Download presentation

Presentation is loading. Please wait.

1

Jerry Rhinehart, CIC, CLU, ChFC, RHU Panama City, FL Estate Planning Techniques: Gifts, Trusts and Life Insurance

2

To understand the importance of Estate Planning and the various options available. To be familiar with the usual misconceptions, or “Myths”, of Estate Planning. To know the law and advantages of gifting. Learning Objectives 1

3

To understand the application, benefits and use of various trusts in Estate Planning. Living Trust Charitable Remainder Trust Testamentary Trust Learning Objectives 1

4

Please note the DISCLAIMER 2

5

2

6

The impact of the Federal Estate Tax 3 The Judge said...

7

High Federal Estate Tax (FET) The Cost of Doing Nothing vs. The Cost/Time/Aggravation of Doing it Right! 3

8

Know This Regarding FET... $5,000,000 (2011 & 2012) 35% Payable in 9 Months Payable in Cash!

35% Payable in 9 Months Payable in Cash!")

9

High Federal Estate Tax (FET) The Cost of Doing Nothing vs. The Cost/Time/Aggravation of Doing it Right! 3 High Probate Cost Delays in Settlement

10

The Importance of Estate Planning 4 Some “famous people” have done a good job of estate planning and some...

11

4 Estates of Well-Known People

12

4 Elvis Aaron Presley — 1936-1977 Would you have “wasted your time” calling on Elvis for his estate planning? Did Elvis (or his manager) do a “good job” of estate planning? 73% erosion of his “stuff”. Seven years delay in settlement.

do a good job of estate planning. 73% erosion of his stuff . Seven years delay in settlement..")

14

Dan Duncan (Houston, TX) – Died March, 2010. He was listed as #74 on Forbes Wealthiest (@$9 Billion). Married, 4 adult kids. Supposedly had used various Trusts and Charitable techniques to avoid greater than $2 Billion in taxes.

. Married, 4 adult kids. Supposedly had used various Trusts and Charitable techniques to avoid greater than $2 Billion in taxes..")

15

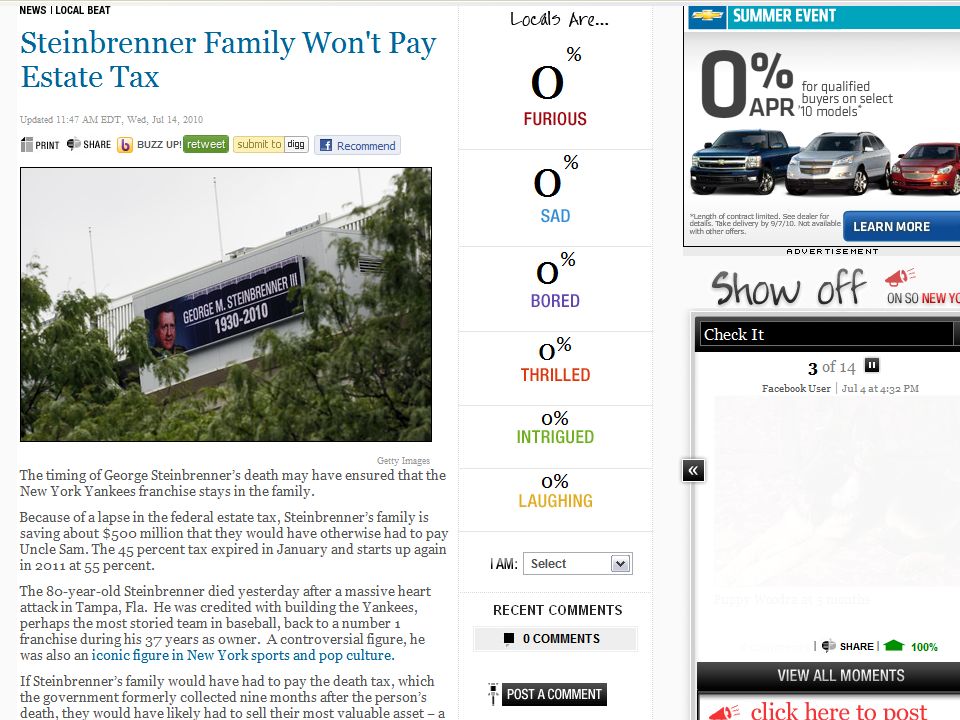

George Steinbrenner (“The Boss”) – World Series Win - 2000

– World Series Win")

19

High Federal Estate Tax (FET) The Cost of Doing Nothing vs. The Cost/Time/Aggravation of Doing it Right! 3 High Probate Cost Delays in Settlement Low (or no) FET Reduced (or no) Probate Prompt Settlement

FET Reduced (or no) Probate Prompt Settlement.")

20

Possible liquidity problems for loved ones! 3 Ample cash flow to pay taxes, debts, and provide an income for the life of your spouse! The Cost of Doing Nothing vs. The Cost/Time/Aggravation of Doing it Right!

21

Tough decisions to be made by loved-ones — probably not trained for such a task... 3 Pre-determined decisions that treat loved-ones, benefi- ciaries, charities, employees, etc., based exactly on your wishes! The Cost of Doing Nothing vs. The Cost/Time/Aggravation of Doing it Right!

22

Basic Truths in Estate Planning You cannot die without a will!

23

Basic Truths in Estate Planning Just what is a will? What are the advantages of a will? How does a will work? Is it the only “legal document” most people need? 6

24

Basic Truths in Estate Planning You cannot die without a will! Everybody has an Estate Plan!

25

5 Estate Planning “Myths” Myths Concerning a Will (or no will)

")

26

Allows me to avoids probate Will save me estate taxes My loved ones will be treated equally I told my kids how to distribute my possessions … My business is very successful … 5

27

5 Estate Planning “Myths” Myths Concerning a Will (or no will) “I’m not rich” (life insurance)

I’m not rich (life insurance) ")

28

“Stuff” For Estate Calculation DescriptionFair Market ValueDebt House1,500,000(200,000) Mutual Funds1,000,000- 0 - Real Estate2,000,000(500,000) Q-Plans1,000,000- 0 - TOTAL5,500,000(700,000) 5,500,000 -700,000 4,800,000

Mutual Funds1,000, Real Estate2,000,000(500,000) Q-Plans1,000, TOTAL5,500,000(700,000) 5,500, ,000 4,800,000")

29

“Stuff” For Estate Calculation Net Estate: 4,800,000 Personal Life Insurance (Owned): 1,000,000 Group Life Insurance 100,000 Travel Accident 100,000 Total Life Insurance 1,200,000

: 1,000,000 Group Life Insurance 100,000 Travel Accident 100,000 Total Life Insurance 1,200,000")

30

“Stuff” For Estate Calculation Non-Life Insurance “Stuff”4,800,000 Life Insurance “Stuff”1,200,000 Total6,000,000 Less Year 2012 “Freebie”-5,000,000 Total Subject to FET 1,000,000 FET Owed (@35%) 350,000

31

5 Estate Planning “Myths” Myths Concerning a Will (or no will) “I’m not rich” (life insurance) “I’ll worry about it later”

I’m not rich (life insurance) I’ll worry about it later ")

32

5 Estate Planning “Myths” Myths Concerning a Will (or no will) “I’m not rich” (life insurance) “I’ll worry about it later” “I don’t have to do anything to get the tax breaks that are available”

I’m not rich (life insurance) I’ll worry about it later I don’t have to do anything to get the tax breaks that are available ")

33

“The sale would give the Robbies cash to pay off an estate tax bill of about $47 million.” U.S. Today - March 24, 1993 7

34

$5,000,000 Exemption (2011 & 2012) 35% FET rate (2011 & 2012 / (per person) Possible 5% probate expense FET due in 9 months (exceptions exist) CASH – The IRS wants it! 7 years – possible delays 7

35

What About a Liquidity Problem? “The Great Garage Sale” “The Dreaded Discount Buyer” 7

36

8

37

$100,000 $300,000 A View of Your “Stuff” - 2012 $4,000,000 $1,000,000 $250,000 $5,650,000 IRS Hose

38

Who Are Your Heirs? Mary - daughter John - son Will - son Will, Jr. - G-son Church University Hospital LOVE Sara (CPA) Barry (atty) OTHER HATE IRS Dreaded Discount Buyer 9

Barry (atty) OTHER HATE IRS Dreaded Discount Buyer 9.")

39

The News... You’re alive You have an Estate Plan Correctable Good News Q-Plans (401k) $1,000,000 2 - Good Deals 2 - Bad Deals Bad News Ugly News 9 Months 35% - 50% Cash Dreaded Discount Buyer 40% (-400K) 600K 10

$1,000, Good Deals 2 - Bad Deals Bad News Ugly News 9 Months 35% - 50% Cash Dreaded Discount Buyer 40% (-400K) 600K 10.")

41

11 Why Give Away Your “Stuff”? Reduce current estate size / tax Enjoyment of the donor Fund life insurance trust Gifts to a charity / individuals Future appreciation to another

42

What if You Can Not Prove Your Cost Basis? The IRS rules state that without proof of basis — then your basis is ZERO! (Thus ALL gain!) 12

12.")

43

You Sell the stock You Give the stock away during your lifetime The stock is Transferred at your death Intel, Inc. Basis - $1,000 FMV - $10,000 12

44

Intel, Inc. Basis - $1,000 FMV - $10,000 You Sell the stock - 10,000 - 1,000 = 9,000 x 15% Capital Gains Tax -- $1,350 Tax

45

Intel, Inc. Basis - $1,000 FMV - $10,000 You Give away the stock (during your life time) 10,000 - 1,000 = 9,000 x 15% Capital Gains Tax -- $1,350 Tax to Seller

10, ,000 = 9,000 x 15% Capital Gains Tax -- $1,350 Tax to Seller.")

46

The stock is Transferred to another person at your death 10,000 - 10,000 (step-up-in basis) = - 0 - No Tax to the Seller Basis - $1,000 FMV - $10,000 Intel, Inc.

= No Tax to the Seller Basis - $1,000 FMV - $10,000 Intel, Inc.")

47

13 An unlimited amount can be given to a college or medicalfacility for the benefit of anyone! Three year rule Excess gifts — $13,000 maximum / “completed gift” (present interest) An unlimited amount can be gifted between husband / wife

An unlimited amount can be gifted between husband / wife.")

48

Parties of a Trust Trustee Grantor Beneficiaries Bank

49

13 Irrevocable Life Insurance Trust (ILIT) Why is this Trust beneficial for a husband and wife that have an Estate Tax problem? How does an ILIT work?

50

Irrevocable Life Insurance Trust in Action GrantorTrust Trust Beneficiaries Crummey Withdrawal Notice Annual Gifts Premium Paid Insurance Company Death Benefit Grantor’s Estate Provides Estate Liquidity Assets Distributed 14

51

What does it do? What does it NOT do? 15

52

Why would someone give away their “stuff” to a charity? 17 FMV in Estate Pay tax on the sale of the asset May not produce adequate income Expense to maintain asset Managing the asset

53

What about “basis”? 17

54

You Sell the stock You Give the stock away during your lifetime The stock is Transferred at your death Intel, Inc. Basis - $1,000 FMV - $10,000 12

55

You Sell the stock You Give the stock away during your lifetime The stock is Transferred at your death Intel, Inc. Basis - $1,000 FMV - $10,000

56

Bill (58) and Barb (56) Florida property - FMV @ $5,000,000 Basis @ $500,000 Sale - 15% (2012) Capital Gains Tax on $4.5 million or $675,000

and Barb (56) Florida property - $5,000,000 $500,000 Sale - 15% (2012) Capital Gains Tax on $4.5 million or $675,000 ")

57

In addition to the Capital Gains Tax, what are some other potential financial issues that Bill and Barb might be concerned about?

58

Gift Charitable Remainder Trust Mom and Dad Low Basis “Stuff” Low Income “Stuff” “Stuff” FET Trustee(s) Receives Income Tax Deduction Sell Asset(s) Pays Income Pays No Tax Wealth Replacement Trust - Life Insurance - Mom & Dad CRT 18

Receives Income Tax Deduction Sell Asset(s) Pays Income Pays No Tax Wealth Replacement Trust - Life Insurance - Mom & Dad CRT 18")

59

How Does a CRT Work? 19 Competent attorney Form your own qualified charity or foundation Name Trustee(s) Gift assets (unlimited amount) Take tax deduction

Gift assets (unlimited amount) Take tax deduction.")

60

How Does a CRT Work? 19 CRT sells asset CRT pays no tax! CRT pays life income to grantors @5% - 8% (monthly / annually) Income taxable to recipient Wealth Replacement Trust (ILIT)

Income taxable to recipient Wealth Replacement Trust (ILIT).")

61

How Does a CRT Work? 19 Trust applies for life insurance (replace lost inheritance) Mom / Dad make $$ gift to ILIT for the benefit of kids - $13,000 maximum per year CRT terminates income to Mom / Dad at last death Heirs receive ILIT proceeds

Mom / Dad make $$ gift to ILIT for the benefit of kids - $13,000 maximum per year CRT terminates income to Mom / Dad at last death Heirs receive ILIT proceeds.")

62

Two Types of CRT Pay-out 20 Unitrust (CRUT) - $70,000 / $98,000 Annuity Trust (CRAT) - $70,000 / $70,000

- $70,000 / $98,000 Annuity Trust (CRAT) - $70,000 / $70,000")

63

2423

64

25 Testamentary Trust An absolute must for parents (single or a couple) who have minor children Questions: Would a life insurance company pay life proceeds to a minor(s)? Would a court allow money to be paid to a minor(s)

.")

65

25 Testamentary Trust An absolute must for parents (single or a couple) who have minor children How can parents be assured of have their life insurance proceeds (and other assets) pass properly to their minor children? Testamentary Trust attached to a Will with a designated Guardian(s)

.")

67

Estate Planning Techniques: Gifts, Trusts and Life Insurance Jerry Rhinehart Panama City, FL jerhinehart@comcast.net

Similar presentations

– until 2003 why? Rates range from.>")

why? Rates range from 18% to 40% ->")

1 Estate Planning for Financial Planners Chapter 8: Trusts.>")