Download presentation

Presentation is loading. Please wait.

2

7.1 A SINGLE-FACTOR SECURITY MARKET

3

Input list (portfolio selection) ◦ N estimates of expected returns ◦ N estimates of variance ◦ n(n-1)/2 estimates of covariance Errors in estimation of correlation coefficients A model to simplifies the way describing the sources of security risk

◦ N estimates of expected returns ◦ N estimates of variance ◦ n(n-1)/2 estimates of covariance Errors in estimation of correlation coefficients A model to simplifies the way describing the sources of security risk")

4

Decomposing uncertainty into the system- wide versus firm-specific sources ◦ Common economic factors Business cycles, interest rates, technological changes, cost of labor and raw materials Affect the fortunes of many firms ◦ Firm specific events Assume one macroeconomic indicator moves the security market as a whole, all remaining uncertainty in stock returns is firm specific

5

Reduces the number of inputs for diversification Easier for security analysts to specialize Advantages of the Single Index Model

6

Decompose rate has mean of 0, SD= Security return, If normal distribution and correlated across securities ◦ joint normally distributed ◦ driven by one or more common variables ◦ Multivariate normal distribution Single factor security ◦ Only one variable rives the joint normally distributed return Expected unexpected

7

Holding-period return on security i =impact of unanticipated macro events on the security ’ s return, SD= = impact of unexpected firm specific event, SD=, have zero expected values, uncorrelated

8

Variance of r arises from two uncorrelated sources m generates correlation across securities Covariance between any two securities i and j is

9

m, unanticipated components of macro factor ß i, responsiveness of security i to macro-events ◦ Different firms have different sensitivities to macroeconomic events Single-Factor model

10

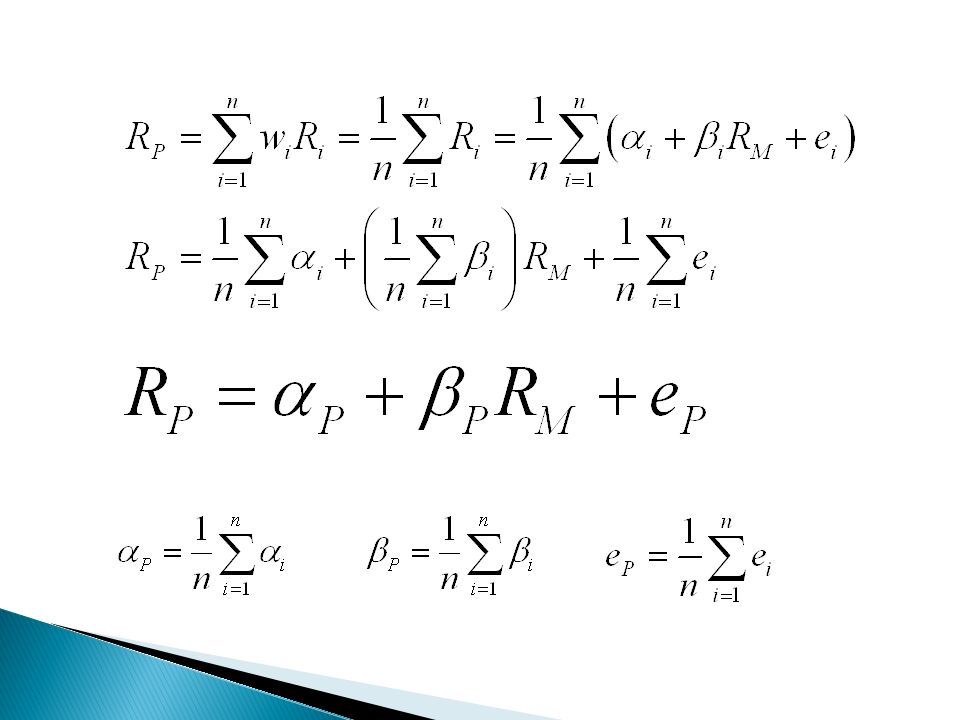

Single-Index Model Continued Risk and covariance: ◦ Total risk = Systematic risk + Firm-specific risk: ◦ covariance Systematic risk

11

7.2 A SINGLE-INDEX MODEL

12

Single-Index model ◦ Assumption: a broad market index like the S&P500 is a valid proxy for the common macroeconomic factor, as the common or systematic factor Regression equation( regress Ri on RM) M: market index, excess return SD=, serurity’s excess return

M: market index, excess return SD=, serurity’s excess return")

13

Holding-period excess return on the stock Due to movements in overall market Residential, Due to firm specific factors Security’s expected excess return when market excess return is 0

14

Let: R i = (r i - r f ) R m = (r m - r f ) Risk premium format R i = i + ß i (R m ) + e i

R m = (r m - r f ) Risk premium format R i = i + ß i (R m ) + e i")

15

Single-Index Model Regression Equation: Expected return-beta relationship: Nonmarket premium Systematic risk premium: market risk premium multiplied by sensitivity

16

Single-Index Model Risk and covariance: ◦ Total risk = Systematic risk + Firm-specific risk: ◦ Covariance = product of betas x market index risk: ◦ Correlation = product of correlations with the market index

17

Input for single-index model ◦ n estimates of expected returns ◦n◦n ◦ n estimate of firm-specific variance ◦ 1 estimate of market risk premium ◦ 1 estimate of variance of macroeconomic factor Index model abstraction is crucial ◦ for specialization of effort in security analysis ◦ provide a simple way to compute covariance

18

Suppose choose an equally weighted portfolio of n securities, the excess return on each security is The excess return on the portfolio of stocks is To show: when n increases, nonmarket factors becomes smaller (diversified away), market risk remain

, market risk remain")

20

Systematic risk component of the portfolio variance: Nonsystematic component is attributable to firm-specific components is average of the firm-specific variances. When n gets large, gets negligible.

21

7.3 ESTIMATING THE SINGLE-INDEX MODEL

22

Using montly data for six stocks (IT/RETAIL/ENERGY), S&P 500, and T-bill from 2001 to 2006 (60 observations) to estimate the regression equation Regress risk premiums for individual stocks against the risk premiums for the S&P 500 Slope is the beta for the individual stock HP as an example

, S&P 500, and T-bill from 2001 to 2006 (60 observations) to estimate the regression equation Regress risk premiums for individual stocks against the risk premiums for the S&P 500 Slope is the beta for the individual stock HP as an example")

23

Relationship between the excess returns on HP and the S&P 500 (regression equation) SCL (security characteristic line) ◦ Regression estimates describe a straight line with, is the sensitivity of HP to the market, slope of the regression line intercept, representing the average firm-specific excess return when the market ’ s excess return is zero. residual, vertical distance of each point from the regression line

24

Figure 8.2 Excess Returns on HP and S&P 500 April 2001 – March 2006 Annualized SD OF S&P=13.58% Annualized SD OF HP=38.17% Greater than average sensitivity to the index, beta>1

25

Scatter Diagram of HP, the S&P 500, and the Security Characteristic Line (SCL) for HP

for HP")

26

Table 8.1 Excel Output: Regression Statistics for the SCL of Hewlett-Packard

27

◦ Variation in the S&P 500 excess return explains about 52% of the variation in the HP series. ◦ Correlation: ◦ SSR: sum of squares of the regression (0.3752) is the portion of the variance of the dependent variable (HP) that is explained by the independent variable (S&P) ◦ SSE: variance of the unexplained portion, independent of the market index SSR df=k SSE df=n-k-1 SST df=n-1

is the portion of the variance of the dependent variable (HP) that is explained by the independent variable (S&P) ◦ SSE: variance of the unexplained portion, independent of the market index SSR df=k SSE df=n-k-1 SST df=n-1.")

28

SSR df=k SSE df=n-k-1 SST df=n-1

29

◦ MSR=SSR/k=0.3752/1=0.3752 ◦ MSE=SSE/n-k-1=0.3410/58=0.0059 ◦ Standard error of the regression is square root of MSE, (firm-specific risk) ◦ Estimate of monthly variance of the dependent variable (HP) =0.7162/59=0.012 ◦ Annualized SD of dependent variable SSR df=k SSE df=n-k-1 SST df=n-1

◦ Estimate of monthly variance of the dependent variable (HP) =0.7162/59=0.012 ◦ Annualized SD of dependent variable SSR df=k SSE df=n-k-1 SST df=n-1")

30

Estimate of Alpha ◦ Alpha=0.86%, t-statistic=0.8719<2, not reject null, too low to reject the hypothesis that the true value of alpha is 0 ◦ HP’s return net of the impact of market movements Explanatory Power of SCL for HP Nonmarket component of HP’s return actual return the return attributable to market movements

31

Estimate of Beta ◦ Beta=2.0348, t-statistic=7.9888>2, reject null, Firm specific risk ◦ Monthly SD of HP’s residual is 7.67%, or 26.6% annually (firm- specific risk) ◦ SD of systematic risk Explanatory Power of SCL for HP

◦ SD of systematic risk Explanatory Power of SCL for HP")

32

Six stocks: ◦ HP,DELL; ◦ TARGET, WALMART; ◦ BP,SHELL.

33

Excess Returns on Portfolio Assets

34

Tremendous firm-specific risk (see excel) For any pairs of securities, get the estimates of the risk parameters of the six securities and S&P500 Correlations of residuals ◦ for same-sector stocks are higher; ◦ cross-industry correlations are far smaller Covariance matrix

For any pairs of securities, get the estimates of the risk parameters of the six securities and S&P500 Correlations of residuals ◦ for same-sector stocks are higher; ◦ cross-industry correlations are far smaller Covariance matrix")

36

Alpha and Security Analysis Index model creates a framework that separates the two quite different sources of return variation, easier to ensure consistency across analysts ◦ Macroeconomic analysis is used to estimate the risk premium and risk of the market index ◦ Statistical analysis is used to estimate the beta coefficients of all securities and their residual variances, σ 2 ( e i ) ◦ establish expected return of the security absent any contribution from security analysis, the market-driven expected return is conditional on information common to all securities ◦ Security-specific expected return forecasts are derived from various security-valuation models, the alpha value distills the incremental risk premium attributable to private information developed from security analysis

◦ establish expected return of the security absent any contribution from security analysis, the market-driven expected return is conditional on information common to all securities ◦ Security-specific expected return forecasts are derived from various security-valuation models, the alpha value distills the incremental risk premium attributable to private information developed from security analysis")

37

Alpha and Security Analysis The alpha helps determine whether security is a good or bad buy ◦ Risk premium on a security not subject to security analysis would be, any expected return beyond this benchmark risk premium (alpha) would be due to some non- market factors uncovered by security analysis ◦ Security with positive alpha is providing a premium over and above the premium it derives from its tendency to track the market index, should be over-weighted in portfolio

would be due to some non- market factors uncovered by security analysis ◦ Security with positive alpha is providing a premium over and above the premium it derives from its tendency to track the market index, should be over-weighted in portfolio")

38

To include the indexed portfolio as an asset of the portfolio to avoid inadequate diversification ◦ Beta=1, no firm-specific risk, alpha=0, no non- market factors in its return ◦ (n+1)th security ◦ The portfolio: n actively researched firms and a passive market index portfolio

th security ◦ The portfolio: n actively researched firms and a passive market index portfolio")

39

Single-Index Model Input List Risk premium on the S&P 500 portfolio Estimate of the SD of the S&P 500 portfolio n sets of estimates of ◦ Beta coefficient ◦ Stock residual variances ◦ Alpha values Generate n+1 expected return, covariance matrix

40

Optimal Risky Portfolio of the Single-Index Model Maximize the Sharpe ratio to get portfolio weights ◦ Expected return, SD, and Sharpe ratio:

41

Basic trade-off of the model ◦ For diversification, holding the market index ◦ Security analysis gives chance to uncover nonzero alpha securities and take differential position ◦ Cost: unnecessary firm-specific risk ◦ The optimal risky portfolio trade off the search for alpha against departure from efficient diversification

42

Optimal Risky Portfolio of the Single- Index Model Continued Combination of: ◦ Active portfolio denoted by A, comprised of the n analyzed securities ◦ Market-index portfolio, the (n+1)th asset which we call the passive portfolio and denote by M Assume beta for A is 1. optimal weight of active portfolio

43

Optimal Risky Portfolio of the Single- Index Model Continued Combination of: ◦ Modification of active portfolio position: ◦ When

44

The Information Ratio The Sharpe ratio of an optimally constructed risky portfolio will exceed that of the index portfolio (the passive strategy): Information ratio: ratio of alpha to its residual SD, measures the extra return we can obtain from security analysis compared to the firm-specific risk we incur when we over-or-underweight securities relative to the passive market index. Maximize Sharpe ratio, to maximize information ratio of A

45

Maximize information ratio, get weight of each security in A The total position in the active portfolio adds up to The weight of each security in the optimal portfolio (M+A) is

is")

46

The positive contribution of a security to the portfolio is made by its addition to the nonmarket risk premium (alpha) The negative impact is to increase the portfolio variance through firm-specific risk (residual variance)

The negative impact is to increase the portfolio variance through firm-specific risk (residual variance)")

47

After security analysis, index-model estimates of security and market index parameters, to form the optimal risky portfolio ◦ Initial position of each security in A ◦ Scale Alpha: ◦ Residual variance of A: Initial position in A ◦ Beta of A Adjust ◦ Optimal risky portfolio weight ◦ Risk premium and variance of the optimal risky portfolio ◦

48

Figure 8.5 Efficient Frontiers with the Index Model and Full-Covariance Matrix

49

Table 8.2 Comparison of Portfolios from the Single-Index and Full-Covariance Models

Similar presentations

Chapter.>")

>")