Download presentation

Presentation is loading. Please wait.

1

E-Banking

2

History of banking sector in India

3

The “Presidency Banks”

The Bank of Bengal obtained its charter with a capital base of Rs 50 lacs in the year 1809. It was given the power of note issue in 1823 and in 1839 the power to open branches and to deal in inland exchange. On the same line two other Presidency Banks , the Bank of Bombay and the Bank of Madras , which were subsequently merges to form the Imperial Bank of India- the predecessor of the present State Bank of India. Constituted under the State Bank of India Act ,

4

Classification of banking development in India

5

Foundation phase ( ) The need of the hour was to reorganize and to consolidate the prevailing banking network. Enactment of Banking Regulations Act,1949. Impetus given to both heavy and SSI. Credit extended to agriculture and small borrowers. Branches were expanded at an annual growth of 1.6% during the period from , with deposit and credit growth of 6.9% and 8.2% respectively. The population served per branch was as high as 65,000 as at the end of foundation phase.

6

Rapid expansion phase (1970-1984)

Two historic events took place in the year 1969 that revolutionized the entire banking scenario in the country. Social control on banking companies. Nationalization of 14 major Indian banks During , the branch expansion was 12% per annum and during , it was around 8.8% per annum. On 15 April 1980, the second dose of nationalization of six more commercial banks was affected taking the number of nationalized banks to 20 out of 28 PSU banks including SBI and its subsidiaries.

7

Consolidation phase (1985-1990)

This was a phase of consolidation, which marked slow down in branch expansion. During this period ,expansion of bank branches came to a halt. Profit, which was the major thrust area during the consolidation phase, grew significantly.

8

Reforms phase (1991 onwards)

In 1991 the Government appointed a high level committee headed by M.Narsimhan to examine the existing Indian Financial System. Out of 28 PSU Banks , New Bank of India was merged with PNB in 1993 reducing the number of PSU to 27. Guidelines in terms of the Narsimhan Committee recommendations for setting up of new Private Sector Banks in India. Bank of Punjab, HDFC bank, ICICI bank, IDBI bank, UTI bank, Centurion bank…

9

1955 : Nationalization of State Bank of India.

1959 : Nationalization of SBI subsidiaries. 1969 : Nationalization of 14 major banks. 1980 : Nationalization of seven banks with deposits over 200 crores.

10

Central Bank of India Bank of Maharashtra Dena Bank Punjab National Bank Syndicate Bank Canara Bank Indian Bank Indian Overseas Bank Bank of Baroda Union Bank Allahabad Bank United Bank of India UCO Bank Bank of India

11

INDIAN BANKING : the changing scenario

12

Commercial banks have diversified in three different ways:

13

Horizontal diversification

Wherein banks have added new products & services that appeal to their existing customers and have spread into new geographical areas. The areas in which commercial banks have diversified includes: - consumer credit, credit card business and housing finance.

14

Concentric diversification

Wherein banks have diversified their business to some other activity, which is related to existing one. Like providing financial support to meet term capital needs of industrial enterprisers and extending medium and long term loans to farmers, and to industrialist.

15

Conglomerate diversification

Wherein banks adds new products that are entirely different from present product line or markets and technologies different from present one. Like diversification in non banking functions such as merchant banking, leasing and mutual funds.

16

Merchant Banking Activities – PNB

The Bank is registered with SEBI as Category – I Merchant Banker for providing all the major Merchant Banking services. Our gamut of Merchant Banking services includes:

17

Issue Management Services – to act as Book Running Lead Manager/Lead Manager for the IPOs/FPOs/Right issues/Debt issues Project appraisal Corporate Advisory Services Underwriting of equity issues Banker to the Issue/Paying Banker

18

Refund Banker Monitoring Agency Debenture Trustee Marketing of the issue through a strong network of QIBs/HNIs/Corporates and Retail investor. The Bank itself is one of the major investor in the market having a treasury of crores.

19

The following are the Scheduled Banks in India (Public Sector):

State Bank of India State Bank of Bikaner and Jaipur State Bank of Hyderabad State Bank of Indore State Bank of Mysore State Bank of Saurashtra State Bank of Travancore Andhra Bank

20

Allahabad Bank Bank of Baroda Bank of India Bank of Maharashtra Canara Bank Central Bank of India Corporation Bank Dena Bank Indian Overseas Bank Indian Bank

21

Oriental Bank of Commerce

Punjab National Bank Punjab and Sind Bank Syndicate Bank Union Bank of India United Bank of India UCO Bank Vijaya Bank

22

The following are the Scheduled Banks in India (Private Sector):

ING Vysya Bank Ltd Axis Bank Ltd Indusind Bank Ltd ICICI Bank Ltd South Indian Bank HDFC Bank Ltd Centurion Bank Ltd Bank of Punjab Ltd IDBI Bank Ltd

23

The following are the Scheduled Foreign Banks in India:

American Express Bank Ltd. ANZ Gridlays Bank Plc. Bank of America NT & SA Bank of Tokyo Ltd. Banquc Nationale de Paris Barclays Bank Plc Citi Bank N.C.

24

Deutsche Bank A.G. Hong Kong and Shanghai Banking Corporation Standard Chartered Bank. The Chase Manhattan Bank Ltd. Dresdner Bank AG.

25

Reasons for diversification of banking functions:

26

1) The branch expansion policy coupled with target –oriented credit policies have brought about dimensional and geographical diversifications.

The branch expansion policy coupled with target –oriented credit policies have brought about dimensional and geographical diversifications.")

27

2) The refinement in rural lending policies such as evolution of the concept of direct lending, liberalization of norms and simplifications of lending procedures.

The refinement in rural lending policies such as evolution of the concept of direct lending, liberalization of norms and simplifications of lending procedures.")

28

3) Fast changes in the environment and revolution in the computer and telecommunications technology have led to geographical and functional integration of financial markets beyond the national boundaries.

Fast changes in the environment and revolution in the computer and telecommunications technology have led to geographical and functional integration of financial markets beyond the national boundaries.")

29

4) Deregulations and intensification of competition among banks as also with non – banking financial sectors have led to the emergence of a more diversified and unified financial systems.

Deregulations and intensification of competition among banks as also with non – banking financial sectors have led to the emergence of a more diversified and unified financial systems.")

30

5) The search for new profit opportunities and the desire to diversify to new areas.

The search for new profit opportunities and the desire to diversify to new areas.")

31

6) The emergence of highly attractive non banking deposit instruments and large scale entry of prime corporate borrowers in the new issue market has compelled banks to diversify.

The emergence of highly attractive non banking deposit instruments and large scale entry of prime corporate borrowers in the new issue market has compelled banks to diversify.")

32

7) The financial disinter mediation process whereby the corporate borrowers have preferred to raise resources directly from the market rather than to borrow from banks resulting in decline in profitability led the banks to embark on diversification.

The financial disinter mediation process whereby the corporate borrowers have preferred to raise resources directly from the market rather than to borrow from banks resulting in decline in profitability led the banks to embark on diversification.")

33

The major services apart from traditional banking functions:

34

Issue of bank guarantees

35

Tender/Bid Guarantee Supports the Principal/Applicant’s obligation to execute a contract if the Principal/Applicant is awarded a bid.

36

Advance Payment Guarantee

Supports an obligation to account for an advance payment made by the Beneficiary to the Principal/Applicant. an Advance Payment Guarantee contain a clause that the guarantee is inoperative until the Advance Payment has been received by the Principal/Applicant, as well as a clause allowing for reductions of the guarantee amount.

37

Bill of Lading-/Steamship Guarantee

Supports the shipping company for any financial damages caused by the goods being delivered without the bill of lading. The guarantee is valid until the bill of lading is presented, or until the shipping company releases the bank from its liability.

38

Maintenance Guarantee

Supports remedies and any defects which become apparent after delivery of the goods or after completion of a plant.

39

Performance Guarantee

Supports an obligation to pay for losses which may arise as a consequence of the Principal/Applicant failing to fulfill his obligations under the contract

40

Retention Guarantee Supports an obligation to account for retention money paid by the Beneficiary to the Principal/ Applicant. the Retention Guarantee explicitly stipulates that is does not come into effect until the retention money has been received by the Principal/Applicant.

41

Warranty Guarantee Supports the Beneficiary’s costs should the Principal/Applicant fail to meet his warranty obligations as per the contract terms.

42

Payment Guarantee Supports the payment obligation of the Beneficiary for goods/services delivered by the Principal/ Applicant.

43

Loan Guarantee Supports the repayment of a credit or credit facility including amortization and interest. The guarantee applies from the date the loan is made until it has been repaid.

44

What should a bank guarantee contain?

A definition of the parties involved A reference to The guarantee amount Effective clause The period of validity Documentation A reduction clause

45

Additional points to consider before signing

a contract • Who pays the Issuing Bank’s charges/ commission/fees? • How should the guarantee be drafted? • Which law and jurisdiction should apply?

46

Letter of credit

47

Letter of credit A standard, commercial letter of credit is a document issued mostly by a financial institution, used primarily in trade finance, which usually provides an irrevocable payment undertaking. The LC can also be the source of payment for a transaction, meaning that redeeming the letter of credit will pay an exporter. Letters of credit are used primarily in international trade transactions of significant value, for deals between a supplier in one country and a customer in another.

48

Almost all letters of credit are irrevocable, i. e

Almost all letters of credit are irrevocable, i.e., cannot be amended or canceled without prior agreement of the beneficiary, the issuing bank and the confirming bank, if any. In executing a transaction, letters of credit incorporate functions common to giros and Traveler's cheques. Typically, the documents a beneficiary has to present in order to receive payment include a commercial invoice, bill of lading, and documents proving the shipment was insured against loss or damage in transit.

49

After a contract is concluded between buyer and seller, buyer's bank supplies a letter of credit to seller.

51

Seller consigns the goods to a carrier in exchange for a bill of lading.

53

Seller provides bill of lading to bank in exchange for payment

Seller provides bill of lading to bank in exchange for payment. Seller's bank exchanges bill of lading for payment from buyer's bank. Buyer's bank exchanges bill of lading for payment from the buyer.

55

Buyer provides bill of lading to carrier and takes delivery of goods.

57

Trade Online Features Submit an online application for a Letter of Credit View details of all letter of credit and bank guarantees opened by the bank and status of the same. View the details of inward and outward bills discounted with ICICI Bank. Track outstanding forward contracts entered with the ICICI Bank.

58

The main instruments of remittance are:

Demand drafts Mail transfers Telegraphic transfer Electronic fund transfer Traveler cheques Gift cheques

59

Merchant banking Management of customer’s securities

Portfolio management Credit syndication Acceptance credit Counseling Insurance etc.

60

Dr Rangarajan committee report (1989)

A 16 member committee with Dr C Rangarajan was formed in 1988 to make recommendations for computerization in banking industry in general and Nationalized banks in particular.

61

Major recommendations:

Regional office/ zonal office / head office should be computerized. All branches located in top 30 centers should be computerized. Branches having average 750 vouchers per day should be computerized. Banknet and Swift to be used by banks. Online terminals should be given at the premises of corporate customers.

62

Total branch automation (TBA)

In contrast to partial automation which involves computerization of front offices ( i.e. SB,CD, Term deposit) or back office ( i.e. day book , GL ,MIS etc.) total branch automation involves computerization of all operations in the branch.

or back office ( i.e. day book , GL ,MIS etc.) total branch automation involves computerization of all operations in the branch.")

63

Main features: Server : it is the main device , which stores data of large capacity and process the request of all users. Work stations: in a TBA branch all operations can be done from any terminals as they are connected to each other and also to the server. A customer desiring to operate his SB account can to so from any counter and not necessarily from SB counter.

64

Networking Networking means linking computers with each other by means of cable so that they can share information and resources and can communicate with each other.

65

LAN LOCAL AREA NETWORK When a network serves a small area, such as one building or a group of building. You might have a LAN for example on a University campus or between office blocks in an office park.

66

WAN WIDE AREA NETWORK When computers located in far off distances are networked .

67

RBINET Connects all offices of RBI and corporate headquarters of commercial banks became functional in December 1994

68

SWIFT Founded in Brussels in 1973, the Society for the Worldwide Interbank Financial Telecommunication (SWIFT) is a co-operative organization dedicated to the promotion and development of standardized global interactivity for financial transactions Swift's original mandate was to establish a global communications link for data processing and a common language for international financial transactions.

is a co-operative organization dedicated to the promotion and development of standardized global interactivity for financial transactions. Swift s original mandate was to establish a global communications link for data processing and a common language for international financial transactions.")

69

The Society operates a messaging service for financial messages, such as letters of credit, payments, and securities transactions, between member banks worldwide. Swift's essential function is to deliver these messages quickly and securely -- both of which are prime considerations for financial matters Member organizations create formatted messages that are then forwarded to SWIFT for delivery to the recipient member organization. SWIFT operates out of its Brussels headquarters and processes data at centers in Belgium and the United States.

70

How is the SWIFT network accessed?

Users can either enter the network via a leased line, dial-up connection or Public Data Network connection to regional processors that link up to the SWIFT network. Each user site has its own terminal for entering the network and entering messages once connected. Access normally requires both a username and password to be entered, and uses Smart Card technology.

71

Can anyone become a member of SWIFT?

No, the organization must hold a Banking License in order to become a member. Members pay a joining fee and are then charged for each message they send.

72

Why was SWIFT created? Because of the limitations of the then used system, Telex. Telex was considered too slow, too insecure and didn't have a standardized format for the data it transferred, all of which added up to an inefficient system. Access normally requires both a username and password to be entered, and uses Smart Card technology. As a result seven major international banks met in 1974 to discuss a suitable replacement for Telex. A society was formed in 1977 and 230 banks from five countries went live with the system. SWIFT currently has around 7,000 members from nearly 200 countries.

73

How many messages does SWIFT handle a day?

Since its inception in the late 1970s, SWIFT has had to increase the number and type of messages it handles to cope with the expansion in the type of financial transactions that are possible. It now handles around five million messages a day.

74

ISO 9362 (also known as SWIFT-BIC, BIC code, SWIFT ID or SWIFT code) is a standard format of Bank Identifier Codes approved by the International Organization for Standardization (ISO). It is the unique identification code of a particular bank. These codes are used when transferring money between banks, particularly for international wire transfers, and also for the exchange of other messages between banks. The codes can sometimes be found on account statements.

75

The SWIFT code is 8 or 11 characters, made up of:

4 characters - bank code (only letters) 2 characters - ISO alpha-2 country code (only letters) 2 characters - location code (letters and digits) (if the second character is '1', then it denotes a passive participant in the SWIFT network) 3 characters - branch code, optional ('XXX' for primary office) (letters and digits)

2 characters - ISO alpha-2 country code (only letters) 2 characters - location code (letters and digits) (if the second character is 1 , then it denotes a passive participant in the SWIFT network) 3 characters - branch code, optional ( XXX for primary office) (letters and digits)")

76

SWIFT BIC Code BANK US [XXX] Institution Country Location Branch Code code code code

![SWIFT BIC Code BANK US 33 [XXX] Institution Country Location Branch.](http://slideplayer.com/slide/8463868/26/images/76/SWIFT+BIC+Code+BANK+US+33+%5BXXX%5D+Institution+Country+Location+Branch..jpg "Code code code code.")

77

Deutsche Bank is an international bank, with its head office in Frankfurt, Germany. The SWIFT code for its primary office is DEUTDEFF: DEUT identifies Deutsche Bank DE is the country code for Germany FF is the code for Frankfurt

78

Deutsche Bank uses an extended code of 11 digits and has assigned branches or processing areas individual extended codes. This allows the payment to be directed to a specific office. For example, DEUTDEFF500 would direct the payment to an office of Deutsche Bank in Bad Homburg.

79

Mumbai SWIFT Code: SBININBB110

Delhi SWIFT Code: SBININBB104 PUNBINBB DIB

80

Advantages of SWIFT message

Security Cheaper cost Speed Side access

81

SWIFT for banks SWIFT was formed more than 35 years ago by, 239 banks in 15 countries. Today, meeting the operational requirements of banks remains a core focus for us.

82

1) The need to reduce costs: payment and cash management businesses (except in Asia) are growing slowly and revenue per transaction is declining. SWIFT provides reach, reusability and standardization to help reduce your costs.

83

2) The need to reduce fraud and risk: you are facing new regulation and industry initiatives such as SEPA and TARGET2 which demand high investments and squeeze margins. SWIFT can help with the regulation and we offer security and reliability to help you reduce your operational risk.

84

Real time gross settlement systems (RTGS) are a funds transfer mechanism where transfer of money takes place from one bank to another on a "real time" and on "gross" basis. Settlement in "real time" means payment transaction is not subjected to any waiting period. The transactions are settled as soon as they are processed. "Gross settlement" means the transaction is settled on one to one basis without bunching with any other transaction

85

RTGS systems covering multiple countries:

TARGET resp. TARGET2 (Trans-European Automated Real-time Gross Settlement Express Transfer System) in 26 countries of the European Union

in 26 countries of the European Union.")

86

A Single Euro Payments Area - SEPA

SWIFT is actively supporting its members and customers in their implementation of SEPA by developing standards and providing a set of products and services to facilitate operation and interoperability across the industry. The Single Euro Payments Area (SEPA) is the area where citizens, companies and other economic players will be able to make and receive payments in euros (whether between or within national boundaries) under the same basic conditions, rights and obligations, regardless of their location.

is the area where citizens, companies and other economic players will be able to make and receive payments in euros (whether between or within national boundaries) under the same basic conditions, rights and obligations, regardless of their location.")

87

Every citizen, merchant, public administration and corporation with a banking relationship in the euro-area ultimately will be impacted by SEPA, as will everyone in the payments supply chain.

88

3) The ability to create new revenue streams: as commoditization continues, one way you can distinguish yourself in the market is through superior customer service. SWIFT supports this with solutions like Exceptions and Investigations and Workers’ Remittances.

89

4) Globalization of the supply chain: you need cross border payments and trade finance solutions. SWIFT offers both, including the industry-leading Trade Service Utility.

90

What can I do with my SWIFT connection?

91

a) For payments Bulk Payments Harmonizing bulk payment practices across communities Cash Reporting Supporting your real-time account information needs Exceptions and Investigations Making investigations pay Workers' Remittances Fast, efficient, and cost-effective clearing and settlement of person-to-person payments

92

b) For treasury Accord Enabling real-time matching and exception handling for foreign exchange, money market and derivative confirmations. Affirmations Providing a cost-effective way of enhancing STP across the treasury and derivative markets. Swift's CLS Third Party Service Providing a global FX settlement solution for non-CLS members

93

Cont.. STP Straight Through Processing (STP)

"The processing of a trade, whose data is compliant with internal and external requirements, through systems from post-execution through settlement without manual intervention".

94

c) For trade Trade Services Utility Helping banks meet the supply chain challenge

For trade Trade Services Utility Helping banks meet the supply chain challenge")

95

Automated teller machine

An automated teller machine (ATM) is a computerized telecommunications device that provides the customers of a financial institution with access to financial transactions in a public space without the need for a human clerk or bank teller.

is a computerized telecommunications device that provides the customers of a financial institution with access to financial transactions in a public space without the need for a human clerk or bank teller.")

96

On most modern ATMs, the customer is identified by inserting a plastic ATM card with a magnetic stripe or a plastic smartcard with a chip, that contains a unique card number and some security information, such as an expiration date or CVVC (CVV). Security is provided by the customer entering a personal identification number (PIN).

..")

97

ATMs rely on authorization of a financial transaction by the card issuer or other authorizing institution via the communications network. This is often performed through an ISO 8583 messaging system.

98

An ATM is typically made up of the following devices:

102

a) Hardware CPU (to control the user interface and transaction devices) Magnetic and/or Chip card reader (to identify the customer) PIN Pad (similar in layout to a Touch tone or Calculator keypad), often manufactured as part of a secure enclosure. Secure crypto processor, generally within a secure enclosure. Display (used by the customer for performing the transaction)

, often manufactured as part of a secure enclosure. Secure crypto processor, generally within a secure enclosure. Display (used by the customer for performing the transaction)")

103

Function key buttons (usually close to the display) or a Touch screen (used to select the various aspects of the transaction) Record Printer (to provide the customer with a record of their transaction) Vault (to store the parts of the machinery requiring restricted access)

Vault (to store the parts of the machinery requiring restricted access)")

104

b) Software

Software")

105

Financial networks in ATMs

Most ATMs are connected to inter bank networks, enabling people to withdraw and deposit money from machines not belonging to the bank where they have their account or in the country where their accounts are held (enabling cash withdrawals in local currency). Some examples of inter bank networks include PULSE, PLUS, Cirrus, Interac, Inters witch, STAR (inter bank network), and LINK.

. Some examples of inter bank networks include PULSE, PLUS, Cirrus, Interac, Inters witch, STAR (inter bank network), and LINK.")

106

Cirrus is a worldwide inter bank network operated by MasterCard Worldwide, and was founded in It links MasterCard, Maestro, Diners Club credit, debit and prepaid cards to a network of over 1,000,000 ATMs in 93 countries Pulse is an inter bank electronic funds transfer (EFT) network in the United States PLUS (also known as Visa PLUS) is an inter bank network that covers all VISA credit, debit, and prepaid cards, as well as ATM cards issued by various banks worldwide. Currently, there are one million PLUS-linked ATMs in 170 countries worldwide

network in the United States. PLUS (also known as Visa PLUS) is an inter bank network that covers all VISA credit, debit, and prepaid cards, as well as ATM cards issued by various banks worldwide. Currently, there are one million PLUS-linked ATMs in 170 countries worldwide.")

107

Growth in Internet Banking

Some of the market factors that may drive a bank’s strategy include the following:

108

1) Competition — Studies show that competitive pressure is the chief driving force behind increasing use of Internet banking technology, ranking ahead of cost reduction and revenue enhancement, in second and third place respectively. Banks see Internet banking as a way to keep existing customers and attract new ones to the bank.

109

2) Cost Efficiencies — National banks can deliver banking services on the Internet at transaction costs far lower than traditional brick-and-mortar branches. The actual costs to execute a transaction will vary depending on the delivery channel used. For example, according to Booz, Allen & Hamilton, as of mid- 1999, the cost to deliver manual transactions at a branch was typically more than a dollar, ATM and call center transactions cost about 25 cents, and Internet transactions cost about a penny. These costs are expected to continue to decline.

110

3) Geographical Reach — Internet banking allows expanded customer contact through increased geographical reach and lower cost delivery channels. In fact some banks are doing business exclusively via the Internet — they do not have traditional banking offices and only reach their customers online. Other financial institutions are using the Internet as an alternative delivery channel to reach existing customers and attract new customers.

111

4) Branding — Relationship building is a strategic priority for many national banks. Internet banking technology and products can provide a means for national banks to develop and maintain an ongoing relationship with their customers by offering easy access to a broad array of products and services.

112

5) Customer Demographics — Internet banking allows national banks to offer a wide array of options to their banking customers. Some customers will rely on traditional branches to conduct their banking business. For many, this is the most comfortable way for them to transact their banking business. Those customers place a premium on person-to-person contact. Other customers are early adopters of new technologies that arrive in the marketplace. The demographics of banking customers will continue to change. The challenge to national banks is to understand their customer base and find the right mix of delivery channels to deliver products and services profitably to their various market segments.

113

Types of Internet Banking

114

1) Informational — This is the basic level of Internet banking

1) Informational — This is the basic level of Internet banking. Typically, the bank has marketing information about the bank’s products and services on a stand-alone server. The risk is relatively low, as informational systems typically have no path between the server and the bank’s internal network. This level of Internet banking can be provided by the bank or outsourced. While the risk to a bank is relatively low, the server or Web site may be vulnerable to alteration. Appropriate controls therefore must be in place to prevent unauthorized alterations to the bank’s server or Web site.

Informational — This is the basic level of Internet banking. Typically, the bank has marketing information about the bank’s products and services on a stand-alone server. The risk is relatively low, as informational systems typically have no path between the server and the bank’s internal network. This level of Internet banking can be provided by the bank or outsourced. While the risk to a bank is relatively low, the server or Web site may be vulnerable to alteration. Appropriate controls therefore must be in place to prevent unauthorized alterations to the bank’s server or Web site.")

115

2) Communicative — This type of Internet banking system allows some interaction between the bank’s systems and the customer. The interaction may be limited to electronic mail, account inquiry, loan applications, or static file updates (name and address changes). Because these servers may have a path to the bank’s internal networks, the risk is higher with this configuration than with informational systems. Appropriate controls need to be in place to prevent, monitor, and alert management of any unauthorized attempt to access the bank’s internal networks and computer systems. Virus controls also become much more critical in this environment.

. Because these servers may have a path to the bank’s internal networks, the risk is higher with this configuration than with informational systems. Appropriate controls need to be in place to prevent, monitor, and alert management of any unauthorized attempt to access the bank’s internal networks and computer systems. Virus controls also become much more critical in this environment.")

116

3) Transactional — This level of Internet banking allows customers to execute transactions.

Since a path typically exists between the server and the bank’s or outsourcer’s internal network, this is the highest risk architecture and must have the strongest controls. Customer transactions can include accessing accounts, paying bills, transferring funds, etc.

117

Convenience or inconvenience banking

118

Risk : it is the possibility that an intruder may be successful in attempting to access your local area network. Threat : threat is posed when anyone with the motivation , attempts to gain unauthorized access to a network or anyone has authorized access to your network.

119

Internet Banking Risks

120

1) Credit Risk Credit risk is the risk to earnings or capital arising from an obligor’s failure to meet the terms of any contract with the bank or otherwise to perform as agreed. Credit risk is found in all activities where success depends on counterparty, issuer, or borrower performance. It arises any time bank funds are extended, committed, invested, or otherwise exposed through actual or implied contractual agreements, whether on or off the banks balance sheet.

121

Internet banking provides the opportunity for banks to expand their geographic range.

Customers can reach a given institution from literally anywhere in the world. In dealing with customers over the Internet, absent any personal contact, it is challenging for institutions to verify the bonafides of their customers, which is an important element in making sound credit decisions. Verifying collateral and perfecting security agreements also can be challenging with out-of-area borrowers. Unless properly managed, Internet banking could lead to a concentration in out-of-area credits or credits within a single industry. Moreover, the question of which state’s or country’s laws control an Internet relationship is still developing.

122

2) Interest Rate Risk Interest rate risk is the risk to earnings or capital arising from movements in interest rates. From an economic perspective, a bank focuses on the sensitivity of the value of its assets, liabilities and revenues to changes in interest rates. Evaluation of interest rate risk must consider the impact of complex, illiquid hedging strategies or products, and also the potential impact that changes in interest rates will have on fee income.

123

3) Liquidity Risk Liquidity risk is the risk to earnings or capital arising from a bank’s inability to meet its obligations when they come due, without incurring unacceptable losses. Liquidity risk includes the inability to manage unplanned changes in funding sources. Liquidity risk also arises from the failure to recognize or address changes in market conditions affecting the ability of the bank to liquidate assets quickly and with minimal loss in value.

124

Internet banking can increase deposit volatility from customers who maintain accounts solely on the basis of rate or terms. Increased monitoring of liquidity and changes in deposits and loans may be warranted depending on the volume and nature of Internet account activities.

125

4) Price Risk Price risk is the risk to earnings or capital arising from changes in the value of traded portfolios of financial instruments. This risk arises from market making, dealing, and position taking in interest rate, foreign exchange, equity, and commodities markets. Banks may be exposed to price risk if they create or expand deposit brokering, loan sales, or securitization programs as a result of Internet banking activities. Appropriate management systems should be maintained to monitor, measure, and manage price risk if assets are actively traded.

126

5) Foreign Exchange Risk

Foreign exchange risk is present when a loan or portfolio of loans is denominated in a foreign currency or is funded by borrowings in another currency. In some cases, banks will enter into multi-currency credit commitments that permit borrowers to select the currency they prefer to use in each rollover period. Foreign exchange risk can be intensified by political, social, or economic developments. The consequences can be unfavorable if one of the currencies involved becomes subject to stringent exchange controls or is subject to wide exchange-rate fluctuations.

127

Banks may be exposed to foreign exchange risk if they accept deposits from non-U.S. residents or create accounts denominated in currencies other than U.S. dollars. Appropriate systems should be developed if banks engage in these activities.

128

6)Transaction Risk Transaction risk is the current and prospective risk to earnings and capital arising from fraud, error, and the inability to deliver products or services, maintain a competitive position, and manage information. A high level of transaction risk may exist with Internet banking products, particularly if those lines of business are not adequately planned, implemented, and monitored Banks that offer financial products and services through the Internet must be able to meet their customers’ expectations

129

Banks must also ensure they have the right product mix and capacity to deliver accurate, timely, and reliable services to develop a high level of confidence in their brand name. Customers who do business over the Internet are likely to have little tolerance for errors or omissions from financial institutions that do not have sophisticated internal controls to manage their Internet banking business. Likewise, customers will expect continuous availability of the product and Web pages that are easy to navigate.

130

7) Compliance Risk Compliance risk is the risk to earnings or capital arising from violations of, or nonconformance with, laws, rules, regulations, prescribed practices, or ethical standards. Compliance risk also arises in situations where the laws or rules governing certain bank products or activities of the bank’s clients may be ambiguous or untested. Compliance risk exposes the institution to fines, civil money penalties, payment of damages, and the voiding of contracts. Compliance risk can lead to a diminished reputation, reduced franchise value, limited business opportunities, reduced expansion potential, and lack of contract enforceability.

131

Most Internet banking customers will continue to use other bank delivery channels.

Accordingly, national banks will need to make certain that their disclosures on Internet banking channels, including Web sites, remain synchronized with other delivery channels to ensure the delivery of a consistent and accurate message to customers.

132

8) Strategic Risk Strategic risk is the current and prospective impact on earnings or capital arising from adverse business decisions, improper implementation of decisions, or lack of responsiveness to industry changes. This risk is a function of the compatibility of an organization’s strategic goals, the business strategies developed to achieve those goals, the resources deployed against these goals, and the quality of implementation. The resources needed to carry out business strategies are both tangible and intangible. The organization’s internal characteristics must be evaluated against the impact of economic, technological, competitive, regulatory, and other environmental changes.

133

Management must understand the risks associated with Internet banking before they make a decision to develop a particular class of business. In some cases, banks may offer new products and services via the Internet. It is important that management understand the risks and ramifications of these decisions. Sufficient levels of technology and MIS are necessary to support such a business venture. Because many banks will compete with financial institutions beyond their existing trade area, those engaging in Internet banking must have a strong link between the technology employed and the bank’s strategic planning process.

134

Before introducing a Internet banking product, management should consider whether the product and technology are consistent with tangible business objectives in the bank’s strategic plan. The bank also should consider whether adequate expertise and resources are available to identify, monitor, and control risk in the Internet banking business. The planning and decision making process should focus on how a specific business need is met by the Internet banking product, rather than focusing on the product as an independent objective.

135

9) Reputation Risk Reputation risk is the current and prospective impact on earnings and capital arising from negative public opinion. This affects the institution’s ability to establish new relationships or services or continue servicing existing relationships. This risk may expose the institution to litigation, financial loss, or a decline in its customer base. Reputation risk exposure is present throughout the organization and includes the responsibility to exercise an abundance of caution in dealing with customers and the community.

136

A bank’s reputation can suffer if it fails to deliver on marketing claims or to provide accurate, timely services. This can include failing to adequately meet customer credit needs, providing unreliable or inefficient delivery systems, untimely responses to customer inquiries, or violations of customer privacy expectations.

137

Risk Management

138

1) The risk planning process is the responsibility of the board and senior management. They need to possess the knowledge and skills to manage the bank’s use of Internet banking technology and technology-related risks. The board should review, approve, and monitor Internet banking technology-related projects that may have a significant impact on the bank’s risk profile. They should determine whether the technology and products are in line with the bank’s strategic goals and meet a need in their market.

139

Senior management should have the skills to evaluate the technology employed and risks assumed.

Periodic independent evaluations of the Internet banking technology and products by auditors or consultants can help the board and senior management fulfill their responsibilities

140

2) Implementing the technology is the responsibility of management.

Management should have the skills to effectively evaluate Internet banking technologies and products, select the right mix for the bank, and see that they are installed appropriately. If the bank does not have the expertise to fulfill this responsibility internally, it should consider contracting with a vendor who specializes in this type of business or engaging in an alliance with another provider with complementary technologies or expertise.

141

3) Measuring and monitoring risk is the responsibility of management.

Management should have the skills to effectively identify, measure, monitor, and control risks associated with Internet banking. The board should receive regular reports on the technologies employed, the risks assumed, and how those risks are managed. Monitoring system performance is a key success factor. As part of the design process, a national bank should include effective quality assurance and audit processes in its Internet banking system.

142

Internal Controls Consistency of technology planning and strategic goals, including efficiency and economy of operations and compliance with corporate policies and legal requirements. Data availability, including business recovery planning. Data integrity, including providing for the safeguarding of assets, proper authorization of transactions, and reliability of the process and output. Data confidentiality and privacy safeguards. Reliability of MIS.

143

The three control categories can be found in the basic internal controls discussed above.

Preventive Controls — Prevent something (often an error or illegal act) from happening. An example of this type of control is logical access control software that would allow only authorized persons to access a network using a combination of a user ID and password. Detective Controls — Identify an action that has occurred. An example would be intrusion detection software that triggers an alert or alarm. Corrective Controls — Correct a situation once it has been detected. An example would be software backups that could be used to recover a corrupted file or database.

from happening. An example of this type of control is logical access control software that would allow only authorized persons to access a network using a combination of a user ID and password. Detective Controls — Identify an action that has occurred. An example would be intrusion detection software that triggers an alert or alarm. Corrective Controls — Correct a situation once it has been detected. An example would be software backups that could be used to recover a corrupted file or database.")

144

Examples of these controls could include:

Monitoring transaction activity to look for anomalies in transaction types, transaction volumes, transaction values, and time-of-day presentment. Monitoring log-on violations or attempts to identify patterns of suspect activity including unusual requests, unusual timing, or unusual formats. Using trap and trace techniques to identify the source of the request and match these against known customers.

145

Regular reporting and review of unusual transactions will help identify:

Intrusions by unauthorized parties. Customer input errors. Opportunities for customer education.

146

Issues in Internet Banking

147

1) Security is an issue in Internet banking systems.

Some national banks allow for direct dial-in access to their systems over a private network while others provide network access through the Internet. Although the publicly accessible Internet generally may be less secure, both types of connections are vulnerable to interception and alteration.

148

2) Authentication is another issue in a Internet banking system.

Transactions on the Internet or any other telecommunication network must be secure to achieve a high level of public confidence. In cyberspace, as in the physical world, customers, banks, and merchants need assurances that they will receive the service as ordered or the merchandise as requested, and that they know the identity of the person they are dealing with.

149

3) Trust is another issue in Internet banking systems.

As noted in the previous discussion, public and private key cryptographic systems can be used to secure information and authenticate parties in transactions in cyberspace. A trusted third party is a necessary part of the process. That third party is the certificate authority.

150

4) Nonrepudiation is the undeniable proof of participation by both the sender and receiver in a transaction. It is the reason public key encryption was developed, i.e., to authenticate electronic messages and prevent denial or repudiation by the sender or receiver.

151

5) Privacy is a consumer issue of increasing importance.

National banks that recognize and respond to privacy issues in a proactive way make this a positive attribute for the bank and a benefit for its customers.

152

6) Availability is another component in maintaining a high level of public confidence in a network environment. All of the previous components are of little value if the network is not available and convenient to customers. Users of a network expect access to systems 24 hours per day, seven days a week.

153

Significance of computerization in banks

Any time banking Anywhere banking Home banking Corporate banking Mobile banking Mobile payment Security Technology

154

Finance portals for the banking industry

User interface Contents and services Backend transactions Enabling functions

155

Constraints in e banking

Start up cost Initial cost Connection cost of internet Cost of hardware and software Cost of setting up organizational activities Training and maintenance Lack of skilled personnel Restricted clientele and technical problem Security Controls Authenticity control Accuracy control Completeness control Redundancy control Privacy control Firewall control Encryption control

156

Legal issues in e banking

Considering the legal position prevalent, there is an obligation on the part of banks not only to establish the identity but also to make enquiries about integrity and reputation of the prospective customer. Therefore, even though request for opening account can be accepted over Internet, accounts should be opened only after proper introduction and physical verification of the identity of the customer. From a legal perspective, security procedure adopted by banks for authenticating users needs to be recognized by law as a substitute for signature.

157

Under the present regime there is an obligation on banks to maintain secrecy and confidentiality of customers‘ accounts. In the Internet banking scenario, the risk of banks not meeting the above obligation is high on account of several factors. ss

158

Despite all reasonable precautions, banks may be exposed to enhanced risk of liability to customers on account of breach of secrecy, denial of service etc., because of hacking/ other technological failures. The banks should, therefore, institute adequate risk control measures to manage such risks.

159

In Internet banking scenario there is very little scope for the banks to act on stop-payment instructions from the customers. Hence, banks should clearly notify to the customers the timeframe and the circumstances in which any stop-payment instructions could be accepted.

160

The Consumer Protection Act, 1986 defines the rights of consumers in India and is applicable to banking services as well. Currently, the rights and liabilities of customers availing of Internet banking services are being determined by bilateral agreements between the banks and customers. Considering the banking practice and rights enjoyed by customers in traditional banking, banks’ liability to the customers on account of unauthorized transfer through hacking, denial of service on account of technological failure etc. needs to be assessed and banks providing Internet banking should insure themselves against such risks

161

Regulatory and Supervisory Issues

As recommended by the Group, the existing regulatory framework over banks will be extended to Internet banking also. In this regard, it is advised that:

162

Only such banks which are licensed and supervised in India and have a physical presence in India will be permitted to offer Internet banking products to residents of India. Thus, both banks and virtual banks incorporated outside the country and having no physical presence in India will not, for the present, be permitted to offer Internet banking services to Indian residents. The products should be restricted to account holders only and should not be offered in other jurisdictions. The services should only include local currency products.

163

The ‘in-out’ scenario where customers in cross border jurisdictions are offered banking services by Indian banks (or branches of foreign banks in India) and the ‘out-in’ scenario where Indian residents are offered banking services by banks operating in cross-border jurisdictions are generally not permitted and this approach will apply to Internet banking also.

and the ‘out-in’ scenario where Indian residents are offered banking services by banks operating in cross-border jurisdictions are generally not permitted and this approach will apply to Internet banking also.")

164

The existing exceptions for limited purposes under FEMA i. e

The existing exceptions for limited purposes under FEMA i.e. where resident Indians have been permitted to continue to maintain their accounts with overseas banks etc., will, however, be permitted. Overseas branches of Indian banks will be permitted to offer Internet banking services to their overseas customers subject to their satisfying, in addition to the host supervisor, the home supervisor.

165

Evolution of Payment Systems in India

Payment instruments and mechanisms have a very long history in India. The earliest payment instruments known to have been used in India were coins, which were either punch-marked or cast in silver and copper. While coins represented a physical equivalent, credit systems involving bills of exchange facilitated inter-spatial transfers.

166

Another instrument in use during the Muslim period was the Pay order.

Pay orders were issued from the Royal Treasury on one of the District or Provincial treasuries. They were called Barattes and were akin to present day drafts or cheques

167

The most important class of credit Instruments that evolved in India were termed Hundis.

Their use was most widespread in the twelfth century, and has continued till today. In a sense, they represent the oldest surviving form of credit instrument. Hundis were used : * as remittance instruments (to transfer funds from one place to another) * as credit instruments (to borrow money [IOUs]) * for trade transactions (as bills of exchange)

* as credit instruments (to borrow money [IOUs]) * for trade transactions (as bills of exchange)")

169

Paper money, in the modern sense, has its origin in the late 18th century with the note issues of private banks as well as semi-government banks. Amongst the earliest issues were those by the Bank of Hindoostan, the General Bank in Bengal and Behar, and the Bengal Bank. Later, with the establishment of three Presidency Banks, the job of issuing notes was taken over by them. Each Presidency Bank had the right to issue notes within certain limits The private banks and the Presidency Banks introduced other payment instruments in the Indian money market. Cheques were introduced by the Bank of Hindoostan, the first joint stock bank established in 1770.

170

Payment Instruments in India

The NI Act, 1881, defines a Negotiable Instrument as a promissory note, Bill of Exchange or cheque. A Bill of Exchange is an instrument in writing containing an unconditional order, signed by the maker, directing a certain person to pay a certain sum of money only to, or to the order of, a certain person or to the bearer of the instrument. A Hundi is a Bill of Exchange in an Indian language, governed by customs and local usage. The NI Act, however, does not govern Hundis. A Bill of Exchange may therefore, include a Hundi, but Hundi may not be a Bill of Exchange.

171

A cheque is a Bill of Exchange drawn on a specified banker and not expressed to be payable otherwise than on demand. The maker of a cheque is called the 'drawer', and the person directed to pay is the 'drawee'. The person named in the instrument, to whom or to whose order the money is, by the instrument directed, to be paid, is called the 'payee'. A cheque is a Negotiable Instrument, which can be further negotiated by means of endorsement and is payable on demand.

172

The Demand Draft is a pre-paid Negotiable Instrument, wherein the drawee bank undertakes to make payment in full when the instrument is presented by the payee for payment. The demand draft is made payable on a specified branch of a bank at a specified centre. In order to obtain payment, the beneficiary has to either present the instrument directly to the branch concerned or have it collected by his / her bank through the clearing mechanism.

173

In essence, the payment systems are required for the following purposes:

1. For protecting key existing assets of the banking system: 2. For strengthening the customer base: 3: For Reducing existing costs and generating new income:

174

Institutional Arrangements

175

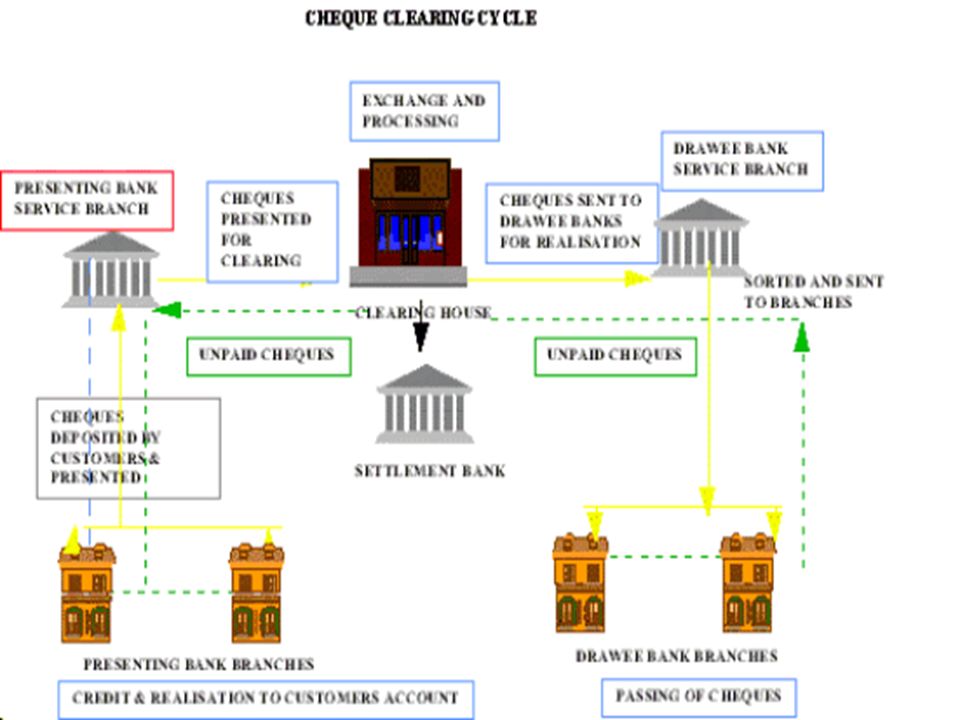

Clearing Process: The clearing process begins with the deposit of a cheque in a bank. The cheque (along with other cheques) is delivered to the bank/branch where it is drawn. The cheque is passed for payment if the funds are available and the banker is satisfied about the genuineness of the instrument. The cheques that are unpaid are returned to the presenting bank through another clearing called the Return Clearing. The realization of the funds occurs after the completion of return clearing and by the absence of an unpaid cheque.

is delivered to the bank/branch where it is drawn. The cheque is passed for payment if the funds are available and the banker is satisfied about the genuineness of the instrument. The cheques that are unpaid are returned to the presenting bank through another clearing called the Return Clearing. The realization of the funds occurs after the completion of return clearing and by the absence of an unpaid cheque.")

177

Settlement of Funds: The settlement of funds in clearing occurs at several levels. The aggregate amount or value of cheques presented by a bank on other banks represents the claim by that bank on other banks. Similar claims are made by all the banks on every other bank in the clearing. A net settlement is arrived at the clearing house and the debit or credit position of the bank is determined. These are booked in their current accounts maintained by the settling bank. This represents the inter- bank settlement. The settlement of funds between the service branch and the branch concerned represents the transfer of funds to the branch level.

178

The payment process is completed only when the funds are debited from the drawer's account and credited to the payee's account. This occurs after the completion of the return clearing mentioned earlier.

180

Return Clearing Realization of a cheque i.e. payment occurs after the cheque that is returned unpaid takes place in this clearing. The aggregate of all items unpaid is debited to the original presenting bank and credited to the drawee bank. The same process is mirrored in the inter-branch settlement at the service branch of a bank. The credit given to the payee on account of the cheque is reversed.

181

Inter-branch clearing

Cheques presented by customers drawn on different branches of the same bank need not be sent to the clearing house as the transfer of funds is internal to the bank. The service branch usually acts as a settlement branch for the branches and the instruments are sent to the drawee branches while the inter-branch accounts are credited or debited internally

183

Notational Money While notes are considerably more convenient than gold coins, they are still difficult to exchange in large amounts, and transport or store securely. Currently, most money consists not of pieces of paper currency, but rather of notations in the ledgers of depository institutions such as banks. We refer to this as notational money to distinguish it from token money or currency. Exchanges based on notational money require the debiting of one party's account and the crediting of another party's account.

184

Today, the amount of money which exists solely in the records of depository institutions vastly exceeds the value of currency in circulation A variety of instruments are used to instruct a bank to transfer notational money between accounts; the most common is a check. A complex system involving the Federal Reserve as a clearinghouse supports check clearing when accounts are held at different banks. Institutions accepting demand deposits are required by law to be prepared to convert these notational deposits into currency on demand, thus providing convertibility between demand deposits and currency.

185

In the last several decades, instructions to transfer notational money between accounts are increasingly sent electronically: wire transfers, ATM transactions, or more generally, Electronic Funds Transfer. Notational and token currency are boundary conditions. For example, cashiers checks are notational money, but they share some of the properties of token money. There are also interfaces between the two: ATM machines and bank tellers exchange notational currency for token currency.

186

Cash: Physical Token Money

Checks: Physical Transfers of Notational Money Credit and Debit Cards: Electronic Transfers of Notational Currency Digicash: Electronic Token Money

187

Payment methods Cash EFT ATMs

Plastic money – Debit cards, credit cards & smart cards ECS – credit and debit clearing

188

Electronic Cash (Ecash)

An anonymous electronic cash system; equivalent to "cash" or "printed bank notes" except that it is transferred through networks with bits of information, in essence it is just another representation of monetary value; anonymity is preserved through public key cryptography, digital signatures, and blind signatures.

189

Electronic Cash Payment Systems

A short list of providers: Pay Pal - A U.S.-based system that allows individuals in the United States to send money to each other via . First-E - A European, Internet-only bank. Mondex - Electronic cash that is made available via "smart card." eCash (formerly Digi Cash) - One of the early developers of electronic payment systems.

- One of the early developers of electronic payment systems.")

190

How it is used: Ecash is used over the Internet, , or personal computer to other workstations in the form of secured payments of "cash" that is virtually untraceable to the user. It is backed by real currency from real banks. The way ecash works is similar to that of electronic fund transfers done between banks. The user first must have an ecash software program and an ecash bank account from which ecash can be withdrawn or deposited. The user withdraws the ecash from the account onto her computer and spends it in the Internet without being traced or having personal information available to other parties that are involved in the process. The recipients of the ecash send the money to their bank account as with depositing "real" cash.

191

Example- What is Mondex®?

Mondex, part of the MasterCard Worldwide suite of smart card products, enables cardholders to carry, store and spend cash value using a payment card. It is faster than handling conventional currency, and in many cases safer. It behaves exactly like cash, offering immediate transfer of value while requiring no signature, PIN or transaction authorization. The unique Mondex platform allows its use in multiple channels where cash cannot be used including: Internet Mobile phones Interactive television

192

How it Works Mondex stores value as electronic information on a microchip, rather than as physical notes and coins. Value is exchanged securely from the chip on the card to a chip in a terminal/card reader.

193

Key Benefits Security - Above all, Mondex is a safe way to carry money. A lock function, available on the card with a Mondex device, enables the cardholder to prevent unauthorized access. The code is chosen by the cardholder, and it can be changed at any time. Convenience - Mondex offers cardholders a quick and easy method of payment. There is no need to fumble for change or search for a pen, no need to wait for authorization, no need even to go to a bank or ATM. Flexibility - Mondex cash can be used for purchases of any size, from a chocolate bar to a suit of clothes. Technically, there is no practical limit to the amount of cash which could be held in and transferred from a Mondex card, but there will be limits set within each country consistent with local regulation and market demand. Control - With Mondex, cardholders can only spend what is on their card, so there is no risk of going into debt. The 'purse' keeps an up-to-the-minute record of the amounts and places of expenditure.

194

EFT EFT is short for Electronic Funds Transfer.

An EFT is a method of transferring money from one bank account directly to another account without any paper money actually changing hands. The two accounts do not have to be in the same bank. One of the most common EFT programs that are used is Direct Deposit. This program allows an employee’s paycheck to be directly deposited into their bank account.

195

However, EFT is more than simply direct deposit

However, EFT is more than simply direct deposit. EFT refers to any direct transfer of funds that are initiated through any terminal, such as credit card, ATM, Fed wire, and point of sale (POS) transactions. It is used for both credit transfers, such as a payroll payment, and for debit transfers, such as a mortgage or credit card payment.

transactions. It is used for both credit transfers, such as a payroll payment, and for debit transfers, such as a mortgage or credit card payment.")

196

ATM Applications of ATM

197

Plastic money Plastic money are the alternative to the cash or the standard 'money'. Plastic money is used to refer to the credit cards or the debit cards that we use to make purchases in our everyday life. Be it credit cards, debit cards, add-on cards, charge cards, co-branded cards, affinity cards or Diners Club cards. More and more Indians are using them as a convenient mode of payment.

198

What is a credit card? A credit card is plastic money that is used to pay for products and services at over 20 million locations around the world. All you need to do is produce the card and sign a charge slip to pay for your purchases. The institution which issues the card makes the payment to the outlet on your behalf; you will pay this 'loan' back to the institution at a later date.

199

What is a debit card? Debit cards are substitutes for cash or check payments, much the same way that credit cards are. However, banks only issue them to you if you hold an account with them. When a debit card is used to make a payment, the total amount charged is instantly reduced from your bank balance.

200

What is a charge card? A charge card carries all the features of credit cards. However, after using a charge card you will have to pay off the entire amount billed, by the due date. If you fail to do so, you are likely to be considered a defaulter and will usually have to pay up a steep late payment charge. When you use a credit card you are not declared a defaulter even if you miss your due date. A 2.95 per cent late payment fees (this differs from one bank to another) is levied in your next billing statement.

is levied in your next billing statement.")

201

What is an Amex card? Amex stands for American Express and is one of the well-known charge cards. This card has its own merchant establishment tie-ups and does not depend on the network of MasterCard or Visa. This card is typically meant for high-income group categories and companies and may not be acceptable at many outlets. There are a wide variety of special privileges offered to Amex cardholders.

202

What are MasterCard and Visa?

MasterCard and Visa are global non-profit organizations dedicated to promote the growth of the card business across the world. They have built a vast network of merchant establishments so that customers world-wide may use their respective credit cards to make various purchases.

203

What is a smart card? A smart card contains an electronic chip which is used to store cash. This is most useful when you have to pay for small purchases, for example bus fares and coffee. No identification, signature or payment authorization is required for using this card. The exact amount of purchase is deducted from the smart card during payment and is collected by smart card reading machines. No change is given. Currently this product is available only in very developed countries like the United States and is being used only sporadically in India.

204

What is the Diners Club card?

Diners Club is a branded charge card. There are a wide variety of special privileges offered to the Diners Club cardholder. For instance, as a cardholder you can set your own spending limit. Besides, the card has its own merchant establishment tie-ups and does not depend on the network of MasterCard or Visa. However, since this card is typically meant for high-income group categories, it may not be acceptable at many outlets. It would be a good idea to check whether a member establishment does accept the card or not in advance.

205

What is a co-branded card?

Co-branded cards are credit cards issued by card companies that have tied up with a popular brand for the purpose of offering certain exclusive benefits to the consumer. For example, the Citi-Times card gives you all the benefits of a Citibank credit card along with a special discount on Times Music cassettes, free entry to Times Music events, etc.

206

What is an affinity card?

The card issuer ties up with popular organizations/ institutions which are often non-profit organizations (Citi-WWF card or the Stanchart-Cricket cards) to offer an affinity card. When the card is used, a certain percentage is contributed to the organization /institution by the card issuer.

to offer an affinity card. When the card is used, a certain percentage is contributed to the organization /institution by the card issuer.")

207

What is an add-on card? An add-on card allows you to apply for an additional credit card within the overall credit limit. You can apply for this card in the name of family members like your father/ mother/ spouse/ brother/ sister/ all children above 18 years of age. Your billing statement would reflect the details of purchases made using the add-on card. You are liable to make good all the payments for the purchases made using the add-on card's).

.")

208

What is Electronic Clearing Service (ECS)?

It is a mode of electronic funds transfer from one bank account to another bank account using the services of a Clearing House. This is normally for bulk transfers from one account to many accounts or vice versa. This can be used both for making payments like distribution of dividend, interest, salary, pension, etc. by institutions or for collection of amounts for purposes such as payments to utility companies like telephone, electricity, or charges such as house tax, water tax, etc or for loan installments of financial institutions/banks or regular investments of persons.

209

Types of ECS ECS (Credit) is used for affording credit to a large number of beneficiaries by raising a single debit to an account, such as dividend, interest or salary payment. ECS (Debit) is used for raising debits to a number of accounts of consumers/ account holders for crediting a particular institution

is used for affording credit to a large number of beneficiaries by raising a single debit to an account, such as dividend, interest or salary payment. ECS (Debit) is used for raising debits to a number of accounts of consumers/ account holders for crediting a particular institution.")

210

Working of ECS Credit System

211

Who can initiate an ECS (Credit) transaction?

ECS payments can be initiated by any institution (called ECS user) who have to make bulk or repetitive payments to a number of beneficiaries. They can initiate the transactions after registering themselves with an approved clearing house. ECS users have also to obtain the consent as also the account particulars of the beneficiary for participating the ECS clearings.

who have to make bulk or repetitive payments to a number of beneficiaries. They can initiate the transactions after registering themselves with an approved clearing house. ECS users have also to obtain the consent as also the account particulars of the beneficiary for participating the ECS clearings.")

212

The ECS user's bank is called as the sponsor bank under the scheme and the ECS beneficiary account holder is called the destination account holder. The destination account holder's bank or the beneficiary's bank is called the destination bank.

213

How does the ECS Credit system work?

The ECS users intending to effect payments have to submit the data in a specified format to one of the approved clearing houses. The list of the approved clearing houses or the list of centre where the ECS facility has been provided is available at The clearing house would debit the account of the ECS user through the account of the sponsor bank on the appointed day and credit the accounts of the recipient banks, for affording onward credit to the accounts of the ultimate beneficiaries.

214

What are the advantages to the ultimate beneficiary?

The end beneficiary need not make frequent visits to his bank for depositing the physical paper instruments. He need not apprehend loss of instrument and fraudulent encashment. The delay in realization of proceeds after receipt of paper instrument.

215

How does the scheme benefit the ECS user-like corporate bodies/ institutions?

The ECS user saves on administrative machinery for printing, dispatch and reconciliation. Avoids chances of loss of instruments in postal transit. Avoids chances of frauds due to fraudulent access to the paper instruments and encashment. Ability to make payment and ensure that the beneficiaries' account gets credited on a designated date.

216

What are the advantages to the banks?

Banks handling ECS get freed of paper handling. Paper handling also creates lot of pressure on banks as they have to encode the instruments, present them in clearing, monitor their return and follow up with the concerned bank and customers. In ECS banks simply get the payment particulars relating to their customers. All they need to do is to match the account particulars like name, a/c number and credit the proceeds Wherever the details do not match, they have to return it back, as per the procedure

217

How can the customer track-down these payments?

Banks have been advised to ensure that the pass-books/statements given to the customers reflect the particulars of the transaction provided by the ECS users. Customers can match these entries with the advice received by them from the payment institution

218

What is ECS (Debit) scheme?

It is a scheme under which an account holder with a bank can authorize an ECS user to recover an amount at a prescribed frequency by raising a debit in his account. The ECS user has to collect an authorization which is called ECS mandate for raising such debits. These mandates have to be endorsed by the bank branch maintaining the account

219

How does the scheme work?

Any ECS user desirous of participating in the scheme has to register with an approved clearing house. The list of approved clearing houses is available at RBI web-site He should also collect the mandate forms from the participating destination account holders, with bank's acknowledgement. A copy of the mandate should be available with the drawee bank.

220

The ECS user has to submit the data in specified form through the sponsor bank to the clearing house. The clearing house would pass on the debit to the destination account holder through the clearing system and credit the sponsor bank's account for onward crediting the ECS user. All the unprocessed debits have to be returned to the sponsor bank within the time frame specified. Banks will treat the electronic instructions received through the clearing system on par with the physical cheques.

221

What are the advantages to the ultimate beneficiary?

Trouble free- Eliminates the need to go to the collection centre/banks by the customers and no need to stand in long ‘Q’s for payment Peace of mind- Customers also need not track down payments by last dates. The debits would be monitored by the ECS users.

222

How does the scheme benefit the ECS user-like corporate bodies/ institutions?

The ECS user saves on administrative machinery for collecting the cheques, monitoring their realization and reconciliation Better cash management. Avoids chances of frauds due to fraudulent access to the paper instruments and encashment. realize the payments on a single date instead of fractured receipt of payments.

223

What are the advantages to the banks?

Banks handling ECS get freed of paper handling. Paper handling also creates lot of pressure on banks as they have to encode the instruments, present them in clearing, monitor their return and follow up with the concerned bank and customers. In ECS banks simply get the mandate particulars relating to their customers. All they need to do is to match the account particulars like name, a/c number and debit the accounts. Wherever the details do not match, they have to return it back, as per the procedure.

224

Which are the institutions eligible to participate in the ECS Debit scheme?

Utility service providers such as telephone companies, electricity supplying companies, electricity boards, credit card collections, collection of loan installments by banks and financial institutions, and investment schemes of Mutual funds, etc.

225

Online & call centre banking

To cut cost Attract new customers Unprofitable Marketing personally Call centre Classification Voice call centre Web based Regional Global call centre Benefits Customer base Economical means Focused attention Round the clock

226

Para banking Coffee pub banking E lobby Mobile vans Narrow banking

227

Financial networks in India

RBI – INFINET SWADHAN, the shared payment network service BANKNET SWIFT

228

RTGS Concepts and Working of the RTGS System