Download presentation

Presentation is loading. Please wait.

2

Life Cycle Model To illustrate the LCM in a world without uncertainty and a zero interest rate, consider a 25-year-old who will work for 40 years and be retired for 10 years. He earns $25,000 each year so his total human capital or wealth (the present value of his lifetime earnings from work) will be $1,000,000

will be $1,000,000.")

3

Life Cycle Model The $1,000,000 of human capital has to be consumed over the individual’s 50 years of remaining life. Since he values smooth consumption over his lifecycle, he can spend $20,000 a year and die with all his assets exhausted.

4

Life Cycle Model To achieve this spending pattern, he saves $5000 a year whilst in work. At retirement he will have accumulated a pension fund of $200,000, which can be drawn down at the rate of $20,000 a year.

5

Life Cycle Model In the above example, the individual had no inherited wealth and leaves no bequests. Suppose instead he inherits $250,000 in financial assets. His total wealth is the sum of his human and financial wealth, namely $1,250,000. He will now be able to spend $25,000 a year and die with zero assets. Consumption=f(Wealth derived from income or sale of assets)

.")

6

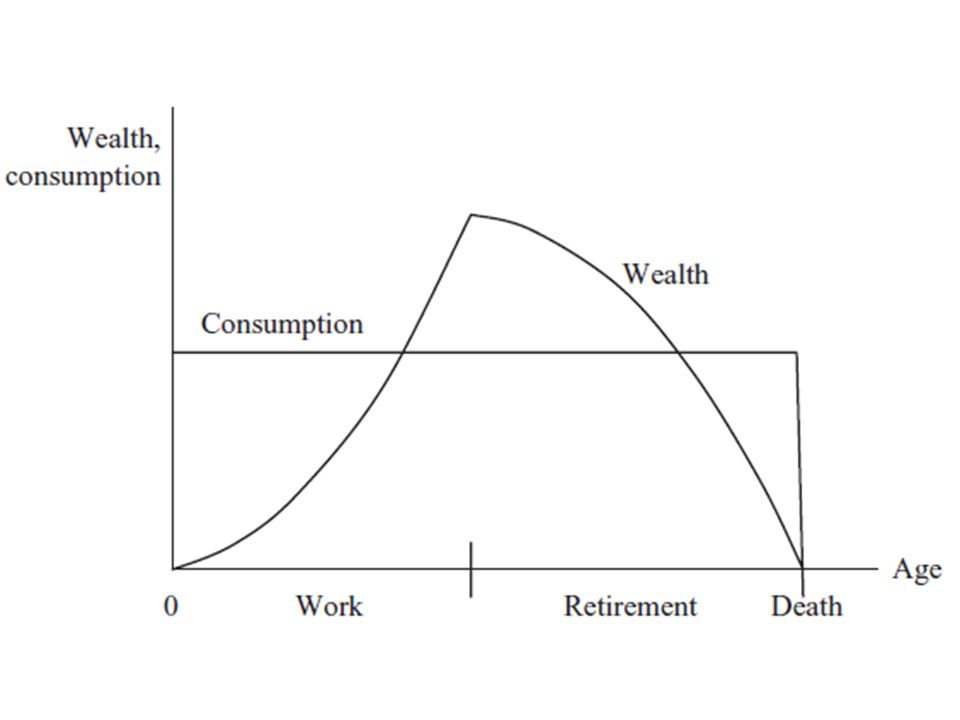

Life Cycle Model The LCM can be extended to allow for borrowing as well as lending. This can be done by dividing the lifecycle into three stages: a period of youth, a period of middle age and a period of old age. The first period of youth begins when the individual first gets a job once full-time education has ended.

7

Life Cycle Model The individual might want to buy physical assets such as a home and start a family. The costs of doing this will typically exceed the individual’s income and so he has to borrow from the future to finance the excess of consumption expenditure over income.

8

Life Cycle Model During mid-life, once these high expenditure levels have tailed off and the individual’s income exceeds consumption, he can pay off his past borrowings and begin to save for retirement by accumulating a fund of financial and physical assets.

9

Life Cycle Model During the final stage of life, the retirement stage, the individual spends more than his income, by dissaving or drawing down the financial assets accumulated during mid- life until death.

10

Life Cycle Model Consumption expenditure might actually be lower than in the pre-retirement stage (travel costs to work are no longer incurred, for example), but income is usually significantly lower than in the pre- retirement stage (pensions are lower than final salary for most people).

, but income is usually significantly lower than in the pre- retirement stage (pensions are lower than final salary for most people).")

12

U(C) = ln(C)

= ln(C)")

13

Life Cycle Model The rate of time preference (sometimes called the personal or subjective discount rate or the degree of impatience) measures the individual’s preference between current consumption and future consumption. Individuals with a high rate of time preference ‘live for today’ rather than ‘plan for the future’.

14

Life Cycle Model They discount the future very heavily: from equation (2.1) future utility such asU(C t+1 ) decreases (is discounted) relative to current utility U(C t ), the higher the value of ρ. The rate of time preference can be interpreted as the personal interest rate of the individual.

15

Life Cycle Model The market interest rate, r, is the weighted average of the rates of time preference of all the individuals in the economy (or society as a whole), where the weights will reflect the distribution of wealth in the economy (i.e., the different values of At for different members of society). Individuals with above average rates of time preference (ρ > r ) will tend to borrow funds (at the current market interest rate r ) from individuals with below average rates of time preference (ρ < r ) to increase further their current consumption, recognising that they must at some future stage repay these borrowings in order to avoid violating their lifetime budget constraint (2.2).

will tend to borrow funds (at the current market interest rate r ) from individuals with below average rates of time preference (ρ < r ) to increase further their current consumption, recognising that they must at some future stage repay these borrowings in order to avoid violating their lifetime budget constraint (2.2)..")

16

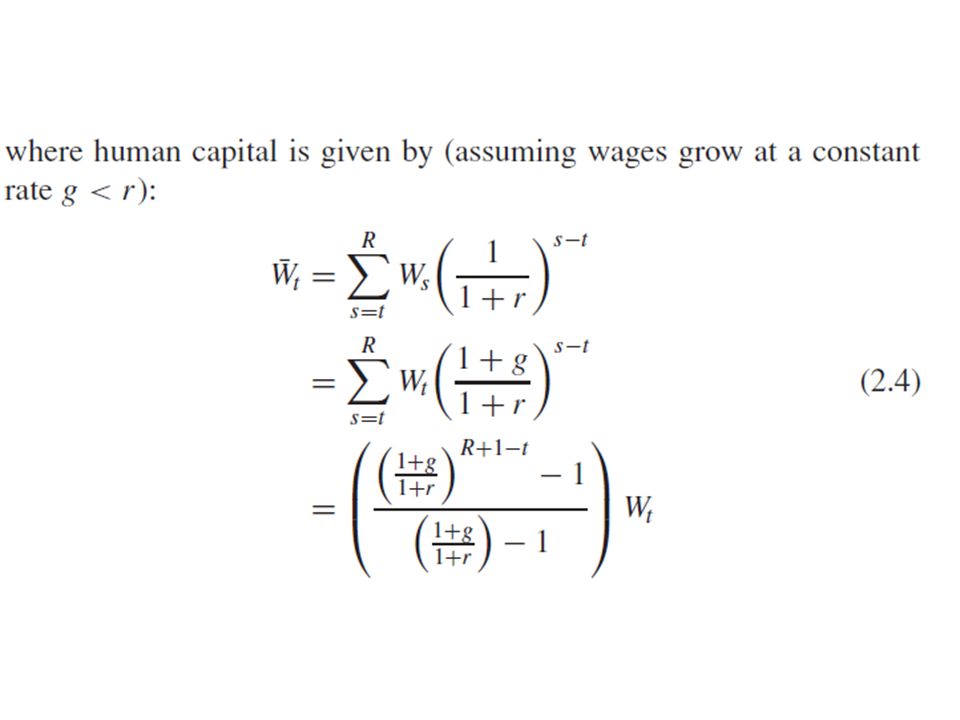

Life Cycle Model The principal feature of the LCM is that current consumption,Ct, depends on the value of lifetime wealth, which is the sum of financial wealth (i.e., non-human wealth, At ) and human wealth or capital (the present value of lifetime labour income, ¯Wt ). If the lifetime budget constraint (2.2) is satisfied, then the above optimisation problem leads to the following utility-maximising LCM current consumption (Ct ) function if the utility function is logarithmic (i.e., U(Ct ) = ln(Ct )): Ct = b(At + ¯Wt )

is satisfied, then the above optimisation problem leads to the following utility-maximising LCM current consumption (Ct ) function if the utility function is logarithmic (i.e., U(Ct ) = ln(Ct )): Ct = b(At + ¯Wt ).")

Similar presentations

>")

Analyze the various sources of borrowing available to a client and.>")