Download presentation

Presentation is loading. Please wait.

1

Using Arbitrage Pricing Theory To Analyse UK and USA Property Cycle Differences European Real Estate Society Stockholm, Sweden June 2009 Terry V. Grissom Ph.D.* Jasmine L.C. Lim Ph.D.* James L. DeLisle Ph.D.** *School of the Built Environment University of Ulster, Jordanstown **College of Built Environments University of Washington, Seattle

2

Investor concerns seeking potential timing market turnaround An Expectation is that an upturn in USA property/investment market will proceed an upturn in the UK: correlation analysis supports this position However analysis of historic property and economic cycles differences suggests alternative scenarios Expectation is not supported by lead-lag analysis

3

Exhibit 2: Correlation of Property Returns in the UK and US and Systematic Factors UK IPD US NCREIF Returns GDP:UKGDP:US Unantici pated Inflation: UK Unantici pated Inflation: US Term Struct ure: UK Term Structu re: US Equity Risk Premiu m: UK Equity Risk Premiu m: US UK IPD Returns 1.000 US NCREIF Returns 0.2691.000 GDP:UK 0.5150.5451.000 GDP:US 0.3230.5540.4321.000 Unanticipated Inflation: UK -0.403-0.173-0.424-0.0021.000 Unanticipated Inflation: US -0.274-0.073-0.2960.1130.9431.000 Term Structure: UK 0.2060.1120.291-0.099-0.920-0.8721.000 Term Structure: US 0.2140.2900.5080.045-0.893-0.8410.8151.000 Equity Risk Premium: UK 0.2910.2520.3360.243-0.550-0.4710.5030.4951.000 Equity Risk Premium: US 0.2380.2360.3340.142-0.579-0.5070.5230.5470.3951.000

4

-.06 -.04 -.02.00.02.04.06 1980198519901995200020052010 UKGDP% USAGDP% UK Trend USA Trend Comparison of UK and USA GDP Percentage Change and Trends 9-11

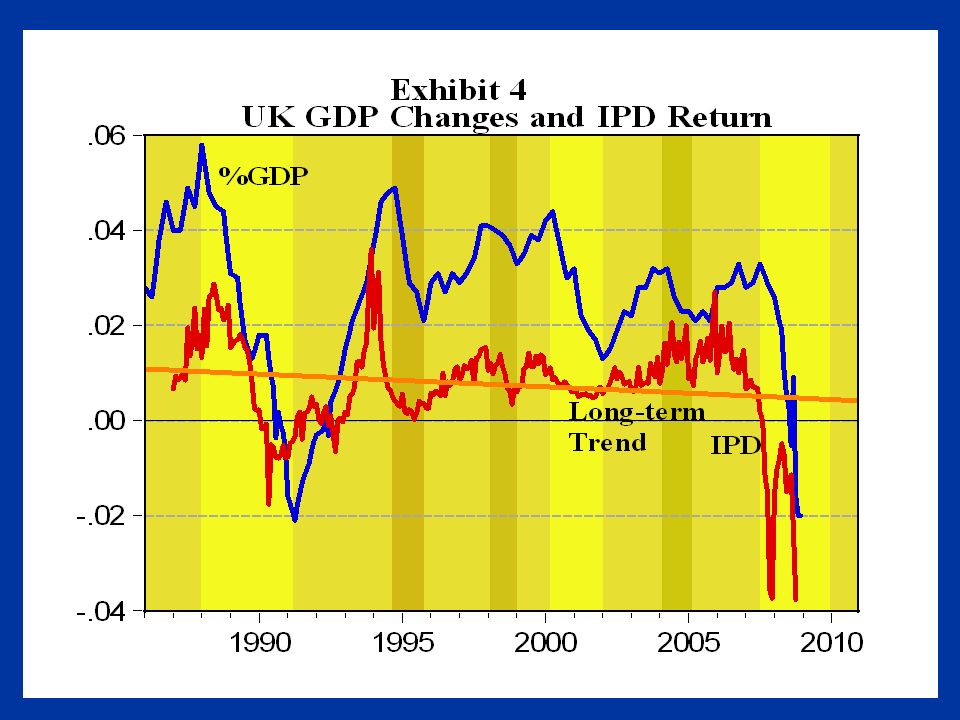

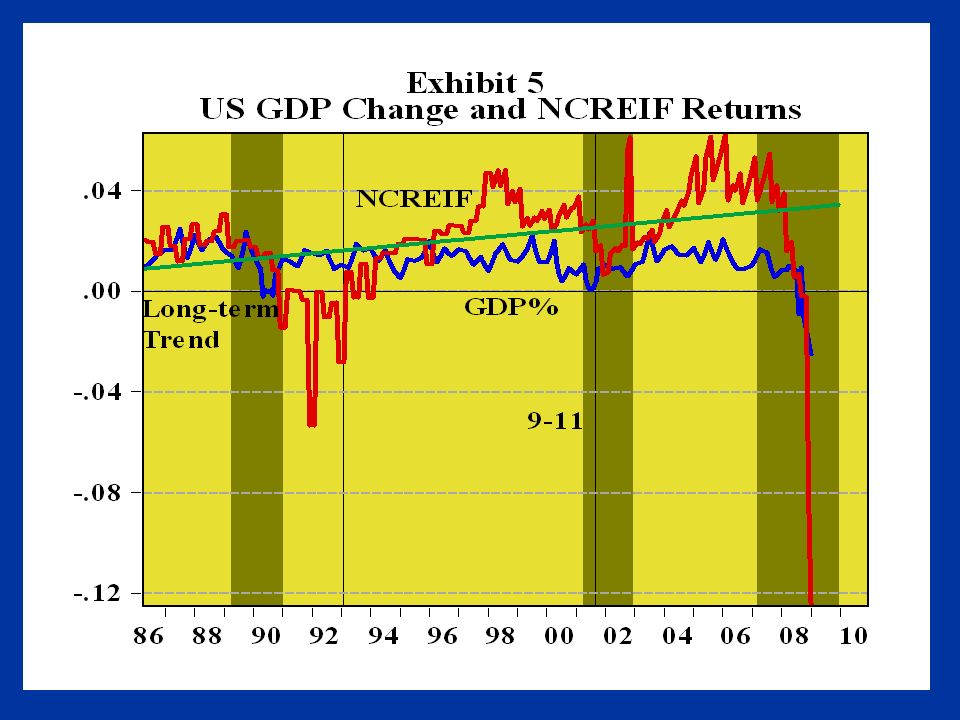

8

The differences in pricing/performance of cross markets in time suggest the arbitrage potential that may not support an equilibrium clearance of differences. This suggest a limited integration and possible segmentation of the two property/equity markets associated with divergent regimes due to differences in economic fluctuations. This suggests the use of an APT macroeconomic variable model to address differences in the cyclical patterns observed. The DCF construct of the APT model suggest pricing differences associated with behavioural differences observed in the two markets.

9

One test of a behavioural pricing differences is noted by Hendershott and MacGreger (2005) They note that investment behaviour difference between UK and USA property markets based on mean/trend reversion behaviour. Where: – UK is rational reflecting trend reversion pricing – USA is non-rational with no trend reversion pricing noted

10

The implication that differences in investor behaviour may contribute to pricing and timing differences defining the two markets fits the construct of the MVM Arbitrage Price Models This achieved using a spline analytic for cycle regime delineation as employed by Grissom & DeLisle (1999). This variable assist in identifying the potential timing and turnarounds observed and expected for both the UK and USA property markets. The theoretical constructs and the procedural steps employed in this analysis is illustrated in the following set of equations

12

APT (US) with Expected risk free rate R 2 = 75.97% Intercept & Beta t statistic (0.070599) + 1.209816 ( ) - 1.221854(U ) + 0.188532( ) + 0.079061( ) + i -2.034205 5.205751 -12.13241 1.529515 2.439929 0.021155 APT (US) with Expected Zero Beta R 2 = 75.97% Intercept & Beta t statistic -0.008317 + 1.209816 ( ) - 1.221854(U ) + 0.188532( ) + 0.079061( ) + i -2.034205 5.205751 -12.13241 1.529515 2.439929 0.021155

with Expected risk free rate R 2 = 75.97% Intercept & Beta t statistic ( ) ( ) (U ) ( ) ( ) + i APT (US) with Expected Zero Beta R 2 = 75.97% Intercept & Beta t statistic ( ) (U ) ( ) ( ) + i")

13

APT (UK) with Expected risk free rate R 2 = 93.28% Intercept & Beta t statistic (0.070599) + 0.347208( ) - 0.868562(U ) + 0.108614( ) + 0.035194( ) + i -1.769832 7.920781 - 17.14555 2.317567 2.576084 0.019971 APT () with Expected Zero Beta R 2 = 93.28% Intercept & Beta t statistic -0.003927 + 0.347208( ) - 0.868562(U ) + 0.108614( ) + 0.035194( ) + i -1.769832 7.920781 -17.14555 2.317567 2.576084 0.019971

with Expected risk free rate R 2 = 93.28% Intercept & Beta t statistic ( ) ( ) (U ) ( ) ( ) + i APT () with Expected Zero Beta R 2 = 93.28% Intercept & Beta t statistic ( ) (U ) ( ) ( ) + i")

14

APT (UK) with Expected risk free rate and US Property Performance R 2 = 65.66 Intercept & Beta t statistic APT (UK) with Expected Zero Beta reflecting US Property Performance R 2 = 65.66 Intercept & Beta t statistic 0.022861 + -0.199716( ) - 1.101734(U ) + 0.021012( ) + 0.029849( ) +0.244874Rit|US 1.897037 -0.652772 -4.355030 0.164764 0.564750 2.099157 (0.070599) -0.199716( ) - 1.101734(U ) + 0.021012( ) + 0.029849( ) +0.244874R it|US 1.897037 -0.652772 - 4.355030 0.164764 0.564750 2.099157

with Expected risk free rate and US Property Performance R 2 = Intercept & Beta t statistic APT (UK) with Expected Zero Beta reflecting US Property Performance R 2 = Intercept & Beta t statistic ( ) (U ) ( ) ( ) Rit|US ( ) ( ) (U ) ( ) ( ) R it|US")

15

UK Returns as a function US MVM factors

16

APT (UK) with Expected risk free rate and US Property PerformanceR 2 = 60.29 Intercept & Beta t statistic (0.070599) -0.151844( |US ) -0.333261(U |US )+0.454337( |US )+0.065742( |US ) + 0.191620R it|US -3.129379 -0.357658 -2.086653 1.122048 1.217944 1.309247 APT (UK) with Expected Zero Beta reflecting US Property PerformanceR 2 = 60.29 Intercept & Beta t statistic -0.023468 -0.151844( |US ) -0.333261(U |US ) +0.454337( |US ) +0.065742( ) + 0.191620R it|US -3.129379 -0.357658 -2.086653 1.122048 1.217944 1.309247

with Expected risk free rate and US Property PerformanceR 2 = Intercept & Beta t statistic ( ) ( |US ) (U |US ) ( |US ) ( |US ) R it|US APT (UK) with Expected Zero Beta reflecting US Property PerformanceR 2 = Intercept & Beta t statistic ( |US ) (U |US ) ( |US ) ( ) R it|US")

17

Recessionary Spline Knot E(R it| ) coefficient t-StatisticR2R2 -value UK 1988-912.09585.591597.950.0000 1994-95-19.1563-1.658388.910.1358 1998-992.30551.184740.310.2738 2001-020.995231.867798.700.0000 2007-093.70721.293651.830.9465 US 1990-911.48785.603086.070.0000 2001-023.64346.074680.450.0000 2007-090.34991.122975.620.2818

coefficient t-StatisticR2R2 -value UK US")

18

Conclusions The UK Property investment market is at best is only moderately integrated with the US property and capital markets suggesting the potential for similar pricing activities. However cycle investigation shows a difference in lead lag associations across markets. This suggest the possibility of arbitrage across markets and time. The application of the APT model shows that an integration of the US property returns and general economic factors however reduce the explanatory effect of MVM factors.

19

Conclusions This suggested a difference in pricing behaviour across the 2 markets. One previously hypothesized reason is that the two markets reflect pricing differentials as a function of mean/trend reversion behaviour, suggesting that the UK more rationally prices general economic variables, while the US shows a decoupling of financial and real economic variables in the estimation of property returns

Similar presentations

, Oliver Holtemöller (Halle Institut for Macroeconomics)>")

–is an equilibrium factor mode of security returns –Principle.>")

? How does CMEs.>")