Download presentation

Presentation is loading. Please wait.

1

An approach to building sustainable SHG federations Kalpana Pant with federations – 7 th August 2012

2

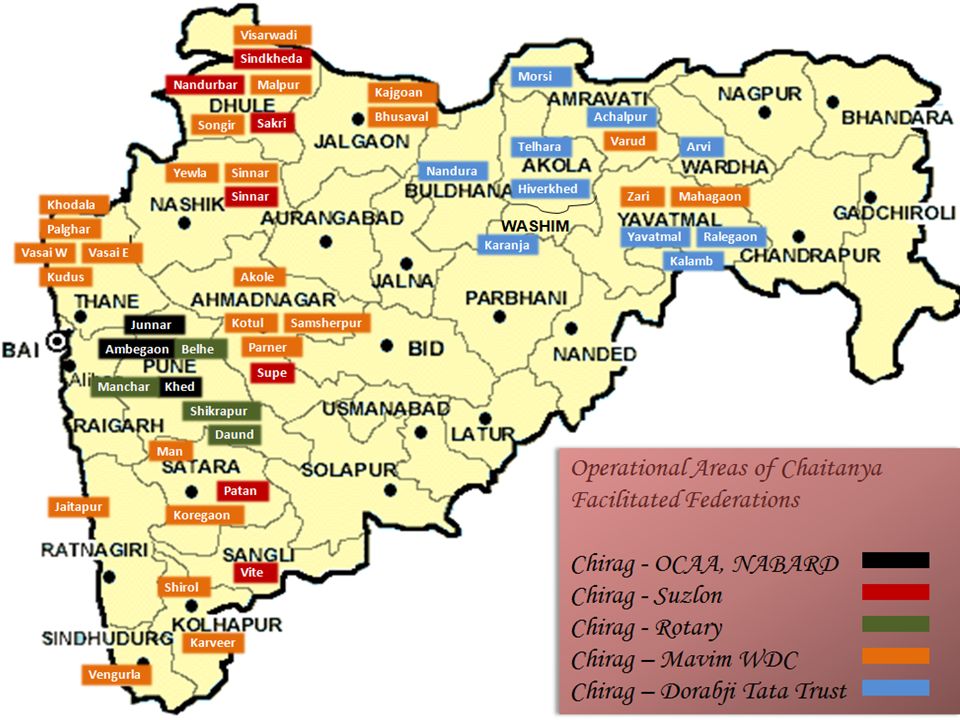

Chaitanya – Empowering Women and Youth One of the earliest institutions to promote SHG women’s financial institution - 1991 Currently, 91000 families organised into SHGs/ clusters and federations in 1200 villages and 50 federations A Resource organisation on self –help groups and federations in the country Closely worked with the government – designing of MRCP (Swa-shakti, Swayamsiddha, CAIM, Tejaswini, Vasundhara) Courses on SHG and micro finance with State Open University and TISS

Courses on SHG and micro finance with State Open University and TISS")

3

Microfinance: Issues and Challenges of Non- community Based Approach Capital Adequacy and Commercial Investment- mobilizing capital to maintain debt equity ratio. Ownership transfer and often mission drift. Elimination of Saving Services - focus of MFs remain primarily on credit services. Drift in Community and Poverty Focus – Without participation of community greater possibility of mission drift Community Remains Mere Group of Customers -Social capital and social development process is alienated

4

Need of Community Based Microfinance Approach Empowering Community– participation of community in decision making is essential Community Ownership Retains Focus on Community and Poverty- Resources from community are invested to leverage funds Need Based Service Delivery – Extends thrift and credit services with social intervention support quite effectively. Strengthening Local Institutions for Local Development – To address context specific local development issues people’s institutions with resources can play crucial role. Eliminates Dependence and Risk Attached to Foreign and Commercial Investments – upholds the interest of people first.

5

Most Importantly… An integration of financial as well as non financial services Social intermediation helps cement the foundation of a micro finance programme – it builds ownership, networks, increases involvement and risk taking capacities

6

Genesis of the Federation SHGs started in 1989 in Chas area in Khed block of Pune District In 1991, 14 SHGs decided to come together and form a federation The federation was registered in 1993 under Societies’ registration Act 1860 and Bombay Public Trust Act 1950

8

Sustainability – what Do we Mean?

9

Key Aspects of sustainability Value orientation to avoid mission drift Increased capacity of members to take risk New innovative ideas Strong governance, community ownership – Networks and convergence Conflict resolution Role transformation of leadership Members perceiving direct benefit

10

Financial Sustainability

11

Business Model-2011 calculations Cost of promotion -Rs. 400 to 500 per year per member over a period of 4 years for a federation with membership of 2500. Recurring cost – Rs. 50000 per month (2011 calculations) Easy to achieve with low cost of operations Demonstrated with 15 sustainable federations – trying different models of income in 35

Easy to achieve with low cost of operations Demonstrated with 15 sustainable federations – trying different models of income in 35.")

12

Sustainability Models Interest spread 6-9% with default risk 100% (Indian Bank, SIDBI, BoM) Interest spread of 9% with default risk10% (Yes Bank BC model) Service charge of 5% with default risk upto 5% (WSHG) 2% as service charge to the federation as BC (ICICI Bank in Maharashrta) Revolving fund by government programmes (Watershed) Contribution of 2000 -3000 from the groups annually (CMRC)

Interest spread of 9% with default risk10% (Yes Bank BC model) Service charge of 5% with default risk upto 5% (WSHG) 2% as service charge to the federation as BC (ICICI Bank in Maharashrta) Revolving fund by government programmes (Watershed) Contribution of from the groups annually (CMRC)")

13

5 Sustainability Model Projections Financial Costs Paid to Bank Model 1 & 215% Model 50% Interest Charged to Borrower Model 1 & 2 –Direct24% Model 5 –interest free12% Loan Loss ProvisionModel 1 & 51% Model 2 –BC0.1% Model 3 - NABARD0.1% Model 40%

14

Assumptions with INR 20000 & 10 Installments Loan O/SModel 1Model 2Model 3Model 4Model 5 Indian BankYes BankNABARDICICI BankVasundhara 20000150 200 900067.5 90 800060 80 700052.5 70 600045 60 500037.5 50 400030 40 300022.5 30 200015 20 10007.5 100040010 Sub Total487.5 1000400650 Less Loss20020 0200 Total287.5 980400450

15

Assumptions with INR 40000 & 20 Installments Loan O/SModel 1Model 2Model 3Model 4Model 5 40000300 2000800400 38000285 380 36000270 360 34000255 340 32000240 320 30000225 300 28000210 280 26000190 260 24000185 240 22000165 220 20000150 1000200 18000135 180 16000120 160 14000105 140 1200090 120 1000075 100 800060 80 600045 60 400030 40 200015 20 Sub Total3150 30008004200 Less Loss40040 0400 Total275031102960800

16

1.The most sustainable option is of course interest free loans where with a spread of 12% p.a. 2.The second best option in case the loan size demanded is small (less than Rs. 25000) is a 5% service charge as in NABARD’S WSHG programme 3.For larger loan sizes, interest spread instead of fees based on loan outstanding is a much better option as clear in the comparison with Yes Bank where the income is higher with limited risk of 10%

is a 5% service charge as in NABARD’S WSHG programme 3.For larger loan sizes, interest spread instead of fees based on loan outstanding is a much better option as clear in the comparison with Yes Bank where the income is higher with limited risk of 10%.")

17

Projections Summary 4. Model of 2% service charge can be explored in case federations are dealing with loans of small sizes – but not for large loan sizes 5. Most banks only give partial payment (1%) and remaining after repayment – in case of default the 1% remaining is not paid 6. Need to negotiate with the banks for an increase in service charge in case of loans of longer duration

and remaining after repayment – in case of default the 1% remaining is not paid 6. Need to negotiate with the banks for an increase in service charge in case of loans of longer duration.")

18

Reducing cost - Human Resources Shift over a period of four years from professional to local staff Recruited from the community – from operational villages Recommended by women’s groups Primarily women – requires high investment in capacity building

19

Developing Capabilities and Skills of Rural SHG Women to Address their Self Identified Needs community resource persons – for capacity building, audit of SHGs as well as financial counseling

20

Profit distribution by GMSS 20% of profits for social programmes – Dipti Arogya Nidhi –community health programme 20% for livelihood promotion – capacity building and loan fund for cow project 20% for Chirag technical support team 40% for other expenses (Older federations want an office of their own!)

")

21

Challenges in Mobilising resources Regulatory issues – savings not legal except in Cooperatives Rating agencies not familiar with CBMFI Capital Adequacy Ratio not sufficient Portfolio at Risk relatively higher that other models MIS – not customised – federations cannot afford Internal audit and control – possible with training of the federation office bearers

22

Thank You!

Similar presentations

![SHG Bank Linkage Programme What is a Self-Help Group ? A Self-Help Group [SHG] is a small, economically homogeneous and affinity group of 15-20 rural poor.](/5/1537054/big_thumb.jpg "SHG Bank Linkage Programme What is a Self-Help Group ? A Self-Help Group [SHG] is a small, economically homogeneous and affinity group of 15-20 rural poor.>")

Guiding Principle stresses on organizing the rural poor into small groups through a process of social.>")

A UNEP INITIATIVE SUPPORTED BY THE UN FOUNDATION www. AREED.org Lenders vs. Investors Lenders: often.>")

M.M. Goel Dr. Virander Pal Goyal.>")

- Project Timeframe: Sept 2006 - Dec 2010 - Village Saving.>")