Download presentation

Presentation is loading. Please wait.

1

Global trends in telecom development Havana, 22 October 2001 The original document was elaborated by Dr Tim Kelly, ITU/SPU. It has been completed by Saburo Tanaka and by Pape-Gorgui Toure. The views expressed in this presentation are those of the authors, and do not necessarily reflect the opinions of the ITU or its membership. Authors can be contacted by e-mail at: Tim.Kelly@itu.int saburo.tanaka@itu.int gorgui.toure@itu.int.Tim.Kelly@itu.intsaburo.tanaka@itu.int

2

Global trends in telecom development The state of the industry Fixed-lines Mobile The Internet The state of the market Increasing competition Private sector participation Independent regulation Situation in the TAL region countries Addressing the digital divide Traffic and tariffs trends Tariff rebalancing

3

A Mobile Revolution Source: ITU World Telecommunication Indicators Database. 0 200 400 600 800 1'000 1'200 1'400 199319951997199920012003 Mobile Users Fixed Lines Fixed Lines vs. Mobile Users,worldwide, Million

4

Domestic fixed- line revenues, 59.2% International revenues, 8.8% Mobile service revenues, 21.2% Other (incl. Internet, leased lines, telex), 10.6% 1999 Telecom service revenue. Total = US$724b The changing pie: Global telecom service revenue, 1999 Source: ITU “World Telecommunication Development Report 1999: Mobile cellular” (forthcoming)

, 10.6% 1999 Telecom service revenue. Total = US$724b The changing pie: Global telecom service revenue, 1999 Source: ITU World Telecommunication Development Report 1999: Mobile cellular (forthcoming).")

5

0 100 200 300 400 500 600 700 800 900 1000 90919293949596979899000102 Service revenue (US$ bn) Actual Projected Domestic Telephone/fax Int'l Mobile Other: Data, Internet, Leased lines, telex, etc Projection of revenue growth (US$bn) Source: ITU.

Actual Projected Domestic Telephone/fax Int l Mobile Other: Data, Internet, Leased lines, telex, etc Projection of revenue growth (US$bn) Source: ITU.")

6

Internet users, millions Annual rate of change Source: ITU.

7

Inter-regional Internet connectivity Asia / Pacific Latin America USA / Canada Europe Africa 56 Gbit/s 0.1 Gbit/s 0.5 Gbit/s Note: Gbit/s = Gigabits (1’000 Mb) per second. Source: ITU adapted from TeleGeography. 18 Gbit/s 0.4 Gbit/s 3 Gbit/s 0.2 Gbit/s

8

The state of the market Increasing competition Around two-thirds of telecom subscribers now have a choice of operator More than 99 per cent of mobile and Internet subscribers now have a choice of operator Dominantly private-ownership 19 out of top 20 top public telecom operators are partially or fully private-owned Of the top 20 mobile operators, 16 are fully- private, 3 are partially private, 1 is state-owned Independent regulators There are currently 102 independent regulators (only 12 in 1990)

")

9

Degree of competition by service, 1999 (ITU Member States) Source: ITU Telecommunication Regulatory Database. 0% 10% 20% 30% 40% 50% 60% 70% 80% Basic services CellularCable TVISPs MonopolyDuopolyCompetition

10

Degree of competition in basic services, 1999, by region Source: ITU Telecommunication Regulatory Database. 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% AfricaAmericasAsia- Pacific Arab States Europe MonopolyDuopolyCompetition

11

0 10 20 30 40 50 60 70 80 90 100 199519971999200120032005 Local Long distance International Countries Increasing competition: By no. of countries, by service, 1995-2005 Source: ITU Telecommunication Regulatory Database.

12

35% 46% 74% 85% 1990199519982005 Mono- poly Compe- tition 4142948 Number of countries permitting more than one operator for international telephony Percentage of outgoing international traffic open to competition Note: Analysis is based on WTO Basic Telecommunications Commitments and thus presents a minimum level of traffic likely to be open to competitive service provision. Source: ITU, WTO.

13

Recent privatisation transactions Source: ITU Telecommunication Regulatory Database. Note: Some countries made sales in several tranches (e.g., Spain)

.")

14

0 20 40 60 80 100 120 140 160 1991199319951999 PrivateState-owned Countries Ownership status of the incumbent Source: ITU Telecommunication Regulatory Database.

15

Separate regulatory bodies, worldwide, 1999 Source: ITU Telecom Regulatory Database.

16

Source: ITU/BDT Regulatory Database Separate regulators in the World 12 22 30 53 84 102 199019921994199619992000

17

Separate regulators by Region 2000, Total: 102

18

Source: ITU World Telecommunication Indicators Database. “The future is here, it’s just not evenly distributed” William Gibson Teledensity 1996 27.8 to68.3 (46) 8.6 to27.8 (45) 1.4 to8.6 (47) 0 to1.4 (48)

8.6 to27.8 (45) 1.4 to8.6 (47) 0 to1.4 (48).")

19

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% Internet users Mobile users Telephone lines Popul- ation High income Upper-mid income Lower-mid income Low income 280 million 490 million 912 million 6 billion 82 % 69 % 58 % 15 % Digital divide = Telecoms divide User distribution, by income group, Jan 2000 Source: ITU World Telecommunication Indicators Database.

20

The digital divide is shrinking, but also shifting Share of low and lower-middle income countries in: Telephone main lines Mobile subscribers Estimated Internet Users Source: ITU World Telecommunication Indicators Database. 18% Jan. 1995Jan. 2000 28% 5%14% 1.1%7.6%

21

LDCs falling further behind: Share of worldwide Internet Users LDCs Share of world population = 10.6% Share of Internet users = 0.1% 0% 2% 4% 6% 8% 10% 19951996199719981999 China Other low & lower- mid income LDCs

23

Share of the USA in the International telephone market

24

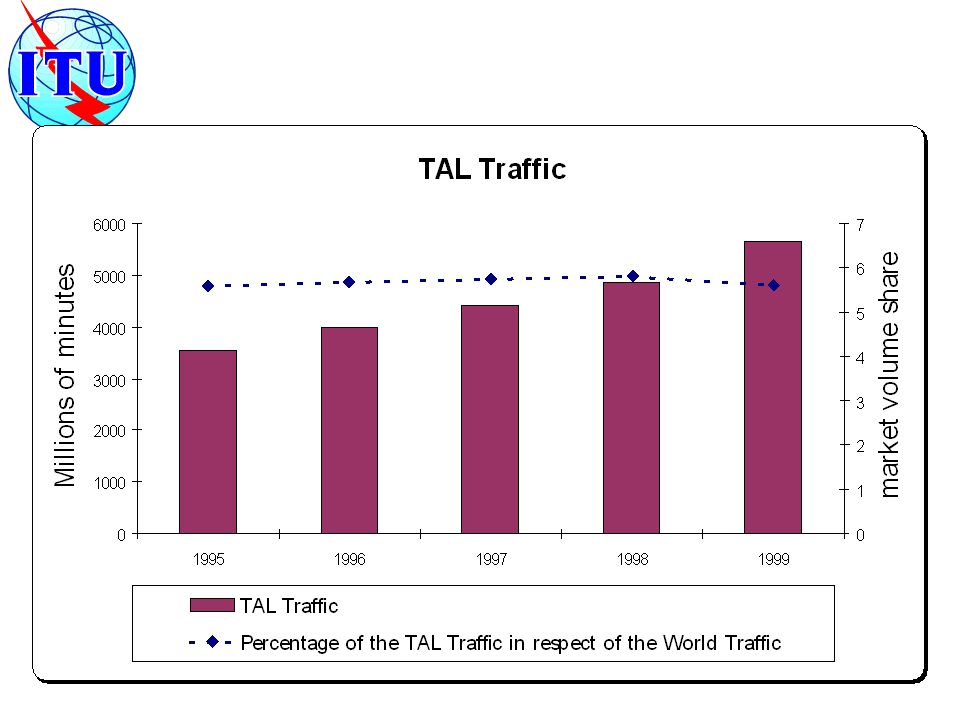

International telephony market TAL Traffic Percentage TAL traffic

26

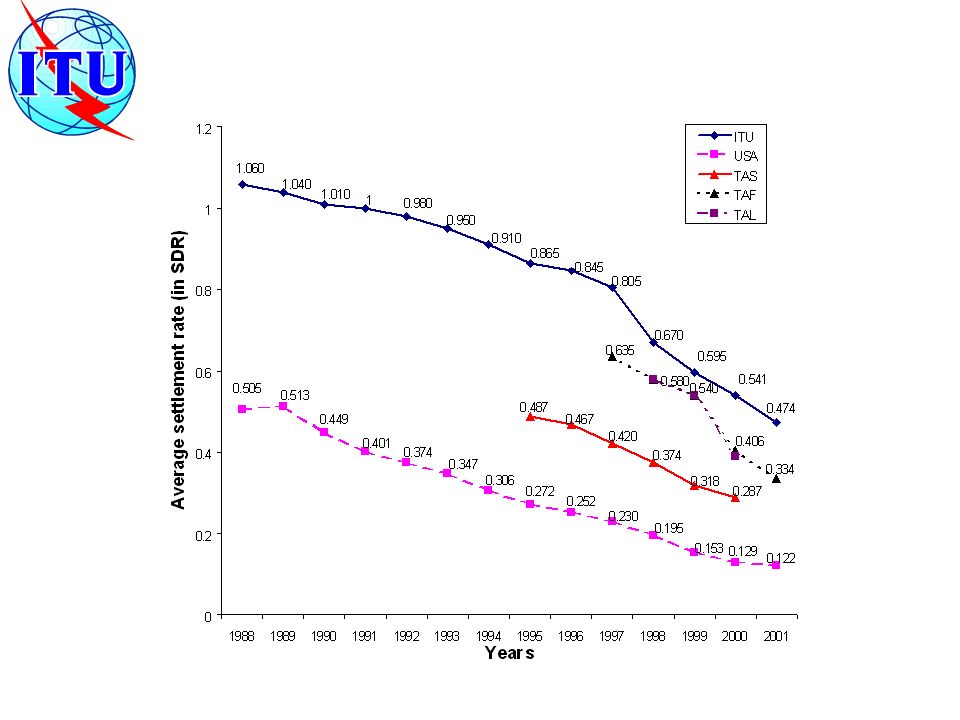

Settlement rates versus Retail prices to the USA in the TAL Region

27

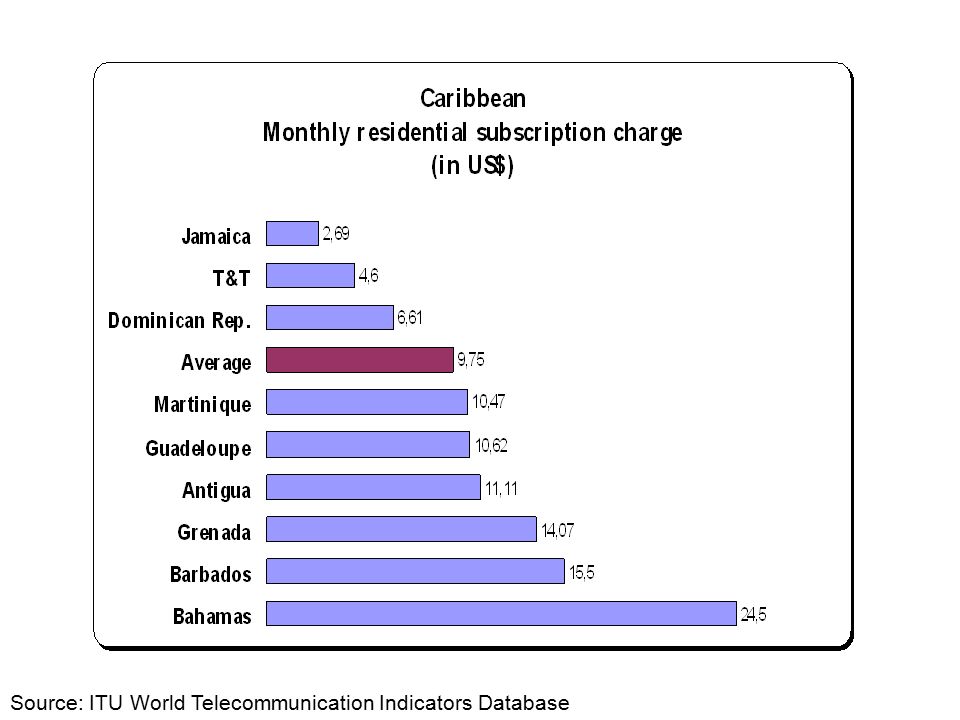

Source: ITU World Telecommunication Indicators Database

31

Degree of competition in cellular services, 2000 by region Source: ITU/BDT Regulatory Database 0% 10% 20% 30% 40% 50% 60% 70% AfricaAmericasAsia- Pacific Arab States Europe MonopolyDuopolyCompetition

32

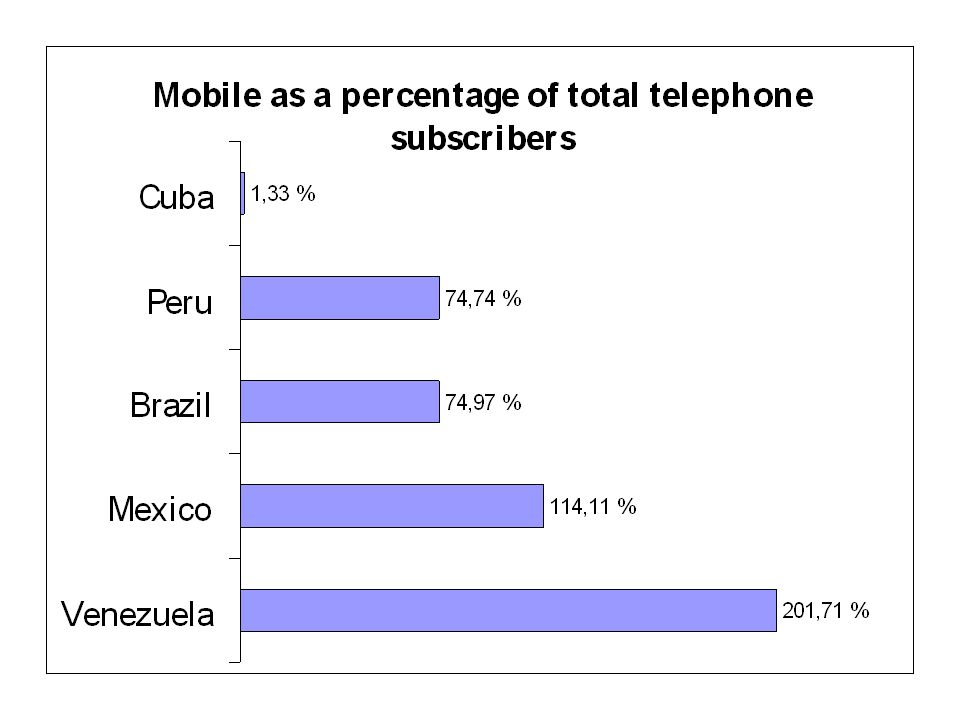

Mobile cellular subscribers, millions Source: ITU

34

Note: The ‘100 minutes of cellular use’ is based on the lowest charge (among different operators in a country) payable for a basket of 50 peak and 50 off-peak minutes of calls per month. Source: ITU adapted from cellular company websites. South America

35

Central America and the Caribbean Note: The ‘100 minutes of cellular use’ is based on the lowest charge (among different operators in a country) payable for a basket of 50 peak and 50 off-peak minutes of calls per month. Source: ITU adapted from cellular company websites.

36

Source: ITU

37

Central America Note: Generally tariffs of leading ISPs. Countries with * indicate unlimited use (no 20 hours package available). Source: ITU adapted from ISP websites

. Source: ITU adapted from ISP websites.")

38

South America

39

As competitors gain market share... Long distance prices come down... Source: ITU Asia-Pacific Telecommunication Indicators, 1997.

40

0 0.2 0.4 0.6 0.8 1 1.2 1.4 1.6 Jan- 88 Jul- 88 Jul- 89 Nov- 90 Oct- 91 Feb- 92 Sep- 93 Jun- 94 Aug- 95 Dec- 96 01- Nov- 97 11- Nov- 97 Local Medium Long distance Rebalancing in action (1): Iceland Telecom, price of 3 minute, peak-rate call, includ. tax Source: Iceland Telecom, OECD.

41

Rebalancing in action (2): SwissCom, price per minute of local call and call to US

: SwissCom, price per minute of local call and call to US")

42

0 2 4 6 8 10 12 19901991199219931994199519961997 300 minutes, local calls 3 mins Int'l call to US Monthly line rental Source: ITU World Telecommunication Indicators Database. Rebalancing in action (3): Average trends in 39 major economies, in US$

: Average trends in 39 major economies, in US$.")

43

Rebalancing in action (4): Trends in Thailand, in US$ Source: ITU World Telecommunication Indicators Database. 0 2 4 6 8 10 12 14 1993199419951996199719981999 300 mins, local calls Monthly line rental 3 mins Int'l call to US

44

Rebalancing in action (5): Trends in price per minute of an international call to USA

: Trends in price per minute of an international call to USA")

45

Conclusion and Recommendation Erosion of traditional system of accounting rates for exchange of international traffic Domestic interconnect fees will be dominant mode Major price cuts in international calls Availability of new infrastructures Impact of Internet pricing model (distance and duration independent) Mobiles exceed fixed-line phones worldwide by 2002/03 Introduction of “third generation” mobiles after 2001 Generational shift, as new users reject fixed-lines “ Interconnection and tariff rebalancing”

Mobiles exceed fixed-line phones worldwide by 2002/03 Introduction of third generation mobiles after 2001 Generational shift, as new users reject fixed-lines Interconnection and tariff rebalancing")

Similar presentations

CTO Annual Council, Gaborone, 20 September 1999 The views expressed in this presentation are those.>")

CTO Annual Council, Gaborone, 21 September 1999 The views expressed in this presentation.>")

Workshop on settlement reform and the costing and.>")

Indicators Gaborone, Botswana 26-29 October 2004>")

Future development of Telecoms and Strategic Initiatives of the ITU HKUST, 7 th December 2000 The.>")

>")