Download presentation

Presentation is loading. Please wait.

1

Functional Ito Calculus and PDE for Path-Dependent Options Bruno Dupire Bloomberg L.P. PDE and Mathematical Finance KTH, Stockholm, August 19, 2009

2

Outline 1)Functional Ito Calculus Functional Ito formula Functional Feynman-Kac PDE for path dependent options 2)Volatility Hedge Local Volatility Model Volatility expansion Vega decomposition Robust hedge with Vanillas Examples

Functional Ito Calculus Functional Ito formula Functional Feynman-Kac PDE for path dependent options 2)Volatility Hedge Local Volatility Model Volatility expansion Vega decomposition Robust hedge with Vanillas Examples")

3

1) Functional Ito Calculus

Functional Ito Calculus")

4

Why?

5

Review of Ito Calculus 1D nD infiniteD Malliavin Calculus Functional Ito Calculus current value possible evolutions

6

Functionals of running paths 0 T 12.87 6.32 6.34

7

Examples of Functionals

8

Derivatives

9

Examples

10

Topology and Continuity ts X Y

11

Functional Ito Formula

12

Fragment of proof

13

Functional Feynman-Kac Formula

14

Delta Hedge/Clark-Ocone

15

P&L Break-even points Option Value Delta hedge P&L of a delta hedged Vanilla

16

Functional PDE for Exotics

17

Classical PDE for Asian

18

Better Asian PDE

19

2) Robust Volatility Hedge

Robust Volatility Hedge")

20

Local Volatility Model Simplest model to fit a full surface Forward volatilities that can be locked

21

Summary of LVM Simplest model that fits vanillas In Europe, second most used model (after Black- Scholes) in Equity Derivatives Local volatilities: fwd vols that can be locked by a vanilla PF Stoch vol model calibrated If no jumps, deterministic implied vols => LVM

in Equity Derivatives Local volatilities: fwd vols that can be locked by a vanilla PF Stoch vol model calibrated If no jumps, deterministic implied vols => LVM")

22

S&P500 implied and local vols

23

S&P 500 Fit Cumulative variance as a function of strike. One curve per maturity. Dotted line: Heston, Red line: Heston + residuals, bubbles: market RMS in bps BS: 305 Heston: 47 H+residuals: 7

24

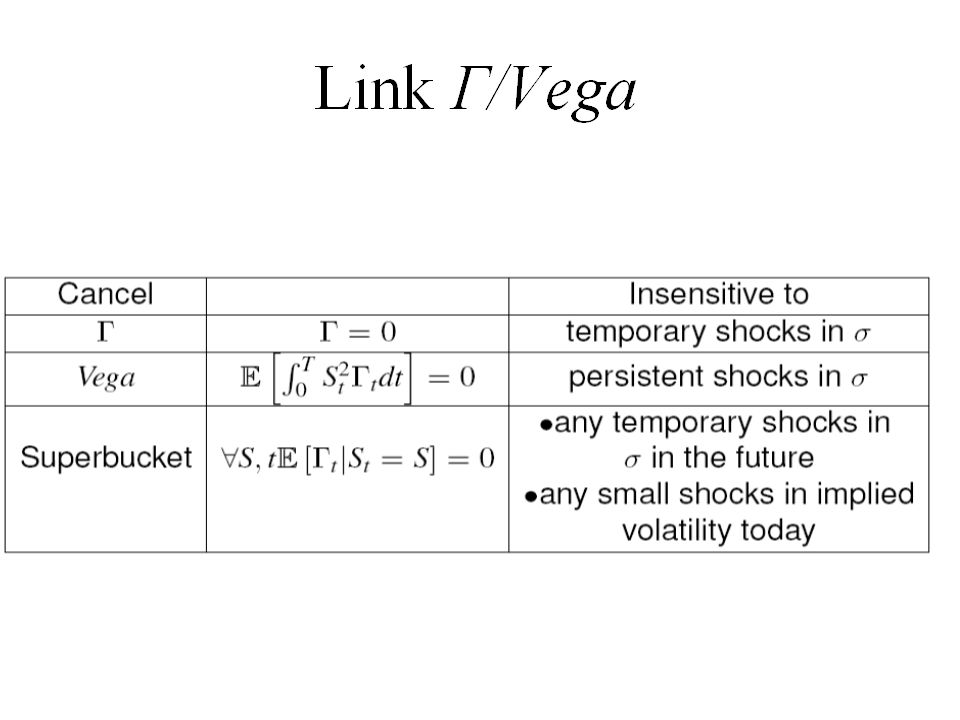

Hedge within/outside LVM 1 Brownian driver => complete model Within the model, perfect replication by Delta hedge Hedge outside of (or against) the model: hedge against volatility perturbations Leads to a decomposition of Vega across strikes and maturities

the model: hedge against volatility perturbations Leads to a decomposition of Vega across strikes and maturities")

25

Implied and Local Volatility Bumps implied to local volatility

26

P&L from Delta hedging

27

Model Impact

28

Comparing calibrated models

29

Volatility Expansion in LVM

30

Frechet Derivative in LVM

31

One Touch Option - Price Black-Scholes model S 0 =100, H=110, σ=0.25, T=0.25

32

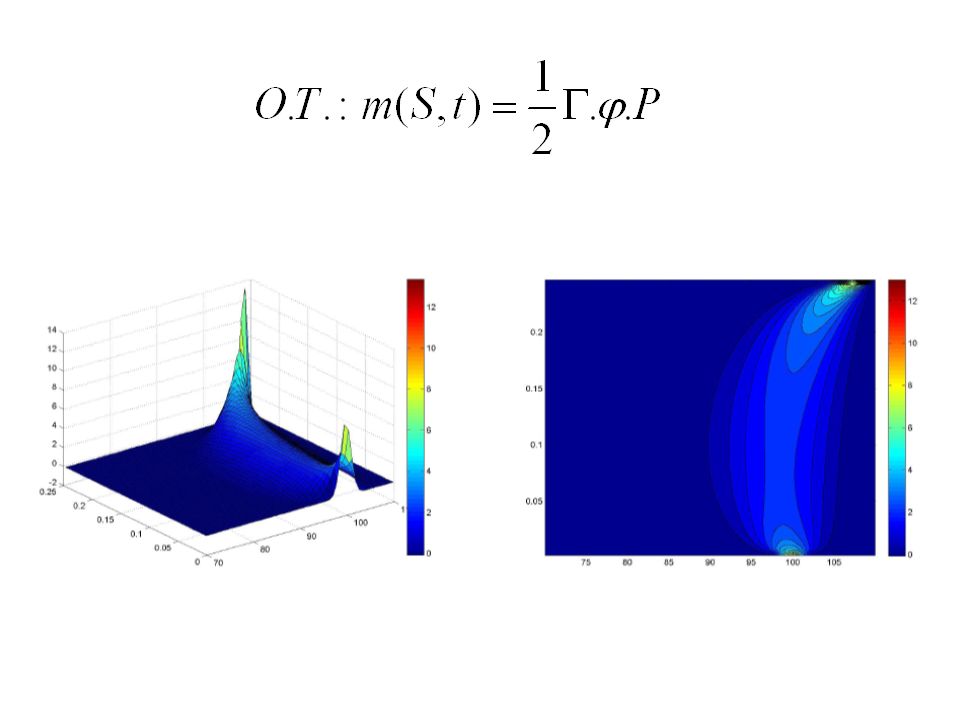

One Touch Option - Γ

34

Up-Out Call - Price Black-Scholes model S 0 =100, H=110, K=90, σ=0.25, T=0.25

35

Up-Out Call - Γ

37

Black-Scholes/LVM comparison

38

Vanilla hedging portfolio I

39

Vanilla hedging portfolios II

40

Example : Asian option K T K T

41

Asian Option Superbuckets K T K T

43

Conclusion Ito calculus can be extended to functionals of price paths Local volatilities are forward values that can be locked LVM crudely states these volatilities will be realised It is possible to hedge against this assumption It leads to a strike/maturity decomposition of the volatility risk of the full portfolio

Similar presentations

Formulation Donald C. Williams Doctoral Candidate Department of Computational and Applied.>")