Download presentation

Presentation is loading. Please wait.

2

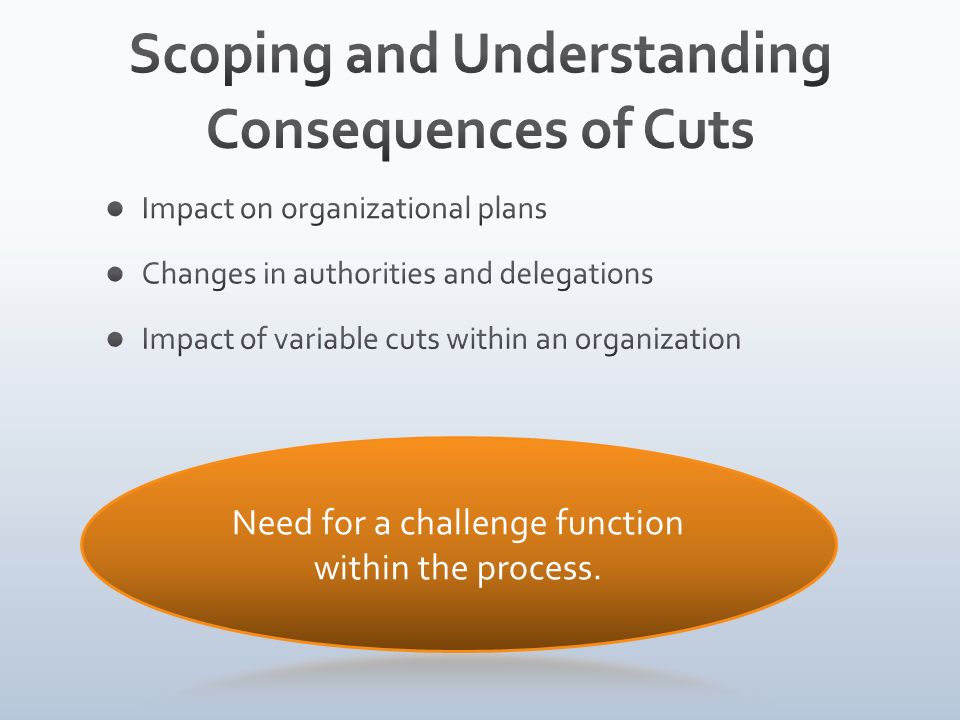

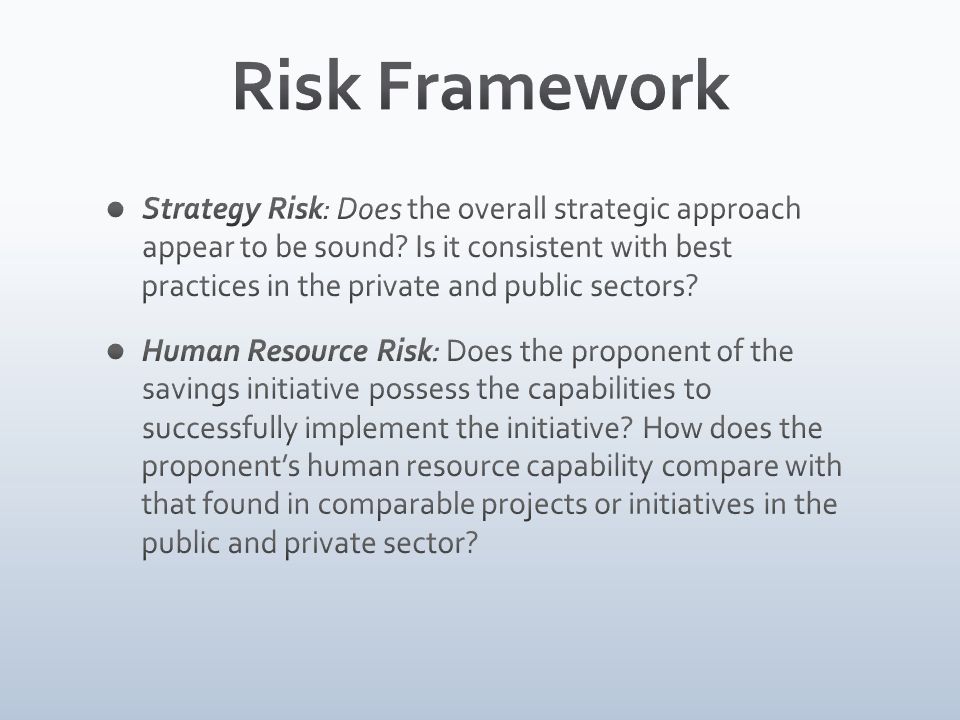

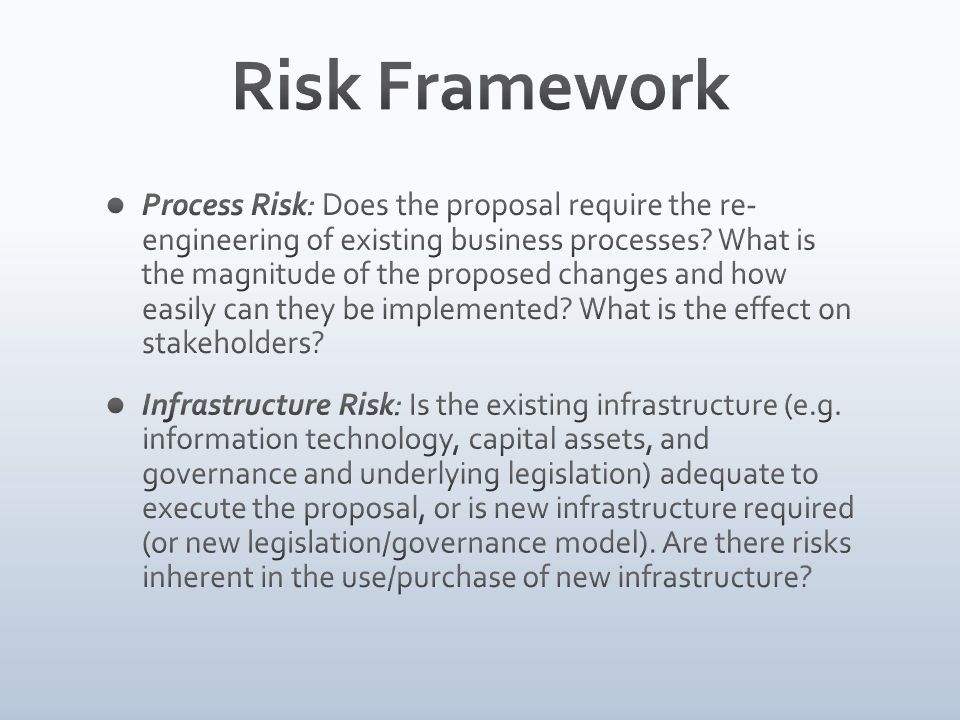

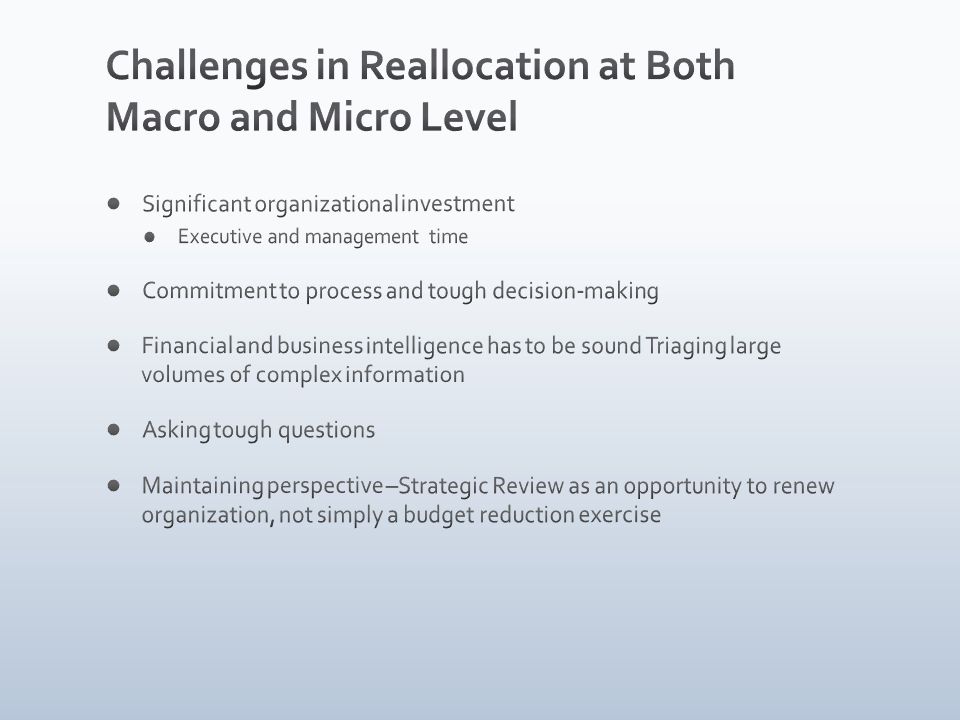

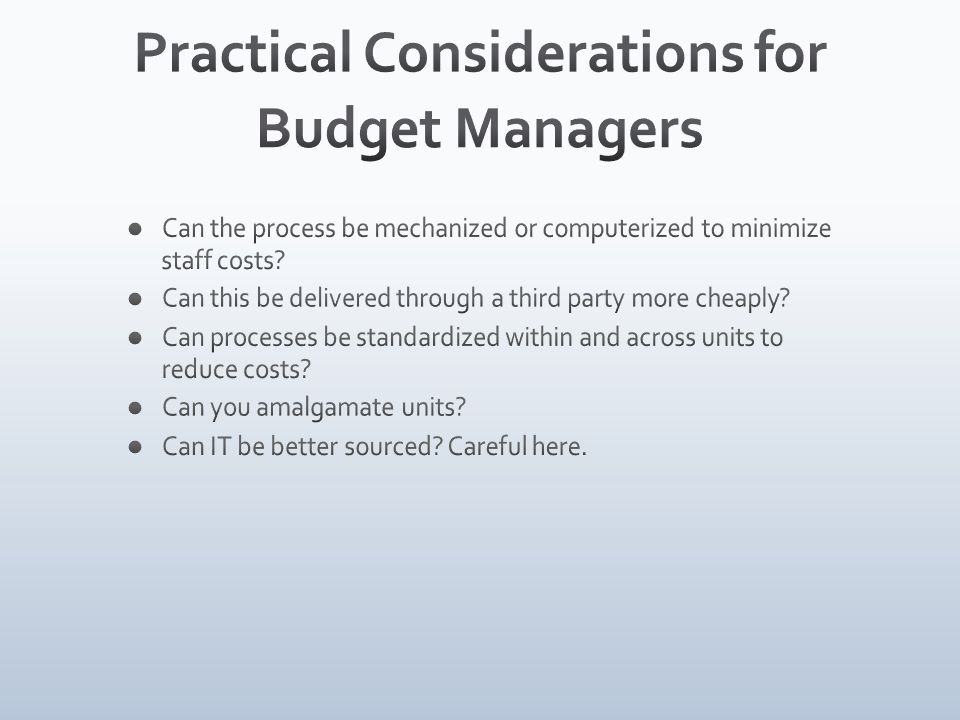

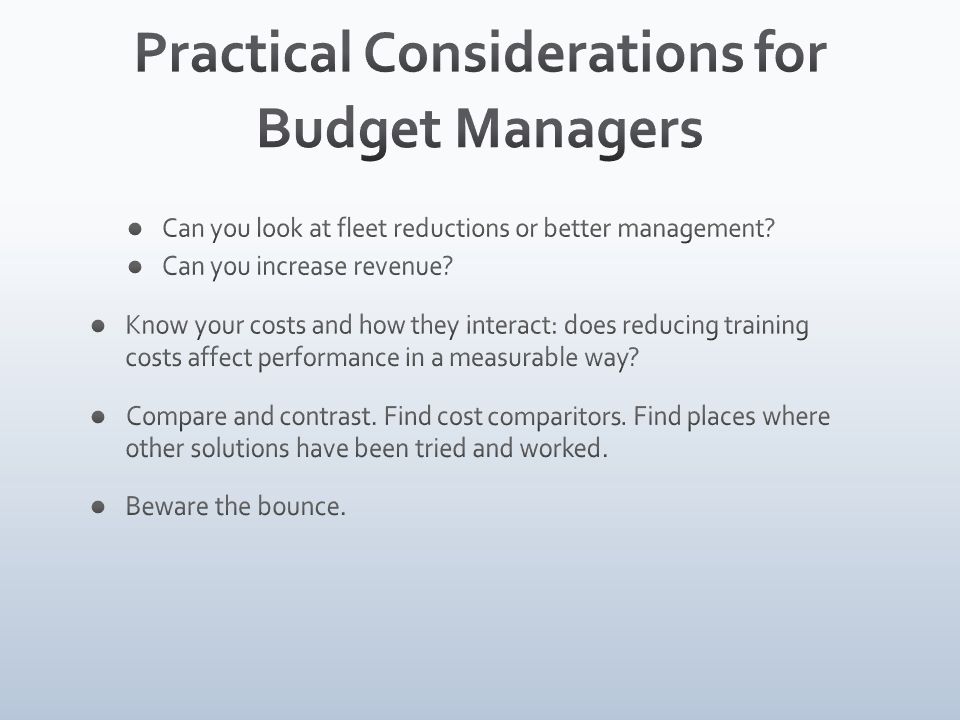

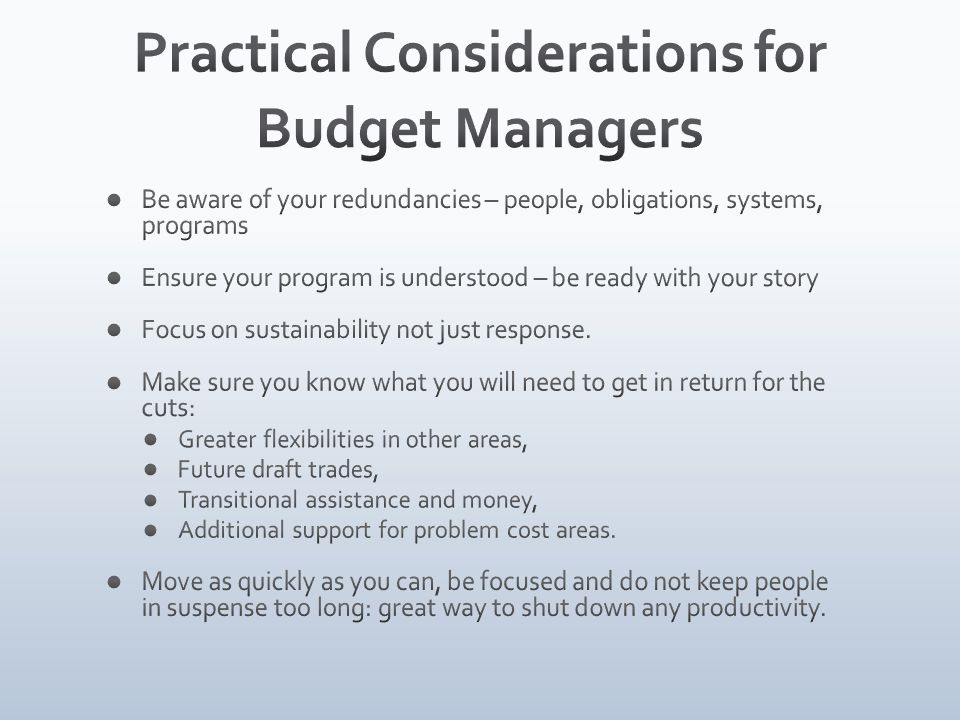

Reallocation in the budget process Strategic Reviews around the world Cutting Tools: How to Cut Risks, consequences, sustainability Practical Considerations for Budget Managers

4

What are the current challenges you face as a public sector manager? Survey in UK of public sector managers by the Institute on Leadership and Management, 2010

6

Reallocation Policy Change Fiscal Change Control Adjustment Performance Adjustment Cost Adjustment

9

All direct program spending reviewed - 25% each year Treasury Board and its Secretariat set terms of reference: Comprehensiveness – assessment of mandate, departmental objectives, program effectiveness, efficiency and alignment to government priorities Reallocation proposals – options for program reductions or eliminations to reallocate to government priorities and support overall spending control Reinvestment proposals – options to better support government priorities Departments review the relevance and performance of their spending, identify lowest performing/priority 5% of programs, seek outside expert advice and report to the Treasury Board Privy Council Office identifies review departments every year and assesses, with Treasury Board and the Department of Finance, the departmental proposals Strategic Review Process – Centrally Driven 9

10

Strategic Reviews – Scope and Key Elements Departmental Strategic Reviews to answer specific questions in key areas: Government Priority, Federal Role, Relevance (i.e. continued program need) Performance (effectiveness, efficiency, value for money) Management Performance Departmental Strategic Reviews to be conducted using the following key elements Analytical Framework: The department’s Program Activity Architecture Information Sources: Evaluations, Audits, Management Accountability Framework assessments, Auditor General Reports, and other reports Reporting Requirements: Outlined in the Terms of Reference Steering Committee: A departmental steering committee to be established with ex officio membership from TBS External Advice: Expert outside advice to be involved on each Review to ensure neutrality and credibility

Performance (effectiveness, efficiency, value for money) Management Performance Departmental Strategic Reviews to be conducted using the following key elements Analytical Framework: The department’s Program Activity Architecture Information Sources: Evaluations, Audits, Management Accountability Framework assessments, Auditor General Reports, and other reports Reporting Requirements: Outlined in the Terms of Reference Steering Committee: A departmental steering committee to be established with ex officio membership from TBS External Advice: Expert outside advice to be involved on each Review to ensure neutrality and credibility.")

11

Strategic Reviews –Conditions for Success Sufficient time for deliberative process Ministerial engagement throughout the Review process Clear and strategic alignment of programs and results (value of a strong Program Activity Architecture) Comprehensive assessment of all programs (100%)-not focussing only on 5% Early involvement of senior management team – policy, communications, and corporate services Multiple lines of evidence – evaluations, audits, benchmarking, international comparisons Overview portion of the Strategic Review should tell a compelling departmental story Arm’s length expert advice as effective challenge to proposals and alternatives

Comprehensive assessment of all programs (100%)-not focussing only on 5% Early involvement of senior management team – policy, communications, and corporate services Multiple lines of evidence – evaluations, audits, benchmarking, international comparisons Overview portion of the Strategic Review should tell a compelling departmental story Arm’s length expert advice as effective challenge to proposals and alternatives")

12

In 2009, the third year of the Strategic Review Process, 20 federal organizations (including departments, agencies and Crown corporations) undertook strategic reviews of 100 percent of their direct program spending. In total, almost $26 billion, or approximately 23 percent, of all government program spending was examined. Savings of $287 million were redirected to Budget 2010 priorities Savings were redirected to fund new initiatives, both within departments and to broader spending priorities in Budget 2009 Moving from ¼ of all departments to whole of government Now, savings will be directed to deficit reduction Targetting total of $11 billion by 2016 The first reviews generated savings but also demonstrated a need to improve the quality of results information … 12

13

13

14

14

15

15

16

16

17

Managers must approach budget cutting with care, so as not to harm the organization's capacity to achieve its purposes. The toughest question they face is how to reduce the budget without compromising the organization's mission.

18

Internal ReallocationInvesting for EfficiencyIn-Year Cash ManagementBudget Cuts

22

General Approaches to Reallocation Cheese Slicing Efficiency Gains Central Priority Setting

23

Equality, delegated, local knowledge, less political Gradual degradation of service, political surprise, budget padding as defence Cheese Slicing Sounds good, doing more with less, avoids pain, can create system change, cut waste Assumes innovations work, may cost money, savings in future not now, takes commitment Efficiency Gains More strategic, politicians in direct control, targeted Death of a thousand cuts, individual constituencies aroused Centralized Priority Setting

28

In an organization with low trust levels, complex programming and relatively poor information, the best approach may be across-the-board cuts.

32

Strategic Sourcing Shared Services Consolidation Asset Liquidation Travel Cost Management Facilities Optimization Process Improvement Service Modernization Revenue Optimization

39

From Treasury Board of Canada Guide on Costing http://www.tbs- sct.gc.ca/pol/doc-eng.aspx?section=text&id=12251http://www.tbs- sct.gc.ca/pol/doc-eng.aspx?section=text&id=12251

49

Transitional CostsRedundancySeverance CostsSalary Period CostsRetraining Costs Substitution/Replacement Costs TransferReallocation

Similar presentations

Policy: Its critical role in expenditure management Presentation to Financial Management Institute Rohit.>")

>")