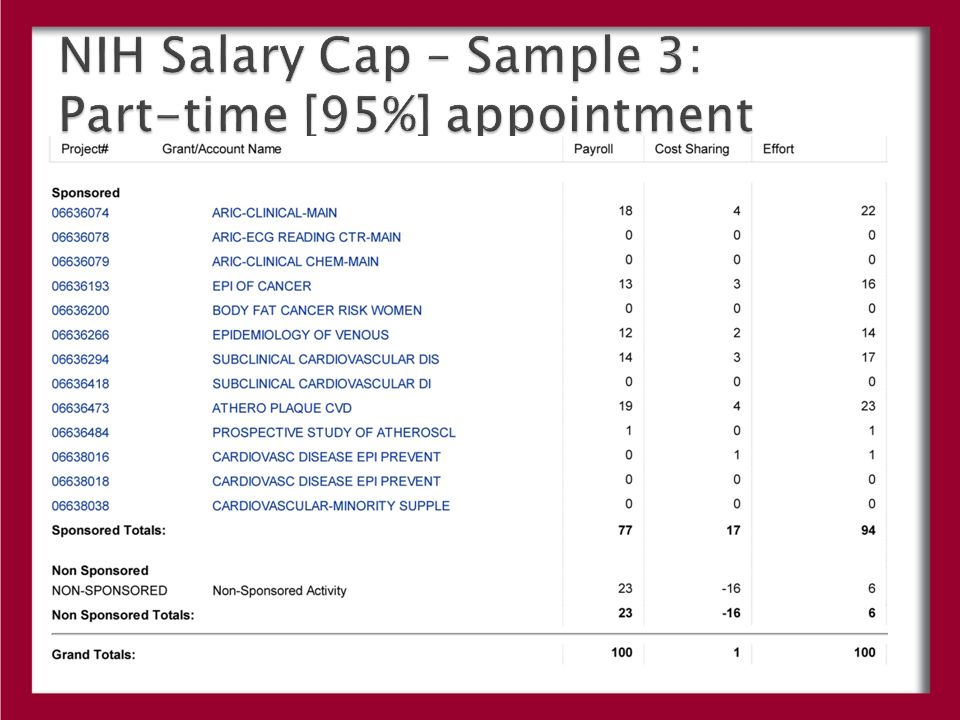

The NIH salary cap is prorated based on the individual’s appointment % (FTE) For the time period shown in the example, for an employee with a 95% appointment, the cap was $191,300 x 95% appt = $181,735 In the example, the employee’s annual base was $229, 908 x 95% = $218,413. The cost- sharing represents the difference between the $218,413 and $181,735.

10

Project sPayrollCost-sharingEffortSalary CapActual Salary Project $/pay period Cost-share $/Pay period 0663607419%4%23% 181,735 218,4131,607.66324.46 0663619313%3%16% 181,735 218,4131,118.37225.71 0663626621%4%25% 181,735 218,4131,747.45352.67 0663629414%3%17% 181,735 218,4131,188.27239.82 066364738%2%10% 181,735 218,413714.02144.10 000099421%0%1% 181,735 218,41369.9014.11 066380160%1% 181,735 218,4130.0084.01 066364841%0%1% N/A 218,41384.010.00 78%16%94% 6,529.681384.88 Non- sponsored 22% -16%6% 218,413 485.93 Total100%0%100% 8,400.49

Similar presentations

Payroll Office 12/18/2014.>")