Download presentation

Presentation is loading. Please wait.

1

Chapter III Demand, Supply, and Equilibrium The Single Market J.F. O’Connor 1/19/05

2

Outline Self-sufficiency versus interdependence The economic problem and alternative ways of solving it Monetary economy versus barter Demand and factors affecting demand Supply and factors affecting supply Equilibrium in the market

3

Social Efficiency of the market equilibrium How does the equilibrium change when the factors affecting demand and supply change? Government intervention in the market: price floor, price ceiling, tax and subsidy.

4

Two Contrasting Economies Self-sufficiency (Subsistence): Each unit, individual or family, produces the goods and services that it wants. Each unit consumes what it produces. Kentucky 1770. Interdependent: Each unit produces little if any of the goods and services that it wants. Each unit consumes little if any of the services that it produces. Kentucky 2002

5

The Economic Problem What goods and services will be produced and who will produce them? (Choice) How will the goods and services be produced? ( Organization) For whom will the goods and services be produced? (Distribution) Who makes economic decisions and by what process? (System)

How will the goods and services be produced. ( Organization) For whom will the goods and services be produced. (Distribution) Who makes economic decisions and by what process. (System).")

6

Solving the Economic Problem Not very complicated for the self-sufficient units in a subsistence economy The modern economy, with its specialization, needs a mechanism to: a) bring potential buyers and sellers of each product together b) coordinate the plans of the specialized individuals and groups A system of markets is one such mechanism

bring potential buyers and sellers of each product together b) coordinate the plans of the specialized individuals and groups A system of markets is one such mechanism")

7

A Modern Market Barter economy: goods are exchanged for other goods. Monetary economy: goods are exchanged for money. We have talked about the value of oranges in terms of apples. We could also value all the other goods in the economy in terms of apples. Apples would then be the unit of account. However, we still have a problem in that we need a medium of exchange and apples are not too convenient. So we introduce money.

8

The Role of Money The unit of account The medium of exchange A store of value The importance of money in the market process is that it allows one to sell what one has without having to find a buyer who is selling what you want to buy.

9

Two Kinds Of Money Currency Demand deposits - what is in your checking account. Be careful to distinguish income, wealth, and money.

10

A Single Market One good, say, ice cream, and two kinds of people: –Buyers –Sellers Demand represents the intentions of buyers. Supply represents the intentions of sellers.

11

Demand Demand gives the relationship between the quantity of the good that buyers are willing and able to purchase and the price of the good, while other factors affecting quantity demanded are held constant. We can represent demand in a table, a graph, or an equation. Accordingly, we talk about a demand schedule, curve, or function.

12

Factors Affecting Demand Prices of other goods Income of buyers Preferences or tastes of buyers Number of buyers Expectations about prices Advertising ?

13

Demand Schedules Two buyers, Cath and Nick

14

Demand Curve The market demand is the sum of the individual demands

15

Supply Supply is the relationship between the quantity of the good that sellers are willing and able to supply and the price of the good, while other factors affecting quantity supplied are constant. We can represent supply in a table, a graph, or an equation. Accordingly, we talk about a supply schedule, curve, or function.

16

Factors Affecting Supply Input prices Technology of production Number of sellers Expectations

17

Supply Schedules Two sellers, Ben and Jerry

18

Supply Curve

19

Market Equilibrium Balancing Demand and Supply. The equilibrium price is the price at which the quantity demanded is equal to the quantity supplied. If you have excess demand or excess supply the market is not in equilibrium. Why? Excess demand (shortage) increases price; excess supply (surplus) depresses price.

increases price; excess supply (surplus) depresses price..")

20

Market Demand and Supply

21

Equilibrium price $2 quantity 7 units Equilibrium price $2 quantity 7 units Supply Demand Market Equilibrium

22

Markets and Social Welfare Social optimal quantity of a good –The quantity that results in the maximum possible economic surplus. –The socially optimal quantity will occur where the marginal cost equals the marginal benefit. Economic efficiency –Occurs when all goods and services are produced and consumed at their respective socially optimal levels.

23

Markets and Efficiency Efficiency Principle: –Efficiency is an important social goal. –Everyone can have a larger slice of a larger pie. Equilibrium Principle: –A market in equilibrium leaves no unexploited opportunities for individuals. –No “cash on the table” remains. –All opportunities for profit have been exploited. Efficiency occurs when: –the market-demand curve captures all the marginal benefits of the good. –the market-supply curve captures all the marginal costs of the good.

24

Terminology If the good’s price changes, you have a: –“change in quantity demanded” A movement along the demand curve –“change in quantity supplied” A movement along the supply curve If something else changes, you have a: –“change in demand” A shift of the entire demand curve –change in supply” A shift of the entire supply curve

25

Fig. 4.9 An Increase in the Quantity Demanded Versus an Increase in Demand

26

Increase in Demand Means the demand curve shifts right Caused by factors other than the price of the good: –For a normal good, an increase in income –An increase in the price of a substitute or a decrease in the price of a complement –An increase in the number of buyers –Change in preferences

27

Increase in Demand

28

Note that demand increases by 6 units but the new equilibrium quantity is only 3 units greater than old. Why? Note that the increase in demand results in a movement up the supply curve. You should analyze a decrease in demand.

29

Increase in Supply Sellers are willing to supply more units of the good at each price. Major Causes: –decrease in input prices –improvement in technology of production –increase in the number of sellers

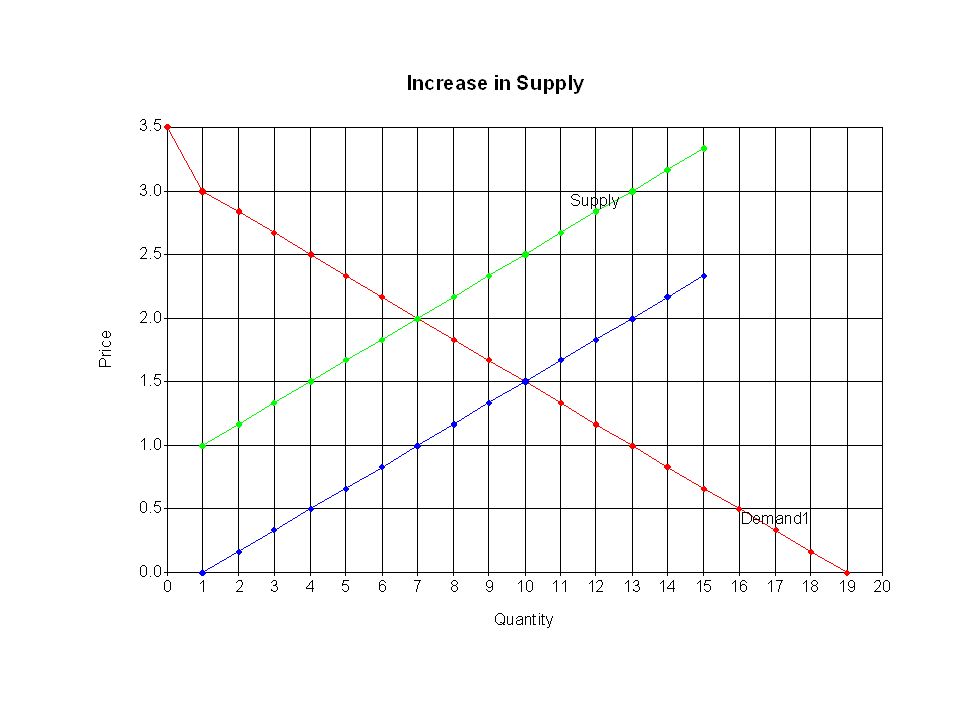

31

Increase in Supply Increase in supply results in an increase in the equilibrium quantity and a decrease in price. Note that the increase in supply results in a movement down the demand curve. You should analyze a decrease in supply

32

Free Markets and Equilibrium Free markets have an automatic tendency to eliminate excess supply and excess demand. –Surplus leads producers to decrease the price –Shortage leads producers to increase the price

33

Reasons for Government Activity Efficiency Concerns: Imperfect Competition Externalities Public goods Equity considerations: Distribution of outcomes Distribution of endowments

34

Legislation and Markets Market equilibrium does not mean that everyone has what they want. –E.G. a poor person may not be able to afford the item at the equilibrium price. Legislators protect consumers by using: –price ceilings A maximum allowable price specified by law Price signal is too low, so consumers want too much e.g. rent controls, limits on the price of gasoline Result in shortages

35

Legislation and Markets Legislators protect producers by using: –price floors A minimum allowable price specified by law For example, price supports, minimum wage Price signal is too high, so consumers don’t want as much. Result in surpluses

36

Fig. 4.6 An Unregulated Housing Market

37

Fig. 4.7 Rent Controls

38

Economists and the Poor Economists realize there are more effective ways of helping the poor than violating the free market system. Using rent controls or price ceilings results in inefficiency for everyone. Using a direct income transfer to the poor is a more efficient way to help.

39

Fig. 4.8 Price Controls in the Hamburger Market

40

and

41

Shifts in Supply Favorable changes to the producer shift supply curve rightward. –lower equilibrium price –higher equilibrium quantity Unfavorable changes to the producer shift supply leftward. –higher equilibrium price –lower equilibrium quantity

42

Fig. 4.10 The Effect on the Skateboard Market of an Increase in the Price of Fiberglass

43

Shifts in Supply Changes in the Cost of Production Changes in Technology Changes in Weather Changes in Expectations

44

Fig. 4.11 The Effect on the Market for New Houses of a Decline in Carpenters’ Wage Rates

45

Fig. 4.12 The Effect of Technical Change on the Market for Manuscript Revisions

46

Shifts in Demand Complements Substitutes Income Preferences Demand curve shifts rightward –higher equilibrium price –higher equilibrium quantity Demand curve shifts leftward –lower equilibrium price –lower equilibrium quantity

47

Fig. 4.13 The Effect on the Market for Tennis Balls of a Decline in Court Rental Fees

48

Complements Goods that are more valuable when used in combination--e.g. tennis balls and tennis courts. Two goods are complements in consumption if an increase in the price of one causes a leftward shift in the demand curve for the other.

49

Substitutes Goods that replace each other--e.g. email messages and overnight letters. Two goods are substitutes in consumption if an increase in the price of one causes a rightward shift in the demand curve for the other.

50

Fig. 4.14 Effect on the Market for Overnight Letter Delivery of a Decline in the Price of Internet Access

51

Income Normal good –One whose demand curve shifts right when the incomes of buyers increase. Inferior good –One whose demand curves shifts left when the incomes of buyers increase.

52

Fig. 4.15 The Effect of a Federal Pay Raise on the Rent for Conveniently Located Apartments

53

Simultaneous Shifts If, at the same time, –Demand decreases and Supply increases Demand shifts left –Lower price, lower quantity Supply shifts right –Lower price, higher quantity We can predict that price will fall But, what happens to quantity? –We must know the magnitude of the shifts

54

Fig. 4.16 Four Rules Governing the Effects of Supply and Demand Shifts

55

Fig. 4.17 The Effects of Simultaneous Shifts in Supply and Demand

56

Fig. 4.18 Seasonal Variation in the Air Travel and Corn Markets

57

Economic System An economic system is a set of arrangements for solving the economic problem. Important Features: –Ownership of resources –Procedure for making decisions –Objectives of decision makers

58

Alternative Systems Pure Capitalism Private ownership Decentralized decision making Cooperative System Communal ownership Democratic decision making Communal Command Communal ownership Centralized decision making Mixed Systems Democratic capitalism Democratic socialism

59

Mixed Open Economy Consumer sovereignty Substantial private ownership and private enterprise production. Substantial use of markets to guide resource allocation. Substantial government activity Significant international trade

Similar presentations

An Introduction to Supply and Demand What is a market? Where do prices come from? What happens if prices are set “too.>")