Download presentation

Presentation is loading. Please wait.

1

Finnair Group Interim Report January 1 - June 30, 2003

2

Industry faced tough times Effects of Iraq war and SARS even bigger than 911 Economic situation still weak Tough competition Cost cutting resulted in lay-offs and new structures Losses for industry financiers

3

Finnair Q2/2003 8,0 %-unit loss in passenger load factors primarily because of SARS epidemic Business class down 18,1 % Pressure on yields 160 MEUR cost cutting programme proceeds as planned Strong financial position, net debt close to nil

4

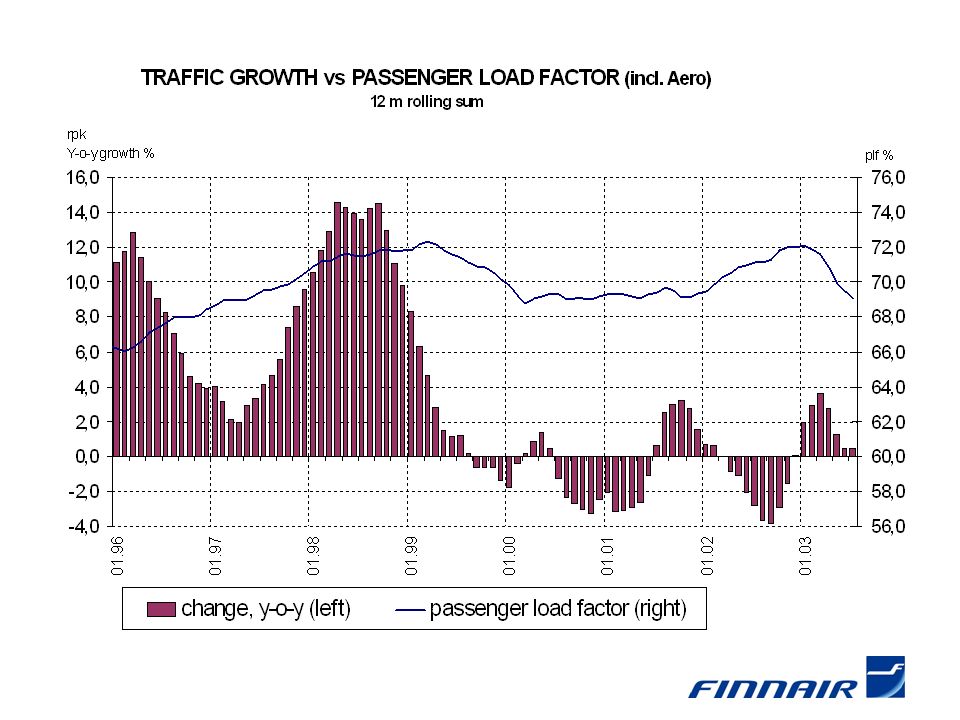

AEA and Finnair demand Scheduled Traffic Total traffic (RPK) Year-on-year change AEA: Association of European Airlines

Year-on-year change AEA: Association of European Airlines")

5

Ups... Operating expenses -5.7 % Unit costs -2.1 % Staff costs -4.4%, at the end of June 877 employees less than year before Strong financial position Considerable savings also on other costs, except for...

6

…and Downs...traffic and authority charges Turnover -14.2 %, Passenger load factor -8 %-unit, Asia -28.2 %- unit despite of severe capacity cuts Negative trend in business class demand and price competition dropped yield by 4.4 % Two-day illegal industrial action in June

7

Finnair Asian demand vs. AEA AEA: Association of European Airlines

8

MEUR 1999 2000 EBIT per quarter 2001 2002 2003

9

MEUR 1999 2000 Change in EBIT per quarter Excluding capital gains from asset disposals 2001 2002 2003

10

Both yield and unit costs down % 2002 2003

11

Leisure traffic Leisure Flights and Suntours Ltd Overall demand still down, might lead to over capacity Market leader Aurinkomatkat-Suntours further strengthened its position Finnair Leisure Flights a clear market leader Q2 capacity down 8.3% => turnover down 12.8 % Weakened profitability Yields -0.5 % Customer satisfaction remains good

12

Finnair Cargo Capacity cuts and weak global economy resulted in decreasing revenues Cargo tonnes carried (Q2) -7.3 % Cuts in chartered cargo capacity Tougher price competition particularly on North Atlantic cargo markets Negative result

-7.3 % Cuts in chartered cargo capacity Tougher price competition particularly on North Atlantic cargo markets Negative result")

13

Aviation Services Aircraft maintenance services, ground handling and catering Turnover down 11.1% due to remarkably decreased volumes and price levels Successful adaptation of operating expenses, increased profitability Ground handling operations at most domestic airports outsourced FinnHandling AB set up at Stockhom Arlanda Finnair Catering Oy has transferred its wine wholesale operations to new SkyCellar Oy of which Finnair Catering Oy owns 19.9%

14

Travel services SMT, Area, Amadeus Finland, Estravel Turnover down by 19.9.% due to weak economic situation and declining yields Result halved Management and transaction fees established As of 1 September 2003 no commissions paid for Finnair tickets in Finland

15

Liquidity has remained strong

16

Net debt close to nil June 30, 2003 Liquid funds € 299 mill. Loan facilities € 219 mill.

17

Strong balance sheet, big buffer Equity ratio and gearing %

18

In 2003 eight additional A320 series aircraft, total of 25 by the end of the year In 2004 orders for one A320, one A319 and two leased A320 series aircraft MD80 aircraft operations continue for the time being Whole year investments approximately 80 MEUR Actively implemented fleet strategy

19

Last DC-9 flight in July European jet flights in coming years with Airbus A320 series aircraft, domestic operations with MD80s Huge savings from fleet commonality Positive impact on eco-efficiency DC-9 operations in history

20

Strategy remains unchanged Cost efficiency vs. competitors Competitive edge from distinct, superior product Partnerships/alliances Growth from Asia, Baltic Sea region and Scandinavia Sustainable, profitable growth, focus on core business and more flexibility through structural changes

21

160 MEUR cost-cutting programme proceeds on time Group unit costs -15% by 2005 Permanent changes in cost and operating structure Main focus on fixed costs Share of personnel costs over 60 million euros 1200 cut in manpower over two years Structural adjustments bring new flexibility and savings Increased efficiency and productivity through fleet renewal

22

At the end of June 877 employees less than year before

23

Nordic Airlink Finnair acquires 85% of shares New low-cost airline Nordic Airlink expands and deepens operations in Scandinavia Five MD-80 aircraft in fleet breeds synergy Competitive cost structure Turnover MSEK 240 (25.6 MEUR), approx. 200 000 passengers in 2003 Operations on mainly busy routes with monopoly at work in terms of services and price

24

Short-term outlook Demand slowly picking up. Global economy still weak. Cost cutting proceeding, but full year result expected to be a clear loss Finnair introduces totally new price concepts New growth in Scandinavia through airline acquisition Strong expansion in Asia continues Aero Airlines prepared to expand into Finnish domestic traffic

25

Appendices

26

Q2/2003 in short: Operating loss excl. capital gains EUR 9,9 million Q2/2003 Q2/2002 Turnover, mill.€366,1426,9 EBITDAR38,976,6 EBIT-5,530,2 - EBIT excl. capital gains-9,929,4 Pre tax profit-6,427,8 Capital gains4,30,8

27

Passenger load factor and yield decreased during the second quarter of 2003 Q2/2003H1/2003 Demand (RPK)- 15,4 %-3,3 % Capacity (ASK)- 4,8 %+3,4 % Passenger load factor- 8,0 %-points-4,7 %-points Yield (EUR/RTK) - 4,4 %- 7,0 % Unit costs (EUR/ATK) - 2,1 %- 2,6 %

- 15,4 %-3,3 % Capacity (ASK)- 4,8 %+3,4 % Passenger load factor- 8,0 %-points-4,7 %-points Yield (EUR/RTK) - 4,4 %- 7,0 % Unit costs (EUR/ATK) - 2,1 %- 2,6 %")

28

Development of Group business units Operating loss/profit, EBIT excl. capital gains

29

Business and tourist class volumes International scheduled traffic Business class: Finnair + Aero Q3/2001 -16.2% Q4/2001 -18.6 % Q1/2002 -18.7 % Q2/2002 - 6.9 % Q3/2002 - 4.1 % Q4/2002 - 0.8 % Q1/2003 - 4.3 % Q2/2003 -18,1%

30

Iraq war and SARS epidemic have also decreased European volumes due to gateway travel through Helsinki

31

EBITDAR, without capital gains Mill. EUR

32

Investments financed with cash flow from operations Estimated investments 2003 about 80 million euros Mill. EUR

33

Operating lease liabilities of aircraft have increased in line with the strategy Flexibility, competitive cost, residual risk management At the end of June 2003 all aircraft leases are operating leases. If the lease liability inherent in an operating lease would be capitalized using the industry standard method (= annual lease payments x 7), the adjusted gearing would have been approximately 100% at the end of June 2003.

, the adjusted gearing would have been approximately 100% at the end of June")

35

Jet fuel price development USD/Tonne and EUR/Tonne

36

ROE and ROCE rolling 12 months %

37

Superiority of product Direct to 30 destinations in the world –no time-consuming transfers at crowded airports Best schedules –morning-evening concept One of the most punctual in Europe with least cancellations Top class service in Europe oneworld - alliance with best quality and best coverage – good connections to 135 countries New aircraft in European traffic and renewed Business Class in long-haul traffic

38

Finnair Financial Targets ”Sustainable value creation” Operating profit (EBIT) EBIT margin at least 6% => 110-120 mill. € in the coming few years EBITDAR EBITDAR margin at least 17% => over 300 mill. € in the coming few years Economic profit To create positive value over pretax WACC of 10% not later than 2004 Pay out ratioMinimum one third of the EPS Gearing Net Debt to Equity max 0.6 Equity ratioEquity to Balance Sheet total more than 30% Total Shareholder Return (TSR) On average 15% annual TSR => to double the value for shareholders in five years Market CapPrice to Book minimum target 1.0

On average 15% annual TSR => to double the value for shareholders in five years Market CapPrice to Book minimum target 1.0.")

39

Finnair’s financial targets description of scorecards

40

www.finnair.com Finnair Group Investor Relations email: investor.relations@finnair.com tel: +358-9-818 4951 fax: +358-9-818 4092

Similar presentations